- Plastics, Polymers & Resins

- Sheet Molding Compound Market

Sheet Molding Compound Market Size, Trends, Share, and Growth Forecast 2026 - 2033

Sheet Molding Compound Market by Resin Type (Unsaturated Polyester, Vinyl Ester, Epoxy, Phenolic), by Performance Grade (General Purpose, Structural, Class-A Surface, Flame-Retardant, Electrical Insulation), Application (Exterior Body Panels, Structural Components, Electrical Enclosures, Building Panels & Facades, Housings & Covers), Industry, and Regional Analysis, for 2026 - 2033

Sheet Molding Compound Market Size and Trend Analysis

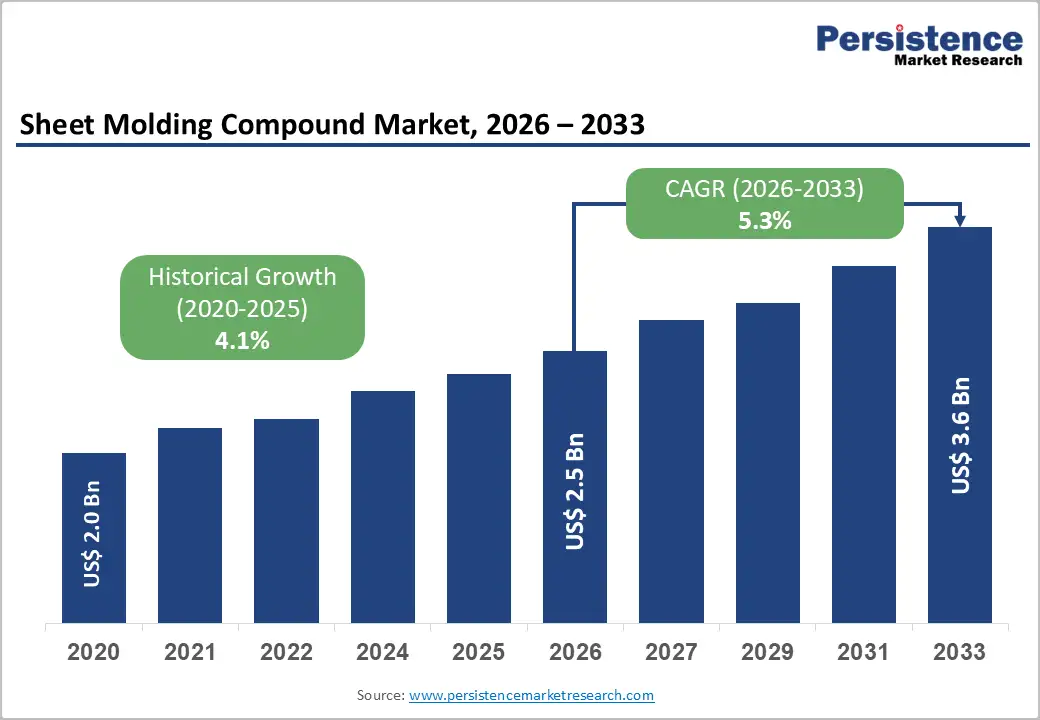

The global sheet molding compound market size is likely to be valued at US$ 2.5 billion in 2026 and is expected to reach US$ 3.6 billion by 2033, growing at a CAGR of 5.3% during the forecast period from 2026 to 2033.

This expansion is driven by the rising demand for lightweight, durable, and cost-effective composite materials across automotive, construction, and electrical industries. Innovations in resin technology and increasing adoption in electric vehicles and infrastructure projects have further accelerated the market's growth trajectory.

Key Industry Highlights:

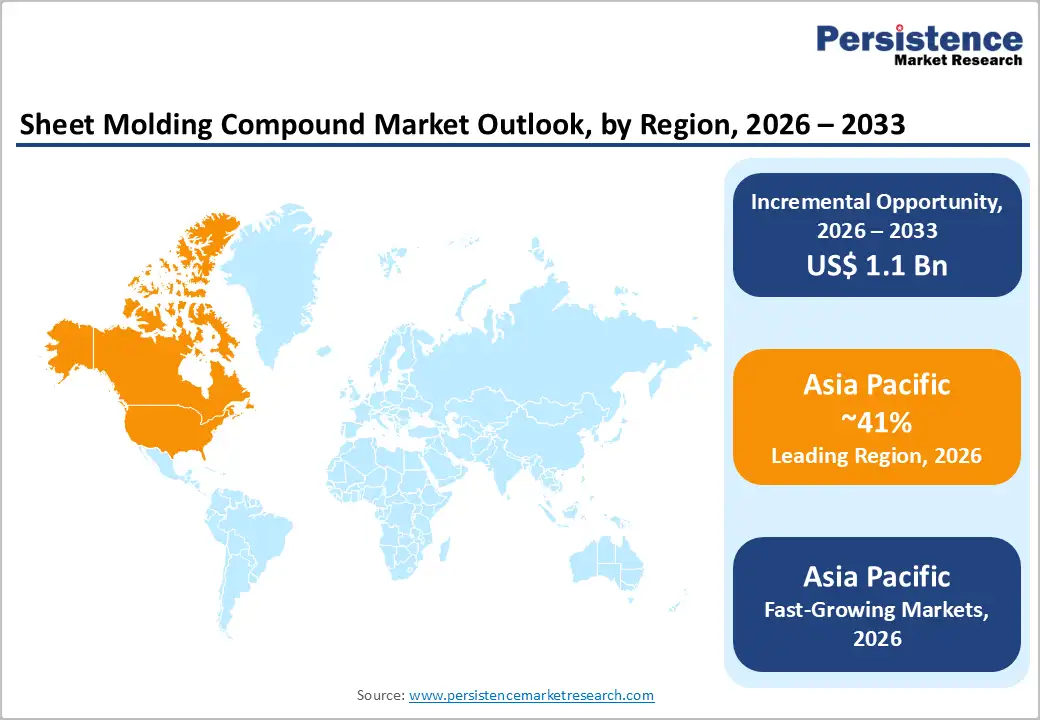

- Leading region & Fastest Growing Region: Asia Pacific leads global SMC demand holding 41% share, due to rapid industrialization, particularly in China and India, and has the highest growth rate of around 6.9%, from infrastructure projects and electric vehicle adoption.

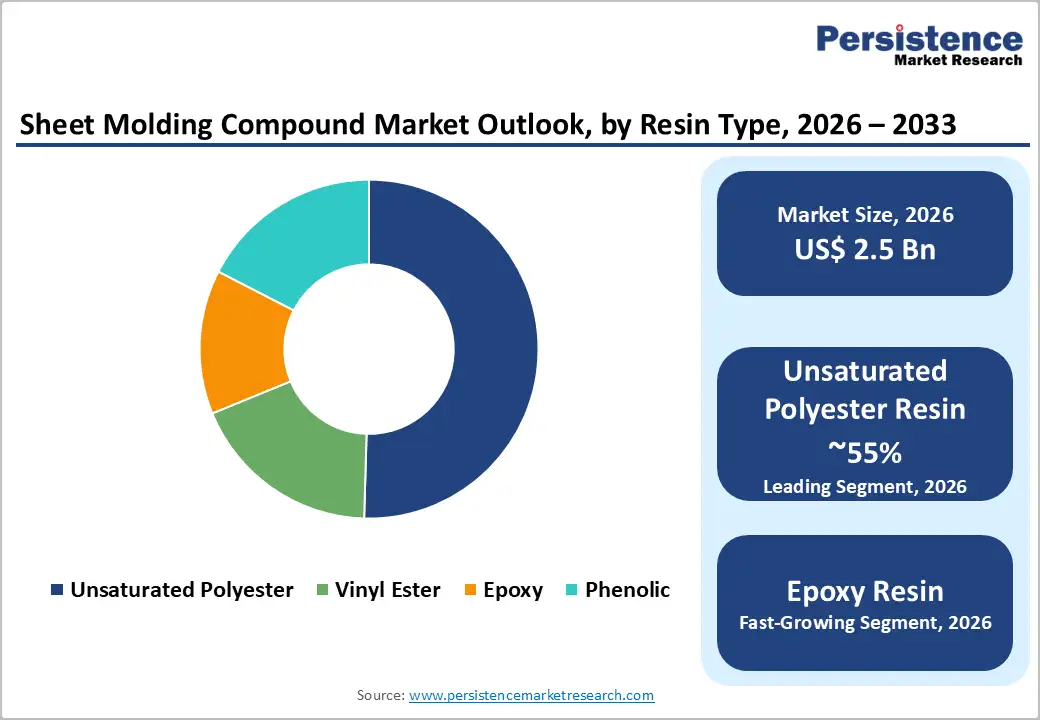

- Dominant Segment: Unsaturated Polyester Resin is the most widely used resin type, accounting for over 55% of market share.

- Fastest Growing Segment: Structural Grade SMC is experiencing the highest growth due to increasing use in automotive and aerospace sectors.

- Key Market Opportunity: Technological advancements in sustainable SMC formulations are creating new growth avenues in renewable energy and green construction.

| Key Insights | Details |

|---|---|

| Sheet Molding Compound Market Size (2026E) | US$ 2.5 Billion |

| Market Value Forecast (2033F) | US$ 3.6 Billion |

| Projected Growth CAGR (2026 - 2033) | 5.3% |

| Historical Market Growth (2020 - 2025) | 4.1% |

Market Dynamics

Drivers - Automotive Lightweighting and EV Adoption Drive Strong Demand for High-Performance Sheet Molding Compound Materials

The automotive and transportation sector continues to be the primary growth driver for the Sheet Molding Compound (SMC) market. Increasing regulatory pressure on vehicle emissions and fuel efficiency, along with growing consumer demand for sustainable mobility, is pushing manufacturers to adopt lightweight materials. SMC offers an ideal balance of weight reduction, strength, and design flexibility, making it highly attractive for modern vehicle platforms.

Currently, the automotive segment accounts for more than 50% of global SMC consumption, with electric vehicles emerging as a key growth area. Automakers are increasingly using SMC in battery enclosures, structural panels, exterior body parts, and underbody components to improve range and safety while maintaining durability.

In 2025, Teijin Automotive Technologies reinforced this trend by highlighting its role as a full-service supplier of glass-fiber SMC components such as doors, exterior panels, and structural parts. These solutions are engineered to reduce vehicle mass while delivering high-quality Class-A surfaces and structural performance, enabling OEMs to meet stringent fuel-efficiency and emissions regulations without compromising safety or durability.

Rising Infrastructure Development and Electrical Safety Requirements Accelerate SMC Adoption in Construction and Power Applications

The construction and electrical sectors are experiencing steady growth in the adoption of Sheet Molding Compound due to its durability, corrosion resistance, and design versatility. SMC is widely used in building panels, façades, electrical enclosures, cable management systems, and structural components, particularly in large-scale urban infrastructure projects. Government initiatives promoting energy-efficient buildings and sustainable construction practices are further accelerating demand for advanced composite materials such as SMC.

In the electrical segment, SMC’s excellent insulation properties, flame resistance, and dimensional stability make it a preferred material for switchgear, circuit breakers, transformers, and outdoor electrical equipment exposed to harsh environments.

In 2025, Polynt S.p.A. released technical insights highlighting the performance of its SMC formulations in battery housings and broader infrastructure applications. These solutions are designed to withstand outdoor weathering, electrical stress, and thermal fluctuations while maintaining structural integrity. This clearly demonstrates how SMC’s durability, insulating performance, and design flexibility are supporting its growing use in modern construction and electrical infrastructure.

Restraints - Fluctuating Resin and Fiber Prices Create Cost Uncertainty and Margin Pressure for Global Sheet Molding Compound Manufacturers

Price volatility of key raw materials remains a significant challenge for the Sheet Molding Compound market. SMC production relies heavily on resins, reinforcing fibers, and additives, all of which are subject to fluctuating prices driven by oil price movements, supply-demand imbalances, and global economic conditions. Sudden increases in raw material costs can raise production expenses and compress profit margins, particularly for small and mid-sized manufacturers with limited pricing power. In recent years, supply chain disruptions, geopolitical tensions, and transportation constraints have further intensified uncertainty around raw material availability and cost stability.

These factors make long-term planning and cost forecasting more difficult for manufacturers and end users. As a result, some customers may delay projects or explore alternative materials when SMC prices become less predictable. This ongoing volatility highlights the importance of supply chain diversification, long-term supplier agreements, and innovation in cost-efficient formulations to reduce the market’s exposure to raw material price fluctuations.

Growing Use of Advanced Thermoplastics and Lightweight Metals Intensifies Competitive Pressure on SMC Applications

The Sheet Molding Compound market faces increasing competition from alternative lightweight and high-strength materials, particularly advanced thermoplastics and metal alloys. Continuous innovation in thermoplastic composites has improved their strength, recyclability, and processing speed, making them attractive substitutes in certain automotive and aerospace applications. Similarly, aluminum and high-strength steel alloys continue to evolve, offering lightweight solutions with well-established supply chains and recyclability advantages.

In some applications, these materials can outperform SMC in specific technical parameters such as impact resistance, thermal conductivity, or cycle time efficiency. This competitive landscape places pressure on SMC manufacturers to differentiate their products through innovation, performance enhancement, and cost optimization. To remain competitive, SMC producers must invest in advanced formulations, improved surface quality, and sustainable material solutions. The presence of strong alternatives underscores the need for continuous R&D and strategic positioning to maintain SMC’s relevance in demanding end-use industries.

Opportunity - Innovations in Sustainable, Fire-Resistant, and Low-Emission SMC Formulations Unlock High-Growth Industrial Opportunities

Technological innovation is creating significant growth opportunities in the Sheet Molding Compound market by expanding its application range and improving performance characteristics. Advances in resin chemistry and manufacturing processes have led to the development of flame-retardant, low-VOC, and bio-based SMC formulations that align with evolving environmental regulations and customer sustainability goals. These next-generation materials are increasingly suitable for renewable energy infrastructure, green buildings, and high-performance industrial applications.

In 2025, Toray Industries, Inc. demonstrated its commitment to sustainable innovation by adopting mass-balance approaches for bio-based materials and securing ISCC PLUS certification. This enables the commercialization of composite solutions with a lower environmental footprint. Additionally, Teijin Automotive Technologies formed a strategic alliance with Aeronautical Service S.r.l. to industrialize advanced ceramic matrix composite technologies using proprietary FireAlt formulations. These materials offer exceptional fire resistance, lightweight performance, and zero toxic emissions, opening new opportunities in sectors requiring high-temperature resistance and strict safety standards, such as renewable energy and green construction.

Rapid Urbanization, EV Expansion, and Infrastructure Spending Position Asia-Pacific as the Fastest-Growing SMC Market

Asia-Pacific is emerging as the fastest-growing region for the Sheet Molding Compound market, driven by rapid urbanization, industrial expansion, and strong government investment in infrastructure development. Countries such as China, India, Japan, and South Korea are major growth engines, supported by large-scale automotive manufacturing, electric vehicle adoption, and urban construction projects. The region’s expanding middle class and increasing focus on sustainable building materials are further strengthening demand for SMC.

In 2025, LyondellBasell Industries Ltd. expanded its Advanced Polymer Solutions business in China by doubling capacity at its Dalian facility to 80,000 tonnes annually, with a dedicated production line serving automotive and infrastructure applications. Additionally, Polynt S.p.A. leveraged its long-standing success in supplying SMC solutions for electric vehicle battery enclosures across Asia-Pacific markets. These developments highlight how SMC manufacturers are scaling production and strengthening regional presence to capture the substantial opportunities created by rapid urban development, vehicle electrification, and infrastructure investment across the Asia-Pacific region.

Category-wise Analysis

Resin Type Insights

The Unsaturated Polyester Resin segment holds the largest share of the Sheet Molding Compound market, accounting for an estimated 55% in 2025. This dominance is largely due to its cost-effectiveness, versatility, and proven performance across a wide range of applications. Unsaturated polyester resins are widely used in automotive, construction, and electrical industries because they offer a balanced combination of mechanical strength, corrosion resistance, and ease of processing. Recent technological improvements have further enhanced their mechanical properties, surface finish, and compatibility with advanced fillers and reinforcements.

These innovations have improved process efficiency and product consistency, making unsaturated polyester resins even more attractive for high-volume manufacturing. Their established supply chain and broad acceptance among manufacturers continue to reinforce their leading position. As a result, this resin type remains the preferred choice for most SMC applications, particularly where cost control and reliable performance are critical decision factors.

Performance Grade Insights

Structural Grade SMC represents the largest performance segment, accounting for approximately 40% of the total market share. This segment is widely adopted in demanding applications that require high mechanical strength, stiffness, and load-bearing capability. Automotive and aerospace industries are the primary users of structural grade SMC, where it is increasingly replacing traditional materials such as steel and aluminum. Continuous research and development efforts are focused on improving fiber reinforcement, resin systems, and molding techniques to enhance structural performance and weight reduction.

These advancements are enabling SMC to meet stringent safety and durability requirements while offering greater design flexibility. Structural grade SMC also supports the production of complex geometries without compromising strength, making it ideal for next-generation vehicle platforms and high-performance components. As lightweighting and performance optimization remain top priorities across industries, demand for structural grade SMC is expected to remain strong.

Application Insights

Exterior body panels represent the largest application segment in the Sheet Molding Compound market, capturing nearly 35% of total demand. SMC is widely preferred for exterior panels due to its ability to form complex shapes, deliver excellent surface finish, and maintain consistent quality in high-volume production. These properties make it particularly suitable for automotive body panels, hoods, fenders, tailgates, and roof components. Manufacturers benefit from SMC’s design flexibility, which allows for integrated features and reduced part count, leading to cost and weight savings.

SMC provides good impact resistance and corrosion protection, enhancing vehicle durability and aesthetics. Its compatibility with Class-A surface requirements further supports its use in visible exterior applications. As automakers continue to focus on lightweighting, design differentiation, and improved production efficiency, exterior body panels are expected to remain a key application area driving SMC demand.

Industry Insights

Automotive and transportation remain the dominant industries accounting for approximately 55% of total market demand. The ongoing shift toward electric vehicles, combined with stricter emissions regulations, is significantly accelerating the adoption of lightweight composite materials. SMC plays a critical role in reducing vehicle weight while maintaining structural integrity, safety, and design flexibility. It is increasingly used in battery enclosures, underbody shields, exterior panels, and structural components for both conventional and electric vehicles.

Automakers value SMC for its ability to support mass production, integrate multiple functions into single components, and deliver consistent quality. As global vehicle manufacturers continue to invest in electric mobility and next-generation vehicle platforms, demand for SMC in the automotive and transportation sector is expected to remain strong. This trend reinforces the industry’s position as the primary driver of long-term market growth.

Regional Insights

North America Sheet Molding Compound Market Trends

North America remains a mature and innovation-driven market for Sheet Molding Compound, led primarily by the United States. The region benefits from a strong automotive industry, advanced manufacturing capabilities, and stringent environmental regulations that promote the use of lightweight and sustainable materials. The U.S. is home to several leading SMC manufacturers and research institutions, fostering continuous innovation and regulatory alignment.

In 2025, Core Molding Technologies, Inc., a major U.S.-based engineered materials company, reported significant new business wins totaling US$ 47 million in the first half of the year. These contracts span electric vehicles, aerospace, and building products across the U.S., Canada, and Mexico. To support this growth, the company announced US$ 25 million in capital investments, including plant expansions in Matamoros and a new facility in Monterrey, Mexico. These initiatives highlight North America’s strong demand outlook and commitment to expanding SMC capacity and technological capabilities.

Europe Sheet Molding Compound Market Trends

Europe continues to demonstrate strong demand for sheet molding compound, particularly in Germany, the U.K., France, and Spain. The region’s advanced automotive manufacturing base and well-established construction sector are key drivers of SMC adoption. European regulatory frameworks emphasizing sustainability, emissions reduction, and circular economy principles are encouraging manufacturers to adopt eco-friendly SMC formulations. Germany stands out as a hub for innovation in high-performance composites and composite recycling technologies.

In 2025, Wacker Chemie AG strengthened its position in the European SMC market by expanding production capabilities for sustainable polymer resin binders and advanced materials. These initiatives target renewable energy infrastructure and support manufacturers in meeting European Union sustainability regulations. Wacker’s innovation hub in Germany continues to develop high-performance composite solutions for automotive and construction applications. This reflects Europe’s strong focus on environmentally responsible materials and advanced composite technologies.

Asia Pacific Sheet Molding Compound Market Trends

Asia Pacific is the fastest-growing region for the sheet molding compound market, led by China, Japan, India, and ASEAN countries. Rapid industrialization, large-scale urbanization, and strong government support for electric vehicles and infrastructure development are major drivers of growth. The region’s competitive manufacturing environment and cost advantages continue to attract investments from global SMC producers.

In 2025, Mitsubishi Chemical Group expanded its operations across the Asia Pacific, including polypropylene compounding and industrial gas facilities in India, while announcing plans to enter India’s semiconductor and electric vehicle supply chains. Additionally, LyondellBasell Industries Ltd. expanded its Advanced Polymer Solutions compounding capacity at its Dalian facility in China to 80,000 tonnes annually, with dedicated output for automotive and infrastructure applications. These investments highlight Asia Pacific’s position as a key growth hub for composite materials, supported by rising EV adoption, infrastructure spending, and strong government policy support.

Competitive Landscape

The global sheet molding compound market is moderately concentrated, characterized by the presence of established global players alongside numerous regional manufacturers. Leading companies such as LyondellBasell Industries Ltd., Toray Industries, Inc., Polynt S.p.A., Ashland Inc., Mitsubishi Chemical Holdings Corporation, Teijin Limited, Wacker Chemie AG, Core Molding Technologies, Inc., and IDI Composites International dominate the market through strong research and development capabilities, broad product portfolios, and extensive global distribution networks.

These companies focus on innovation, sustainability, and capacity expansion to maintain their competitive positions. At the same time, emerging regional players are targeting cost-effective solutions and local market penetration, increasing competitive intensity. This combination of global leadership and regional specialization is driving continuous innovation, price competition, and product differentiation across the SMC market, supporting its steady long-term growth.

Key Market Developments

- In June, 2025: Ashland Inc launched a new low-density, high-performance SMC formulation (Arotran 771) with specific gravity of 1.2, targeting automotive lightweighting and green building applications where superior mechanical properties and cost-effectiveness are required for sustainable construction materials

- In March, 2025: Teijin Automotive Technologies expanded SMC production capacity in China by commencing commercial operations at its Changzhou facility (39,000 square meters) and constructing a third plant in Shenyang to meet growing demand from electric vehicle manufacturers.

- In February, 2025: Polynt S.p.A. reinforced its comprehensive flame-retardant SMC portfolio meeting UL94 V0 standards and developed specialized grades for electrical and power applications, including halogen-free formulations for switchgear, circuit breakers, and outdoor electrical equipment requiring superior fire performance and electrical insulation properties.

Companies Covered in Sheet Molding Compound Market

- LyondellBasell Industries Ltd.

- TORAY INDUSTRIES, INC

- Polynt S.p.A.

- Ashland Inc, Premix Inc.

- Mitsubishi Chemical Holdings Corporation

- TEIJIN LIMITED

- Wacker Chemie AG

- ASTAR S.A.

- Core Molding Technologies, Inc.

- IDI Composites International

- National Composites

- MENZOLIT

- Zhejiang Yueqing SMC & BMC Manufacture Factory

- Huayuan Advanced Materials Co., Ltd.

Frequently Asked Questions

The global sheet molding compound market is projected to reach US$ 2.5 Billion by 2026 and US$ 3.6 Billion by 2033.

Key drivers include lightweighting in automotive, growth in construction and electrical applications, and technological advancements in SMC formulations.

The Unsaturated Polyester Resin segment is the largest, with over 55% market share due to its versatility and cost-effectiveness.

Asia Pacific is the largest and fastest-growing region, driven by industrialization and urbanization in countries like China and India.

Major opportunities include sustainable SMC formulations, infrastructure growth in Asia-Pacific, and increasing adoption in electric vehicles.

Leading companies include LyondellBasell Industries Ltd., TORAY INDUSTRIES, INC, Polynt S.p.A., Ashland Inc, Premix Inc., Mitsubishi Chemical Holdings Corporation, TEIJIN LIMITED, Wacker Chemie AG, ASTAR S.A.