- Inks, Coatings, Adhesives & Sealants (ICAS)

- Rotogravure Printing Inks Market

Rotogravure Printing Inks Market Size, Share, and Growth Forecast, 2026 – 2033

Rotogravure Printing Inks Market by Resin Type (Polyamide, Polyurethane, Nitro-Cellulose, Others), Application (Flexible Packaging, Labels & Wrappers, Publication Printing, Others), and Regional Analysis for 2026 – 2033

Rotogravure Printing Inks Market Size and Trends Analysis

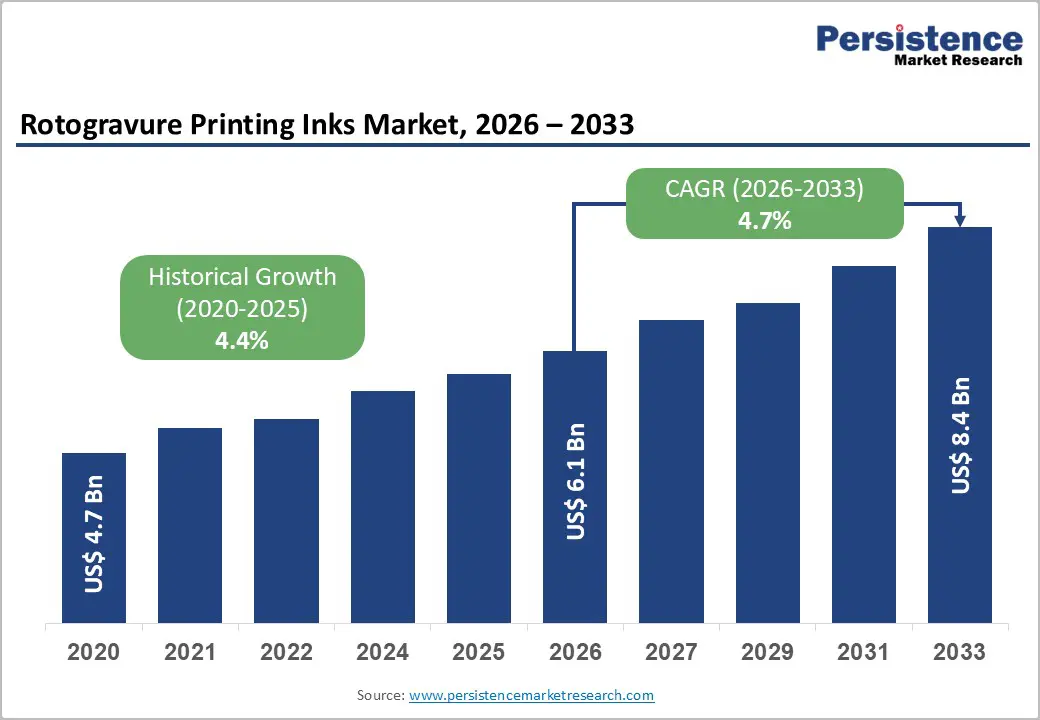

The global rotogravure printing inks market size is likely to be valued at US$6.1 billion in 2026 and is expected to reach US$8.4 billion by 2033, growing at a CAGR of 4.7% during the forecast period from 2026 to 2033, driven by its strong positioning in high-volume, high-quality printing applications, particularly within the packaging industry. Demand is largely driven by the food and beverage sector, where brand owners prioritize superior print clarity, color consistency, and durability to enhance shelf appeal and meet stringent packaging standards.

The rapid expansion of e-commerce has strengthened market adoption, as rotogravure inks are widely used for large-scale production of labels and wrappers, which together account for a significant share of overall application demand. The growing use of flexible packaging across consumer goods, personal care, and household products continues to favor rotogravure printing due to its cost efficiency at high print runs and excellent performance on plastic films and laminates

Key Industry Highlights:

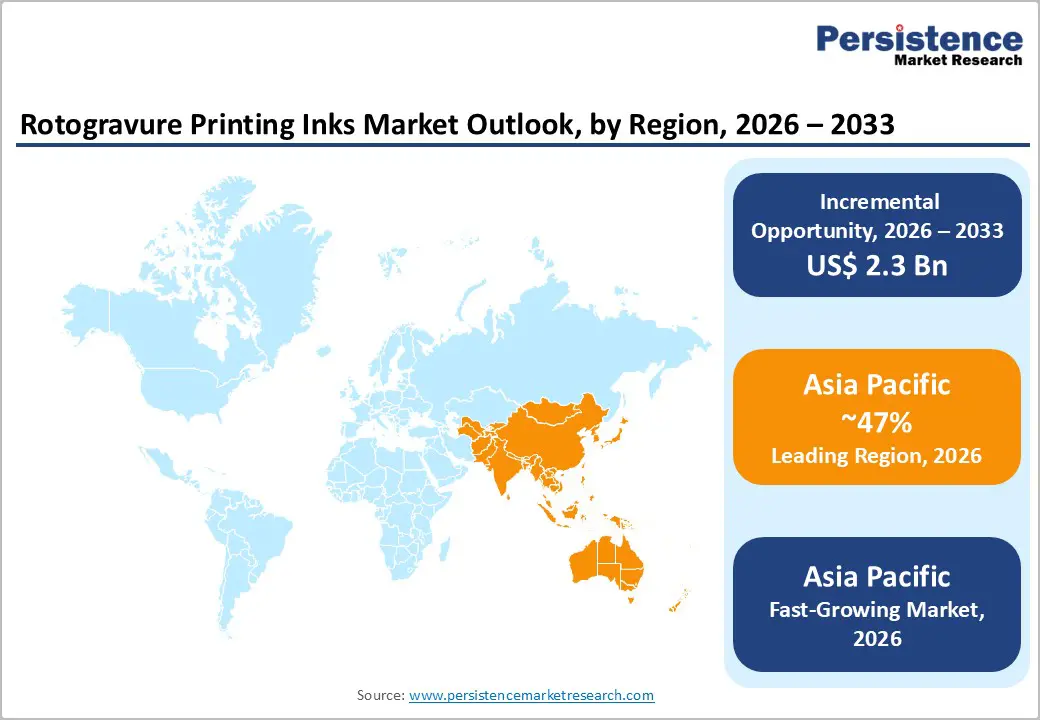

- Leading Region: Asia Pacific is anticipated to be the leading region, accounting for a market share of 47% in 2026, driven by robust manufacturing advantages, expanding flexible packaging and FMCG demand, and rapid growth in e-commerce across China, Japan, India, and ASEAN.

- Fastest-growing Region: Asia Pacific is likely to be the fastest-growing region in the rotogravure printing inks in 2026, supported by increasing manufacturing investments and rising adoption of cost-efficient, high-volume printing technologies across emerging economies.

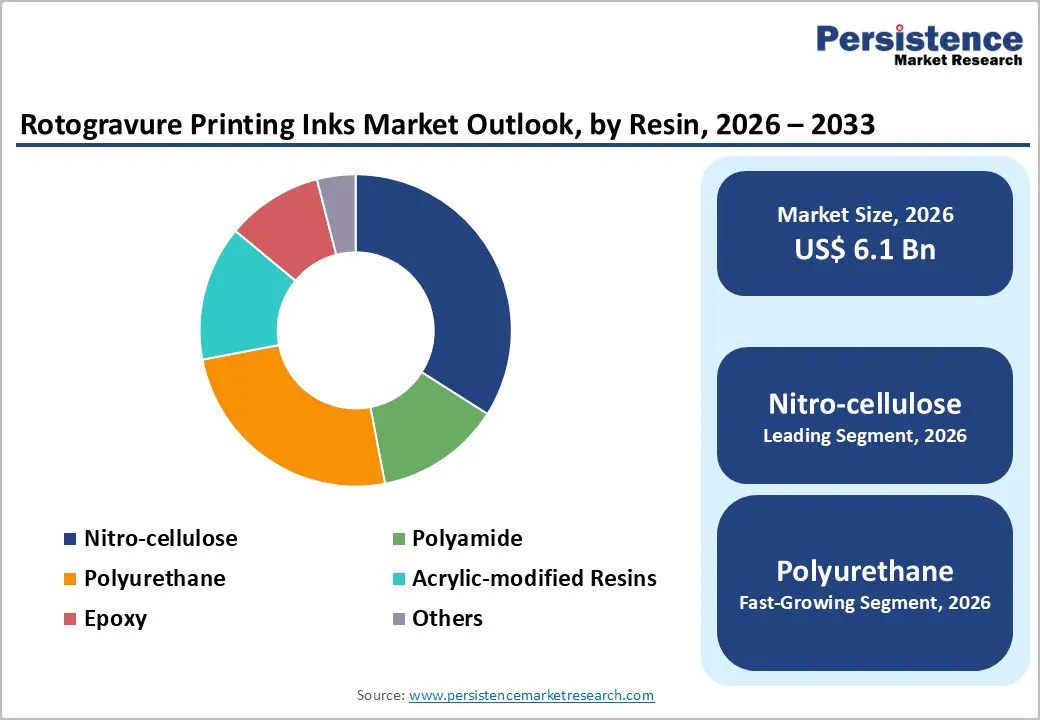

- Leading Resin Type: Nitro-cellulose is projected to represent the leading product type in 2026, accounting for 40% of the revenue share, driven by its strong adhesion and fast-drying performance on flexible substrates.

- Leading Application: Flexible packaging is anticipated to be the leading application type, accounting for over 45% of the revenue share in 2026, supported by its extensive use in food, beverage, and FMCG packaging.

| Key Insights | Details |

|---|---|

| Rotogravure Printing Inks Market Size (2026E) | US$ 6.1 Bn |

| Market Value Forecast (2033F) | US$ 8.4 Bn |

| Projected Growth (CAGR 2026 to 2033) | 4.7% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.4% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growth Analysis - Rising Demand from the Flexible Packaging Industry

The flexible packaging industry is the largest demand generator for rotogravure printing inks due to its requirement for high-quality, consistent, and durable printing. Food and beverage packaging, in particular, relies heavily on rotogravure inks for vibrant colors, fine image resolution, and excellent adhesion on plastic films, foils, and laminates. As consumer preferences shift toward convenient, lightweight, and shelf-stable packaged products, flexible packaging continues to replace rigid formats, directly supporting sustained ink consumption across large-volume printing operations. Brand owners increasingly use premium graphics and complex designs to enhance shelf differentiation, strengthening reliance on rotogravure printing.

The rapid expansion of e-commerce has amplified demand for flexible packaging formats such as pouches, sachets, and wrappers that require high-speed, long-run printing. Rotogravure inks enable efficient mass production while maintaining print quality across extended runs, making them cost-effective for converters. Growth in FMCG, pharmaceuticals, and personal care packaging reinforces the importance of flexible packaging. Increased focus on product protection, barrier properties, and tamper resistance in transit has increased demand for durable printed packaging. The ability of rotogravure inks to deliver uniform quality over long print runs makes them indispensable for large-scale packaging converters.

Technological Advancements and Sustainability Regulations

Ongoing technological advancements in ink formulation are driving market growth by improving performance, efficiency, and compliance. Innovations in resin chemistry, pigment dispersion, and drying mechanisms have enhanced print sharpness, color stability, and substrate compatibility. These improvements allow rotogravure inks to perform effectively across a wide range of films and laminates while supporting faster production speeds and reduced downtime for printers. Improved ink transfer and reduced solvent retention help enhance production consistency and minimize waste.

Sustainability regulations are pushing manufacturers toward low-VOC, toluene-free, and water-based ink solutions. Environmental mandates from regulatory authorities are accelerating innovation, encouraging ink producers to develop compliant formulations without compromising print quality. As packaging companies increasingly align with sustainability goals and corporate ESG commitments, technologically advanced and environmentally compliant rotogravure inks are gaining wider acceptance. These regulations are also driving investments in cleaner production technologies and greener supply chains.

Barrier Analysis - Stringent Environmental Regulations and VOC Restrictions

Traditional solvent-based inks face increasing scrutiny due to their environmental and health impacts, forcing manufacturers to reformulate products. Compliance with emission standards often requires costly investments in R&D, alternative solvents, and emission control systems, which can increase operational expenses for ink producers and printers alike. Reformulation efforts may affect ink performance, drying speed, and substrate compatibility, requiring extensive testing and validation. Regulatory compliance also extends approval timelines, delaying product launches and increasing time to market.

These regulatory pressures are particularly challenging for small and mid-sized printing companies with limited capital resources. Transitioning to low-VOC or water-based inks may also require equipment modifications and process adjustments, increasing costs. Investments in ventilation, solvent recovery, and waste management systems raise overall production expenses. Regulatory compliance can slow adoption rates in certain regions and limit market expansion, especially where enforcement is strict and financial incentives are limited. Some printers delay modernization or reduce production capacity.

Shift to Digital Printing and Cost Barriers

Digital printing offers flexibility, faster setup times, and variable data printing, making it attractive for brands seeking personalization and reduced inventory. This shift is gradually reducing demand for conventional rotogravure printing in certain label and publication segments. Short-run packaging, promotional materials, and customized designs are increasingly produced using digital technologies, limiting rotogravure ink consumption in these areas. Frequent design changes and shorter product lifecycles favor digital printing over long-run processes. Digital print quality continues to improve, and it poses a growing competitive threat to traditional rotogravure applications, especially in niche and premium segments.

Rotogravure printing involves high capital investment in presses, engraving cylinders, and specialized inks, which can be prohibitive for smaller converters. The cost-intensive nature of the process limits adoption in price-sensitive markets and restricts the entry of new players. High setup costs make rotogravure economically viable mainly for long print runs, reducing flexibility for smaller batch production. Maintenance costs and skilled labor requirements increase operational expenses. These financial and technological barriers reduce market penetration and create sustained competitive pressure from alternative printing technologies, particularly flexographic and digital printing systems.

Opportunity Analysis - Growth in Sustainable and Bio-Based Inks

The increasing focus on sustainability presents a significant opportunity for the rotogravure printing inks market through the development of sustainable and bio-based ink solutions. Brand owners and packaging converters are actively seeking inks with reduced environmental impact, driving demand for renewable, biodegradable, and recyclable formulations. Bio-based resins and water-based systems help lower carbon emissions and support circular economy initiatives. These inks reduce dependence on fossil-based solvents, improving workplace safety and environmental compliance. Regulatory support and sustainability certifications are encouraging adoption across food, beverage, and consumer goods packaging. As sustainability becomes a purchasing criterion, eco-friendly inks are gaining strategic importance.

Manufacturers that invest in sustainable ink innovation can gain a competitive advantage by meeting regulatory requirements and customer sustainability goals. As consumer awareness of environmental issues continues to rise, demand for eco-friendly packaging solutions is expected to accelerate. This trend creates long-term growth opportunities for rotogravure ink producers offering compliant, high-performance, sustainable products. Companies focusing on green R&D can strengthen brand positioning and customer loyalty. Sustainable ink portfolios enable access to premium packaging segments and brand contracts.

Technological Convergence with Hybrid Systems

Hybrid printing combines the efficiency of rotogravure with the flexibility of digital or flexographic technologies, enabling printers to handle both high-volume runs and customized designs. Ink manufacturers are developing versatile formulations compatible with multiple printing platforms, expanding their application potential. These hybrid systems allow seamless transitions between printing processes without compromising print quality or speed. Improved ink adaptability supports consistent color reproduction across different technologies. This convergence also reduces dependency on a single printing method, enhancing operational flexibility for converters.

This convergence allows packaging converters to optimize production costs, reduce material waste, and respond quickly to changing market demands. As packaging designs become more complex and brand differentiation intensifies, hybrid compatible rotogravure inks can support innovation while maintaining production efficiency. Hybrid systems also enable shorter setup times and reduced downtime between print jobs. This improves overall equipment utilization and profitability for printers. Hybrid compatibility supports sustainable production by minimizing waste and energy consumption.

Category-wise Analysis

Resin Type Insights

Nitrocellulose is projected to lead the rotogravure printing inks market, contributing around 40% of the revenue by 2026, due to its proven effectiveness in high-volume flexible packaging applications. Its market dominance stems from its excellent adhesion to plastic films, foils, and laminated substrates, which are commonly used in food and beverage packaging. Nitrocellulose inks offer quick drying times, strong color intensity, and consistent print quality, making them ideal for long-run printing operations where efficiency is key. These characteristics help converters maintain high production speeds while minimizing defects and downtime. For instance, they are extensively used in food wrappers, where sharp graphics and reliable ink transfer are crucial for meeting both branding and regulatory standards.

Polyurethane inks, on the other hand, are expected to be the fastest-growing segment by 2026, driven by the increasing demand for durable, high-performance inks in labels, decorative films, and premium packaging. Offering superior abrasion resistance, chemical stability, and flexibility, polyurethane-based inks are particularly suited for applications subject to handling, friction, and environmental stress. Their ability to perform well on complex substrates supports their growing adoption in value-added packaging formats. An example of this is their rising use in e-commerce packaging, where labels and graphics need to endure transportation and repeated handling without degradation.

Application Insights

Flexible packaging is expected to dominate the market, capturing around 45% of the revenue share by 2026, due to its widespread use across food, beverage, personal care, and household products. Rotogravure inks are particularly well-suited for flexible packaging as they offer superior color consistency, fine image resolution, and strong adhesion to films and laminates. These qualities are essential for enhancing brand visibility and shelf appeal in competitive retail markets. For instance, in food packaging, flexible formats such as pouches and wraps require durable, high-quality printing to maintain branding integrity and meet labeling standards. The scalability of rotogravure printing also allows for cost-effective production of large packaging volumes, reinforcing its dominance in this sector.

Labels and wrappers are expected to be the fastest-growing application, driven by increasing demand for customization, branding differentiation, and packaging suited for e-commerce. This segment benefits from a greater focus on visual appeal, product traceability, and consumer engagement through high-quality printed labels. For example, in consumer goods packaging, labels and wrappers are crucial for brand recognition and delivering product information. Advances in printing technology have enabled more intricate designs and consistent reproduction, fostering wider adoption. Rotogravure inks are favored for labels and wrappers due to their ability to maintain print clarity across long production runs while working with a wide variety of substrates.

Regional Insights

North America Rotogravure Printing Inks Market Trends

North America is expected to be a key market, driven by a mature packaging industry, particularly in the U.S. and Canada, where flexible packaging remains the dominant ink consumer. The region is placing increasing emphasis on eco-friendly, low-VOC, and water-based ink technologies to meet stringent environmental regulations and reduce emissions from solvent-based systems, prompting converters to adopt more sustainable printing solutions. For example, Sun Chemical is advancing its portfolio of sustainable, high-quality inks to address the rising demand for compliant packaging inks and maintain a competitive edge in a regulation-driven market.

Sustainability trends and technological innovation are shaping the regional market, with converters embracing advanced printing methods such as hybrid and digital integration to boost efficiency, minimize downtime, and support shorter print runs alongside traditional gravure production. Functional inks with specialized properties, such as UV resistance and chemical stability, are becoming more popular for industrial and premium packaging applications. Ongoing regulatory frameworks in North America are influencing procurement strategies, encouraging manufacturers to create ink formulations that meet both performance standards and environmental guidelines.

Europe Rotogravure Printing Inks Market Trends

Europe is likely to be a significant market, due to sustainability mandates and regulatory focus on low-VOC, water-based, and eco-friendly ink formulations. Converters are shifting away from traditional solvent-based systems to meet stringent emissions requirements and reduce environmental impact. This trend is most pronounced in flexible packaging and food contact applications, where adherence to strict safety and migration limits is essential. The region's mature packaging industry also demands high-definition print quality and excellent substrate compatibility to support premium branding and multi-layer films used across food, cosmetics, and luxury products.

Innovation and collaboration among key players are advancing market trends, with companies increasingly launching specialized ink solutions tailored to European demand. For example, Germany-based Siegwerk Druckfarben AG & Co. KGaA develops next-generation nitrocellulose and low-VOC ink series designed for high-performance gravure and flexo packaging applications, reinforcing its leadership in sustainability-aligned rotogravure printing technology. Beyond sustainability, the rising popularity of premium packaging in cosmetics and personal care sectors is creating demand for specialty inks that provide vibrant colors, improved adhesion, and multifunctional properties such as UV resistance and barrier performance.

Asia Pacific Rotogravure Printing Inks Market Trends

The Asia Pacific region is expected to be both the largest and fastest-growing market, capturing a 47% share of the market by 2026. This growth is fueled by rapid industrialization and the expansion of the packaging sector in key economies, including China, India, Japan, and ASEAN countries. As flexible packaging becomes the preferred choice for food, beverage, personal care, and pharmaceutical products, the region's demand for rotogravure inks remains strong, particularly for high-volume print runs that require vibrant colors and excellent adhesion to multilayer films and laminates. Local converters benefit from cost-effective raw materials and integrated supply chains, which help reduce production costs while maintaining quality, making it attractive for multinational brands to source locally.

Technological innovation and regulatory influences are driving distinct trends in the Asia Pacific market. An increasing number of converters and ink manufacturers are developing low-VOC, water-based, and hybrid ink formulations to comply with evolving sustainability requirements and minimize environmental impact. Local companies are enhancing their R&D capabilities to improve print performance and broaden the versatility of applications across both traditional and emerging packaging formats. For example, Toyo Ink SC Holdings Co., Ltd. has introduced advanced rotogravure inks specifically tailored to meet the demands of the Asian packaging market, focusing on improved pigment stability and enhanced substrate adhesion to support premium labeling and flexible film applications.

Competitive Landscape

The global rotogravure printing inks market exhibits a moderately fragmented structure, driven by the presence of numerous regional and multinational players competing on product innovation, sustainability, and geographic reach. Large chemical and ink manufacturers maintain strong positions through broad product portfolios that cater to flexible packaging, publication, and specialty applications, with an increasing focus on environmental compliance and performance enhancements.

With key leaders including DIC Corporation, Flint Group, Sun Chemical, Siegwerk Druckfarben AG & Co. KGaA, and Toyo Ink SC Holdings Co., Ltd., the competitive landscape balances scale with localized customer service and rapid response to regional trends. These players compete through continuous R&D investment, strategic partnerships, and expansion of sustainable and high-performance product lines to differentiate themselves in the market.

Key Industry Developments:

- In January 2026, Sun Chemical launched a new portfolio of NC-alternative inks for flexible packaging to tackle supply chain volatility, rising costs, and sustainability challenges. These NC-free inks are fully recyclable and comply with RecyClass and CEFLEX guidelines, supporting better recyclability and high-quality recyclate output. The portfolio, suitable for gravure and flexographic printing, includes inks, coatings, primers, and adhesives as an integrated system.

- In November 2025, Siegwerk introduced the first NC-free surface ink systems for PE and PP flexible packaging, advancing recyclability for polyolefin-based packaging. Designed for gravure and flexographic printing, the inks meet RecyClass and CEFLEX guidelines and provide high-quality recyclate. Made with proprietary polyurethane binders, the inks offer strong adhesion, fast drying, heat resistance, and excellent rub and sealing resistance, eliminating the need for additional varnishes.

Companies Covered in Rotogravure Printing Inks Market

- artience Co., Ltd.

- Changzhou Tiansheng New Materials

- DIC Corporation

- Flint Group

- FUJIFILM Holdings Corporation

- hubergroup Deutschland GmbH

- Kao Corporation

- Nazdar Ink Technologies

- Polymeric Group

- Sakata INX Corporation

- Siegwerk Druckfarben AG & Co. KGaA

- SÜDPACK

- Sun Chemical

- Superior Printing Inks Co.

Frequently Asked Questions

The global rotogravure printing inks market is projected to reach US$6.1 billion in 2026.

The rotogravure printing inks market is driven by rising demand for high-quality, high-speed printing in flexible packaging, fueled by growth in food, beverage, and consumer goods packaging.

The rotogravure printing inks market is expected to grow at a CAGR of 4.7% from 2026 to 2033.

Key market opportunities lie in the development of sustainable, NC-free, and bio-based inks, along with growing demand from flexible packaging and e-commerce-driven high-volume printing applications

artience Co., Ltd., Changzhou Tiansheng New Materials, DIC Corporation, and Flint Group are the leading players