- Plastics, Polymers & Resins

- Medical Plastic Compounds Market

Medical Plastic Compounds Market Size, Share, and Growth Forecast 2026 - 2033

Medical Plastic Compounds Market by Material Type (Polyvinyl Chloride, Acrylics, Polyethylene, Polypropylene, Polystyrene, Polyester, Polycarbonate, Polyurethane, Others), Application (Disposables, Catheters, Surgical Instruments, Medical Bags, Implants, Drug Delivery Systems, Others), and Regional Analysis for 2026 - 2033

Medical Plastic Compounds Market Size and Trend Analysis

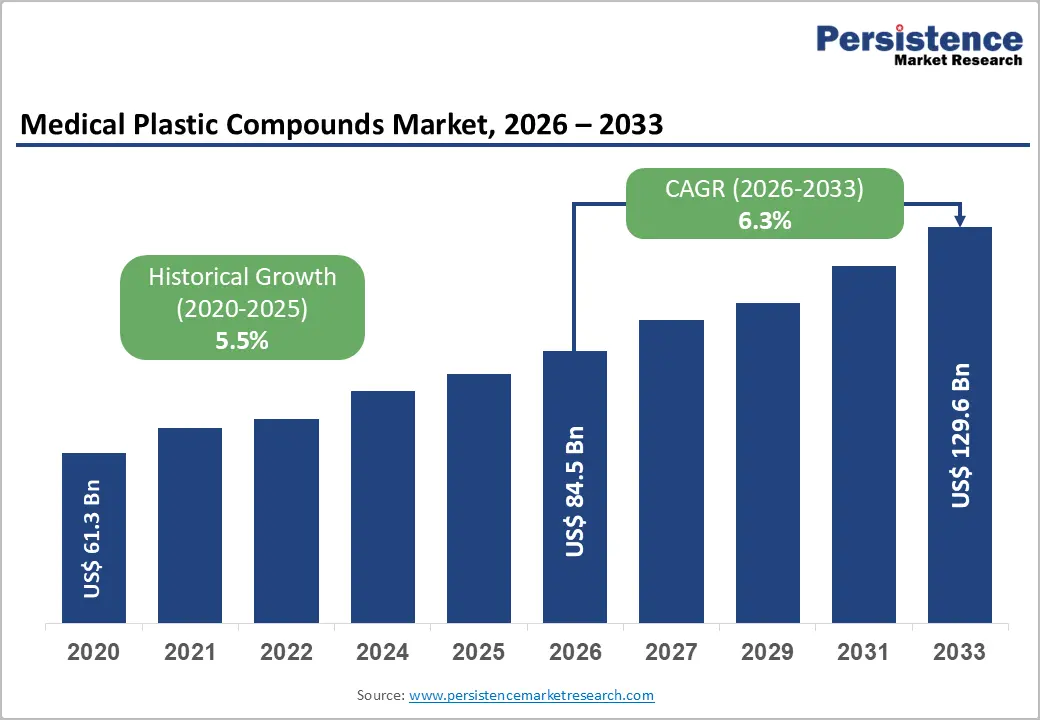

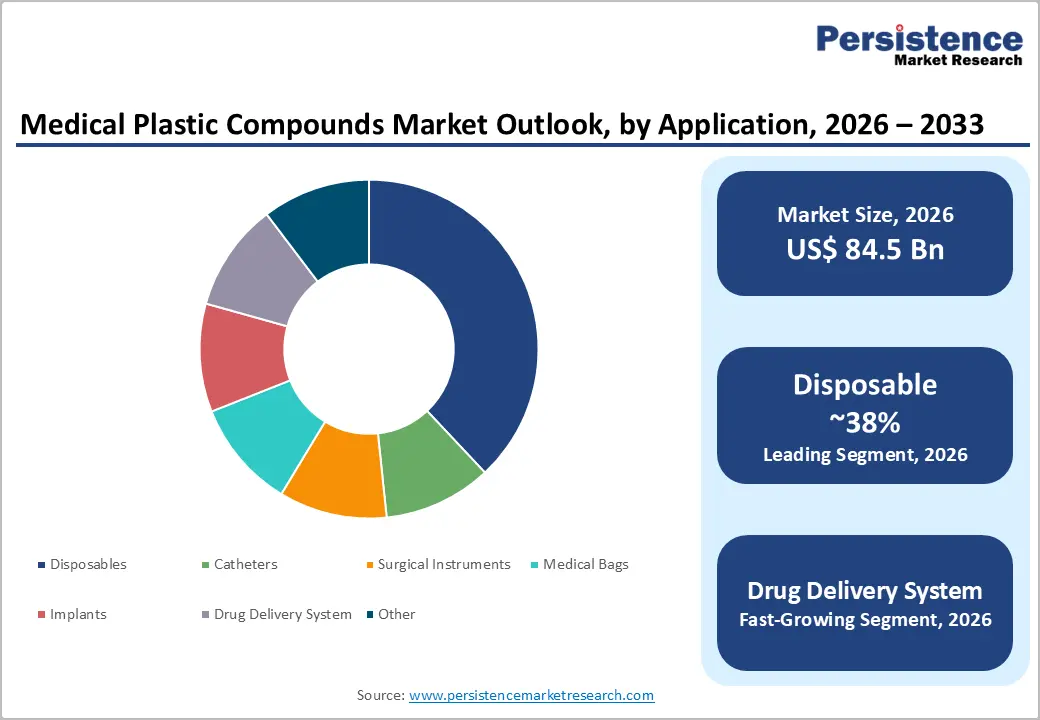

The global medical plastic compounds market size is valued at US$ 84.5 billion in 2026 and is projected to reach US$ 129.6 billion by 2033, growing at a CAGR of 6.3% between 2026 and 2033. Medical plastic compounds are experiencing durable demand growth, anchored in the global healthcare sector's deepening reliance on high-performance polymers for devices, drug delivery systems, and single-use medical equipment.

The World Health Organization (WHO) estimates that the global population aged 60 and above will double to 2.1 billion by 2050, driving chronic disease management needs that directly translate into sustained medical device and plastic compound procurement.

Key Industry Highlights:

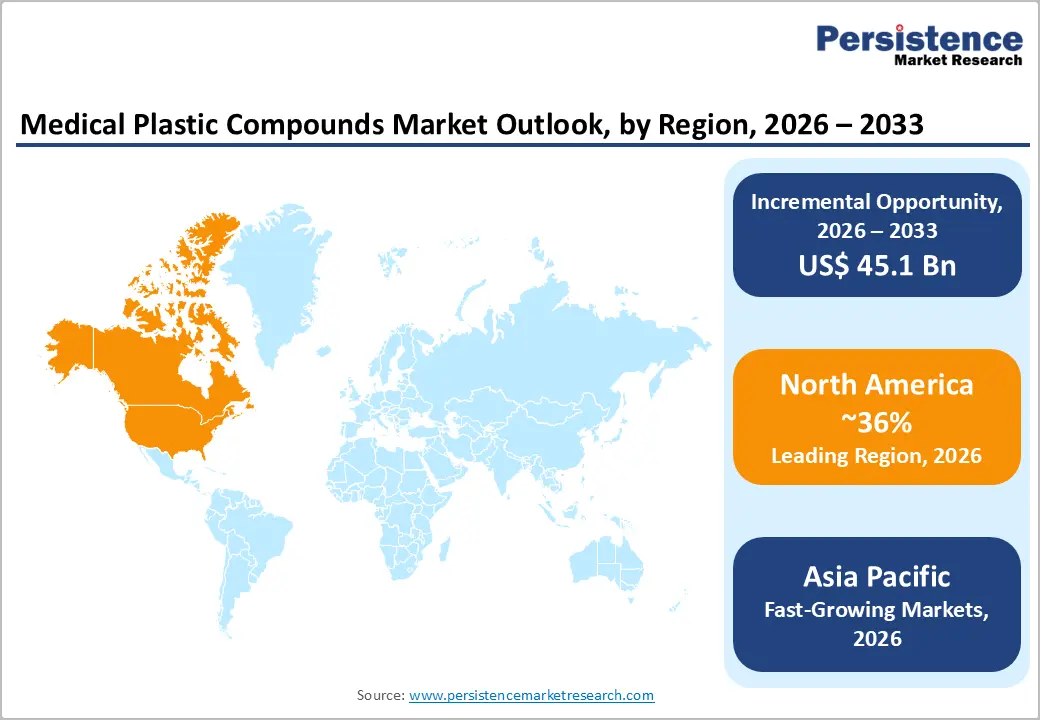

- Regional Leader: North America leads the global medical plastic compounds market with approximately 36% revenue share in 2025, anchored by the U.S.'s US$ 4.9 trillion healthcare spending, 6,500+ domestic medical device companies, and FDA/ISO 10993 biocompatibility frameworks compelling premium compound procurement from BASF, Dow, Celanese, and Eastman.

- Fastest Growing Region: Asia Pacific is the fastest-growing region through 2033, driven by China's 14th Five-Year Plan healthcare expansion, India's AB-PMJAY 500-million-beneficiary health insurance program, and PLI medical device incentives, and Japan's world-leading aging population intensity, sustaining the highest per-capita medical device consumption globally.

- Leading Material Type: PVC (Polyvinyl Chloride) dominates the Material Type category with approximately 34% market share in 2025, driven by its unmatched combination of processability, chemical resistance, biocompatibility track record, and cost across IV bags, catheters, blood bags, tubing, and oxygen delivery devices at industrial volumes.

- Fast-Growing Application: Drug Delivery Systems represent the fastest-growing Application segment, propelled by bioresorbable polymer drug-eluting platforms, FDA Breakthrough Device Program acceleration of bioresorbable implants, and the global expansion of biologics administration systems requiring specialized polymer compound formulations from Evonik's RESOMER and Corbion's PURASORB platforms.

- Key Opportunities: The most compelling market opportunity lies in bioresorbable polymer compounds for implantable devices, with over 70 FDA Breakthrough Device designations in relevant categories by 2024, where Evonik, BASF, and specialty compounders can command premium per-kilogram pricing while capturing long-term OEM qualification lock-in for orthopedic, cardiovascular, and ophthalmologic applications.

DRO Analysis

Drivers - Aging Global Population Driving Chronic Disease Management Device Demand

The structural demographic shift toward older populations across developed and rapidly developing economies is the most durable fundamental demand for medical plastic compounds, as chronic disease management and neurological conditions require a continuous pipeline of plastic-component-intensive medical devices. The WHO projects that non-communicable diseases (NCDs) will account for 77% of all deaths globally by 2030, with diabetes affecting an estimated 700 million people and cardiovascular disease remaining the leading cause of mortality.

The U.S. Centers for Disease Control and Prevention (CDC) reports that 60% of American adults have a chronic disease, underpinning a structurally non-cyclical domestic procurement base for medical plastic compounds that has no meaningful downside scenario over the forecast horizon.

Single-Use Medical Device Adoption Institutionalized by Infection Control Protocols

The global healthcare sector's permanent shift toward single-use medical devices is generating sustained and structurally embedded volume demand for disposable medical plastic compounds. The Centers for Disease Control and Prevention (CDC)'s Healthcare Infection Control Practices Advisory Committee guidelines and WHO's injection safety protocols both mandate single-use devices for sharps, syringes, catheters, and IV administration sets, creating regulatory-backed demand that is immune to cyclical healthcare spending pressures.

The Association for the Advancement of Medical Instrumentation (AAMI) has documented that reusable device reprocessing failures remain a persistent patient safety concern, further institutionalizing single-use adoption across hospital procurement committees. The disposables application segment, which constitutes the largest revenue category in the medical plastic compounds market, is served predominantly, making these material types the primary beneficiaries of single-use device growth.

Restraints - Extended Biocompatibility Testing Timelines Adding Development Costs

The medical plastic compounds market is subject to the most stringent regulatory frameworks governing any polymer application, with FDA 21 CFR Part 177, ISO 10993 biocompatibility testing standards, and the EU Medical Device Regulation (MDR 2017/745) collectively mandating extensive preclinical testing before any new compound can be incorporated into a regulated medical device. Full ISO 10993 compliance typically requires 18-36 months of cytotoxicity, sensitization, irritation, and systemic toxicity testing, adding significant time and cost to new compound development cycles.

The EU MDR, which replaced the Medical Device Directive (MDD) in 2021, introduced substantially more rigorous clinical evidence requirements that have created compliance backlogs at Notified Bodies across Europe, delaying product launches and increasing the time-to-market cost burden for compound manufacturers supplying newly registered device formulations.

Sustainability Pressure and Regulatory Action Against PVC and Phthalate Plasticizers

Despite Polyvinyl Chloride (PVC)'s dominance in medical plastic applications, the material faces mounting regulatory and institutional pressure driven by concerns about phthalate plasticizers, particularly DEHP (di-2-ethylhexyl phthalate), which has been classified as a Substance of Very High Concern (SVHC) under the EU REACH Regulation.

The European Chemicals Agency (ECHA) has published authorization decisions restricting DEHP use in medical devices for sensitive patient populations, including neonates and pregnant women, compelling device manufacturers to qualify alternative plasticizer systems. This substitution requirement creates short-to-medium-term formulation complexity and qualification cost for PVC compound suppliers, while simultaneously opening opportunities for alternative materials, including polyurethane, cyclic olefin copolymers (COC), and phthalate-free PVC grades, a transition that adds cost and extends qualification timelines.

Opportunities - Biocompatible Polymer Platforms for Next-Generation Implants and Drug Delivery

The development and commercialization of bioresorbable and biocompatible polymer platforms represents one of the highest-growth and highest-margin opportunity frontiers in medical plastic compounds. The growth is driven by the expanding clinical adoption of biodegradable implants, drug-eluting stents, resorbable sutures, and controlled-release drug delivery systems. PLLA, PGLA, and PCL are establishing clinical track records in orthopedic fixation, cardiovascular scaffolding, and ophthalmology.

The FDA's Breakthrough Device Program has accelerated approval pathways for bioresorbable implant technologies, with over 70 breakthrough designations granted in relevant device categories as of 2024, compressing clinical development timelines and bringing bioresorbable compound-intensive products to market faster than traditional pathways. Evonik Industries and Corbion are among the established suppliers of medical-grade bioresorbable polymer compounds, and the segment's inherently high per-kilogram value positions it as a structurally margin-accretive growth vector for incumbent compounders.

Healthcare Expansion Demands High-Volume in Emerging Markets

The rapid expansion of formal healthcare infrastructure across China, India, Southeast Asia, and the Middle East is creating the most significant volume growth opportunity. India's Ayushman Bharat Pradhan Mantri Jan Arogya Yojana (AB-PMJAY) program, the world's largest government health insurance scheme covering 500 million beneficiaries, is generating procurement of medical devices and single-use plastic-intensive supplies at a scale that is compelling domestic compound manufacturing investment.

China's 14th Five-Year Plan explicitly targets healthcare service capacity expansion, with hospital bed targets and medical device localization policies driving compound procurement from domestic suppliers, including Sinopec and international players including BASF, SABIC, and Dow, operating local production. The U.S.-China trade tensions and reshoring incentives under the Biosecure Act considerations are simultaneously incentivizing domestic U.S. and European compound capacity expansion, creating dual geographic demand drivers.

Category-wise Analysis

Material Type Insights

Polyvinyl Chloride (PVC) dominates the medical plastic compounds market by material type, commanding approximately 34% of total market share in 2025. PVC's market leadership stems from its unique combination of processability, chemical resistance, clarity, flexibility range, and low cost, which has made it the material of choice for IV bags, blood bags, tubing, catheters, and oxygen masks for over five decades. The U.S. FDA has an extensive biocompatibility database for medical-grade PVC formulations, providing compound suppliers and device OEMs with established regulatory pathways that are far more predictable than those for alternative materials.

RAUMEDIC AG, Tekni-Plex, and Teknor Apex are among the leading medical PVC compound specialists. Despite DEHP substitution pressures, REACH-compliant PVC formulations incorporating DINP, DEHT, or other approved plasticizer systems are maintaining the material's dominant position, with the transition representing a formulation upgrade cycle rather than a displacement event.

Application Insights

The disposables application segment leads the medical plastic compounds market, representing approximately 38% of total market share in 2025. This dominance reflects the healthcare sector's structural dependence on single-use plastic devices, including syringes, IV administration sets, gloves, surgical drapes, specimen containers, and collection bags, where infection control protocols, regulatory mandates, and hospital liability management collectively create non-negotiable demand volumes.

The WHO's Safe Injection Global Network (SIGN) estimates that 16 billion injections are administered annually worldwide, each requiring a single-use syringe, a statistic that alone illustrates the scale of disposable plastic compound consumption independent of all other single-use device categories. Polypropylene and polyethylene are the dominant material inputs for disposable device manufacturing, while PVC serves IV-related disposables.

Regional Analysis

North America Medical Plastic Compounds Market Trends & Analysis

North America is the leading regional market for medical plastic compounds, commanding approximately 36% of global revenue in 2025, anchored by the United States' position as the world's largest medical device market. The region's market is being shaped by the Inflation Reduction Act's pharmaceutical provisions, the proposed Biosecure Act, and broader supply chain reshoring sentiment.

U.S. Medical Plastic Compounds Market Size

The U.S. Medical Plastic Compounds market is valued at approximately US$ 26.8 Bn in 2025, driven by the world's largest installed base of medical device manufacturers, with over 6,500 medical device companies operating domestically, and healthcare spending of US$ 4.9 trillion in 2023. The FDA's active enforcement of 21 CFR Part 820 Quality System Regulation and the EU MDR-equivalent compliance requirements for export markets are compelling U.S. compound buyers to maintain strict biocompatibility documentation.

Europe Medical Plastic Compounds Market Trends, Drivers & Insights

Europe holds approximately 27% of the global Medical Plastic Compounds market revenue in 2025, characterized by the region's simultaneous roles as both a major demand center and a leading innovation hub for biocompatible and sustainable polymer compound technologies. ECHA's ongoing SVHC evaluations of phthalates and bisphenols are continuously reshaping the European compound formulation landscape, creating a rolling innovation cycle.

Germany Medical Plastic Compounds Market Size

Germany's Medical Plastic Compounds market is valued at approximately US$ 7.2 Bn in 2025, reflecting the country's position as Europe's largest medical device manufacturing economy. Germany's Medizinproduktegesetz (MPG) implementation of EU MDR and the country's Fraunhofer research network's active polymer biocompatibility research programs make Germany the European innovation epicenter for advanced medical compound development.

U.K. Medical Plastic Compounds Market Size

The U.K. Medical Plastic Compounds market is valued at approximately US$ 4.6 Bn in 2025, supported by the NHS's status as the world's fifth-largest purchaser of healthcare goods and the MHRA's post-Brexit independent regulatory pathway. The UK's Life Sciences Vision strategy and UKRI's £1 billion medical technologies investment program are stimulating domestic compound innovation, particularly in bioresorbable polymers for implantable devices.

France Medical Plastic Compounds Market Size

France's Medical Plastic Compounds market is valued at approximately US$ 3.8 Bn in 2025, supported by the Agence nationale de sécurité du médicament (ANSM)'s rigorous oversight of medical devices and France's significant medical device manufacturing base, anchored by Sanofi's device divisions, Air Liquide Healthcare, and specialized domestic OEMs.

Asia Pacific Medical Plastic Compounds Market Drivers & Analysis

Asia Pacific is the fastest-growing regional market, projected to expand at the highest CAGR through 2033, commanding approximately 28% of global revenue in 2025. China dominates the regional landscape, with domestic compound demand driven simultaneously by export-oriented device production and the 14th Five-Year Plan's healthcare capacity expansion targets.

China Medical Plastic Compounds Market Size

China's medical plastic compounds market was valued at approximately US$ 16.4 billion in 2025, reflecting the country's dual role as the world's largest medical device exporter by volume and a domestic healthcare market serving 1.4 billion people. However, U.S. tariffs on Chinese medical device components and the proposed Biosecure Act restrictions on Chinese biotech suppliers are creating headwinds for export-oriented Chinese compound producers.

India Medical Plastic Compounds Market Size

India's medical plastic compounds market was valued at approximately US$ 4.8 billion in 2025 and is among the fastest-growing national markets globally. The market is driven by the PLI scheme for medical devices, allocating Rs. 3,420 crores in incentives for domestic manufacturing, the AB-PMJAY scheme's 500 million beneficiary coverage, and India's growing medical tourism sector. SABIC, Dow India, and BASF India are among the major international compound suppliers building domestic production capacity aligned with India's device manufacturing ambitions.

Japan Medical Plastic Compounds Market Size

Japan's medical Plastic Compounds market is a mature, premium-quality-focused demand base valued at approximately US$ 5.1 billion in 2025, sustained by the country's aging population, with over 29% of citizens above 65, generating the highest per-capita medical device consumption intensity globally. The Pharmaceuticals and Medical Devices Agency (PMDA)'s rigorous compound biocompatibility documentation requirements and Mitsubishi Chemical Group Corporation's leadership in medical-grade polymer compound supply make Japan a technically sophisticated market where premium functional compounds command premium pricing.

Competitive Landscape

The global medical plastic compounds market exhibits a moderately consolidated structure at the tier-1 level, with global chemical and specialty polymer conglomerates, including BASF SE, Dow Inc., Covestro AG, Evonik Industries, SABIC, Solvay, and Celanese, commanding significant combined revenue share through broad material portfolios, global regulatory support infrastructure, and deep OEM qualification relationships. Specialist medical compounders, including RAUMEDIC AG, Tekni-Plex, and Mitsubishi Chemical, differentiate through application-specific formulation expertise and vertically integrated compound-to-tubing manufacturing. The dominant emerging trend is the integration of sustainability credentials, including recycled-content and biobased polymer compounds, into medical-grade portfolios, driven by hospital GPO sustainability mandates.

Key Developments:

- February 2026: SABIC announced the debut of its latest biocompatible medical-grade thermoplastics at the MD&M West 2026 event, targeting advanced healthcare and medical device applications. The company introduced a new family of UL746G-certified polycarbonate copolymers along with SILTEM™ HU biocompatible resins, which can potentially replace fluoropolymers in medical tubing, addressing growing regulatory pressure on PFAS-based materials.

- October 2025: SABIC announced a collaboration with Zuyderland Medical Center in the Netherlands to develop a closed-loop recycling model for hospital plastic waste, marking a breakthrough in sustainable medical materials.

- November 2025: Eastman Chemical Company announced that Medipack has adopted its Eastar™ 6763 Renew copolyester for use in sustainable medical packaging, marking a significant advancement in the medical plastic compound market.

Top Companies in Medical Plastic Compounds Market

- BASF SE (Ludwigshafen, Germany) is a global leader in specialty chemicals and one of the most influential participants in the medical plastic compounds space. With an extensive portfolio including engineering plastics, polyurethanes, and biopolymers, BASF serves medical device OEMs across implants, surgical instruments, and drug delivery systems. The company's strong R&D infrastructure and global technical service network, combined with a robust regulatory compliance capability across FDA, EMA, and ISO standards, position it as a preferred tier-one supplier to the medical sector.

- Dow Inc. (Midland, Michigan, U.S.) is a premier supplier of polyethylene, silicone-based compounds, and specialty polymer formulations for the medical industry. Dow's HEALTH+ science platform is specifically designed to deliver solutions for medical packaging, tubing, and device components. The company's vertically integrated supply chain, from monomer production to finished compound delivery, provides high cost and consistency advantages. Dow's scale, global manufacturing network, and investment in sustainable medical-grade materials make it a dominant force in the sector.

- Covestro AG (Leverkusen, Germany) specializes in high-performance polycarbonates, polyurethanes, and specialty films that find extensive application in medical device housings, blood-contact components, diagnostic platforms, and wearable devices. The company's Makrolon and Baymedix product lines are recognized benchmarks in medical-grade transparency, impact resistance, and sterilization compatibility. Covestro's recent investments in solvent-free manufacturing and sustainable compound formulations position it well for next-generation medical device requirements.

Medical Plastic Compounds Market - Key Insights & Details

| Key Insights | Details |

|---|---|

| Historical Market Value (2020) | US$ 61.3 Bn |

| Current Market Value (2026) | US$ 84.5 Bn |

| Projected Market Value (2033) | US$ 129.6 Bn |

| CAGR (2026 - 2033) | 6.3% |

| Leading Region | North America, 36% market share (2025) |

| Dominant Segment (Material Type) | Polyvinyl Chloride (PVC), 34% market share (2025) |

| Top-ranking Segment (Application) | Disposables, 38% market share (2025) |

| Incremental Opportunity (2026 - 2033) | US$ 45.1 Bn |

Companies Covered in Medical Plastic Compounds Market

- BASF SE

- Dow Inc.

- Eastman Chemical Company

- Evonik Industries AG

- SABIC

- Celanese Corporation

- Covestro AG

- Tekni-Plex Inc.

- RAUMEDIC AG

- Solvay SA

- Mitsubishi Chemical Group Corporation

- Teknor Apex Company

- Mexichem (Orbia)

- Lubrizol Corporation

- Kraton Corporation

- Trinseo S.A.

Frequently Asked Questions

The global medical plastic compounds market is valued at US$ 84.5 billion in 2026 and is projected to reach US$ 129.6 billion by 2033, growing at a CAGR of 6.3%, representing an incremental opportunity of approximately US$ 45.1 Bn.

The aging global population is projected to reach 2.1 billion people aged 60 and older by 2050, leading to increased demand for chronic disease management devices. Additionally, the approval of single-use medical device protocols by the CDC's Healthcare Infection Control Practices Advisory Committee (HICPAC) and the WHO's injection safety guidelines is creating a consistent demand for disposable materials. This affects PVC, polyethylene, and polypropylene compounds, which are used in the 16 billion injection procedures conducted annually worldwide.

Polyvinyl Chloride (PVC) leads with approximately 34% market share in 2025, reflecting its decades-long biocompatibility track record, unmatched processability for IV bags, catheters, blood bags, and tubing, and established FDA regulatory pathways. Despite ECHA's DEHP restrictions under EU REACH, REACH-compliant PVC formulations incorporating approved plasticizer alternatives are maintaining PVC's dominant position as a formulation upgrade rather than a replacement cycle.

North America leads with approximately 36% revenue share in 2025, anchored by the U.S. market valued at approximately US$ 26.8 Bn, driven by the world's largest medical device industry, US$ 4.9 trillion in healthcare spending, and FDA and ISO 10993 biocompatibility frameworks that compel premium-grade compound procurement from established suppliers, including BASF, Dow, Celanese, Eastman, and Tekni-Plex.

Bioresorbable polymer compounds for implantable devices represent the highest-margin near-term opportunity, with over 70 FDA Breakthrough Device Program designations granted in relevant implant categories as of 2024.

The market is led by BASF SE, Dow Inc., and Covestro AG. Evonik Industries, SABIC, Celanese, Solvay, and RAUMEDIC are also significant market participants.