- Plastics, Polymers & Resins

- Rotomolding Compounds Market

Rotomolding Compounds Market Size, Share, and Growth Forecast, 2025 - 2032

Rotomolding Compounds Market by Material Type (Polypropylene, Polyethylene, Polyamide, Polycarbonate, PVC, and Others), Application (Storage Tanks, Portable Water Tanks, Automotive, Packaging, Consumer Goods, Furniture, and Others), and Regional Analysis from 2025 - 2032

Rotomolding Compounds Market Share and Trends Analysis

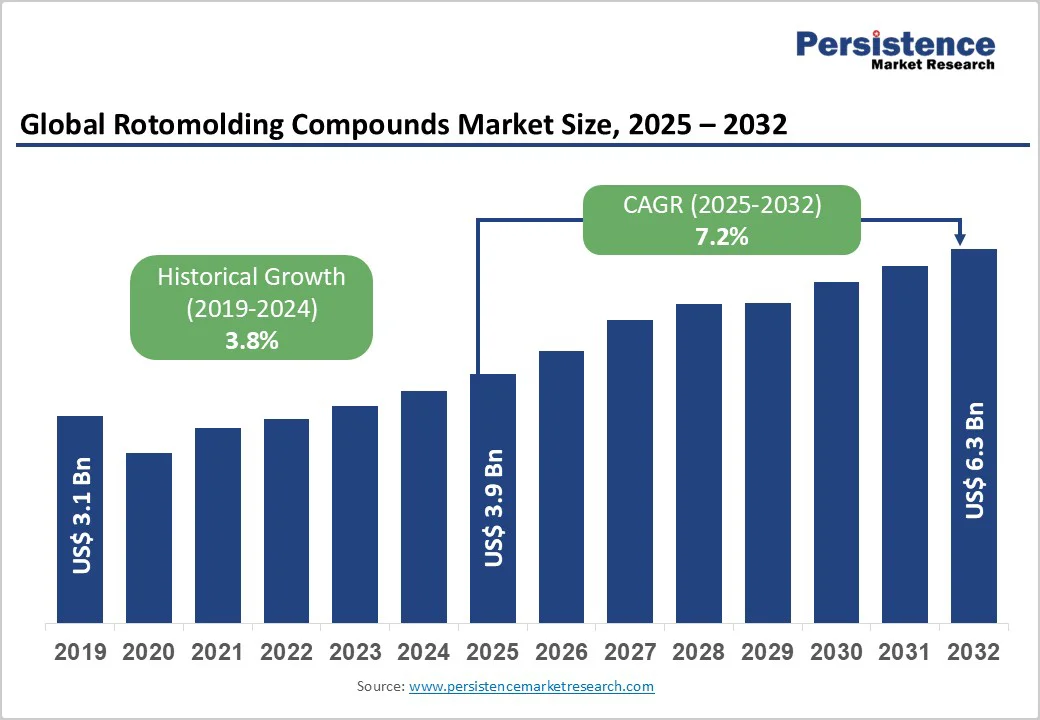

The global rotomolding compounds market size is likely to be valued at US$ 3.9 billion in 2025, and is projected to reach US$ 6.3 billion by 2032, growing at a CAGR of 7.2% during the forecast period 2025-2032, driven by the increasing adoption of rotomolded components across automotive and industrial sectors. The cost-effectiveness of rotomolding compounds, combined with the ability to produce large, seamless parts without requiring secondary assembly operations, makes this process attractive for manufacturers seeking to optimize production efficiency and reduce material waste. The growing emphasis on sustainability and circular economy principles is further boosting demand, as rotomolding optimizes material utilization and supports the use of recycled polymers.

Key Industry Highlights

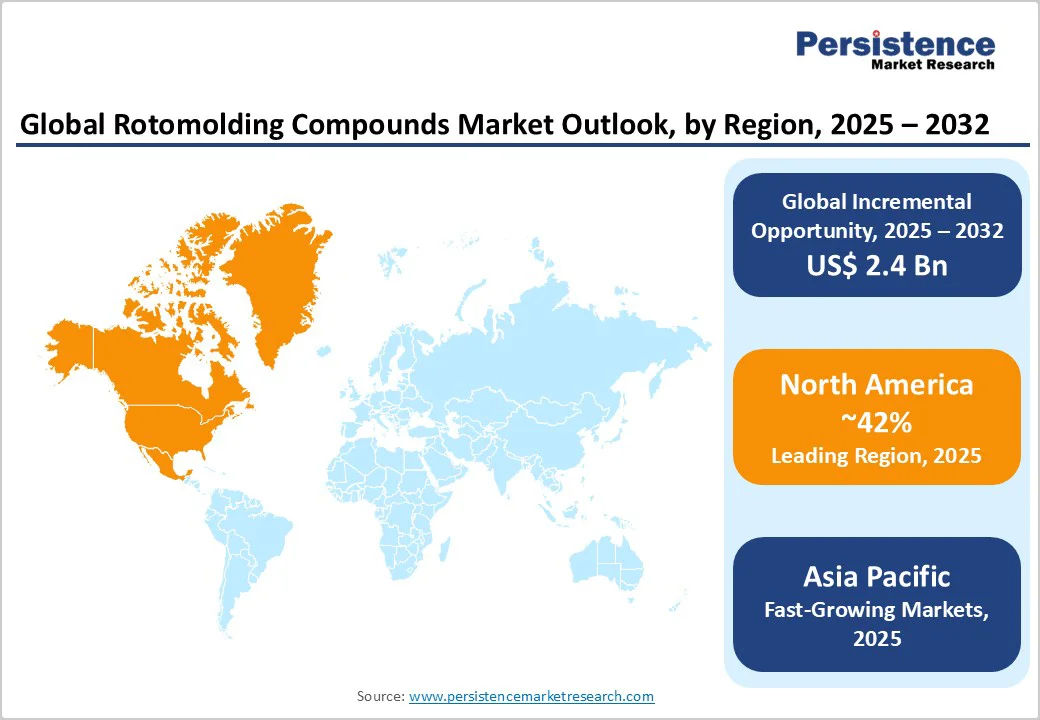

- Regional Leader: North America is set to dominate the market with approximately 42% share in 2025, driven by advanced manufacturing capabilities, stringent automotive emission regulations, and robust infrastructure investments.

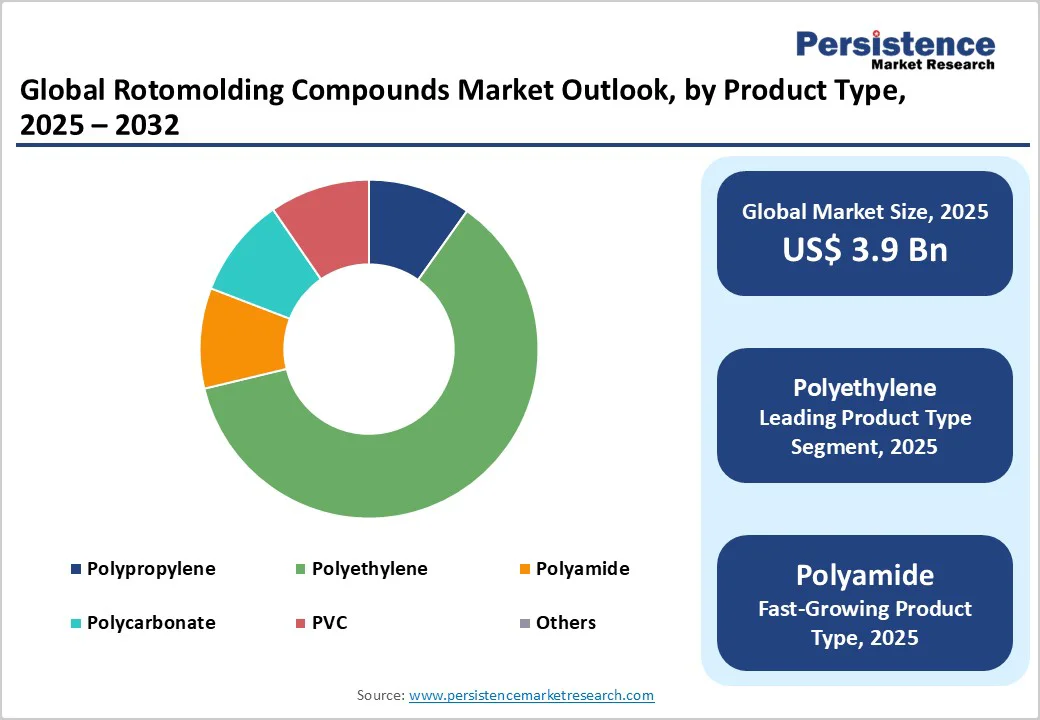

- Leading Material: Polyethylene is poised to lead with around 80% market revenue share in 2025 due to its impact strength, chemical resistance, cost-effectiveness, and ease of processing.

- Largest Application: Storage tanks are likely to remain the largest application segment in 2025, representing 63% of the market, fueled by municipal water supply, agriculture, and chemical processing projects.

- Market Drivers: Key growth drivers include the increasing adoption of rotomolded components in automotive, water storage, and industrial applications, and rising regulatory pressure for fuel efficiency and emissions reduction.

- Market Opportunities: Key opportunities lie in the expansion of bio-based and mechanically recycled resin portfolios, innovations in specialty polymer blends for healthcare and life sciences, and rising demand for sustainable, high-performance, and circular-economy, compliant rotomolding solutions.

| Key Insights | Details |

|---|---|

|

Rotomolding Compounds Market Size (2025E) |

US$ 3.9 Bn |

|

Market Value Forecast (2032F) |

US$ 6.3 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

7.2% |

|

Historical Market Growth (CAGR 2019 to 2024) |

3.8% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Rising Demand for Rotomolding Compounds in Automotive Industry for Fuel Efficiency

The automotive sector’s continuous drive for improved fuel efficiency and reduced emissions is a key factor boosting the adoption of rotomolding compounds. Weight reduction of up to 25% can be achieved in modern passenger vehicles when key components, such as fuel tanks, bumpers, and underbody shields, are manufactured via rotational molding instead of traditional injection molding. This trend is reinforced by stringent global regulations such as the U.S. Corporate Average Fuel Economy (CAFE) standards and the European Union (EU)’s CO2 emission limits for new cars, which mandate automakers to achieve fleet-wide averages below 95 g/km.

Rapid urbanization and the increasing demand for dependable water supply systems are also driving strong adoption of rotomolded storage solutions in both municipal and industrial sectors. In India, for instance, the Jal Jeevan Mission aims to provide clean drinking water to 100 million rural households by 2025, which can fuel the deployment of rotomolded potable water tank installations across the country. As global infrastructure spending surpasses US$ 1.5 trillion annually, the rotomolding compounds market stands to benefit from a steady pipeline of water, wastewater, and chemical containment projects through 2032.

Underdeveloped Recycling Infrastructure and Regulatory Hurdles

While rotomolding generates minimal scrap during manufacturing, the post-consumer recovery and recycling of rotomolded products face substantial challenges. Globally, only a small percentage of end-of-life rotomolded containers and parts are collected and processed due to inadequate collection networks, limited sorting capabilities for mixed-polymer waste streams, and low economic incentives for recyclers. In the EU, the Plastics Packaging Regulation mandates 50% recycling rates by 2025, but enforcement varies by member state, leaving rotomolding compound producers uncertain about recycled content supply.

North America lacks federal mandates for high-density polyethylene recycling beyond curbside programs, which seldom accept large-format products like tanks. This regulatory patchwork and infrastructure gap hinder the development of a robust circular economy for rotomolding compounds, potentially slowing adoption in regions with strict plastic waste management policies.

Expansion of Bio-based and Mechanically Recycled Resin Portfolios

Increasing corporate sustainability commitments and regulatory pressures are compelling compounders to innovate in circular material streams. Partnerships between compounders and waste-management firms are establishing closed-loop supply chains, such as the joint venture announced by Avantor, Inc., in March 2025, to convert agricultural film scrap into high-performance rotomolding grades. Concurrently, bio-based polyethylene produced from sugarcane ethanol has achieved technical parity with virgin resin, offering a potentially sizeable reduction in cradle-to-gate greenhouse gas emissions. These developments are playing a central role in unlocking new market segments in consumer goods and medical applications, where sustainability credentials are increasingly pivotal for procurement decisions.

Category-wise Analysis

Material Type Insights

Polyethylene is well-positioned to retain its dominance, capturing approximately 80% of the rotomolding compound market revenue share in 2025, on account of its unparalleled balance of performance and cost. This leading position stems from polyethylene’s excellent impact strength, chemical resistance, and ease of processing, which collectively support high-volume manufacturing of seamless parts such as storage tanks and automotive fuel system components.

Recent process improvements in polyethylene catalyst systems have reduced cycle times, enhancing throughput and lowering energy consumption. As a result, compounders continue to prioritize polyethylene grades for portfolio expansion, including specialty UV-stabilized and antimicrobially treated variants to meet stringent outdoor and hygiene-focused applications.

Application Insights

Storage tanks are expected to represent the largest application area, accounting for around 63% of the rotomolding compounds market share in 2025, driven by a robust demand in municipal water supply, agriculture, and chemical processing sectors. Rotomolded tanks are preferred for their seamless construction, eliminating weld lines and potential leak points, and offering service lives that often exceed 20 years under continuous UV exposure. Government-led rural water projects in India and Africa have accelerated installations, contributing to a 12% compound annual growth rate in tank production over the past three years.

The automotive sector is anticipated to grow at about 8% CAGR from 2025 to 2032, as OEMs embrace lightweighting mandates. Consumer goods and packaging applications are smaller but fast-growing niches, where custom-shaped containers and industrial casings leverage the design flexibility offered by rotomolding. The combination of durability, design versatility, and cost-efficiency cements storage tanks as the cornerstone of the market’s application landscape.

Regional Insights

North America Rotomolding Compounds Market Trends

North America is forecasted to command a 42% share of the rotomolding compounds market in 2025, underpinned by a robust automotive industry and sizeable infrastructure investments. In the United States, stringent CAFE standards have driven OEM partnerships with compounders to advance high-density polyethylene blends for fuel tanks, which achieved a 6% year-on-year volume increase in 2024. Research hubs in Michigan and Ohio are fast-tracking polymers with enhanced thermal stability and impact resistance, essential for both internal combustion and electric vehicle components.

The allocation of a considerable amount of financial resources under the Infrastructure Investment and Jobs Act to water and wastewater infrastructure has spurred municipal procurement of rotomolded water tanks, with installations rising 10% in 2024. Complementing these trends, recycling initiatives in California and New York are piloting closed-loop programs to reclaim post-consumer polyethylene tank scrap, bolstering sustainability and circular-economy credentials in the region.

Europe Rotomolding Compounds Market Trends

Europe offers significant growth opportunities stimulated by stringent environmental regulations of the EU and robust industrial demand for the rotomolding process. Germany leads with advanced manufacturing hubs that reported a 5.5% rise in compounding volumes for agricultural and chemical applications in 2024. The circular economy targets under the European Green Deal, mandating 60% polyethylene recycling by 2030, are prompting compounders to scale recycled-content and mass-balance certified resin production, opening new high-margin product lines. In the United Kingdom and France, the transition to Euro 7 emission standards is accelerating lightweighting initiatives in the transportation sector, with collaborative development of specialty polypropylene blends projected to grow at over 8% annually through 2032. These factors position Europe as a dynamic growth market underpinned by regulatory harmonization and technological innovation.

Asia Pacific Rotomolding Compounds Market Trends

Asia Pacific is the fastest-growing market for rotomolding compounds during 2025-2032, propelled by rapid urbanization, infrastructure development, and expanding manufacturing ecosystems. China leads the regional market, driven by government investments totaling US$ 200 billion in water treatment and housing projects. Domestic compounders have ramped up capacity for medium-density polyethylene, meeting both local demand and export requirements.

India’s Jal Jeevan Mission has also triggered a surge in potable water tank installations, with rural markets adopting UV-stabilized rotomolding grades for long-term durability. ASEAN countries, including Vietnam and Thailand, are attracting greenfield compounding facilities due to favorable incentives and competitive labor costs. In Japan, innovation in copolymer blends for consumer electronics housings has spurred a niche growth segment, supported by partnerships between technology firms and specialty polymer suppliers.

Competitive Landscape

The global rotomolding compounds market structure is moderately consolidated, with leading chemical companies and specialized compounders dominating production. Major players pursue capacity expansions and vertical integration to secure feedstock supply and improve margins. Research collaborations with academic institutes and start-ups are driving innovation in high-performance and sustainable resins. Key differentiators implemented by top players include proprietary polymer blends, recycling partnerships, and customization capabilities for complex part geometries. Emerging business models focus on material-as-a-service offerings, enabling end-users to lease specialized compounds and equipment.

Key Industry Developments

- In October 2025, Valencia Pipe Co., a subsidiary of VPC Global, opened a new 70,000-square-foot roto-molding manufacturing facility in Rocky Mount, North Carolina, to support its growing polyethylene tank operations. This marks the company’s third plant expansion in just over a year, complementing existing facilities in Oklahoma and Nevada. The new plant employs 25 people and focuses on producing septic, water, and multi-use tanks compliant with state and local regulations. VPC Global emphasizes quality, certification, and customer service as key drivers of its strategic growth in the roto-molding market.

- In August 2025, Myers announced the closure of its rotomolding operations in Ohio as part of a strategic realignment to improve efficiency and focus on core business areas. The shutdown reflects broader industry trends of consolidation and optimization, aiming to streamline production capabilities. While the Ohio facility will cease operations, Myers plans to continue serving customers through other manufacturing sites and ongoing investments in advanced technologies to support growth and competitiveness in the plastics market.

- In June 2025, a new AI software called RotoEdge Pro was launched and has been helping rotational-molding manufacturers with actionable insights, real-time production visibility, and automatic scheduling. The solution targets the niche demands of rotomolding operations, such as complex scheduling across machines, materials and batches, enabling faster, more efficient production planning. By automating scheduling and providing detailed production analytics, it supports manufacturers in reducing downtime, managing order progress and improving throughput.

Companies Covered in Rotomolding Compounds Market

- LyondellBasell Industries

- ExxonMobil Chemical Corporation

- Chevron Phillips Chemical Company

- PTT Global Chemical Public Company Limited

- Dow Inc.

- TotalEnergies Inc.

- NOVA Chemicals Corporation

- SCG Chemicals PLC.

- Poddar Pigments Limited

- Cabot Corporation

Frequently Asked Questions

The global rotomolding compounds market is projected to reach US$ 3.9 billion in 2025.

Regulatory pressure for improved fuel economy and stringent light-weighting mandates for vehicles have stoked the adoption rate of rotomolded fuel system components.

The market is poised to witness a CAGR of 7.2% from 2025 to 2032.

The growing emphasis on sustainability and circular economy principles and ability of rotomolding to optimize material utilization and support the use of recycled polymers will open up new market opportunities.

LyondellBasell Industries, TotalEnergies Inc., and ExxonMobil Chemical Corporation are some of the key players.