- Advanced Materials

- 3D Printing Photopolymers Market

3D Printing Photopolymers Market Size, Share, Trends, Growth, Regional Forecasts, 2026 to 2033

3D Printing Photopolymers Market by Material (Monomers, Polymers, Additives, Oligomers), End-User (Automotive, Healthcare, Consumer Goods, Aerospace & Defense), Application (Surgical Models, Wearable Biosensors, Implants), and Regional Analysis for 2026-2033

3D Printing Photopolymers Market Share and Trends Analysis

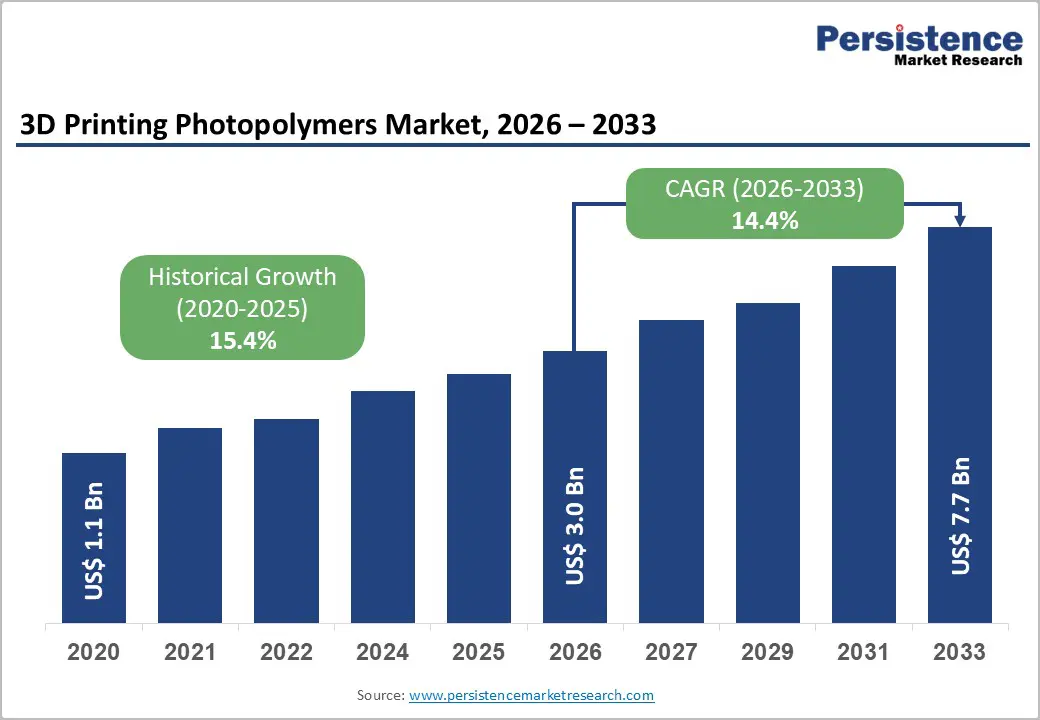

The global 3D printing photopolymers market size is likely to be valued at US$ 3.0 billion in 2026, and is projected to reach US$ 7.7 billion by 2033, growing at a CAGR of 14.4% during the forecast period 2026−2033.

The market's sustained expansion is underpinned by accelerating adoption of stereolithography (SLA), digital light processing (DLP), and photopolymer jetting (PolyJet) technologies across aerospace, automotive, healthcare, and consumer electronics sectors. Increasing demand for high-resolution, patient-specific medical devices and dental prosthetics, combined with rapid expansion of on-demand manufacturing ecosystems, constitutes a primary growth catalyst.

Key Industry Highlights

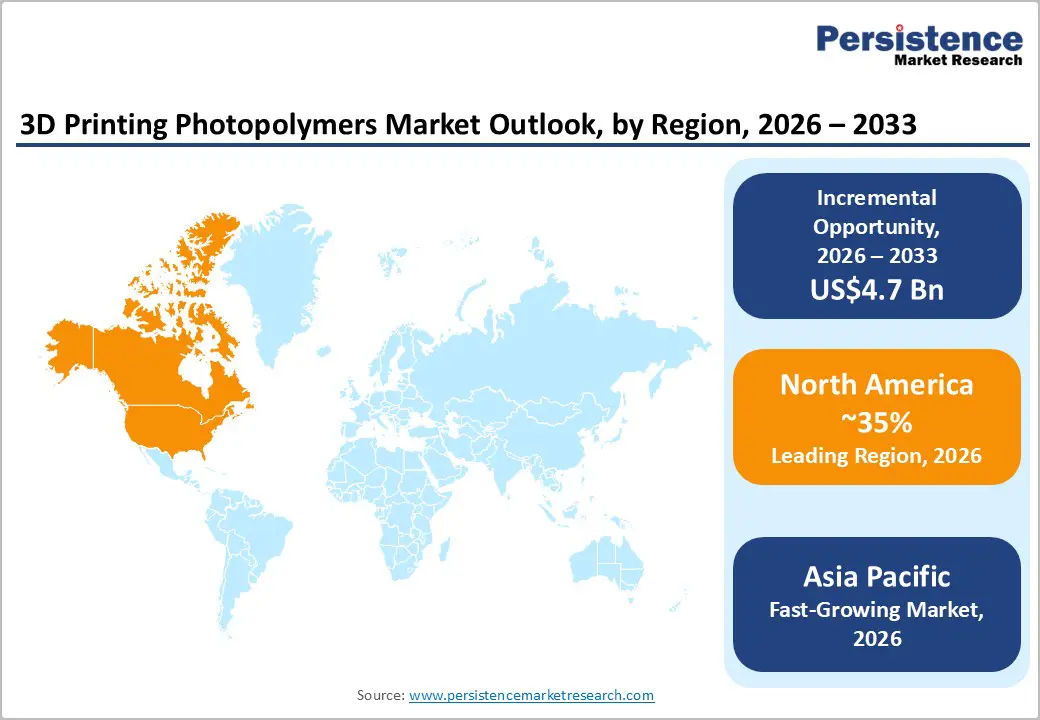

- Dominant Region: North America is expected to command about 35% market share in 2026, supported by its well-established additive manufacturing ecosystem and strong industrial adoption.

- Fastest-growing Region: The Asia Pacific market is poised to be the fastest-growing during the forecast period, due to the rapid industrialization and increasing adoption of advanced manufacturing technologies.

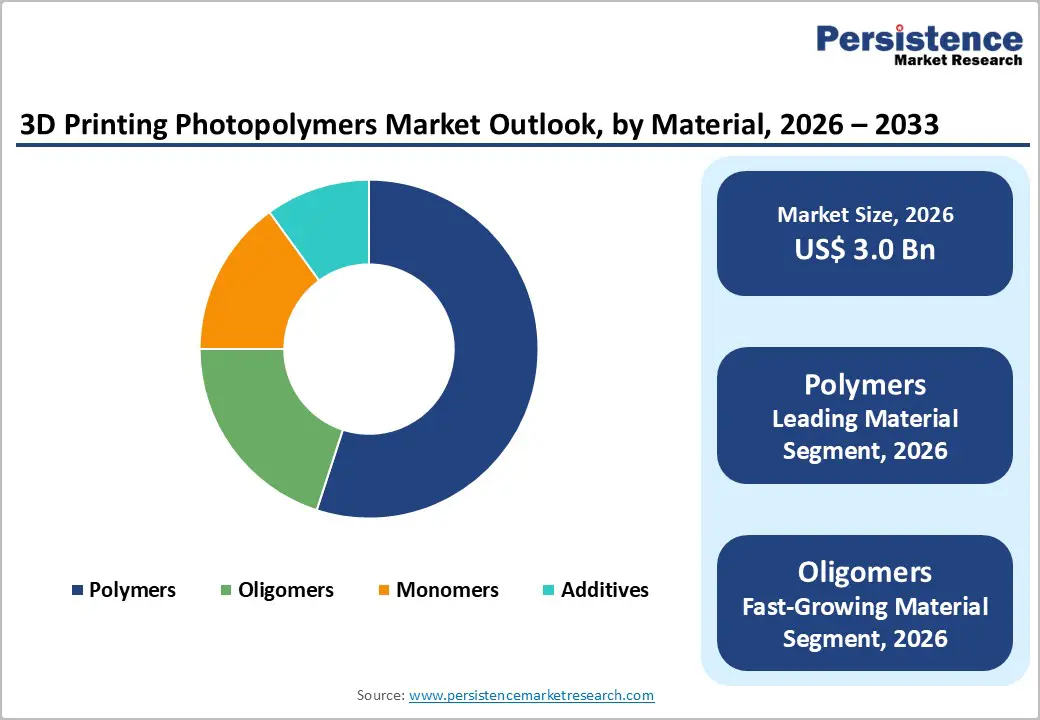

- Leading & Fastest-growing Material: Polymers currently dominate the material segment, commanding approximately 55% of total market revenue, while oligomers are likely to be the fastest-growing segment during the 2026-2033 forecast period.

- Leading & Fastest-growing End-user: Healthcare represents the dominant end-user segment, capturing approximately 45% of market revenue share in 2026, whereas aerospace & defense is expected to be the fastest-growing segment over the 2026-2033 forecast period.

| Key Insights | Details |

|---|---|

|

3D Printing Photopolymers Market Size (2026E) |

US$ 3.0 Bn |

|

Market Value Forecast (2033F) |

US$ 7.7 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

14.4% |

|

Historical Market Growth (CAGR 2020 to 2025) |

15.4% |

DRO Analysis

Rapid Proliferation of Additive Manufacturing in Industrial Applications

The global additive manufacturing (AM) industry is experiencing rapid growth, driven by increasing adoption of photopolymer-based processes such as SLA and PolyJet in sectors including aerospace, automotive, and electronics tooling. Companies are continuously developing advanced photopolymer formulations to improve part strength, surface finish, and production speed, enabling more complex and precise components. Industrial users are integrating these processes into their production lines to reduce lead times and enhance design flexibility. This focus on high-performance materials is also opening new opportunities for functional prototyping and low-volume manufacturing, allowing firms to test and optimize designs more efficiently before committing to large-scale production.

Institutional investment is significantly accelerating these advancements, supporting both material innovation and process optimization. Government programs and research initiatives are funding projects aimed at expanding the practical applications of photopolymer-based components, including in defense, healthcare, and industrial manufacturing. These strategic investments are helping to bridge the gap between laboratory research and commercial adoption, ensuring that cutting-edge technologies reach the market more quickly. The AM industry is positioned to expand its market reach, enhance production efficiency, and create new value for manufacturers by enabling faster, more precise, and highly customized production solutions.

Technological Advancement in High-Performance Photopolymer Formulations

Breakthroughs in material science are continuously redefining the performance of photopolymers, enabling manufacturers to produce functional parts with higher strength, thermal stability, and durability. New formulations incorporating ceramic-filled compounds, carbon fiber reinforcement, and thermally stable acrylate or epoxy blends are expanding the capabilities of additive manufacturing beyond conventional prototyping. Leading product lines such as BASF’s Ultracur3D and DSM Somos photopolymer portfolio demonstrate how research and development efforts are translating into commercially viable, performance-grade materials. These innovations are allowing industries to adopt photopolymer-based processes for critical applications in aerospace, automotive, and industrial tooling, where precision, reliability, and material performance are essential.

The adoption of advanced photopolymer materials is driving a structural shift in the AM market, moving from prototyping-only use to production of end-use components. This transition is opening new opportunities for manufacturers to integrate additive manufacturing into their core production strategies, creating more value from faster design iterations and reduced material waste. Material innovation is also enhancing the economic feasibility of producing small to medium batch runs and highly customized parts. As photopolymer chemistries continue improving, industries are expanding the total addressable market for additive manufacturing, enabling applications that were previously considered impractical and positioning AM as a central component of modern manufacturing strategies.

Regulatory Complexity and Post-Processing Requirements

Photopolymer-based manufacturing is requiring more complex post-processing steps, including ultraviolet (UV) post-curing, surface washing, and secondary finishing, which are increasing both operational complexity and capital investment. Manufacturers are continuously optimizing these processes to reduce labor intensity and improve part consistency, but the additional steps remain a critical consideration when integrating photopolymer technologies into production lines. The need for specialized equipment and controlled environments is driving companies to carefully balance efficiency with quality, especially when producing components with tight tolerances or intricate geometries. Process improvements and automation are gradually reducing cycle times and operational costs, but the inherent complexity of photopolymer workflows is shaping investment decisions and production planning across industries.

Regulatory and environmental requirements are also influencing the development and adoption of photopolymer materials. For biomedical applications, compliance with International Organization for Standardization (ISO) 10993 biocompatibility standards and Food and Drug Administration (FDA) clearance is extending product development timelines and adding procedural rigor. At the same time, environmental scrutiny over photoinitiator toxicity and hazardous waste management is increasing under the European Union (EU) Registration, Evaluation, Authorization and Restriction of Chemicals (REACH) framework and United States Environmental Protection Agency (EPA) regulations.

Constraints of Material Capabilities

One of the primary challenges restraining growth in the photopolymer 3D printing market is the limitation of available materials. Although photopolymer resins provide a wide range of properties such as strength, flexibility, and transparency, achieving the optimal balance between these characteristics and printability is a complex and ongoing task. Manufacturers are continuously working to develop resins that meet specific functional requirements for diverse applications while ensuring compatibility with different 3D printing technologies and equipment. Each formulation requires careful consideration of factors such as viscosity, curing behavior, and thermal stability, which directly influence part quality and reliability.

Additional factors including print speed, layer resolution, and post-processing needs further complicate material development and selection. Resins that perform well under one set of conditions may not deliver the same results under different printing parameters or for complex geometries. These limitations can restrict the ability of manufacturers to address highly specialized or demanding applications, slowing innovation in fields such as medical devices, aerospace components, and high-precision tooling. The market may face challenges in fully realizing its potential, as material constraints continue to influence adoption rates, production efficiency, and the development of new end-use applications.

Adoption in Electronics and Microelectronics Manufacturing

The miniaturization of consumer and industrial electronics is creating a significant opportunity for high-resolution photopolymer 3D printing. Manufacturers are exploring the direct printing of circuit substrates, microfluidic devices, and other intricate components that require precise geometries and fine feature resolution. Photopolymers with dielectric properties, thermal resistance, and mechanical stability are being developed to meet the demanding requirements of embedded electronics. These materials are enabling designers to integrate multiple functions into smaller, more compact devices, reducing assembly steps and improving overall performance.

Collaborations between material suppliers and semiconductor original equipment manufacturers (OEMs) in Japan, Taiwan, and South Korea are accelerating the qualification of electronics-grade photopolymer systems. These partnerships are streamlining testing and certification processes, allowing new materials to reach production environments more quickly. By integrating photopolymers into advanced electronics manufacturing, companies are enhancing design flexibility, enabling rapid prototyping, and shortening development cycles. This structural shift is expanding the addressable market for additive manufacturing in electronics, opening opportunities for innovative applications such as embedded passive components, high-density interconnects, and next-generation microfluidic systems, ultimately positioning photopolymer printing as a key technology in the evolution of compact, high-performance electronic devices.

Sustainable and Bio-Based Photopolymer Development

Sustainability requirements are increasingly shaping the development of photopolymer materials used in AM. Regulatory initiatives in regions such as the EU and North America are encouraging manufacturers to adopt environmentally responsible chemistries and production methods. Policies connected with the European Green Deal are guiding industries toward lower greenhouse gas emissions and more sustainable material systems. In response, researchers and material developers are creating bio based, recyclable, and low volatile organic compound (VOC) photopolymer formulations that can reduce environmental impact during manufacturing and disposal. Research is demonstrating that bio acrylate photopolymers derived from plant-based feedstocks, including levulinic acid derivatives, are achieving printing performance comparable to conventional petroleum derived materials.

Industry participants are actively investing in green material research and development to align with environmental, social, and governance (ESG) expectations and regulatory compliance. Companies such as Henkel and Arkema are expanding their sustainable photopolymer portfolios and are collaborating with manufacturing partners to accelerate commercialization. These efforts are enabling manufacturers to adopt environmentally responsible materials without compromising process efficiency or product performance. As sustainability standards continue strengthening, organizations that integrate greener photopolymer technologies will have improved access to environmentally focused procurement programs and public sector contracts.

Category-wise Analysis

Product Type Insights

Polymers currently dominate the material segment, commanding approximately 55% of total market revenue, driven by their superior mechanical properties such as strength, flexibility, and durability. These characteristics are making polymers highly suitable for producing functional components and end-use products across multiple industries. Sectors including automotive, consumer goods, and healthcare are increasingly adopting polymer-based materials to manufacture parts that require precision, structural reliability, and consistent performance. Ongoing research and development activities are continuously improving polymer formulations to meet evolving industry standards and application requirements.

Oligomers are likely to be the fastest-growing segment during the 2026-2033 forecast period. The segment serves as the fundamental building blocks of photopolymer resins, forming the structural backbone that determines the mechanical and chemical properties of the final cured material. Their composition directly influences characteristics such as rigidity, flexibility, and durability, which are critical for achieving consistent performance in additive manufacturing applications. Growing demand for customized and application-specific photopolymer formulations is driving increased focus on oligomer development. Researchers and material manufacturers are continuously advancing oligomer chemistry to create resins with improved performance capabilities.

End-user Insights

Healthcare represents the dominant end-user segment, capturing approximately 45% of market revenue share in 2026, driven by the growing use of photopolymer-based 3D printing to produce highly customized medical devices and patient-specific solutions. These materials enable manufacturers to create precise and complex components that meet individual anatomical requirements. Photopolymers provide excellent resolution and dimensional accuracy, which are essential for applications such as dental aligners, hearing aids, surgical guides, and prosthetic devices. In addition, certain photopolymer formulations demonstrate strong biocompatibility, making them suitable for applications that involve direct contact with human tissue.

Aerospace & Defense is expected to be the fastest-growing segment over the 2026-2033 forecast period, reinforced by increasing demand for lightweight materials that maintain high structural strength and durability. Components used in aircraft and defense systems must perform reliably under extreme temperatures, pressure variations, and demanding operational conditions. Photopolymers are gaining attention in this sector because they can be engineered to provide properties such as high thermal resistance, dimensional stability, and reduced weight. These characteristics help manufacturers produce complex parts with greater precision while minimizing material usage.

Regional Insights

North America 3D Printing Photopolymers Market Trends

North America is set to command a significant portion of the 3D printing photopolymers market share at approximately 35% in 2026, due to its well-established additive manufacturing ecosystem and strong industrial adoption. The United States is driving regional growth through the presence of major OEMs such as Stratasys, 3D Systems, and Carbon. These companies are supporting innovation in photopolymer materials and printing technologies while collaborating with service bureaus and manufacturing partners. End user industries including aerospace, defense, healthcare, and consumer electronics are increasingly integrating photopolymer based additive manufacturing into product development and production processes.

Regulatory institutions and research organizations are also shaping the direction of material innovation in the region. Agencies such as the U.S. FDA and the U.S. EPA are guiding safety, chemical compliance, and medical device approvals for photopolymer-based products. Research funding through the National Science Foundation is supporting collaborative projects between universities and industrial partners to develop advanced photopolymer formulations. Canada is also expanding its role through applications in aerospace maintenance, repair, and overhaul and in energy related industries. The regional market is evolving through a combination of established manufacturers and specialized material developers that are addressing niche application requirements.

Europe 3D Printing Photopolymers Market Trends

Europe is playing a major role in the global market for photopolymer 3D printing, supported by strong industrial capabilities and growing adoption of additive manufacturing across advanced sectors. Countries including Germany, the United Kingdom, France, and the Netherlands are serving as key centers of innovation and demand. Germany is leading regional activity through its highly developed automotive manufacturing ecosystem, which includes major original equipment manufacturers such as Volkswagen, BMW, and Mercedes-Benz. These companies and their supplier networks are integrating photopolymer based additive manufacturing to support prototyping, tooling development, and component testing. The United Kingdom is strengthening its position in aerospace and healthcare manufacturing through collaborative research environments, particularly through the work of the Manufacturing Technology Centre.

France is also expanding its industrial use of photopolymers through leading defense and aeronautics companies such as Thales and Safran. Regulatory alignment across the region is guiding the development and commercialization of photopolymer materials. Policies including the EU Medical Device Regulation (MDR) and regulatory oversight from the European Chemicals Agency under the REACH framework are encouraging standardized safety and chemical compliance. Strategic initiatives from the European Union are strengthening regional manufacturing independence. Programs such as the European Chips Act and broader industrial strategy efforts are encouraging the localization of advanced manufacturing capabilities.

Asia Pacific 3D Printing Photopolymers Market Trends

Asia Pacific is anticipated to emerge as the fastest-growing 3D printing photopolymers market, supported by rapid industrialization and increasing adoption of advanced manufacturing technologies. Major economies including China, Japan, India, and South Korea are acting as key growth drivers. China is strengthening its position through large scale manufacturing capacity and strong government support for industrial modernization. National initiatives such as Made in China 2025 and the Fourteenth Five Year Plan are encouraging investment in additive manufacturing and advanced materials. Domestic original equipment manufacturers are also expanding their presence, including companies such as Bambu Lab, CreatBot, and UnionTech. These firms are developing photopolymer compatible printing systems, which is increasing demand for specialized resins across industrial production environments.

Japan is continuing to demonstrate technological leadership in precision manufacturing, particularly in electronics and automotive applications that require highly reliable materials. Companies such as Mitsui Chemicals and DIC Corporation are advancing photopolymer formulations designed for high performance applications. India is also expanding its additive manufacturing ecosystem through national policy initiatives that are supporting domestic technology adoption and industrial innovation. In Southeast Asia, countries including Singapore, Vietnam, and Malaysia are attracting electronics manufacturing investments and benefiting from supply chain diversification.

Competitive Landscape

The global 3D printing photopolymers market structure is moderately consolidated, dominated by leading players such as Stratasys Ltd., 3D Systems Corporation, BASF SE, Evonik Industries AG, and DSM-Firmenich. These players collectively capture 45-55% of the market share. Market consolidation is becoming increasingly evident in high performance industrial and medical photopolymer segments, where advanced material capabilities, regulatory compliance, and strong research and development investment are essential for market participation.

Large and established material manufacturers are strengthening their presence in these specialized segments by developing certified, application specific photopolymer formulations. In contrast, the prototyping and hobbyist segments are remaining relatively fragmented, with numerous smaller suppliers offering cost effective resin options for desktop 3D printing systems. This divergence is creating a competitive landscape in which premium industrial applications are dominated by a few major players, while entry level markets continue to support a broad range of independent material providers.

Key Industry Developments

- In November 2025, Lawrence Livermore National Laboratory researchers developed a novel resin for digital light processing 3D printing that cures and hardens under blue light but degrades into a liquid under UV light, enabling hybrid additive-subtractive manufacturing.

- In February 2026, Hawk Ridge Systems partnered with Stratasys, a leader in polymer additive manufacturing, to expand its 3D printing portfolio with production-grade technologies such as PolyJet multi-material jetting, Neo SLA, and Origin P3 printers.

Companies Covered in 3D Printing Photopolymers Market

- Stratasys Ltd.

- 3D Systems Corporation

- BASF SE

- Evonik Industries AG

- DSM-Firmenich

- Carbon, Inc.

- Henkel AG & Co. KGaA

- Arkema S.A.

- Formlabs Inc.

- DWS Systems S.r.l.

- Mitsui Chemicals, Inc.

- EnvisionTEC

- Sartomer

- Allnex Group

- Photocentric Group

Frequently Asked Questions

The global 3D printing photopolymers market is projected to reach US$ 3.0 billion in 2026.

The market is driven by technological advancements in high-resolution photopolymer resins and rising healthcare demand for custom medical models.

The market is poised to witness a CAGR of 14.4% from 2026 to 2033.

Major opportunities lie in hybrid manufacturing integration that can further unlock precision engineering applications.

Stratasys Ltd., 3D Systems Corporation, BASF SE, Evonik Industries AG, and DSM-Firmenich are some of the key players in the market.