- Advanced Materials

- 3D Printing Materials Market

3D Printing Materials Market Size, Trends, Share, and Growth Forecast 2025 - 2032

3D Printing Materials Market by Product Type (Plastics/Polymers, Metals, Ceramics, Composites, Food Materials), Form (Filaments/Wire, Powders, Resins/Liquids, Paste/Slurry), Technology (Fused Deposition Modeling, Stereolithography, Selective Laser Sintering, Direct Metal Laser Sintering, Contour Crafting), Industry (Aerospace & Defence, Automotive, Building & Construction, Food and Beverages), by Regional Analysis, 2025 - 2032

3D Printing Materials Market Size and Trend Analysis

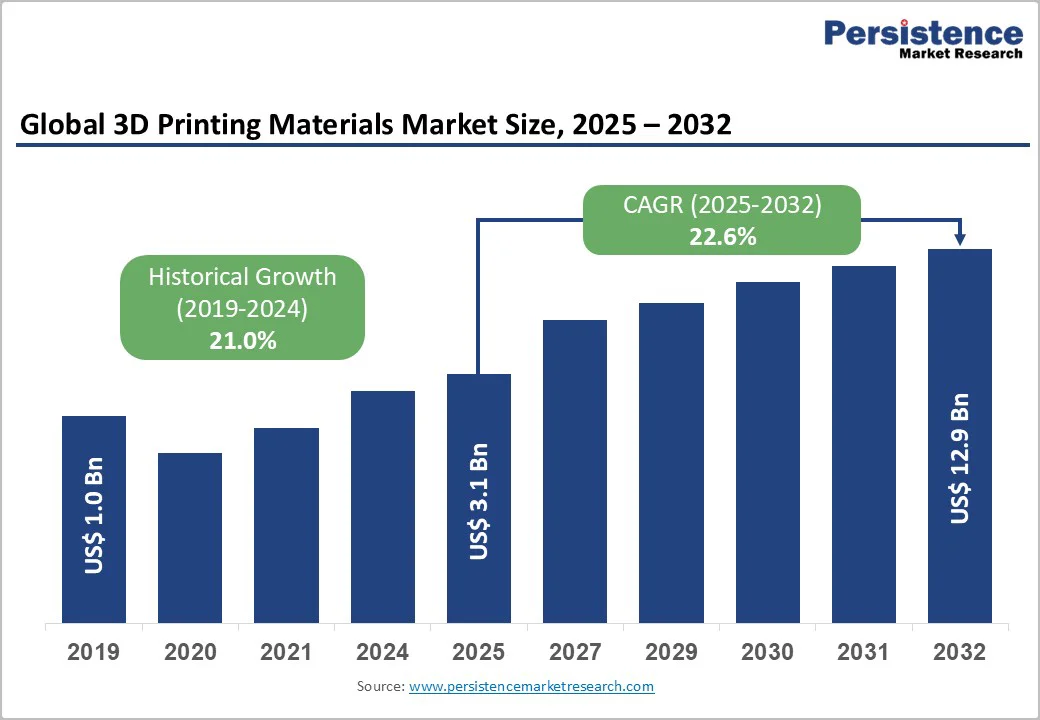

The global 3D printing materials market size is valued at US$ 3.1 billion in 2025 and is projected to reach US$ 12.9 billion by 2032, growing at a CAGR of 22.6% between 2025 and 2032.

This remarkable expansion is driven by rapidly accelerating adoption of additive manufacturing across aerospace, automotive, and healthcare sectors, where lightweight component manufacturing and rapid prototyping capabilities deliver substantial cost savings and design flexibility. Market growth is further catalyzed by continuous material science innovations including high-performance thermoplastics, metal alloys, and biocompatible polymers that expand application possibilities, coupled with government-backed advanced manufacturing initiatives and increasing supply from polymer manufacturers through vertical integration strategies.

Key Market Highlights

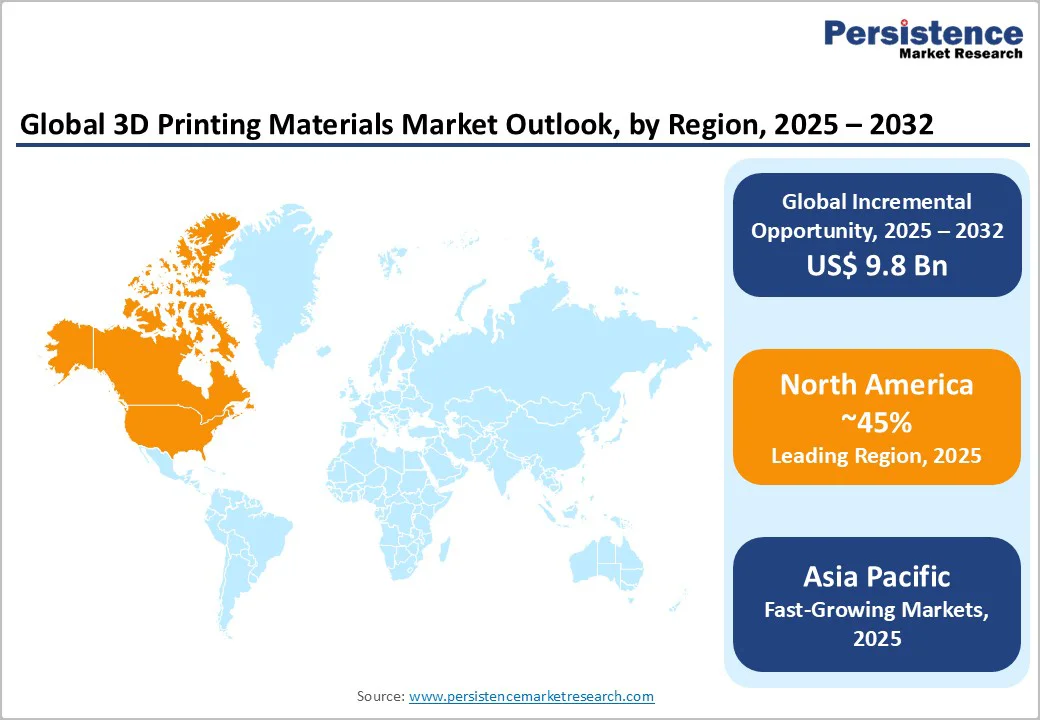

- Leading Region: North America dominates with approximately 45% market share in 2025, driven by robust aerospace and defense industries, substantial government research investment, and a comprehensive ecosystem of manufacturers and early-adopting companies across automotive, healthcare, and consumer goods sectors.

- Fastest Growing Region: Asia Pacific projects the fastest regional growth at approximately 28.5% CAGR through 2032, driven by government-backed manufacturing initiatives in China, rapid industrialization in India, and strategic manufacturing hub development across ASEAN nations.

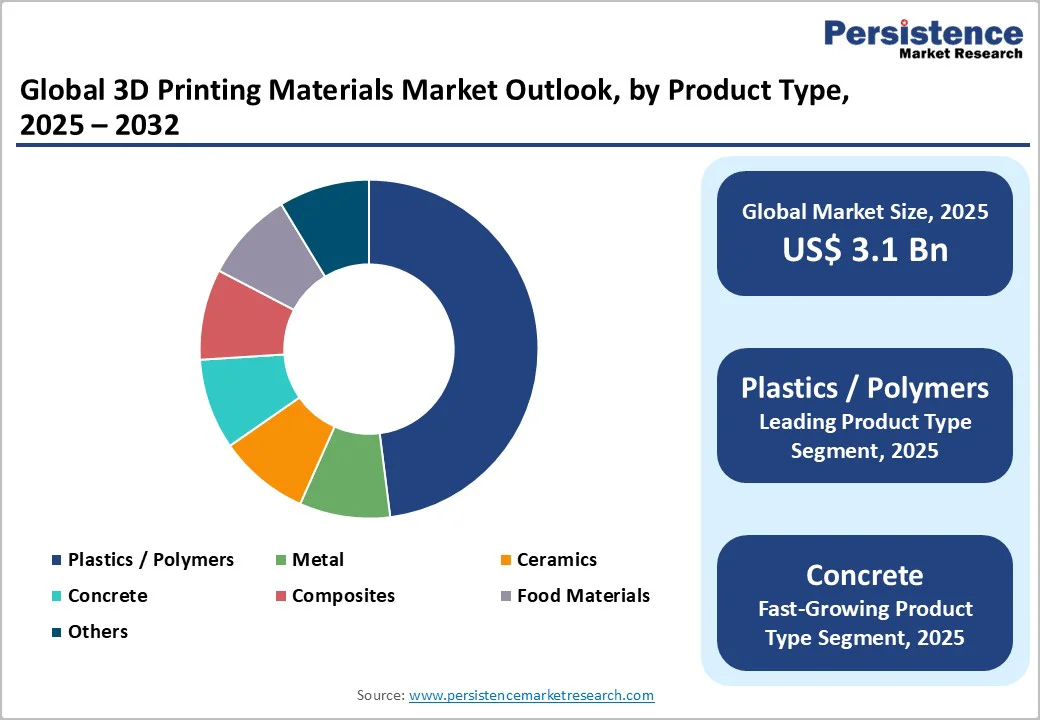

- Dominant Segment: Plastics and Polymers materials maintain dominance with approximately 48% market share in 2025, driven by material versatility, cost-effectiveness, established supply chains, and broad compatibility with FDM, SLA, and SLS technologies.

- Fastest Growing Segment: Powders form demonstrates the fastest growth trajectory at approximately 24.2% CAGR through 2032, driven by expanding powder bed fusion adoption, enabling complex geometries, support-free designs, and superior mechanical properties in aerospace and industrial manufacturing.

- Key Opportunity: 3D printing Building and Construction materials represents the highest-growth opportunity supported by exceptional cost reduction potential, architectural design capabilities, and government-backed infrastructure modernization programs.

| Key Insights | Details |

|---|---|

|

3D Printing Materials Market Size (2025E) |

US$ 3.1 billion |

|

Market Value Forecast (2032F) |

US$ 12.9 billion |

|

Projected Growth CAGR(2025-2032) |

22.6% |

|

Historical Market Growth (2019-2024) |

21.0% |

Market Dynamics

Driver - Accelerating Demand for Lightweight Components in Aerospace and Automotive Applications

The aerospace and defence sector stands as a primary market catalyst, with additive manufacturing enabling production of ultra-lightweight, high-strength components that reduce aircraft weight by up to 30%, translating directly to 1-2% fuel efficiency improvements across fleet operations and generating lifetime savings for airlines. Advanced materials, including titanium alloys, aluminum-based powders, and high-performance polymers, enable the creation of complex engine geometries, structural brackets, and thermal management systems that were previously unachievable through conventional machining.

Boeing, Airbus, and GE Additive have substantially increased 3D printing investment, with engine components representing 41.8% of aerospace material demand by 2025, while component consolidation reduces part counts by up to 80%. Similarly, the automotive sector leverages additive manufacturing for electric vehicle prototyping and lightweight structural components, with leading manufacturers including Toyota, BMW, and Ford reporting 40% reductions in design cycle time through 3D printing adoption, supporting the automotive 3D printing market to expand at a 20% CAGR between 2025-2032.

Rising Adoption of Additive Manufacturing in Healthcare and Medical Device Manufacturing

Healthcare sector transformation represents a secondary but highly consequential growth driver, with 3D printing enabling the production of patient-specific implants, dental prosthetics, and bioprinted tissue scaffolds that fundamentally improve clinical outcomes while reducing manufacturing timelines. Biocompatible resins, medical-grade polymers, and specialized metal powders support customized prosthetic production that matches individual patient anatomy, driving the healthcare 3D printing market to reach US$ 20 billion by 2032 at a 23% CAGR. Applications spanning dental implants, orthopedic implants, surgical guides, and regenerative tissue scaffolds demonstrate consistent clinical validation, with hospitals increasingly establishing in-house bioprinting labs to enable point-of-care production.

Restraints - High Material Costs and Manufacturing Complexity Limiting Widespread Industrial Adoption

Specialized 3D printing materials, including high-performance polymers, aerospace-grade metal alloys, and biocompatible resins, command premium pricing compared to conventional manufacturing inputs, with some specialized materials exhibiting cost structures 3-5 times higher than traditional alternatives.

Material-related costs comprise approximately 35-40% of total 3D printing production expenses, creating significant barriers for cost-sensitive manufacturing applications and price-sensitive consumer markets. Supply chain dependencies on specialty chemical suppliers and limited secondary material recycling infrastructure further constrain cost reduction opportunities, with unsintered powder waste representing 20-30% of material inputs in powder-based technologies, translating to substantial material costs that complicate production economics for mid-volume manufacturing applications.

Fragmented Regulatory Landscape and Standardization Gaps Creating Market Uncertainty

The rapid advancement of 3D printing technologies has substantially outpaced regulatory framework development, creating inconsistent qualification requirements across aerospace, medical device, and high-performance industrial applications. Absence of uniform international standards for material certification, process validation, and quality assurance procedures introduces complexity and extended timelines for new material introduction, particularly within aerospace and healthcare, where regulatory approval pathways remain fragmented across different jurisdictions. ISO and ASTM International continue developing standards for additive manufacturing materials and processes, yet regulatory gaps persist, particularly for novel material compositions, metal alloy specifications, and biocompatible polymer certifications, creating uncertainty that delays technology adoption and increases market entry costs for innovative material suppliers.

Opportunities - Growing Adoption of 3D Printing in Building and Construction for Complex Architectural Applications

The construction technology sector represents an emerging opportunity segment with 3D printing demonstrating exceptional potential for reducing labor costs by 50-80%, construction time by 50-75%, and material waste by 30-60% compared to traditional building methods. Concrete materials, composite formulations, and specialty adhesive systems engineered specifically for construction-scale additive manufacturing are experiencing rapid adoption, with the 3D printing building construction market projected to reach US$ 15 billion by 2032 at an unprecedented 65% CAGR.

The technology enables the production of complex architectural geometries that would be prohibitively expensive through conventional construction methods, supporting designer creativity while delivering dramatic cost reductions. Government programs in China and Singapore actively promote additive manufacturing adoption for urban housing development and infrastructure modernization, establishing expanding demand for specialized construction materials.

Expansion of Bio-based and Sustainable 3D Printing Materials Addressing Environmental Priorities

Sustainability imperatives across manufacturing industries are driving accelerating demand for environmentally-responsible 3D printing materials including bio-based polymers, recyclable thermoplastics, and closed-loop material recycling systems. Materials manufacturers are launching innovative formulations incorporating recycled content, plant-based feedstocks, and fully biodegradable polymers that address growing regulatory requirements and corporate sustainability commitments while maintaining performance characteristics required for industrial applications.

Arkema introduced Orgasol PA12 powders with outstanding recyclability features reducing material variable costs by up to 50%, while Covestro expanded its portfolio with sustainable thermoplastic polyurethane formulations and low-smoke flame-retardant materials addressing aerospace safety requirements. The integration of bio-based raw materials including polycaprolactone derived from renewable sources, and development of advanced recycling systems enabling powder reuse for up to five printing cycles significantly improve environmental credentials while establishing cost reduction pathways.

Category-wise Analysis

Product Type Insights

Plastics and Polymers materials maintain market leadership with approximately 48% market share in 2025, driven by exceptional versatility, cost-effectiveness, and broad compatibility with established 3D printing technologies including Fused Deposition Modeling (FDM), Stereolithography (SLA), and Selective Laser Sintering (SLS). The category encompasses diverse formulations, including photopolymers growing at 17% CAGR through 2032, thermoplastic polyurethanes with exceptional elastomeric properties, and engineering-grade composites of polyamides including PA11 and PA12 variants engineered for high-strength applications. Material innovation in photopolymers has expanded application possibilities significantly, with biocompatible resin formulations enabling medical device production and specialty formulations offering enhanced thermal resistance, flame retardancy, and chemical resistance, meeting stringent aerospace and industrial requirements.

Form Analysis

The Powders form segment demonstrates fastest growth momentum at approximately 24% CAGR through 2032, driven by expanding adoption of powder bed fusion technologies including Selective Laser Sintering, Multi Jet Fusion, and Direct Metal Laser Sintering across aerospace, automotive, and industrial manufacturing applications. Powder-based technologies enable the production of fully functional parts with complex internal geometries, mechanical interlocking features, and support-free designs previously unachievable through 3D printing filament approaches, while substantially reducing material waste through powder recycling programs, enabling reuse of unsintered material for up to five consecutive print cycles. 3D printing metal powders including titanium alloys, aluminum-based formulations, and nickel superalloys, command premium pricing reflecting sophisticated atomization processes and rigorous quality specifications. The powder segment benefits from increasing equipment manufacturer investment in powder bed fusion technology development, with GKN Powder Metallurgy, Höganäs AB, and emerging suppliers expanding production capacity and developing innovative material formulations optimized for industrial-scale manufacturing, establishing favorable supply-demand dynamics supporting accelerated segment growth throughout the forecast period.

Technology Insights

Fused Deposition Modeling (FDM) technology holds approximately 42% market share in 2025 across the 3D printing materials market, reflecting the technology's exceptional ease-of-use, material versatility, minimal infrastructure requirements, and established ecosystem of compatible equipment, software, and service providers. FDM technology dominates desktop and industrial 3D printing markets through accessibility, with materials including PLA (Polylactic Acid), ABS (Acrylonitrile Butadiene Styrene), PETG (Polyethylene Terephthalate Glycol), and advanced engineering thermoplastics delivering practical performance characteristics for rapid prototyping, functional testing, and low-volume production applications. Material availability, cost-effectiveness, and established supply chains supporting FDM systems from consumer-focused providers to industrial equipment manufacturers, including Ultimaker, Stratasys, and Markforged reinforce market leadership, while continuous material innovation expanding high-temperature, flexible, and reinforced polymer offerings sustains competitive positioning.

Industry Insights

Aerospace & Defence sector holds approximately 38% market share in 2025 among end-use industries, establishing a commanding market position through exceptional material requirements, rigorous performance specifications, and industry willingness to invest in advanced manufacturing technologies delivering competitive advantages through weight reduction, design optimization, and supply chain efficiency improvements. Aerospace applications spanning engine components, structural elements, heat management systems, and airframe components drive demand for titanium alloys, aluminum-based powders, nickel superalloys, and high-performance polymers, including PEEK (Polyetheretherketone) and PEKK (Polyetherketoneketone) materials.

Material innovation addressing aerospace-specific requirements including extreme temperature performance, radiation resistance, and fatigue strength optimization continues driving engagement between aerospace manufacturers and 3D printing material suppliers, establishing sustained demand growth for premium-performing aerospace-qualified materials throughout the forecast period.

Regional Insights

North America 3D Printing Materials Market Trends & Analysis

North America established a dominant position commanding approximately 45% global market share in 2025, anchored by the region's exceptional ecosystem of technology providers, equipment manufacturers, material specialists, and early-adopting industries in aerospace, automotive, healthcare, and consumer goods sectors. The United States dominates regional market dynamics, benefiting from substantial government investment in additive manufacturing research and development through programs including America Makes partnership framework providing collaborative research funding, National Science Foundation advanced manufacturing initiatives, and Department of Defense technology demonstration programs supporting development of mission-critical 3D printing applications.

The region's leadership in aerospace and defense manufacturing drives exceptional demand for advanced material systems, with companies like Boeing and Lockheed Martin extensively using 3D printing for structural components and specialized systems, establishing a stable demand pipeline for premium materials. Emerging opportunities in medical device manufacturing and in-home personalized healthcare solutions further strengthen regional growth prospects, with hospitals and surgical centers increasingly establishing additive manufacturing facilities supporting on-demand production of patient-specific implants and surgical tools.

Europe 3D Printing Materials Market Trends

Europe represents second largest market for global 3D printing materials in 2025, establishing strong competitive positioning for additive manufacturing across industrial sectors. Germany leads European market dynamics as a global additive manufacturing innovation center, with companies including EOS, Concept Laser, and SLM Solutions pioneering metal additive manufacturing technologies and driving material development collaboration with aerospace and automotive suppliers, including Airbus, Siemens, and specialty chemical manufacturers.

The United Kingdom and France contribute substantial market activity through government-backed manufacturing initiatives promoting digital transformation and advanced production technologies, while the European Union's Industrial Strategy emphasizes additive manufacturing as critical capability for future manufacturing competitiveness, establishing regulatory support favoring technology adoption. Aerospace industry consolidation and defense modernization programs drive sustained demand for specialized materials meeting EASA (European Union Aviation Safety Agency) certification requirements and military performance specifications, establishing a stable growth trajectory for advanced aerospace-qualified materials throughout the forecast period.

Asia Pacific 3D Printing Materials Market Trends

Asia Pacific region projects fastest growth momentum at approximately 28.5% CAGR through 2032, driven by rapid industrialization, government support for advanced manufacturing technologies, and expanding demand for customized manufacturing solutions in automotive, healthcare, and consumer electronics sectors. China establishes a dominant regional position through government-backed Made in China 2025 strategic initiative promoting “3D printed in China” moment in manufacturing industries. Japan contributes in material innovation focusing on precision manufacturing and high-performance applications, with companies including Evonik and GKN Powder Metallurgy establishing regional technical centers supporting aerospace, automotive, and medical device applications.

India emerges as high-growth opportunity market with additive manufacturing materials market projected to grow at 26.1% CAGR through 232. The market is driven by government’s Make in India initiatives, healthcare industry modernization supporting medical device manufacturing, and emerging aerospace sector development. ASEAN nations, including Singapore and Vietnam establish emerging manufacturing hubs through government-backed digital transformation programs and strategic positioning as regional manufacturing centers, creating expanding opportunities for material suppliers serving industrial and consumer goods applications throughout the region.

Competitive Landscape

The 3D printing materials market demonstrates a moderately consolidated competitive structure characterized by specialized material suppliers maintaining strong competitive positions in distinct technology segments and application areas, while larger diversified chemical companies increasingly expand additive manufacturing material portfolios through acquisition and organic development strategies. Leading companies, including Covestro AG, Stratasys Ltd., 3D Systems Corporation, and Materialise NV maintain competitive advantages through vertically-integrated capabilities spanning material development, equipment manufacturing, software solutions, and application engineering services, establishing ecosystem control advantages and customer lock-in effects supporting premium pricing strategies.

Market entry barriers reflect substantial R&D investment requirements for material qualification, regulatory compliance and certification procedures, particularly in aerospace and medical device applications, intellectual property protection through proprietary formulations and manufacturing processes, and technical service requirements supporting industrial-scale deployment. Strategic partnerships between equipment manufacturers and material suppliers increasingly define competitive dynamics, with Stratasys and Materialise establishing formal collaboration frameworks, and emerging technology platforms creating material specification requirements, establishing differentiation opportunities for specialized suppliers.

Key Market Developments

- September 2024: Stratasys Ltd. and Materialise NV collaborate to develop the Stratasys Neo Build Processor for Investment Casting, delivering up to 50% faster file processing and printing speeds for complex pattern production, reducing investment casting production timelines from weeks to days and demonstrating 75%-time savings compared to traditional manufacturing methods.

- November 2024: Arkema Inc. introduced advanced Orgasol PA12 powders engineered for high-performance 3D printing with outstanding powder recyclability characteristics, reducing material variable costs by up to 50% through improved powder reuse efficiency and enhanced surface quality.

- December 2024: Biomedical researchers at the University of Queensland published groundbreaking research demonstrating successful alveolar bone regeneration using 3D-printed patient-specific polycaprolactone scaffolds, establishing clinical validation for complex bone regeneration applications and demonstrating potential for widespread adoption in dental implant preparation and maxillofacial surgery procedures.

Companies Covered in 3D Printing Materials Market

- Covestro AG

- Ultimaker B.V.

- Materialise NV

- GKN Powder Metallurgy

- Höganäs AB

- Kennametal Inc.

- Arkema Inc.

- CRP Technology

- Stratasys Ltd.

- SABIC

- Polyone Corporation

- ATI Materials

- CNPC Powder

- CyBe Construction

- Markforged Inc.

- 3D Systems Corporation

- EOS GmbH

- Evonik Industries

- BASF SE

- Nano Dimension Ltd.

Frequently Asked Questions

The global market is valued at US$ 3.1 billion in 2025 and projected to reach US$ 12.9 billion by 2032 at 22.6% CAGR.

Key drivers include aerospace demand for lightweight components, healthcare applications for patient-specific implants, automotive electric vehicle development, rapid prototyping adoption, and government support for advanced manufacturing initiatives.

Plastics and Polymers maintain dominance with approximately 48% market share in 2025, led by photopolymers growing at 17% CAGR.

North America commands approximately 45% global market share, driven by robust aerospace and defense industries, substantial government research investment, and comprehensive manufacturing ecosystems.

The Building and Construction sector represents the largest opportunity, projected to expand from US$ 0.99 billion in 2025 to US$ 13.81 billion by 2029 at 93.2% CAGR with exceptional cost reduction and design capabilities.