- Carbon Capture & Storage

- Carbon Footprint Management Market

Carbon Footprint Management Market Size, Share, and Growth Forecast 2026 - 2033

Carbon Footprint Management Market by Component (Solution, Service), Deployment Mode (Cloud-based, On-premises), Organization Size (Large Enterprises, Small & Medium Enterprises), End-user (Manufacturing, Energy & Utility, Residential & Commercial Buildings, Transportation & Logistics, IT & Telecom, Financial Services, Government), by Regional Analysis, 2026 - 2033

Carbon Footprint Management Market Size and Trend Analysis

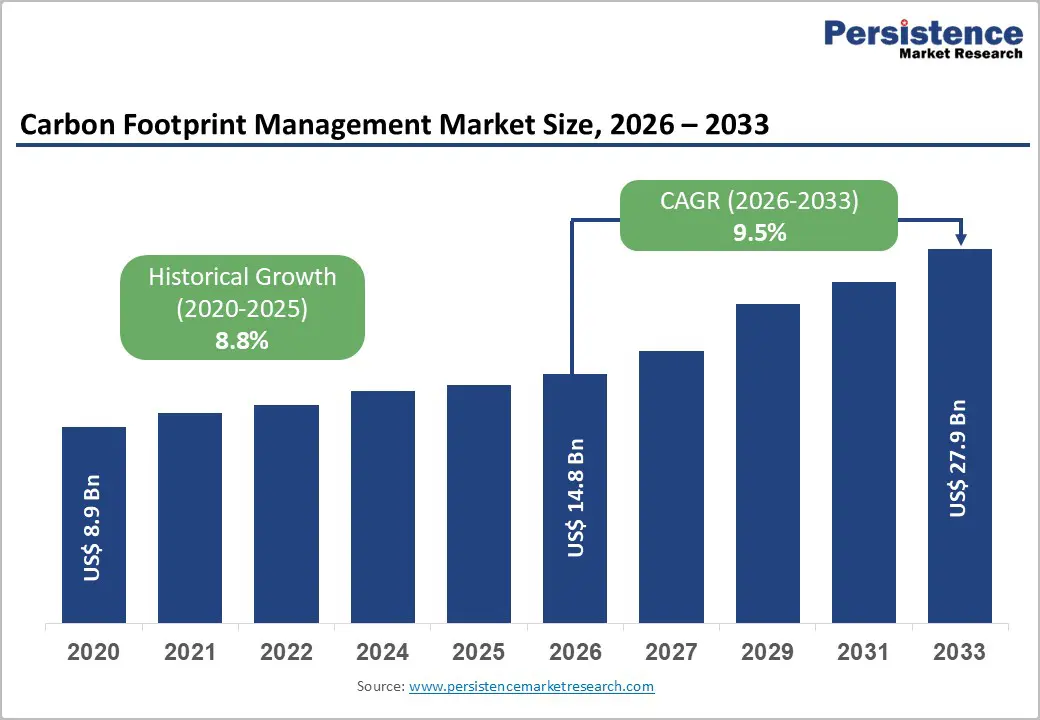

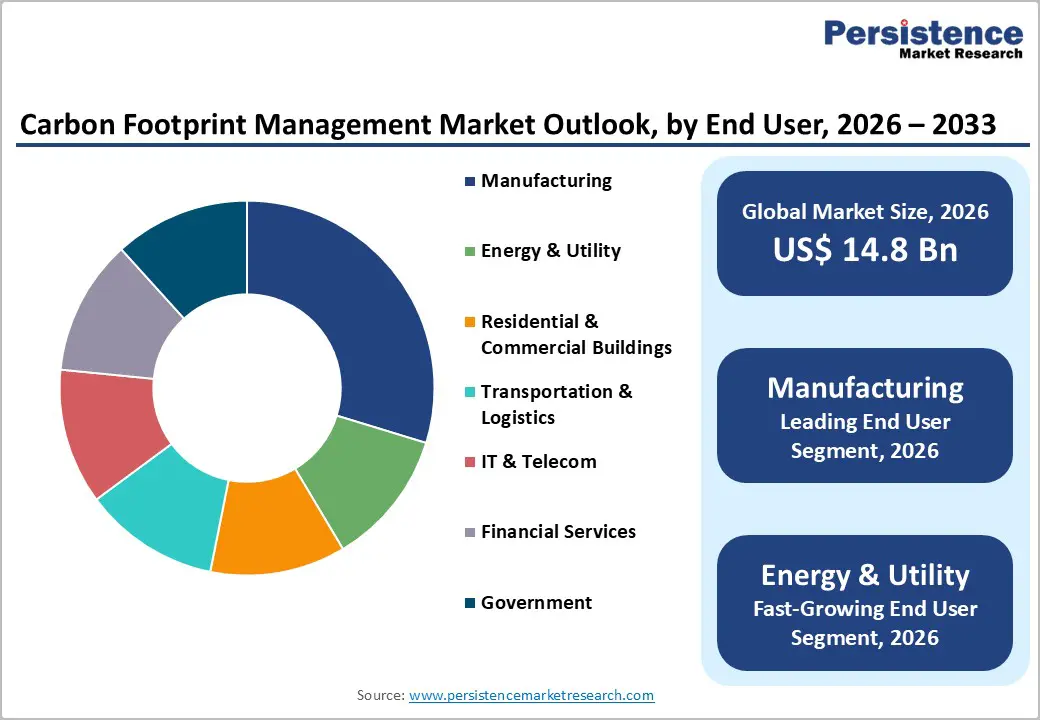

The global carbon footprint management market size is expected to be valued at US$ 14.8 billion in 2026 and projected to reach US$ 27.9 billion by 2033, growing at a CAGR of 9.5% between 2026 and 2033.

The carbon footprint management market is on a steep growth trajectory, primarily propelled by an unprecedented wave of mandatory corporate emissions disclosure frameworks, net-zero commitments, and accelerating digital transformation of sustainability operations across industries. The International Financial Reporting Standards (IFRS) Foundation's climate disclosure standards (IFRS S1 and S2) and the U.S. Securities and Exchange Commission (SEC) climate disclosure rules are compelling thousands of publicly listed companies to implement sophisticated carbon accounting and reporting platforms.

Key Industry Highlights:

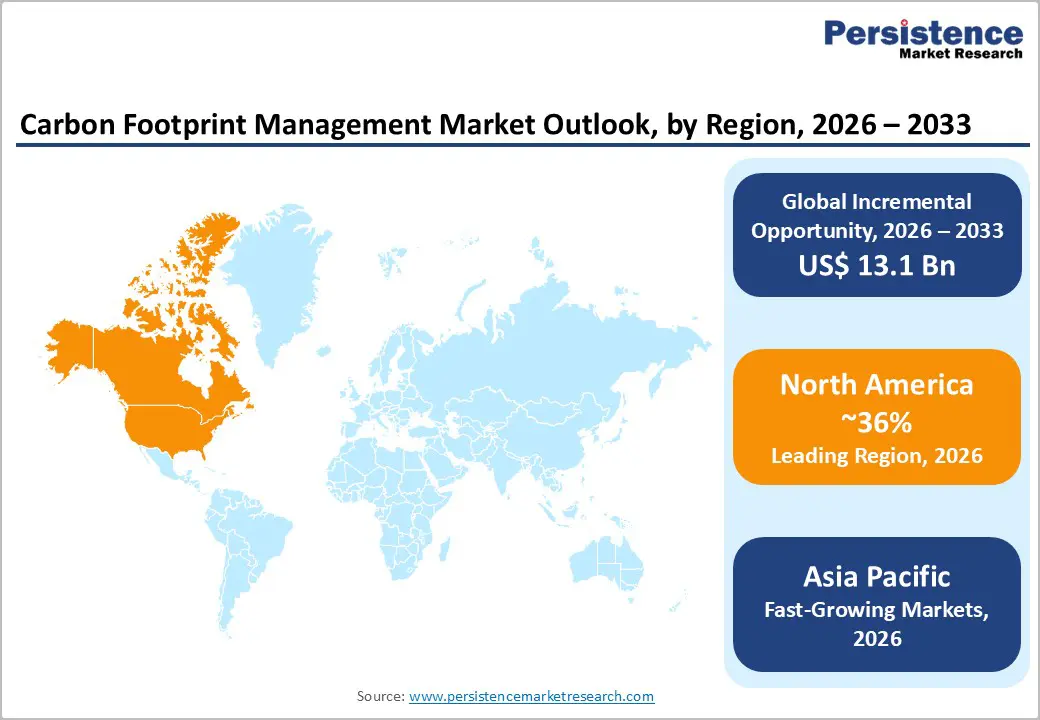

- Leading Region: North America commands approximately 36% share of the global carbon footprint management market in 2025, driven by SEC climate disclosure mandates, deep enterprise software ecosystems, and over 6,000 U.S. companies subject to mandatory Scope 1 and 2 emissions reporting requirements.

- Fastest Growing Region: Asia Pacific is projected at a CAGR of 11.2% through 2033, led by China's national ETS covering 4.5 billion tonnes of CO2 annually, India's Carbon Credit Trading Scheme, and Japan's GX Emissions Trading System driving enterprise carbon platform adoption.

- Dominant Component Segment: The solutions component holds approximately 62% market share in 2025, anchored by enterprise adoption of integrated carbon accounting platforms aligned with CSRD, IFRS S2, and SEC climate disclosure rules across North America and Europe.

- Fastest Growing End-user: Consulting and managed services are the fastest-growing component, as organizations seek expert guidance on Scope 3 accounting complexity, multi-framework regulatory alignment, and AI-powered emissions analytics implementation to fulfill SBTi and CSRD commitments.

- Key Opportunity: AI-native carbon management platforms automating Scope 3 data collection and regulatory reporting, combined with affordable SaaS tools for Europe's 23 million+ SMEs facing supply chain Scope 3 disclosure pressure, represent the highest-growth revenue opportunity through 2033.

| Key Insights | Details |

|---|---|

| Carbon Footprint Management Market Size (2026E) | US$ 14.8 Billion |

| Market Value Forecast (2033F) | US$ 27.9 Billion |

| Projected Growth CAGR (2026 - 2033) | 9.5% |

| Historical Market Growth (2020 - 2025) | 8.8% |

Market Dynamics

Drivers - Rise in Mandatory Corporate Climate Disclosure Regulations Globally

The single most transformative driver of the carbon footprint management market is the rapid proliferation of mandatory climate disclosure and emissions reporting regulations across major economies. The European Union's Corporate Sustainability Reporting Directive (CSRD), effective from January 2024, requires approximately 50,000 companies to report detailed sustainability data including Scope 1, 2, and 3 greenhouse gas emissions against the European Sustainability Reporting Standards (ESRS). In parallel, the U.S. Securities and Exchange Commission (SEC) finalized its climate-related disclosure rules in March 2024, requiring large public companies to disclose Scope 1 and Scope 2 emissions. The International Sustainability Standards Board (ISSB) under the IFRS Foundation published IFRS S2 climate disclosure standards that are being adopted across more than 20 jurisdictions including the U.K., Australia, Singapore, and Canada, creating a globally harmonized demand for integrated carbon accounting software and emissions reporting platforms.

Accelerating Corporate Net-Zero Commitments and Science-Based Targets Adoption

Beyond regulatory mandates, voluntary corporate net-zero commitments and science-based emissions reduction targets are independently generating substantial demand for carbon footprint management tools. The Science Based Targets initiative (SBTi) reported that over 7,000 companies globally had committed to or validated science-based targets as of 2024, with new signatories joining at the rate of approximately 10 companies per day. The UN Race to Zero campaign counts over 11,000 non-state actors, including companies, cities, and financial institutions, committed to achieving net-zero by 2050 at the latest. Fulfilling these commitments requires granular, auditable emissions data and dynamic carbon accounting software capable of tracking progress against reduction targets across entire value chains, driving enterprise adoption of advanced carbon footprint management platforms with Scope 3 value chain analytics and carbon credit management capabilities.

Restraints - High Implementation Complexity and Data Quality Challenges for Scope 3 Emissions

One of the most significant restraints for the carbon footprint management market is the inherent complexity of measuring, verifying, and managing Scope 3 value chain emissions, which typically constitute over 70% of a company's total carbon footprint according to the Greenhouse Gas Protocol. Collecting accurate primary emissions data from thousands of suppliers across fragmented global supply chains requires deep integration with ERP systems, supplier portals, and logistics platforms, a technically challenging and resource-intensive undertaking. The CDP's annual supply chain report noted that fewer than 40% of companies feel confident in their Scope 3 data quality, creating barriers to full platform deployment and limiting reported emissions accuracy. This data deficit restrains confidence in carbon management outputs and slows enterprise-wide adoption.

Lack of Standardization Across Emissions Accounting Methodologies and Frameworks

The proliferation of competing emissions accounting methodologies, including the GHG Protocol, ISO 14064, TCFD framework, ESRS, and sector-specific protocols, creates significant interoperability and compliance complexity for organizations deploying carbon footprint management platforms. Companies operating across multiple jurisdictions must simultaneously comply with divergent reporting standards, requiring platform customization that increases implementation costs and timelines. A 2023 survey by the IFRS Foundation found that regulatory fragmentation was cited by over 60% of multinational CFOs as a key barrier to comprehensive sustainability reporting, indirectly constraining full-scale carbon management platform investments in smaller enterprises and emerging market organizations.

Opportunity - AI and Machine Learning Integration for Predictive Emissions Analytics and Automated Reporting

The integration of artificial intelligence (AI) and machine learning (ML) into carbon footprint management platforms represents one of the most compelling opportunities for market participants to differentiate and capture premium pricing. AI-powered platforms can automate emissions data collection from disparate enterprise systems, detect anomalies in emissions inventories, generate predictive decarbonization scenarios, and automate regulatory reporting across multiple frameworks simultaneously. The World Economic Forum (WEF) estimates that AI could contribute up to 4% of global greenhouse gas reductions by 2030 through optimization across energy, agriculture, and industrial sectors. As organizations seek to move from reactive compliance reporting to proactive emissions management, AI-native carbon accounting platforms, such as those incorporating natural language processing for automated CSRD and TCFD narrative generation, will command significant competitive advantages and higher per-user contract values.

SME Market Expansion Driven by Supply Chain Pressure and SaaS Accessibility

Small and medium enterprises (SMEs) represent a vast, underpenetrated growth opportunity for carbon footprint management solution providers. As large enterprises comply with CSRD and SBTi requirements obligating Scope 3 supply chain emissions reporting, they are cascading carbon data requests to SME suppliers, creating a compliance-pull effect that is drawing millions of smaller businesses into the carbon management ecosystem for the first time. The European Commission estimates there are over 23 million SMEs in the EU alone, the vast majority of which lack formal carbon accounting capabilities. Cloud-native, subscription-based SaaS carbon management platforms priced for SME budgets, offering simplified Scope 1 and 2 tracking, automated utility bill parsing, and one-click report generation, are uniquely positioned to unlock this enormous demand frontier at scale through 2033.

Category-wise Analysis

Component Insights

The solutions segment, encompassing carbon accounting software, emissions tracking platforms, reporting and disclosure tools, and ESG integration software, holds the leading share of approximately 62% of the global carbon footprint management market by component in 2025. This dominance reflects the fundamental role of software platforms as the core infrastructure upon which all carbon management activity is built. The rapid adoption of cloud-based carbon accounting solutions, accelerated by mandatory reporting mandates under CSRD and IFRS S2, has particularly elevated demand for integrated ESG and emissions reporting software. Leading vendors including SAP, IBM, and Schneider Electric have embedded carbon accounting capabilities within broader enterprise software ecosystems, ensuring that software solutions remain the revenue-dominant component category. The Services segment, particularly consulting and managed services, is the fastest-growing component, as organizations require expert implementation guidance for complex Scope 3 accounting and regulatory framework alignment.

Deployment Mode Insights

Cloud-based deployment is the dominant mode in the carbon footprint management market, accounting for approximately 71% of total market share in 2025. Cloud-native platforms offer critical advantages for carbon management: real-time data aggregation from distributed operational sites, seamless integration with utility APIs and supply chain systems, automatic regulatory update deployment, and scalable multi-entity reporting, all without substantial on-premises IT infrastructure investment. The International Data Corporation (IDC) reported that over 65% of enterprise sustainability software investments in 2023 were directed toward cloud-based solutions, reflecting the broader enterprise SaaS adoption trend. Cloud deployment also democratizes access for SMEs and mid-market enterprises that lack dedicated IT teams for on-premises software maintenance, further accelerating cloud's share gain within carbon footprint management deployments through the forecast period.

Organization Size Analysis

Large enterprises constitute the dominant organization size segment, representing approximately 68% of global carbon footprint management market revenue in 2025. Multinational corporations, subject to CSRD, SEC climate disclosure rules, and investor-driven Task Force on Climate-related Financial Disclosures (TCFD) reporting, have been the early adopters of enterprise-grade carbon accounting platforms capable of managing complex, multi-entity, multi-geography emissions inventories spanning all three Scopes. The S&P Global reported that over 90% of S&P 500 companies published sustainability reports in 2023, a majority of which employed dedicated emissions management software. However, the SMEs segment is growing at the fastest rate, driven by supply chain Scope 3 reporting pressure from large corporate buyers and the proliferation of affordable SaaS-based carbon accounting tools tailored for smaller organizations.

End-user Insights

The Manufacturing end-user segment is the leading consumer of carbon footprint management solutions, accounting for approximately 27% of global market share in 2025. The manufacturing sector is among the largest industrial sources of greenhouse gas emissions, responsible for approximately 24% of global CO2 emissions according to the International Energy Agency (IEA), and faces intense regulatory and investor scrutiny regarding decarbonization progress. Industrial manufacturers require sophisticated emissions tracking across production processes, energy consumption, fugitive emissions, and value chain logistics, driving investment in enterprise-grade carbon management platforms integrated with manufacturing execution systems (MES) and energy management systems. The Energy & Utility sector is the fastest-growing end-user segment, as utilities prepare for compliance with evolving carbon pricing mechanisms including the EU Emissions Trading System (EU ETS) and its global equivalents.

Regional Insights

North America Carbon Footprint Management Market Trends and Insights

North America leads the global carbon footprint management market with 36% market share in 2025, supported by a mature enterprise software industry, strong institutional investor pressure for ESG disclosure, and an evolving regulatory framework for mandatory climate reporting. The U.S. Securities and Exchange Commission (SEC) climate disclosure rules, requiring large accelerated filers to begin disclosing Scope 1 and Scope 2 emissions in fiscal year 2025 filings, have significantly accelerated enterprise carbon platform procurement across publicly listed U.S. companies. Over 6,000 companies are expected to be directly subject to these rules, creating a substantial near-term demand surge for carbon accounting software vendors.

Canada's Canadian Securities Administrators (CSA) proposed climate-related disclosure rules aligned with IFRS S2 further extend the compliance perimeter across North American capital markets. The U.S. is also home to the highest concentration of carbon footprint management software innovators, including IBM Corporation, Salesforce (Net Zero Cloud), and emerging AI-native startups. The voluntary carbon market infrastructure, centered in Chicago and New York, additionally drives demand for carbon credit management modules within enterprise carbon management platforms, creating a uniquely comprehensive demand ecosystem in the region.

Europe Carbon Footprint Management Market Trends and Insights

Europe is the world's most regulatory-advanced market for carbon footprint management, driven by the European Green Deal, Corporate Sustainability Reporting Directive (CSRD), and the EU Emissions Trading System (EU ETS). The CSRD, the world's most comprehensive mandatory sustainability reporting law, requires approximately 50,000 companies to report detailed emissions data from fiscal year 2024 onwards, creating an unprecedented compliance-driven procurement wave for carbon accounting software across Germany, France, the U.K., and Spain. Wolters Kluwer and SAP, both with strong European footprints, have positioned their platforms to align natively with ESRS reporting requirements.

Germany's industrial manufacturing sector, the continent's largest, is a major consumer of integrated emissions management platforms, particularly those capable of tracking industrial process emissions against EU ETS allowance obligations. France's loi Énergie-Climat mandates carbon reporting for large companies, while Spain's Law 7/2021 on Climate Change and Energy Transition reinforces similar requirements. The U.K., post-Brexit, has implemented its own Sustainability Disclosure Standards (SDS) aligned with IFRS S2, ensuring that European regulatory harmonization continues to be the primary growth engine for carbon management platform adoption across the region through 2033.

Asia Pacific Carbon Footprint Management Market Trends and Insights

Asia Pacific is the fastest-growing regional market for carbon footprint management with 11.2% CAGR between 2026 and 2033, propelled by the world's two largest national carbon emissions trading schemes and rapidly maturing corporate sustainability disclosure ecosystems. China's national Emissions Trading System (ETS), operational since 2021 and covering over 2,200 power sector entities responsible for approximately 4.5 billion tonnes of CO2 annually, is the world's largest carbon market by covered emissions according to the International Carbon Action Partnership (ICAP). Regulated entities require sophisticated carbon accounting and allowance management platforms to ensure compliance, driving enterprise software procurement at scale.

India's Carbon Credit Trading Scheme (CCTS), launched under the Energy Conservation (Amendment) Act 2022, is creating a new domestic carbon market infrastructure, stimulating demand for emissions tracking and credit management platforms. Japan's GX (Green Transformation) Emissions Trading System, launched in 2023, extends compliance obligations to major industrial emitters. Singapore's Monetary Authority of Singapore (MAS) climate disclosure requirements for financial institutions and ASEAN taxonomy developments are further accelerating carbon management software adoption across Southeast Asia, positioning the region as the defining growth frontier for the carbon footprint management market through 2033.

Competitive Landscape

The global carbon footprint management market is moderately fragmented, comprising enterprise software vendors, dedicated sustainability technology firms, and emerging SaaS-native providers. While entry barriers for basic reporting tools remain relatively low, enterprise-grade platforms require robust regulatory alignment, data security, and system integration capabilities, creating structural advantages for established providers. Competitive intensity is increasing as organizations move from voluntary disclosure to mandatory, audit-ready carbon accounting.

Business strategies focus on delivering end-to-end platforms that integrate emissions measurement, Scope 1-3 tracking, ESG reporting, and compliance management within existing enterprise ecosystems. Artificial intelligence-driven automation, multi-framework reporting alignment, and advanced value chain analytics are central differentiation levers. Vendors are strengthening market positions through partnerships with consulting firms, carbon data providers, and ERP integrators to offer comprehensive decarbonization solutions. Meanwhile, agile SaaS competitors target SMEs with modular, subscription-based offerings and rapid deployment models, prompting incumbents to accelerate innovation cycles and selectively pursue acquisitions to expand capabilities and geographic reach.

Key Developments

- December 2025: BASF Coatings unveiled a real-time digital tool to track carbon footprint data across 120,000 products, enhancing transparency and sustainability measurement for its coatings and materials portfolio.

- November 2025: Normative launched a product carbon footprint service to help businesses calculate and report the greenhouse gas emissions of products across the lifecycle for improved sustainability insights.

- September 2025: Watershed launched an AI-powered product carbon footprint solution designed to help companies measure and manage the carbon impact of products, materials, and processes with greater accuracy and efficiency.

- May 2025: SET (Stock Exchange of Thailand) launched a carbon footprint management platform to enable businesses and financial institutions to measure, monitor, and report greenhouse gas emissions for improved sustainability and compliance.

Companies Covered in Carbon Footprint Management Market

- IBM Corporation

- Wolters Kluwer

- Dakota Software

- ENGIE

- ProcessMAP Corporation

- Schneider Electric

- IsoMetrix

- SAP SE

- Ecova (Willow)

- Salesforce (Net Zero Cloud)

- Microsoft Corporation (Sustainability Manager)

- Intelex Technologies

- Enviro Accounting Solutions (Urjanet)

- Normative

- Persefoni AI

- BASF SE

- Watershed

Frequently Asked Questions

The market is projected to reach US$ 14.8 billion in 2026, supported by mandatory climate disclosure regulations and ESG compliance requirements.

Growth is driven by CSRD, SEC climate rules, IFRS S2 adoption, and rising corporate net-zero commitments worldwide.

North America leads in 2025, while Asia Pacific is the fastest-growing region due to expanding emissions trading systems.

AI-enabled Scope 3 automation and SME adoption present major growth opportunities.

Key players include SAP SE, IBM Corporation, Schneider Electric, Wolters Kluwer, ENGIE, Salesforce, and Microsoft.