- Biotechnology

- 3D Printed Surgical Models Market

3D Printed Surgical Models Market Size, Share, and Growth Forecast, 2026 - 2033

3D Printed Surgical Models Market by Surgical Model (Cardiac Surgery/Interventional Cardiology, Gastroenterology Endoscopy of Esophageal, Neurosurgery, Orthopedic Surgery, Reconstructive Surgery, Surgical Oncology, Transplant Surgery), Technology (Stereo-lithography, Fused Deposition Modeling), Material (Plastic, Metal), End-User (Hospitals, Ambulatory Surgical Centers), and Regional Analysis for 2026 - 2033

3D Printed Surgical Models Market Share and Trends Analysis

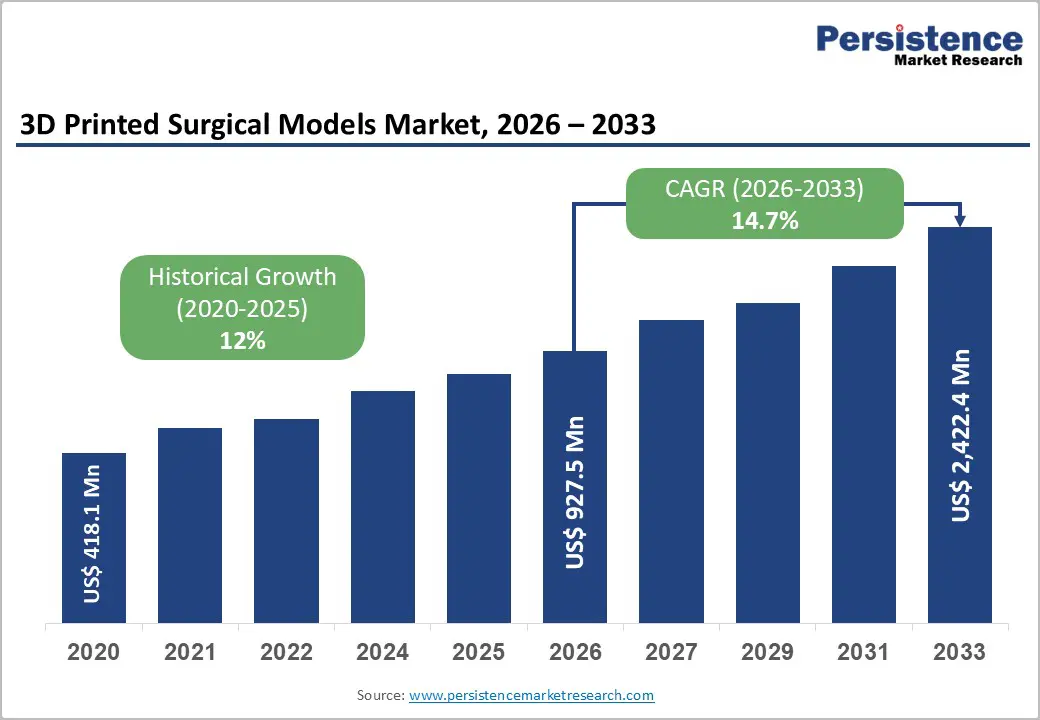

The global 3D printed surgical models market size is likely to be valued at US$ 927.5 million in 2026, and is projected to reach US$ 2,422.4 million by 2033, growing at a CAGR of 14.7% during the forecast period 2026−2033. Growth outlook remains strong, driven by clinical precision requirements and increasing integration of personalized healthcare technologies. Rising prevalence of complex surgical conditions increases demand for patient-specific anatomical models, enabling improved surgical planning and reduced intraoperative uncertainty. Aging population trends contribute to higher surgical volumes, particularly in cardiovascular, orthopedic, and oncological procedures, strengthening demand for advanced preoperative visualization tools.

Expanding clinical awareness among surgeons regarding improved procedural outcomes supports adoption across tertiary care centers and academic institutions. Technological advancement in additive manufacturing, including improved resolution, material diversity, and multi-color printing, enhances model accuracy and realism, enabling broader clinical applications. Integration of digital imaging modalities such as computed tomography and magnetic resonance imaging into 3D modeling workflows improves diagnostic precision and accelerates model production timelines.

Key Industry Highlights

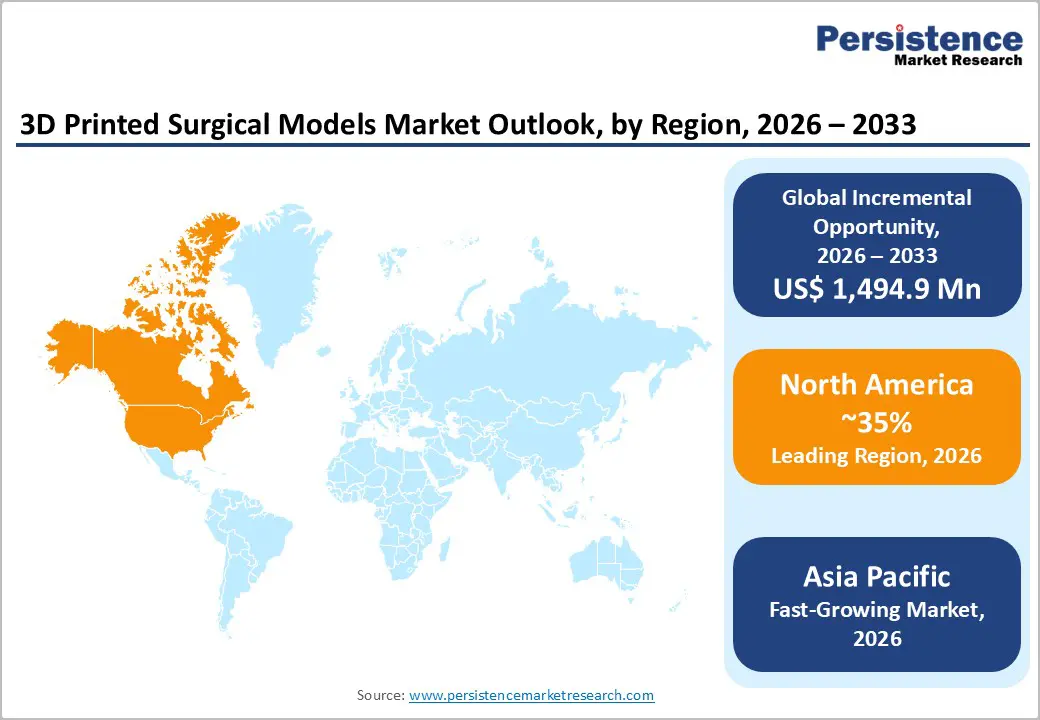

- Dominant Region: North America is expected to dominate with around 35% market share in 2026, driven by hospital digitization and clinical adoption of 3D models.

- Fastest-growing Regional Market: Asia Pacific is forecasted to be the fastest-growing market between 2026 and 2033, supported by healthcare expansion and rising surgical demand.

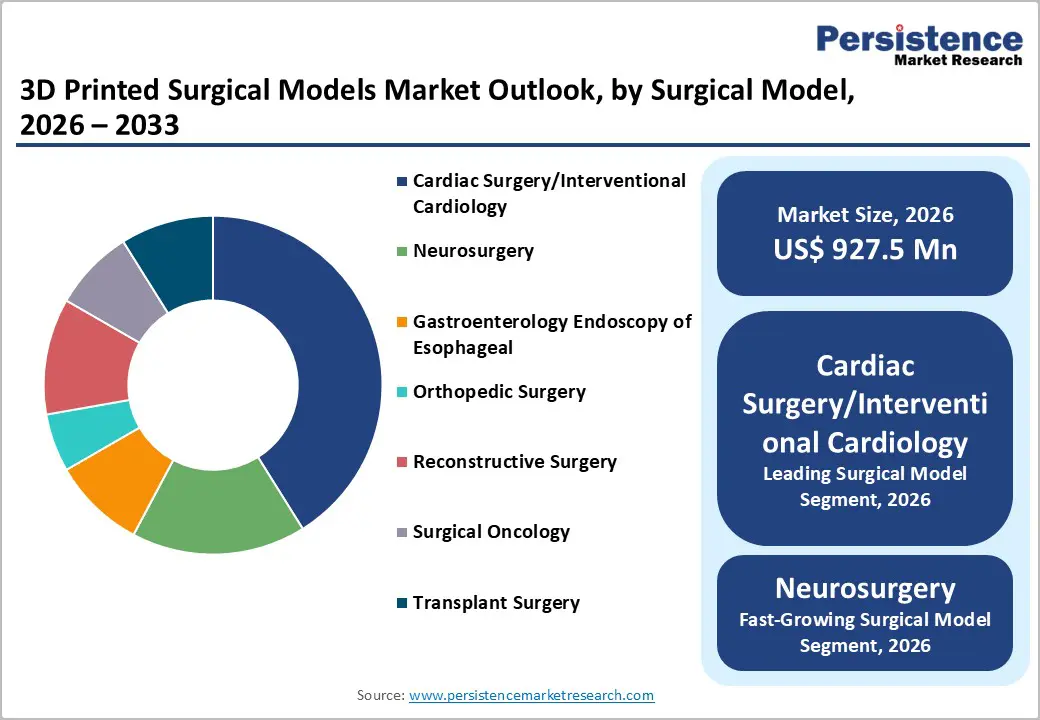

- Leading Surgical Models: Cardiac surgery/interventional cardiology is likely to lead with around 37% share in 2026, owing to reliance on patient-specific anatomical models for precise surgical planning.

- Fastest-growing Surgical Models: Neurosurgery is expected to grow fastest between 2026 and 2033, driven by rising demand for precise 3D models in complex brain and spinal procedures.

| Key Insights | Details |

|---|---|

|

3D Printed Surgical Models Market Size (2026E) |

US$ 927.5 Mn |

|

Market Value Forecast (2033F) |

US$ 2,422.4 Mn |

|

Projected Growth (CAGR 2026 to 2033) |

14.7% |

|

Historical Market Growth (CAGR 2020 to 2025) |

12% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Rising Demand for Patient-Specific Surgical Planning and Precision Medicine

Patient-specific surgical planning reflects a transition toward precision-oriented healthcare delivery, where anatomical variability directly shapes procedural strategy. Conventional imaging methods provide limited spatial interpretation in complex cases involving tumors, vascular deformities, or congenital conditions. Three-dimensional printed anatomical models transform imaging datasets into physical replicas, enabling surgeons to assess structural relationships and rehearse interventions prior to surgery. This approach improves surgical preparedness, reduces intraoperative uncertainty, and strengthens decision accuracy. Guidance frameworks from the National Institutes of Health (NIH) support integration of patient-specific modeling into clinical workflows, reinforcing adoption across advanced surgical specialties and institutional settings.

Precision medicine advances clinical decision-making by aligning treatment strategies with individual anatomical and pathological characteristics. Digital imaging technologies enable high-resolution reconstruction of organs and tissues, forming the basis for customized model development. Surgeons apply these models to refine surgical pathways, evaluate risk factors, and optimize implant positioning during preoperative planning. Policy direction from the U.S. Department of Health and Human Services promotes personalized care frameworks, encouraging adoption of technologies that enhance outcome predictability. Increasing procedural complexity and demand for consistent surgical performance strengthen reliance on individualized planning tools within modern healthcare systems.

Advancements in 3D Printing Technology and Material Innovation

Continuous evolution in additive manufacturing capabilities strengthens clinical adoption through improved accuracy, efficiency, and material functionality. Layer-by-layer fabrication enables production of complex anatomical geometries derived from imaging datasets, supporting precise replication of patient-specific structures for surgical planning and simulation. High-resolution printing systems combined with advanced segmentation Gastroenterology Endoscopy of Esophageal convert computed tomography and magnetic resonance imaging data into tangible models, improving visualization and procedural preparedness. Material innovation expands application scope through biocompatible polymers, resins, and metals that replicate tissue properties. A 2025 study indexed by the U.S. National Library of Medicine indicates reduced energy consumption and material usage in medical additive manufacturing, supporting operational efficiency.

Advancement in multi-material and hybrid printing technologies enables differentiation of soft and hard tissues within a single model, improving clinical interpretation and device selection accuracy. Integration with artificial intelligence and digital modeling platforms enhances design automation, reducing turnaround time from imaging to model creation. Expansion of printable material categories, including bio-inks and metal alloys, supports applications across orthopedic, cardiovascular, and reconstructive procedures. Improved mechanical strength and flexibility allow repeated handling during simulation and training. Standardization of printing protocols and material performance enhances reproducibility, supporting regulatory acceptance and institutional procurement decisions across healthcare systems.

High Production Costs and Limited Reimbursement Frameworks

Production of 3D printed surgical models requires advanced additive manufacturing systems, specialized materials, and skilled personnel trained in imaging segmentation and model design. Capital investment in high-resolution printers and post-processing equipment increases fixed cost burdens. Workflow integration across radiology and surgical planning raises operational complexity and labor intensity. Customization for patient-specific anatomy limits economies of scale, keeping per-unit costs elevated. Budget allocation in hospitals prioritizes direct treatment interventions, placing financial pressure on supportive planning tools. Cost recovery challenges influence procurement decisions, particularly in resource-constrained healthcare environments.

Reimbursement frameworks lack standardized coding and valuation, limiting financial viability for widespread adoption. Agencies such as the Centers for Medicare & Medicaid Services (CMS) provide limited coverage clarity, resulting in fragmented payer policies. Hospitals absorb costs within procedural budgets, affecting departmental margins and capital planning. Financial uncertainty restricts investment in dedicated 3D printing infrastructure. Service providers face pricing pressure while maintaining clinical-grade quality, constraining scalability. Regional variation in reimbursement policies creates uneven adoption patterns, restricting penetration across mid-sized hospitals and ambulatory surgical centers.

Limited Technical Expertise and Workflow Integration Challenges

Healthcare providers face operational barriers when adopting advanced manufacturing technologies within clinical environments. Implementation of 3D printed surgical models requires interdisciplinary coordination across radiology, biomedical engineering, and surgical teams, creating complexity in standard hospital workflows. Skilled professionals with expertise in image segmentation, computer-aided design, and additive manufacturing remain limited in many healthcare systems, particularly outside major academic centers. Training programs demand time and financial resources, restricting scalability. Variability in technical proficiency leads to inconsistencies in model accuracy and production timelines, influencing clinical trust and surgical decision-making.

Workflow alignment presents structural constraints within surgical planning processes. Conversion of imaging data into printable models involves multiple steps, including data extraction, file optimization, and printer calibration, extending preparation timelines compared to conventional methods. Time-sensitive surgical environments require streamlined processes, yet fragmented workflows create bottlenecks that reduce efficiency. Dependence on external service providers introduces logistical delays and limits real-time customization. Cost pressures intensify as extended production cycles and skilled labor requirements increase per-unit expenditure, influencing budget allocation decisions across healthcare institutions.

Expansion into Emerging Healthcare Markets and Infrastructure Development

Rapid healthcare system expansion across developing economies creates a structurally larger addressable base for advanced surgical planning tools. Public-sector investment programs and multilateral financing initiatives increase the number of hospitals, surgical centers, and diagnostic facilities, expanding procedural capacity. The World Health Organization (WHO) reported that nearly 2.1 billion people face financial hardship in accessing healthcare services as of 2025, indicating unmet demand for efficient surgical care delivery. Infrastructure upgrades introduce advanced imaging systems and digital health platforms, enabling conversion of radiological data into physical anatomical models. This transition strengthens clinical workflows in tertiary care centers and improves procedural efficiency.

Healthcare modernization strategies in emerging regions emphasize capability building through new infrastructure rather than incremental upgrades. Newly developed hospitals integrate digital surgery planning ecosystems at the design stage, enabling seamless adoption of additive manufacturing solutions. Private sector participation through public–private partnerships accelerates deployment of specialized surgical services, particularly in cardiology, oncology, and orthopedics. Local production ecosystems evolve with reduced equipment costs and technology transfer initiatives, improving accessibility and turnaround time. Expanding clinical training programs across academic institutions increase reliance on simulation-based learning, supporting broader adoption across surgeons and institutional procurement strategies.

Integration with Digital Health Platforms and Surgical Simulation Ecosystems

Integration with digital platforms and simulation environments creates a structurally stronger clinical workflow, where data, visualization, and physical modeling operate within a unified ecosystem. Hospitals rely on interoperable systems such as electronic health records and imaging platforms to support decision-making. The WHO reported in 2025 that 129 countries established national digital health strategies, reflecting institutional commitment toward connected care delivery models. This alignment enables seamless transfer of imaging data into modeling gastroenterology endoscopy of esophageal, reducing manual intervention and improving turnaround time. Surgeons access synchronized datasets and physical replicas, improving procedural confidence and planning accuracy within standardized clinical pathways.

Simulation ecosystems expand clinical and commercial value by transforming physical models into components of broader training and decision-support frameworks. Surgical platforms incorporating augmented reality, virtual environments, and artificial intelligence generate immersive planning scenarios, where physical models act as validation tools for digital insights. Academic medical centers incorporate hybrid systems to enhance surgical education and improve skill acquisition. Device manufacturers use integrated environments for preclinical testing and product validation. Digital ecosystems create continuous feedback loops, where surgical outcomes inform future model design and simulation accuracy, strengthening adoption across healthcare providers and medical technology companies.

Category-wise Analysis

Surgical Model Insights

Cardiac surgery/interventional cardiology is likely to lead with roughly 37% of the 3D printed surgical models market revenue share in 2026, due to high procedural complexity and strong clinical reliance on anatomical accuracy. Cardiac procedures require precise understanding of patient-specific anatomy, particularly in congenital heart defects and structural heart interventions. 3D printed models enable surgeons to simulate procedures, optimize device selection, and reduce intraoperative risks. High adoption in specialized cardiac centers supports segment leadership. Clinical validation studies demonstrate improved procedural outcomes, reinforcing provider confidence. Integration with imaging modalities enhances model accuracy. Strong institutional adoption in developed healthcare systems contributes to sustained demand.

Neurosurgery is expected to witness the fastest growth between 2026 and 2033, as increasing demand for precision in complex brain and spinal procedures accelerates adoption. Neurosurgical interventions require detailed visualization of intricate anatomical structures. 3D printed models support preoperative planning and improve surgical navigation. Growing incidence of neurological disorders and expanding neurosurgical capabilities drive demand. Technological advancements enable high-resolution replication of neural structures, enhancing clinical utility. Increased adoption in academic and research institutions supports rapid growth.

Technology Insights

Stereo-lithography is expected to hold a dominant position, accounting for an anticipated 55% of the 3D printed surgical models market share in 2026, owing to superior resolution and surface finish. Stereo-lithography enables production of highly detailed models, essential for complex surgical planning. High precision supports clinical accuracy, driving adoption among specialized healthcare providers. Established use in medical applications and compatibility with diverse materials enhance segment dominance. Provider preference for high-quality models reinforces leadership.

Fused deposition modeling are anticipated to be the fastest-growing segment between 2026 and 2033, driven by cost efficiency and accessibility. Fused deposition modeling offers lower production costs and ease of operation, making it suitable for broader adoption across healthcare facilities. Smaller hospitals and training centers are increasingly adopting this technology due to affordability. Expansion of digital commerce platforms supports distribution of equipment and materials. Preventive healthcare adoption and increasing focus on training applications are driving demand for cost-effective solutions.

Regional Insights

North America 3D Printed Surgical Models Market Trends

North America is expected to dominate with an estimated 35% of the 3D printed surgical models market value in 2026, reflecting high procedural integration across the United States and Canada supported by advanced hospital digitization and precision surgery demand. Clinical adoption extends beyond pilot use, with surgical teams routinely incorporating patient-specific anatomical replicas into preoperative workflows, particularly in cardiovascular, orthopedic, and oncological procedures. Strong alignment between imaging infrastructure such as CT (Computed Tomography) and MRI (Magnetic Resonance Imaging) and 3D modeling platforms enables accurate and rapid model generation. Concentration of specialized additive manufacturing firms and academic medical centers strengthens translational efficiency from design to surgical application.

Sustained dominance is reinforced by structured reimbursement pathways, regulatory clarity, and continuous innovation across the United States and Canada, enabling scalable clinical deployment. Healthcare systems prioritize surgical outcome optimization, supporting premium-priced, high-fidelity models with measurable reductions in operating time and intraoperative uncertainty. Extensive collaboration between hospitals, research institutions, and device manufacturers accelerates development of biocompatible materials and AI-enabled design automation. High procedural volumes combined with strong capital investment capacity ensure continuous utilization rather than intermittent adoption.

Europe 3D Printed Surgical Models Market Trends

Europe demonstrates strong positioning in the market for 3D printed surgical models, supported by regulatory standardization and clinically validated adoption across Germany, the United Kingdom, France, and Italy. A harmonized framework under the European Union (EU) Medical Device Regulation (MDR) ensures consistent quality, safety, and traceability of anatomical models, strengthening clinical trust. Hospitals are embedding 3D printing within radiology and surgical units, enabling direct conversion of imaging data into patient-specific models. Academic medical centers collaborate with engineering institutions, accelerating translational research. High utilization is observed in complex procedures including craniofacial, orthopedic, and cardiovascular surgeries, where precision planning significantly improves procedural outcomes and efficiency.

Adoption is further driven by structured healthcare systems emphasizing outcome optimization and cost control, supporting technologies that reduce operative time and complications. Germany and the United Kingdom lead implementation due to strong funding mechanisms and advanced clinical infrastructure. France and Italy are expanding usage through digital health initiatives and increasing focus on precision medicine. Integration of sustainable and bio-based materials is gaining attention, aligning with environmental priorities in healthcare manufacturing. Cross-border research programs and innovation funding frameworks are strengthening development pipelines, enabling continuous advancement in 3D modeling technologies and supporting long-term scalability across diverse clinical applications.

Asia Pacific 3D Printed Surgical Models Market Trends

Asia Pacific is forecasted to be the fastest-growing market for 3D printed surgical models between 2026 and 2033, stimulated by rapid healthcare infrastructure expansion and increasing demand for precision-based surgical planning. China and India are driving volume-led adoption due to large patient pools, rising surgical procedures, and accelerating hospital digitization. Japan and South Korea are advancing high-precision integration supported by robotics, imaging technologies, and established clinical innovation frameworks. Hospitals are transitioning toward in-house 3D printing capabilities, reducing production timelines and improving surgical preparedness. Public investment in digital health and modernization programs further strengthens integration of imaging and modeling technologies.

Growth momentum is reinforced by cost efficiency and expanding accessibility across healthcare systems, enabling adoption beyond premium institutions. China and India benefit from declining equipment costs and strong domestic manufacturing ecosystems, supporting broader deployment in mid-tier hospitals. Japan and South Korea contribute through advanced research collaboration, material innovation, and integration of artificial intelligence in model design. Medical education systems are incorporating 3D printed models into surgical training, creating long-term clinical familiarity. Increasing demand for personalized treatment approaches and complex procedures such as oncology and transplant surgeries continues to elevate reliance on patient-specific anatomical models in decision-making workflows.

Competitive Landscape

The global 3D printed surgical models market reflects a moderately fragmented structure, shaped by the presence of both technology providers and specialized firms. Companies such as Osteo3D, Axial3D, and Lazarus 3D, LLC focus on patient-specific solutions. Meanwhile, Formlabs and Materialise NV deliver scalable platforms, ensuring diversified market share without global concentration.

Competitive positioning depends on clinical integration and innovation capabilities. Onkos Surgical differentiates through alignment with complex surgical applications. Companies invest in automation, artificial intelligence-enabled design, and material advancement to enhance efficiency. Service quality and turnaround time remain critical decision factors, while partnerships with hospitals and research institutions support geographic expansion and sustained competitiveness across evolving surgical modeling applications.

Key Industry Developments

- In January 2026, University of South Florida highlighted the use of patient-specific 3D printed anatomical models developed by its medical lab to enhance surgical planning, reduce complications, and enable more precise rehearsal of complex procedures before actual operations.

- In December 2025, researchers from the Ohio State University Wexner Medical Center demonstrated that patient-specific 3D printed surgical models significantly improved cancer surgery precision, achieving up to 92% complete tumor removal while preserving surrounding healthy tissue.

- In May 2025, researchers at the University of Washington developed a pioneering 3D printing technique capable of producing highly realistic surgical models with tissue-like mechanical properties and embedded blood-like microstructures, significantly enhancing surgical training and procedural simulation accuracy.

Companies Covered in 3D Printed Surgical Models Market

- Osteo3D

- Axial3D

- Lazarus 3D, LLC

- Onkos Surgical

- Formlabs

- Materialise NV

- 3D LifePrints U.K. Ltd.

- WhiteClouds Inc.

Frequently Asked Questions

The global 3D printed surgical models market is projected to reach US$ 927.5 million in 2026.

Rising demand for patient-specific surgical planning, increasing procedural complexity, and advancements in medical imaging and additive manufacturing technologies are driving the market.

The market is poised to witness a CAGR of 14.7% from 2026 to 2033.

Expansion of personalized medicine, integration with artificial intelligence–driven design, and increasing adoption across emerging healthcare systems are creating key market opportunities.

Some of the key market players include Osteo3D, Axial3D, Lazarus 3D, LLC, Onkos Surgical, Formlabs, and Materialise NV.