- Non-food Packaging

- Print Label Market

Print Label Market Size, Share, and Growth Forecast, 2026 - 2033

Print Label Market by Print Process (Offset Lithography, Gravure, Others), Label Format (Wet-Glue Labels, Others), End-user Industry (Food & Beverage, Healthcare and Pharmaceuticals, Others), and Regional Analysis for 2026 – 2033

Print Label Market Size and Trends Analysis

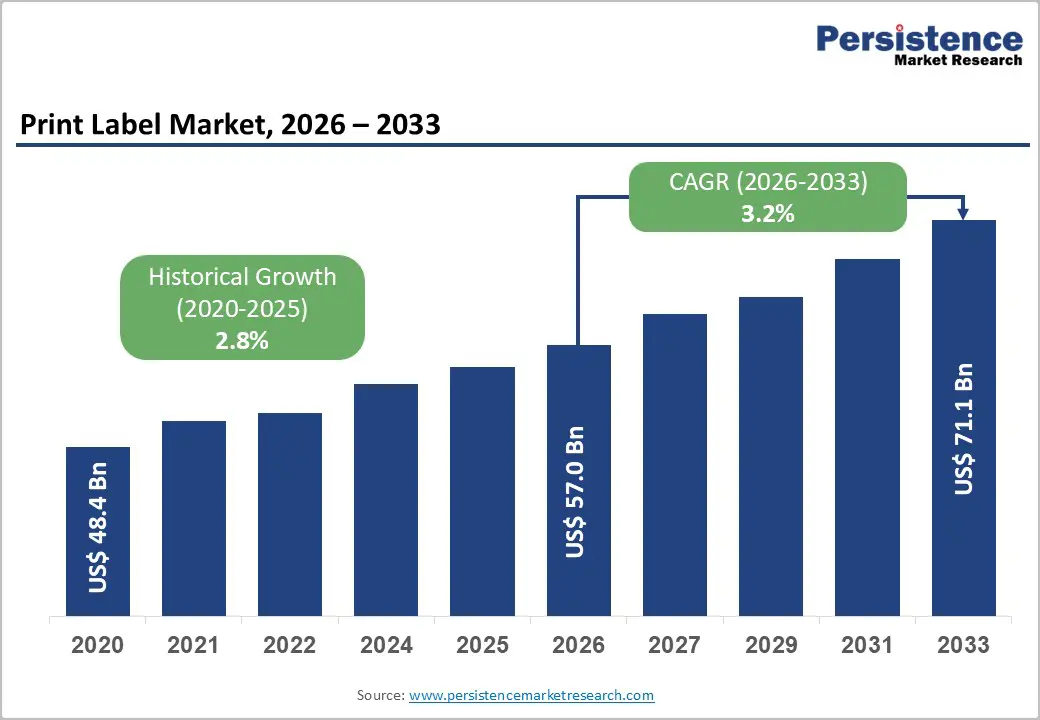

The global print label market size is likely to be valued at US$57.0 billion in 2026, and is expected to reach US$71.1 billion by 2033, growing at a CAGR of 3.2% during the forecast period from 2026 to 2033, driven by the increasing prevalence of packaged consumer goods, rising demand for brand differentiation on shelf, and growing adoption of variable-data and smart labels in logistics and e-commerce.

The growing demand for high-quality, durable print labels, especially pressure-sensitive and shrink sleeves, is driven by industries such as food & beverage and healthcare. Advances in digital inkjet printing, linerless formats, and sustainable substrates are boosting adoption by offering cost efficiency, reduced waste, and eco-regulation compliance. Print labels are also gaining recognition for their role in product identification, traceability, anti-counterfeiting, and enhancing promotional impact in modern retail and supply chains.

Key Industry Highlights:

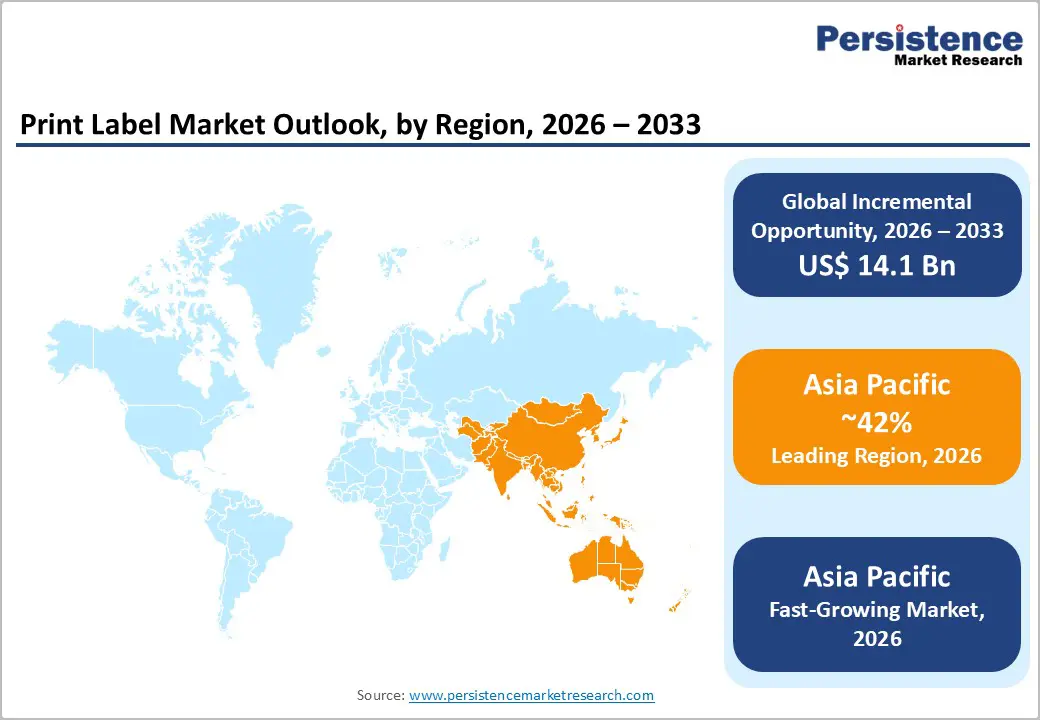

- Leading Region: Asia Pacific, anticipated to account for a 42% market share in 2026, driven by massive FMCG production, rapid e-commerce growth, and strong demand in China and India.

- Fastest-growing Region: Asia Pacific, fueled by expanding organized retail, pharmaceutical exports, and increasing variable-data labeling requirements.

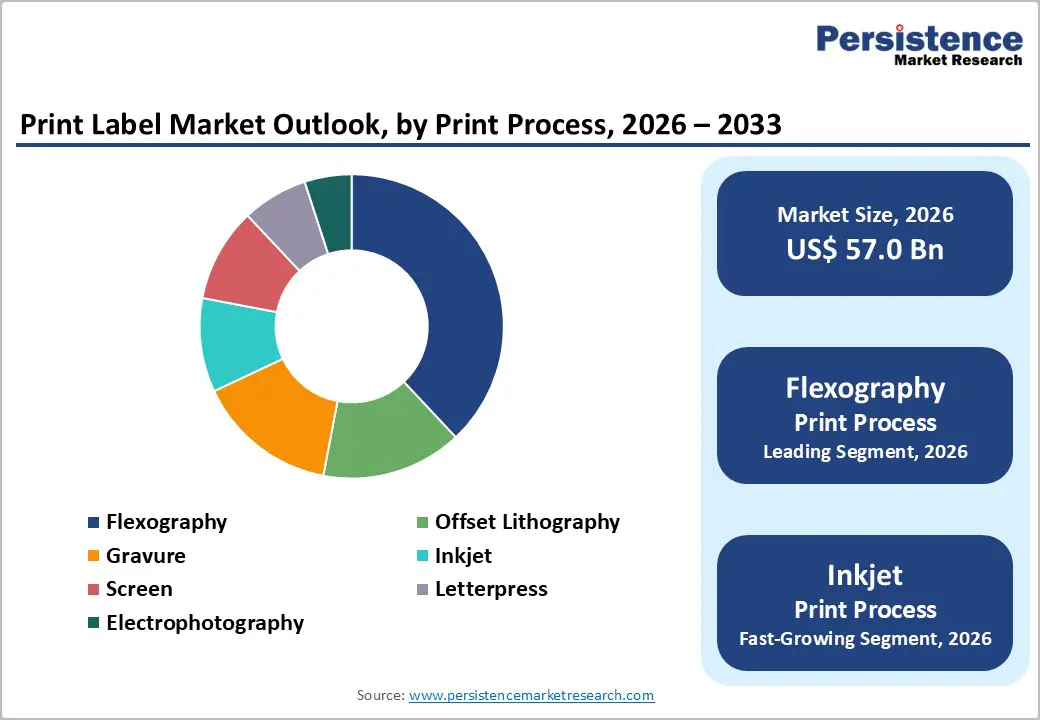

- Dominant Print Process: Flexography, to hold approximately 38% of the market share, as it remains the workhorse for high-volume label production.

- Leading Label Format: Pressure-sensitive labels, to contribute nearly 48% of the market revenue, due to their versatility and ease of application.

- Leading End-user Industry: Food, to account for over 32% of the market revenue, due to highest volume of packaged goods.

| Key Insights | Details |

|---|---|

| Print Label Market Size (2026E) | US$57.0 Bn |

| Market Value Forecast (2033F) | US$71.1 Bn |

| Projected Growth CAGR (2026-2033) | 3.2% |

| Historical Market Growth (2020-2025) | 2.8% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growth Analysis – Expansion of Organized Retail and E-commerce Packaging

Rapid expansion in organized retail and e?commerce across India is significantly amplifying demand for printed labels. As stores multiply and online shopping grows, consistent, high-quality labelling becomes essential for pricing, SKU management, compliance, and branding. As products move from warehouses to homes at scale, this surge drives demand for durable, printed packaging and labels that include barcodes, handling instructions, and traceability codes, supporting supply chain efficiency and customer experience.

The trend toward multi?channel retailing increases SKU proliferation and packaging variants, compelling manufacturers and brands to invest in sophisticated label printing solutions. In a competitive landscape where shelf appeal and brand differentiation influence buying decisions, printed labels serve not only functional purposes such as logistics and regulatory compliance but also enhance brand visibility across digital and physical touchpoints. Growth in organized retail formats and online marketplaces thus creates structural demand for print label technologies that can scale with product complexity and volume, reinforcing this segment as a key driver of the broader print label market.

Regulatory Traceability and Brand Premiumization

Government?mandated traceability regimes and rising emphasis on authentic branding are catalysing demand for sophisticated print labels throughout supply chains. Indian regulations under the Food Safety and Standards Authority of India (FSSAI) require pre?packaged foods to carry clear batch/lot numbers, manufacturing and expiry dates, and manufacturer details to enable traceability back to the point of origin, supporting compliance and public safety. Simultaneously, Ministry of Agriculture directives now mandate QR codes with unique identifiers on certain agro?input packaging to ensure product authenticity and quality information is accessible, creating greater reliance on printed labelling infrastructure. These requirements heighten the functional necessity for durable, accurate print labels that support both regulatory traceability and logistical accountability across complex distribution networks.

Brand premiumization further reinforces print label market expansion. As brands invest in premium positioning to command higher value segments, labels become a strategic touchpoint that communicates quality, certifications, and authenticity elements that drive consumer trust and willingness to pay more. With regulatory bodies enforcing transparent disclosures and standardized markings, brands are compelled to use higher?quality printed labels to convey compliance and differentiate themselves in crowded markets. Statutory traceability and quality disclosure frameworks thus intersect with brand?led premiumization strategies, driving sustained demand for advanced print label solutions that uphold both compliance and aspirational brand narratives.

Barrier Analysis – Raw Material Price Volatility and Supply Disruptions

Raw material price volatility and supply disruptions present a tangible restraint on the print label market’s growth trajectory. Price movements in key inputs such as plastics resins and paper pulp directly influence cost structures for label manufacturers. For instance, India’s plastic raw materials market showed a 20?% rise in prices for essential feedstocks like PVC, polyethylene, and polypropylene due to import dependence and global demand pressures, leading to a cost burden on domestic processors. Concurrently, regulatory changes affecting duty and taxation have made primary materials like paper and paperboard more expensive for converters; a GST hike raised the tax on paper from 12?% to 18?%, which industry bodies cautioned would push up prices for packaging inputs and constrain working capital for MSMEs engaged in printing and packaging. These input cost pressures reduce margin stability for print label producers and complicate pricing negotiations with brand owners.

Disruptions in supply chains compound this volatility. Import dependency for petrochemical?derived polymers and periodic logistical bottlenecks mean that raw material availability can fluctuate, forcing label converters to hold higher safety stock or accept shorter lead time fills at a premium. As many converters operate with limited working capital, unpredictable cost spikes erode financial planning accuracy and elevate product lead times. This environment dampens investment confidence in capacity expansion for advanced label technologies and narrows the window for competitive pricing, thereby acting as a restraint on the broader print label market’s expansion.

Sustainability Mandates and Format Restrictions

Retailers and regulators are increasingly prioritizing sustainability in packaging, imposing mandates that directly impact print label requirements. Environmental norms now push brands to reduce non?recyclable materials and switch to eco?friendly substrates. This shift means traditional adhesive films and plastic?based labels are being replaced by recyclable paper labels, water?soluble adhesives, or compostable alternatives. These changes can slow production cycles and raise initial costs for converters as they test, qualify, and adopt new materials that meet sustainability standards. Retailers are setting their own restrictions on packaging formats, limiting packaging mass or banning certain label types in sustainable assortments, which forces manufacturers to rethink label placement, size, and composition to align with store compliance while still providing necessary product information.

In practice, meeting sustainability mandates often requires investment in new printing technologies and supply chain adjustments. Converters must ensure inks, adhesives, and substrates are compatible with recycling streams or composting processes, which can involve trial runs and supplier qualification. Format restrictions from retailers can also constrain design flexibility, requiring tighter integration between brand design teams and label printers to maintain legibility and brand identity within smaller or altered label footprints.

Opportunity Analysis – Growth in Smart Labels and Sustainable Substrates

Emerging smart labels and sustainable substrates are creating a compelling opportunity for the print label market by aligning product identification with environmental and digital trends. Indian regulation under the Plastic Waste Management (Amendment) Rules, 2025, mandates that from 1?July?2025, all plastic packaging must carry a barcode or QR code, enabling traceability and compliance tracking throughout the product lifecycle, which directly increases demand for printed labels with these capabilities. Smart labels incorporating QR codes, NFC, or RFID support not only regulatory traceability but also interactive consumer engagement features such as authenticity verification and product information access, making them valuable across food, pharmaceutical, and retail segments. This regulatory push embeds label printing deeper into compliance workflows for brand owners and packaging converters.

Sustainable substrates offer another growth vector. As brands and regulators prioritize recyclability and reduced environmental impact, recyclable paper liners, compostable adhesives, and eco?friendly films are gaining traction in label production. Government?level consultations on sustainable packaging, such as those hosted by FSSAI, underscore the focus on recyclable materials and sustainability credentials in packaging design. These substrates allow print label producers to offer differentiated, eco?compliant solutions that meet both regulatory demands and consumer expectations, creating a competitive edge.

Expansion in E-commerce and Direct-to-Consumer Labeling

Rapid expansion of e?commerce and direct?to?consumer (D2C) business models is reshaping how products are packaged and labelled, creating significant opportunities for the print label market. Online channels require comprehensive product information, brand reinforcement, and logistical data on packaging to support fulfilment and returns processes. Labels serve as the primary interface of this information, carrying SKU identifiers, courier details, handling instructions, and customer?facing messaging. In D2C models, where brands handle fulfilment and customer interaction directly, labels play an elevated role in reinforcing brand identity and delivering tailored messaging at the point of unboxing. This increases demand for customized, small?batch print label runs that can be integrated seamlessly into variable packaging formats.

E?commerce’s reliance on multi?stage logistics and diversified delivery partners also drives demand for labels that offer durability and scanability throughout transit. Unlike traditional retail, where product packaging is final after shelving, online fulfilment exposes packages to more handling and environmental conditions, placing a premium on high?quality printed labels that remain legible and adhesive from warehouse to doorstep. This shift encourages investments in advanced printing technologies and flexible materials, enabling label converters to offer solutions that meet the specific requirements of e?commerce logistics.

Category-wise Analysis

Print Process Insights

Flexography is anticipated to dominate, accounting for approximately 38% of the market share in 2026, fueled by its versatility, high-speed production capabilities, and cost-efficiency for large-volume runs. It supports a wide range of substrates, including paper, plastics, and films, making it suitable for diverse packaging applications across food, beverage, pharmaceuticals, and consumer goods. The process allows quick plate changes, short setup times, and vibrant, consistent print quality, which are essential for brand differentiation and regulatory compliance. Tri-Flex Label Corp. is a pressure-sensitive label converter based in Long Island, New York. Tri-Flex regularly employs flexographic printing presses for producing consumer packaged goods labels across food, beverage, health, and other retail products due to the technology’s high speed, precision, and cost-effective large-volume output.

Inkjet is likely to be the fastest-growing print process, with its digital nature and flexibility for variable data. It enables on-demand, short-run production with minimal setup, reducing waste and inventory costs for converters and brands. Inkjet systems can print high-resolution graphics, barcodes, and unique identifiers without physical plates, allowing rapid changes in designs, promotions, or compliance information. This adaptability suits personalized packaging and e-commerce fulfilment, where SKU proliferation and customized branding require agile output. Kolibri Labels BV, the Netherlands-based converter that installed an EFI Jetrion 4830 inkjet system to meet customer demand for high-quality, full-color labels with quick turnaround times and variable data capability. This deployment allowed Kolibri to expand its service offering and deliver more attractive, customized labels across sectors such as cosmetics, food, and chemical products, demonstrating how inkjet supports flexible, short-run production while enhancing print quality.

Label Format Insights

Pressure-sensitive labels are expected to dominate the market, contributing nearly 48% of revenue in 2026, due to their ease of application, versatility, and compatibility with automated packaging lines. These labels require no heat, water, or solvent for activation, enabling faster production speeds and reduced operational complexity for manufacturers. They adhere effectively to a wide range of surfaces, including glass, plastic, metal, and paper, making them suitable for food, beverage, pharmaceuticals, personal care, and logistics applications. Avery Dennison Corporation is an American multinational manufacturer and distributor of pressure-sensitive adhesive materials (such as self-adhesive labels), apparel branding labels and tags, RFID inlays, and specialty medical products.

Linerless labels are likely to be the fastest-growing label format, driven by their efficiency and sustainability advantages. Without a backing liner, they eliminate up to 50–70% of label waste, reducing disposal costs and environmental impact for manufacturers and end users. Their continuous roll format also increases the number of labels per roll, extending run lengths and lowering downtime for label applicators. Linerless technology is especially attractive in logistics and retail environments where frequent labeling and scanning occur, supporting higher throughput and reduced material handling. HERMA GmbH, a German label materials and systems manufacturer that has developed its HERMA InNo-Liner linerless labelling technology. HERMA’s system eliminates traditional backing paper on shipping and logistics labels, reducing waste and increasing the number of labels per roll while maintaining reliable adhesion and automated application performance.

Regional Insights

North America High Visible Packaging Market Trends

North America driven by the region’s advanced retail and supply-chain infrastructure, strong brand compliance focus, and high public awareness of traceability benefits. Distribution systems in the U.S. and Canada provide extensive support for print label programs, ensuring wide accessibility across pressure-sensitive, food, and flexography populations. Increasing demand for variable-data, convenient, and easy-to-apply forms is further accelerating adoption, as these formats improve traceability and reduce barriers associated with manual labeling.

Innovation in print label technology, including stable linerless, improved digital inkjet delivery, and targeted e-commerce enhancement, is attracting significant investment from both public and private sectors. Government initiatives and FDA/USDA campaigns continue to promote use against compliance risks, sustainability concerns, and emerging DTC threats, creating sustained market demand. The growing focus on logistics grades and specialty uses, particularly for food and other products, is expanding the target applications for print labels.

Europe Print Label Market Trends

The growth of Europe is increasing awareness of sustainability and traceability benefits, strong regulatory systems, and government-led circular economy programs. Countries such as Germany, France, the United Kingdom, and Italy have well-established packaging and retail frameworks that support routine print label use and encourage adoption of innovative format delivery methods, including linerless and recyclable substrates. These high-compliance formulations are particularly appealing for food populations, regulation-conscious brand owners, and logistics users, improving traceability and coverage rates.

Technological advancements in print label development, such as enhanced digital printing, application-targeted delivery, and improved bioplastic grades, are further boosting market potential. European authorities are increasingly supporting research and trials for labels against both routine and specialized needs, strengthening market confidence. The growing emphasis on convenient, eco-friendly options is aligned with the region’s focus on preventive plastic reduction and supply-chain transparency. Public awareness campaigns and promotion drives are expanding reach in both food & beverage and logistics segments, while suppliers are investing in sustainable materials and novel variants to increase efficacy.

Asia Pacific Print Label Market Trends

Asia Pacific is expected to dominate and to be the fastest growing market, capturing the 42% of the revenue in 2026, driven by rising organized retail awareness, increasing government initiatives, and expanding application programs across the region. Countries such as China, India, Indonesia, and Thailand are actively promoting label campaigns to address FMCG growth and emerging traceability needs. Print labels are particularly attractive in these regions due to their cost-effective administration, ease of adoption, and suitability for large-scale food & beverage and logistics drives in both urban and semi-urban populations.

Technological advancements are supporting the development of stable, effective, and easy-to-apply print labels, which can withstand challenging supply-chain conditions and minimize compliance dependence. These innovations are critical for reaching domestic brand owners and improving overall product coverage. Growing demand for pressure-sensitive, food, and flexography applications is contributing to market expansion. Public-private partnerships, increased retail expenditure, and rising investments in label research and production capacity are further accelerating growth. The convenience of label delivery, combined with improved traceability and reduced risk of counterfeiting, positions it as a preferred choice.

Competitive Landscape

The global print label market is characterized by intense competition between well-established packaging converters and agile digital-print specialists seeking technological differentiation. In North America and Europe, multinational leaders such as CCL Industries and Avery Dennison Corporation maintain strong market positions through vertically integrated operations, broad geographic distribution, and deep relationships with multinational brand owners. Their sustained investment in research and development supports innovation in pressure-sensitive constructions, linerless technologies, smart labels, and sustainable material science. These capabilities enable them to address regulatory compliance, traceability, and premium branding requirements across food, beverage, pharmaceutical, and personal care sectors.

In Asia Pacific, regional manufacturers compete by offering cost-efficient production models and scalable solutions tailored to fast-growing domestic markets. Competitive pricing, flexible batch production, and proximity to manufacturing hubs enhance accessibility for small and mid-sized brands. Pressure-sensitive label formats continue to gain traction due to faster application speeds, compatibility with automated lines, and reduced risk of adhesive waste. Strategic partnerships, technology collaborations, and acquisitions are consolidating expertise and accelerating the commercialization of advanced printing platforms.

Key Industry Developments:

- In September 2025, Avery Dennison Corporation (NYSE: AVY) unveiled several product innovations at Labelexpo 2025 in Barcelona. These solutions, focused on circularity and connectivity, improved packaging sustainability and digital integration. They enhanced recycling and reuse capabilities, boosted shelf appeal, and elevated functionality and performance. Advanced labeling technologies also enabled better supply chain transparency, improving traceability and operational efficiency.

Companies Covered in Print Label Market

- CCL Industries

- Avery Dennison Corporation

- Multi-Color Corporation

- 3M

- Brady Worldwide, Inc.

- Mondi

- Amcor plc

- Taylor Corporation

Frequently Asked Questions

The global print label market is projected to reach US$57.0 billion in 2026.

Growth in modern retail formats and online marketplaces is significantly increasing the need for high-quality, durable, and information-rich labels.

The print label market is poised to witness a CAGR of 3.2% from 2026 to 2033.

Increasing integration of QR codes, RFID, NFC, and variable data printing is creating opportunities for value-added label solutions.

CCL Industries, Avery Dennison Corporation, Multi-Color Corporation, 3M, and Mondi are the key players.