- Executive Summary

- Global POU Water Purifier Market Snapshot, 2026 and 2033

- Market Opportunity Assessment, 2026 - 2033, US$ Bn

- Key Market Trends

- Future Market Projections

- Specialty Clinics Market Insights

- Industry Developments and Key Market Events

- PMR Analysis and Recommendations

- Market Overview

- Market Scope and Definition

- Market Dynamics

- Drivers

- Restraints

- Opportunity

- Key Trends

- Macro-Economic Factors

- Global Sectorial Outlook

- Global GDP Growth Outlook

- COVID-19 Impact Analysis

- Forecast Factors - Relevance and Impact

- Value Added Insights

- Treatment Type Adoption Analysis

- Regulatory Landscape

- Value Chain Analysis

- Key Deals and Mergers

- PESTLE Analysis

- Porter’s Five Force Analysis

- Global POU Water Purifier Market Outlook:

- Key Highlights

- Market Size (US$ Bn) and Y-o-Y Growth

- Absolute $ Opportunity

- Market Size (US$ Bn) Analysis and Forecast

- Historical Market Size (US$ Bn) Analysis, 2020-2025

- Market Size (US$ Bn) Analysis and Forecast, 2025-2033

- Global POU Water Purifier Market Outlook: By Product Type

- Introduction / Key Findings

- Historical Market Size (US$ Bn) Analysis, By Product Type,2020-2025

- Market Size (US$ Bn) Analysis and Forecast, By Product Type, 2026- 2033

- Under The Counter Filters

- Counter Top Filters

- Pitcher Filters

- Faucet-mounted Filters

- Free-Standing Water Purifiers

- Others

- Market Attractiveness Analysis: By Product Type

- Global POU Water Purifier Market Outlook: By Category Type

- Introduction / Key Findings

- Historical Market Size (US$ Bn) Analysis, By Category Type,2020-2025

- Market Size (US$ Bn) Analysis and Forecast, By Category Type, 2026- 2033

- RO Filters

- UV Filters

- Gravity Filters

- Activated Carbon

- Ion Exchange

- Others

- Market Attractiveness Analysis: Indication

- Global POU Water Purifier Market Outlook: By Application

- Introduction / Key Findings

- Historical Market Size (US$ Bn) Analysis, By Application,2020-2025

- Market Size (US$ Bn) Analysis and Forecast, By Application, 2026- 2033

- Residential

- Non-Residential

- Light Commercial

- Others

- Market Attractiveness Analysis: Indication

- Key Highlights

- Global POU Water Purifier Market Outlook: Region

- Key Highlights

- Historical Market Size (US$ Bn) Analysis, By Region,2020-2025

- Market Size (US$ Bn) Analysis and Forecast, By Region, 2026- 2033

- North America

- Europe

- East Asia

- South Asia and Oceania

- Latin America

- Middle East & Africa

- Market Attractiveness Analysis: Region

- North America POU Water Purifier Market Outlook:

- Key Highlights

- Historical Market Size (US$ Bn) Analysis, By Market,2020-2025

- By Country

- By Product Type

- By Category Type

- By Application

- Market Size (US$ Bn) Analysis and Forecast, By Country, 2026- 2033

- U.S.

- Canada

- Market Size (US$ Bn) Analysis and Forecast, By Product Type, 2026- 2033

- Under The Counter Filters

- Counter Top Filters

- Pitcher Filters

- Faucet-mounted Filters

- Free-Standing Water Purifiers

- Others

- Market Size (US$ Bn) Analysis and Forecast, By Category Type, 2026- 2033

- RO Filters

- UV Filters

- Gravity Filters

- Activated Carbon

- Ion Exchange

- Others

- Global POU Water Purifier Market Outlook: By Application

- Introduction / Key Findings

- Historical Market Size (US$ Bn) Analysis, By Application,2020-2025

- Market Size (US$ Bn) Analysis and Forecast, By Application, 2026- 2033

- Residential

- Non-Residential

- Light Commercial

- Others

- Market Attractiveness Analysis: Indication

- Europe POU Water Purifier Market Outlook:

- Key Highlights

- Historical Market Size (US$ Bn) Analysis, By Market,2020-2025

- By Country

- By Product Type

- By Category Type

- By Application

- Market Size (US$ Bn) Analysis and Forecast, By Country, 2026- 2033

- Germany

- France

- U.K.

- Italy

- Spain

- Russia

- Türkiye

- Rest of Europe

- Market Size (US$ Bn) Analysis and Forecast, By Product Type, 2026- 2033

- Under The Counter Filters

- Counter Top Filters

- Pitcher Filters

- Faucet-mounted Filters

- Free-Standing Water Purifiers

- Others

- Market Size (US$ Bn) Analysis and Forecast, By Category Type, 2026- 2033

- RO Filters

- UV Filters

- Gravity Filters

- Activated Carbon

- Ion Exchange

- Others

- Global POU Water Purifier Market Outlook: By Application

- Introduction / Key Findings

- Historical Market Size (US$ Bn) Analysis, By Application,2020-2025

- Market Size (US$ Bn) Analysis and Forecast, By Application, 2026- 2033

- Residential

- Non-Residential

- Light Commercial

- Others

- Market Attractiveness Analysis: Indication

- East Asia POU Water Purifier Market Outlook:

- Key Highlights

- Historical Market Size (US$ Bn) Analysis, By Market,2020-2025

- By Country

- By Product Type

- By Category Type

- By Application

- Market Size (US$ Bn) Analysis and Forecast, By Country, 2026- 2033

- China

- Japan

- South Korea

- Market Size (US$ Bn) Analysis and Forecast, By Product Type, 2026- 2033

- Under The Counter Filters

- Counter Top Filters

- Pitcher Filters

- Faucet-mounted Filters

- Free-Standing Water Purifiers

- Others

- Market Size (US$ Bn) Analysis and Forecast, By Category Type, 2026- 2033

- RO Filters

- UV Filters

- Gravity Filters

- Activated Carbon

- Ion Exchange

- Others

- Global POU Water Purifier Market Outlook: By Application

- Introduction / Key Findings

- Historical Market Size (US$ Bn) Analysis, By Application,2020-2025

- Market Size (US$ Bn) Analysis and Forecast, By Application, 2026- 2033

- Residential

- Non-Residential

- Light Commercial

- Others

- Market Attractiveness Analysis: Indication

- South Asia & Oceania POU Water Purifier Market Outlook:

- Key Highlights

- Historical Market Size (US$ Bn) Analysis, By Market,2020-2025

- By Country

- By Product Type

- By Category Type

- By Application

- Market Size (US$ Bn) Analysis and Forecast, By Country, 2026- 2033

- India

- Southeast Asia

- ANZ

- Rest of South Asia & Oceania

- Market Size (US$ Bn) Analysis and Forecast, By Product Type, 2026- 2033

- Under The Counter Filters

- Counter Top Filters

- Pitcher Filters

- Faucet-mounted Filters

- Free-Standing Water Purifiers

- Others

- Market Size (US$ Bn) Analysis and Forecast, By Category Type, 2026- 2033

- RO Filters

- UV Filters

- Gravity Filters

- Activated Carbon

- Ion Exchange

- Others

- Global POU Water Purifier Market Outlook: By Application

- Introduction / Key Findings

- Historical Market Size (US$ Bn) Analysis, By Application,2020-2025

- Market Size (US$ Bn) Analysis and Forecast, By Application, 2026- 2033

- Residential

- Non-Residential

- Light Commercial

- Others

- Market Attractiveness Analysis: Indication

- Latin America POU Water Purifier Market Outlook:

- Key Highlights

- Historical Market Size (US$ Bn) Analysis, By Market,2020-2025

- By Country

- By Product Type

- By Category Type

- By Application

- Market Size (US$ Bn) Analysis and Forecast, By Country, 2026- 2033

- Brazil

- Mexico

- Rest of Latin America

- Market Size (US$ Bn) Analysis and Forecast, By Product Type, 2026- 2033

- Under The Counter Filters

- Counter Top Filters

- Pitcher Filters

- Faucet-mounted Filters

- Free-Standing Water Purifiers

- Others

- Market Size (US$ Bn) Analysis and Forecast, By Category Type, 2026- 2033

- RO Filters

- UV Filters

- Gravity Filters

- Activated Carbon

- Ion Exchange

- Others

- Global POU Water Purifier Market Outlook: By Application

- Introduction / Key Findings

- Historical Market Size (US$ Bn) Analysis, By Application,2020-2025

- Market Size (US$ Bn) Analysis and Forecast, By Application, 2026- 2033

- Residential

- Non-Residential

- Light Commercial

- Others

- Market Attractiveness Analysis: Indication

- Middle East & Africa POU Water Purifier Market Outlook:

- Key Highlights

- Historical Market Size (US$ Bn) Analysis, By Market,2020-2025

- By Country

- By Product Type

- By Category Type

- By Application

- Market Size (US$ Bn) Analysis and Forecast, By Country, 2026- 2033

- GCC Countries

- Egypt

- South Africa

- Northern Africa

- Rest of Middle East & Africa

- Market Size (US$ Bn) Analysis and Forecast, By Product Type, 2026- 2033

- Under The Counter Filters

- Counter Top Filters

- Pitcher Filters

- Faucet-mounted Filters

- Free-Standing Water Purifiers

- Others

- Market Size (US$ Bn) Analysis and Forecast, By Category Type, 2026- 2033

- RO Filters

- UV Filters

- Gravity Filters

- Activated Carbon

- Ion Exchange

- Others

- Global POU Water Purifier Market Outlook: By Application

- Introduction / Key Findings

- Historical Market Size (US$ Bn) Analysis, By Application,2020-2025

- Market Size (US$ Bn) Analysis and Forecast, By Application, 2026- 2033

- Residential

- Non-Residential

- Light Commercial

- Others

- Market Attractiveness Analysis: Indication

- Competition Landscape

- Market Share Analysis, 2024

- Market Structure

- Competition Intensity Mapping by Market

- Competition Dashboard

- Company Profiles (Details - Overview, Financials, Strategy, Recent Developments)

- A. O. Smith Corporation

- Overview

- Segments and Treatment Types

- Key Financials

- Market Developments

- Market Strategy

- Brita LP

- Pentair PLC

- Culligan International Company

- Unilever PLC

- Panasonic Corporation

- LG Electronics

- Helen of Troy Limited

- Best Water Technology Group

- Kent RO Systems Ltd.

- iSpring Water Systems LLC

- The 3M Company

- Honeywell International Inc.

- General Electric Company

- A. O. Smith Corporation

- Appendix

- Research Methodology

- Research Assumptions

- Acronyms and Abbreviations

- Home Care & Utilities

- POU Water Purifier Market

POU Water Purifier Market Size, Share, and Growth Forecast, 2026 - 2033

POU Water Purifier Market by Product Type (Manual Gearbox Housing, Automatic Gearbox Housing, Others), Category (Automotive Gearbox Housing, Aerospace Gearbox Housing, Others), and Regional Analysis for 2026 - 2033

POU Water Purifier Market Size and Trends Analysis

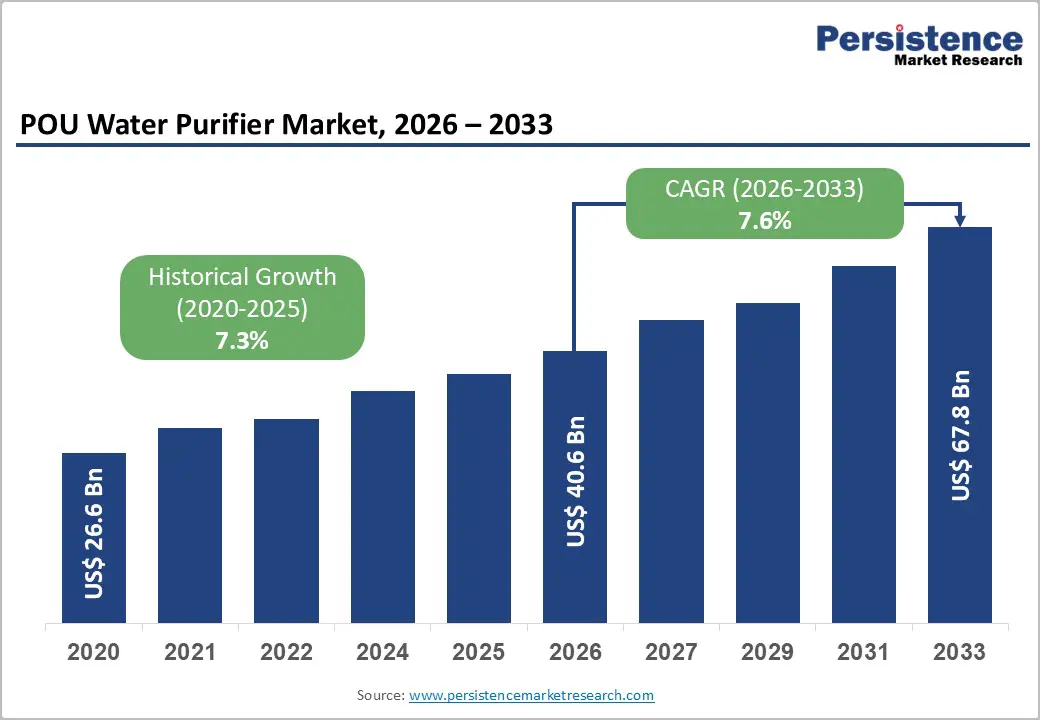

The global POU water purifier market size is likely to be valued at US$40.6 billion in 2026 and is expected to reach US$67.8 billion by 2033, growing at a CAGR of 7.6% during the forecast period from 2026 to 2033, driven by increasing awareness of water quality and health concerns.

Rising urbanization, population growth, and the prevalence of waterborne diseases have amplified the demand for reliable point-of-use purification solutions. Consumers are increasingly seeking convenient, household-level systems that provide safe drinking water, leading to widespread adoption of advanced filtration technologies such as reverse osmosis, ultraviolet, and multi-stage combination systems. Technological innovations, including smart features, app-based monitoring, and eco-friendly designs, are fueling market expansion. Distribution through e-commerce platforms and subscription-based filter replacement services has improved accessibility.

Key Industry Highlights:

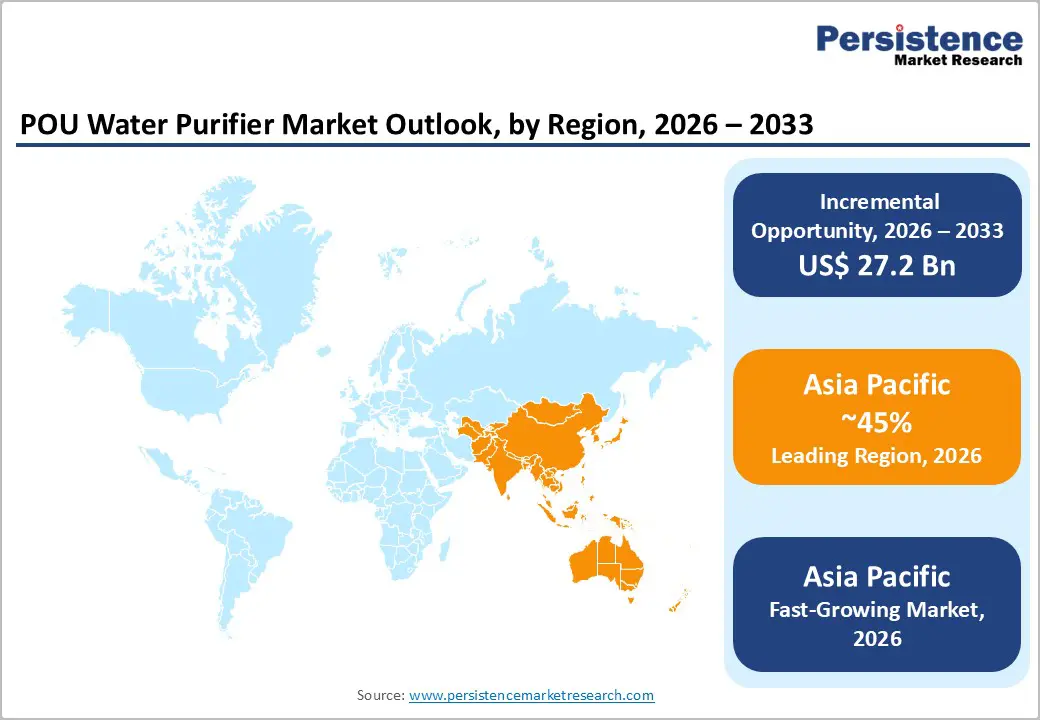

- Leading Region: Asia Pacific is anticipated to be the leading region, accounting for a market share of 45% in 2026, driven by rapid urbanization, rising health awareness, water scarcity, and increasing adoption of advanced POU water purification technologies.

- Fastest-growing Region: Asia Pacific is likely to be the fastest-growing region, supported by increasing population density, heightened awareness of waterborne diseases, and rising adoption of smart and efficient purification systems.

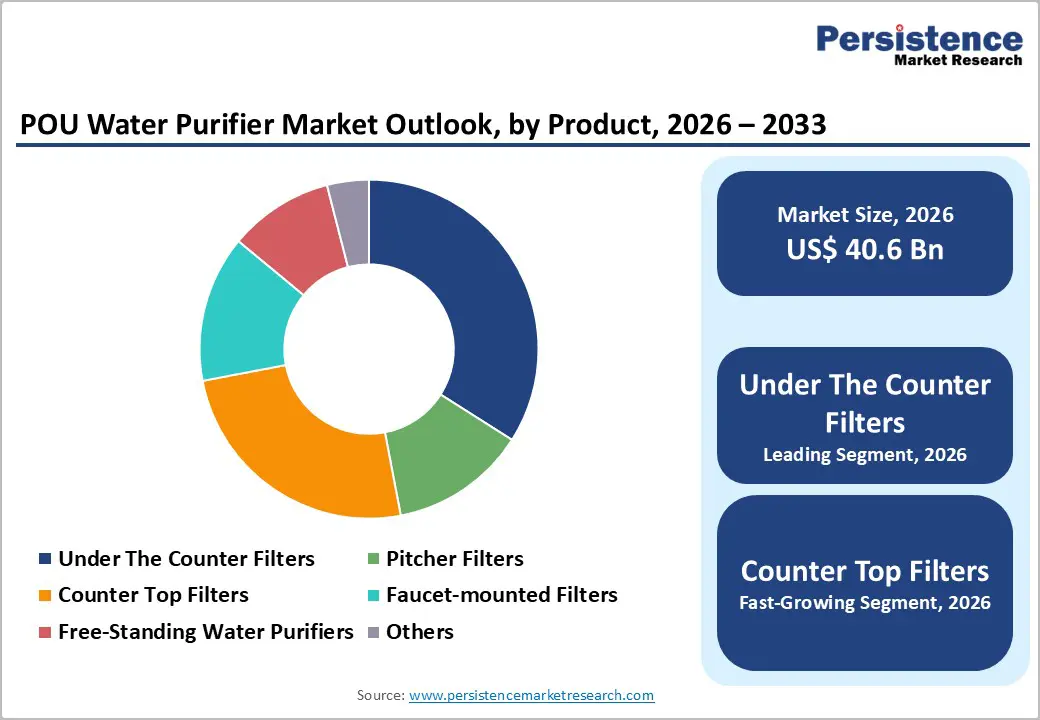

- Leading Product Type: Under-the-counter filters are projected to represent the leading product type in 2026, accounting for 40% of the revenue share, driven by high capacity, seamless kitchen integration, and consistent performance in residential settings.

- Leading Category: RO filters are anticipated to be the leading category type, accounting for over 50% of the revenue share in 2026, supported by their effectiveness in removing dissolved solids, heavy metals, and other contaminants, particularly in high TDS regions.

| Key Insights | Details |

|---|---|

|

POU Water Purifier Market Size (2026E) |

US$40.6 Bn |

|

Market Value Forecast (2033F) |

US$67.8 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

7.6% |

|

Historical Market Growth (CAGR 2020 to 2025) |

7.3% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis- Increasing Awareness of Waterborne Diseases and Health Risks

Consumers are becoming increasingly conscious of contaminants such as bacteria, viruses, heavy metals, and chemical pollutants in drinking water, especially in urban and semi-urban regions. This heightened awareness is prompting households and institutions to invest in reliable purification solutions. Educational campaigns, media coverage of water contamination incidents, and government advisories reinforce the need for safe drinking water. Demand for point-of-use water purifiers that provide immediate, household-level purification is growing steadily, driving market expansion.

The health-focused consumer mindset also encourages adoption of advanced technologies such as RO, UV, and multi-stage filtration systems, which are perceived as effective against a wide range of contaminants. Parents, caregivers, and health-conscious individuals increasingly prioritize water safety, particularly in regions with poor municipal water quality. This awareness has led to increased purchases of certified and branded purifiers, creating sustained revenue streams for manufacturers. Urban migration and population density intensify exposure to contaminated water sources, reinforcing the market growth.

Technological Advancements and Regulatory Support

Advanced filtration technologies, including RO, UV, and combination systems, enhance water quality and user convenience. Integration with smart features such as IoT connectivity, filter-life monitoring, and app-based water quality alerts improves consumer experience and drives adoption. Regulatory support and government initiatives promoting safe drinking water strengthen market growth. Standards for product quality and certification encourage consumer trust in branded systems, facilitating wider acceptance. These innovations and supportive policies collectively enable manufacturers to offer reliable, efficient, and user-friendly solutions, increasing market penetration.

Manufacturers are investing in R&D to develop compact, energy-efficient, and low-maintenance units, catering to both residential and light commercial applications. Regulatory frameworks, such as water safety certifications and performance standards, provide guidance and ensure compliance, enhancing credibility. Government campaigns and subsidies for clean water access indirectly promote POU purifier adoption, especially in developing regions. The combination of technological enhancements and structured regulatory backing accelerates innovation and enhances consumer confidence.

Barrier Analysis - Regulatory Hurdles and Certification Delays

Manufacturers must comply with diverse national and regional standards for water safety, filtration efficiency, and product quality. Lengthy approval processes can delay product launches and increase time to market, impacting revenue. In some regions, inconsistent or unclear regulatory guidelines create challenges for new entrants, especially smaller companies. These delays can limit the availability of innovative solutions in the market and discourage investment. Regulatory bottlenecks remain a critical factor that can restrain market growth, particularly in emerging economies with evolving compliance frameworks.

Such delays also affect consumer trust and market competitiveness. If certified products are scarce, buyers may opt for low-quality alternatives, impacting brand reputation and market penetration. The complexity of obtaining multiple certifications for different regions increases operational costs and slows expansion plans. Manufacturers may also face penalties for noncompliance, deterring new innovations. While demand for POU purifiers grows, regulatory hurdles and certification delays can restrict the speed at which advanced, safe, and efficient systems reach consumers, tempering overall market growth.

Technical Limitations in Certain Technologies

Certain POU purification technologies face inherent technical limitations, which restrain market growth. UV filters require electricity and clear water to effectively disinfect, while RO systems produce wastewater and may remove essential minerals. Gravity-based and activated carbon filters may not eliminate all microbial contaminants or dissolved solids, limiting their effectiveness in areas with highly polluted water. These technical shortcomings can influence consumer perception and adoption, as buyers seek reliable, all-encompassing solutions. Manufacturers must address these limitations through hybrid systems or innovative designs, but inherent constraints in some technologies continue to act as a growth barrier for the market.

Technical limitations also affect maintenance requirements and operational costs. Systems with higher complexity may require frequent filter replacement, energy input, or periodic servicing, which can deter price-sensitive consumers. The need for proper installation and skilled operation for some technologies limits accessibility in rural or resource-constrained regions. While innovation is helping mitigate certain drawbacks, the persistence of technology-specific limitations can reduce user confidence, slow adoption rates, and challenge manufacturers to balance efficiency, cost, and convenience in delivering effective point-of-use water purification solutions.

Opportunity Analysis - Technological Convergence with Smart Features

The integration of smart technologies presents a significant growth opportunity in the POU water purifier market. IoT-enabled systems, mobile app monitoring, automatic filter replacement alerts, and real-time water quality tracking enhance convenience and user experience. Consumers increasingly prefer devices that provide actionable data, energy efficiency, and remote monitoring capabilities. Technological convergence enables manufacturers to differentiate their products, tap into tech-savvy demographics, and offer premium solutions. The growing trend of smart homes and digital adoption reinforces the potential of connected water purifiers, making this convergence a strategic opportunity for market expansion across residential and light commercial segments.

Smart features also support predictive maintenance, reducing downtime and extending system lifespan, which appeals to long-term consumers. Integration with home automation platforms allows seamless operation and monitoring, increasing adoption among urban households. By combining traditional filtration technologies with advanced sensors, connectivity, and user-friendly interfaces, manufacturers can provide enhanced value propositions. This convergence not only improves user satisfaction but also encourages recurring revenue through subscription-based filter replacements and software upgrades, positioning the POU water purifier market for accelerated growth.

Sustainability and Eco-Friendly Innovations

Consumers are increasingly prioritizing environmentally responsible products that reduce plastic waste, energy consumption, and water wastage. Manufacturers are developing low-waste filtration systems, biodegradable filter materials, and energy-efficient purifiers to meet this demand. Eco-conscious designs enhance brand perception and appeal to a growing segment of environmentally aware buyers. Regulations promoting sustainable water solutions encourage the adoption of green technologies. These trends enable companies to differentiate their offerings and capture new customer segments.

Environmental considerations also include water-saving technologies in RO systems, compact designs to minimize resource usage, and longer lasting filters to reduce waste. Green marketing strategies and certifications can enhance consumer trust and loyalty, while collaborations with sustainability initiatives strengthen market positioning. The push toward eco-friendly products aligns with broader efforts to conserve resources and ensure safe drinking water. By incorporating sustainable innovations, manufacturers can address both environmental and consumer needs, opening avenues for product development and premium offerings.

Category-wise Analysis

Product Type Insights

Under the counter filters are expected to lead the POU water purifier market, accounting for approximately 40% of revenue in 2026, driven by seamless kitchen integration, higher purification capacity, and consistent performance in residential applications. These systems are preferred in urban households where aesthetics and space optimization are important considerations. Installed directly beneath sinks, they provide continuous filtered water without occupying countertop space, making them suitable for modern modular kitchens. For example, under-sink systems offered by A. O. Smith Corporation are widely adopted in metropolitan areas due to reliable purification and durable design.

Counter-top filters are likely to represent the fastest-growing segment, supported by ease of installation, portability, and affordability, making these systems highly attractive for rental homes, compact apartments, and temporary residences. Unlike permanent installations, countertop units require minimal plumbing modification, which broadens their accessibility among consumers seeking flexible solutions. For example, countertop filtration solutions from Brita LP have gained popularity among urban renters due to convenience and user-friendly operation.

Category Type Insights

RO filters are projected to lead the market, capturing around 50% of the revenue share in 2026, supported by their high effectiveness in removing dissolved solids, heavy metals, chemical contaminants, and microbial impurities, making them particularly suitable for regions with high TDS levels and polluted water sources. These systems are commonly integrated into under-sink and multi-stage purifiers to deliver superior water quality. For example, Kent RO Systems Ltd. has established a strong presence in markets with challenging water conditions by offering advanced RO-based solutions.

UV filters are likely to be the fastest-growing category type, driven by energy-efficient operation, absence of wastewater generation, and strong effectiveness in microbial disinfection. UV technology is particularly valued in areas where biological contamination is a primary concern and where water conservation is critical. UV systems are increasingly integrated with RO technology to create hybrid purification solutions that enhance overall efficiency. For example, Panasonic Corporation offers UV-based purification systems designed to provide reliable microbial protection while maintaining operational simplicity. Rising environmental awareness, demand for sustainable purification methods, and preference for low-maintenance solutions are accelerating adoption.

Regional Insights

North America POU Water Purifier Market Trends

North America is likely to be a significant market for POU water purifiers in 2026, driven by heightened consumer focus on water quality and stringent regulatory standards for safe drinking water. Increasing concerns over contaminants such as lead, chlorine, and emerging pollutants such as pharmaceuticals and microplastics have stimulated demand for advanced purification technologies among households and commercial users. Consumers increasingly favor multi-stage filtration solutions that combine reverse osmosis (RO), ultraviolet (UV), and activated carbon technologies to address a broad spectrum of contaminants.

Innovation and product differentiation are the key trends shaping the North American POU water purifier market. Manufacturers are integrating smart features such as real-time digital monitoring, IoT connectivity, and filter life indicators that notify users when replacements are due, enhancing convenience and long-term performance. For example, Brita LP has expanded its portfolio in North America with innovative countertop and pitcher filters incorporating advanced activated carbon and ion exchange technologies, appealing to environmentally conscious buyers.

Europe POU Water Purifier Market Trends

Europe is likely to be a significant market for POU water purifiers, due to consumers increasingly prioritizing water quality and sustainability. Heightened awareness of contaminants such as heavy metals, chlorine, and pesticide residues in tap water has driven demand for point-of-use purification solutions across residential and light commercial segments. Environmental consciousness is particularly strong in European markets, leading buyers to prefer systems that minimize wastewater and utilize eco-friendly materials. Regulations and standards related to potable water quality in the European Union encourage the adoption of certified purification technologies, ensuring safe and compliant products.

Technological innovation and premiumization are the key trends shaping the European POU water purifier landscape. Manufacturers are focusing on advanced filtration technologies such as multi-stage RO, UV, and hybrid systems that can address a wide spectrum of contaminants while maintaining environmental efficiency. For example, Philips has introduced UV-based purification systems in select European markets that combine enhanced microbial disinfection with sleek, modern designs, appealing to health-focused and design-savvy households.

Asia Pacific POU Water Purifier Market Trends

The Asia Pacific region is anticipated to be the leading and the fastest-growing region, accounting for a market share of 45% in 2026, driven by concerns over water quality, scarcity, and health risks intensifying across the region. Rapid urbanization, industrial pollution, and uneven access to treated municipal water have driven both residential and light commercial demand for advanced purification systems. Consumers are increasingly opting for point-of-use solutions that provide reliable protection against contaminants such as bacteria, viruses, dissolved solids, and chemical pollutants. Cultural emphasis on health and wellness reinforces the adoption of multi-stage filtration technologies, particularly in densely populated countries such as India and China.

Innovation, affordability, and product diversity are the key trends shaping the POU water purifier market in Asia Pacific. Manufacturers are tailoring offerings to regional needs by balancing performance with cost-effectiveness, making purification solutions accessible to a wider consumer base. Compact designs and plug-and-play models are particularly appealing in urban apartments and rental housing, while larger capacity systems are gaining traction in suburban and peri-urban areas. For example, Kent RO Systems Ltd. has strengthened its presence in multiple Asia Pacific markets by providing a range of products that combine reverse osmosis, UV, and UF technologies, catering to diverse water conditions and consumer preferences.

Competitive Landscape

The global POU water purifier market exhibits a moderately fragmented structure, driven by the presence of numerous regional and local manufacturers striving to innovate and expand their market footprints. A wide range of product offerings, from basic countertop filters to advanced multi-stage systems with RO, UV, and smart features, reflects varied consumer needs across regions. Rising water quality concerns, technological advancements, and increased urbanization are prompting both established brands and emerging players to introduce differentiated solutions.

With key leaders including A. O. Smith Corporation, Brita LP, Pentair PLC, Kent RO Systems Ltd., and Panasonic Corporation shaping market dynamics, competition remains robust. These players compete through continuous product innovation, strategic partnerships, and expansion of sales channels, including e-commerce, retail, and B2B networks. Emphasis on smart technologies, sustainability, and comprehensive service offerings helps brands differentiate.

Key Industry Developments:

- In February 2026, Nephros, Inc. expanded into the Puerto Rican market, offering advanced water filtration solutions for healthcare, hospitality, and foodservice sectors. The company aimed to address concerns over waterborne pathogens and infrastructure challenges with high-performance filtration systems for ice machines, drinking fountains, and sterile processing environments. Nephros planned to differentiate itself through rapid service, localized Spanish-language support, and on-site installation services.

- In July 2024, Unilever PLC sold its water purification business, Pureit, to A. O. Smith Corporation. The transaction strengthened A. O. Smith's position in the premium water treatment segment and expanded its footprint in South Asia and other key emerging markets. Pureit, known for innovations such as gravity-based purifiers and electric RO systems, had built strong brand recognition across regions, including India, Bangladesh, and Mexico.

- In September 2024, WaterBoss, a brand of A. O. Smith Corporation, launched a new whole-house filtration system in the U.S. The system, featuring activated carbon filtration, reduced up to 96.9% of chlorine taste and odor. It was designed for easy DIY installation and sold widely online and in stores, strengthening WaterBoss's presence in the residential water treatment market.

Companies Covered in POU Water Purifier Market

- A. O. Smith Corporation

- Brita LP

- Pentair PLC

- Culligan International Company

- Unilever PLC

- Panasonic Corporation

- LG Electronics

- Helen of Troy Limited

- Best Water Technology Group

- Kent RO Systems Ltd.

- iSpring Water Systems LLC

- The 3M Company

- Honeywell International Inc.

- General Electric Company

Frequently Asked Questions

The global POU water purifier market is projected to reach US$40.6 billion in 2026.

The POU water purifier market is driven by rising concerns over water contamination, increasing health awareness, rapid urbanization, and growing demand for convenient household-level water purification solutions.

The POU water purifier market is expected to grow at a CAGR of 7.6% from 2026 to 2033.

Key market opportunities include integration of smart technologies, expansion in emerging economies, development of sustainable and low-waste filtration systems, and growth of subscription-based service models.

O. Smith Corporation, Brita LP, Pentair PLC, Culligan International Company, and Unilever PLC are the leading players.