- Plastics, Polymers & Resins

- Plastic Compounding Market

Plastic Compounding Market Size, Share, and Growth Forecast, 2025 - 2032

Plastic Compounding Market By Polymer Type (Thermoplastics, Engineering Plastics, Others), Source (Fossil-based/Virgin, Others), Application (Automotive & Transportation, Packaging, Building & Construction, Others), and Regional Analysis for 2025 - 2032

Plastic Compounding Market Share and Trends Analysis

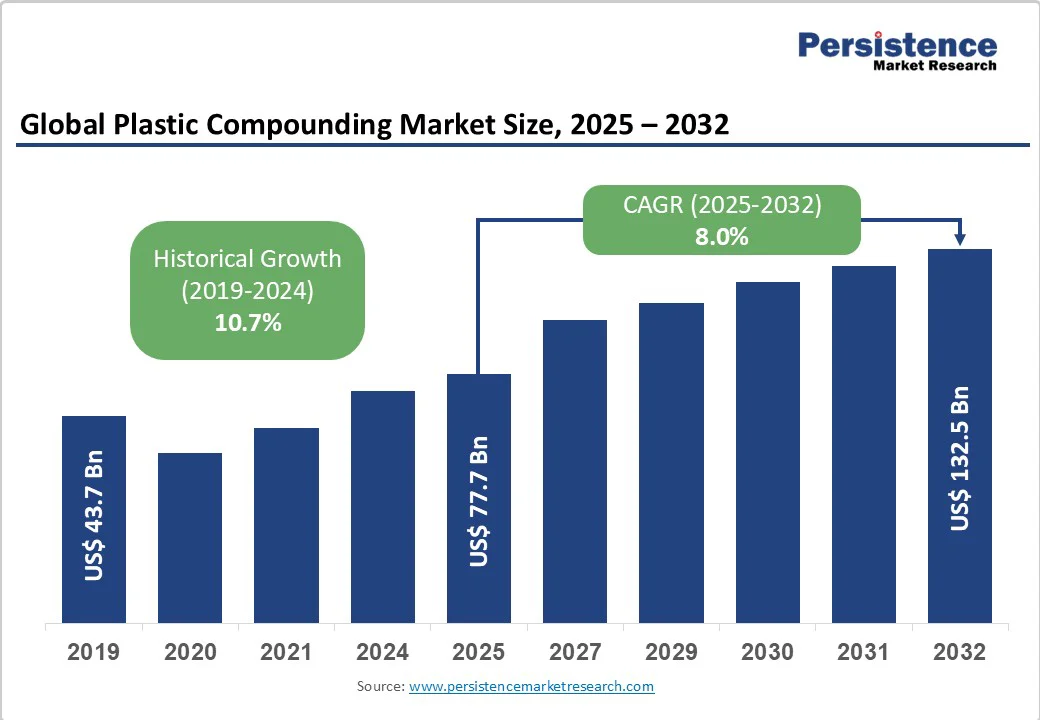

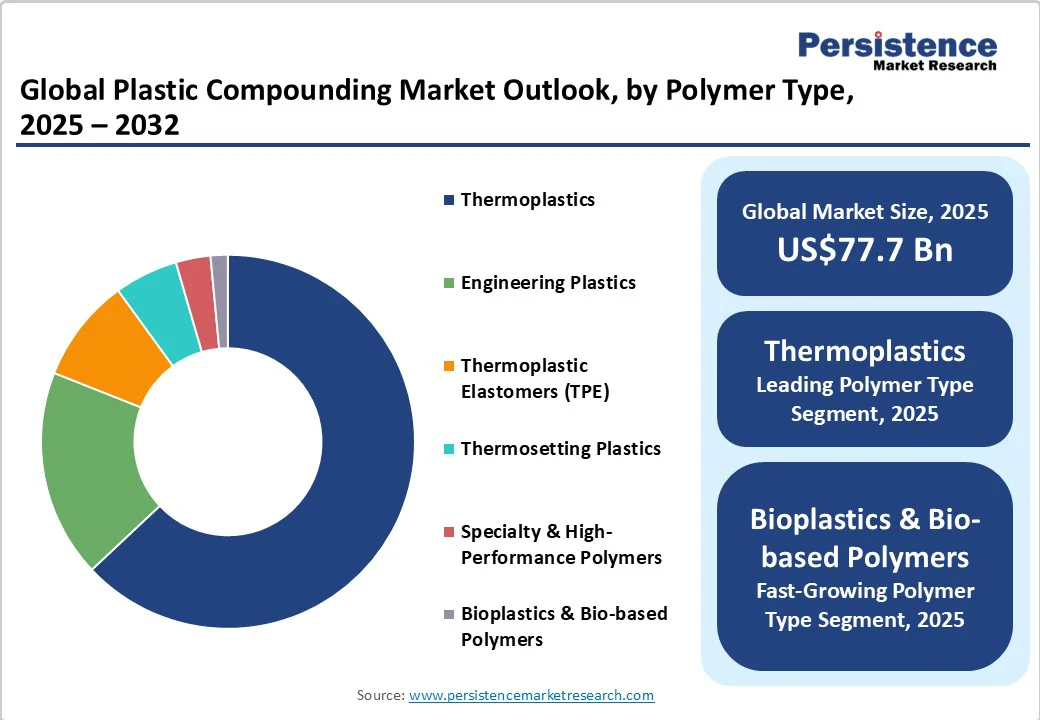

The global plastic compounding market size is likely to be valued at US$77.7 Billion in 2025, and is estimated to reach US$132.5 Billion by 2032, growing at a CAGR of 8.0% during the forecast period 2025 - 2032, driven by its integral role in diverse industries requiring specialized polymers with tailored properties.

Market growth is also spurred by accelerating transportation electrification, sustainability-driven packaging innovation, and industrialization in Asia Pacific. Advances in recycled-content technologies and performance-by-design polymers support balanced, long-term growth amid regulatory and economic shifts.

Key Industry Highlights

- Leading & Fastest-growing Polymers: Among thermoplastics, polypropylene (PP) is set to lead with an estimated 31% share in 2025, while PET is likely to exhibit the fastest growth rate at approximately 10.4% CAGR during 2025 - 2032.

- Fastest-growing Source: The recycled polymer segment is slated to expand rapidly with over 11.2% CAGR, foregrounding circular economy imperatives in market transformation.

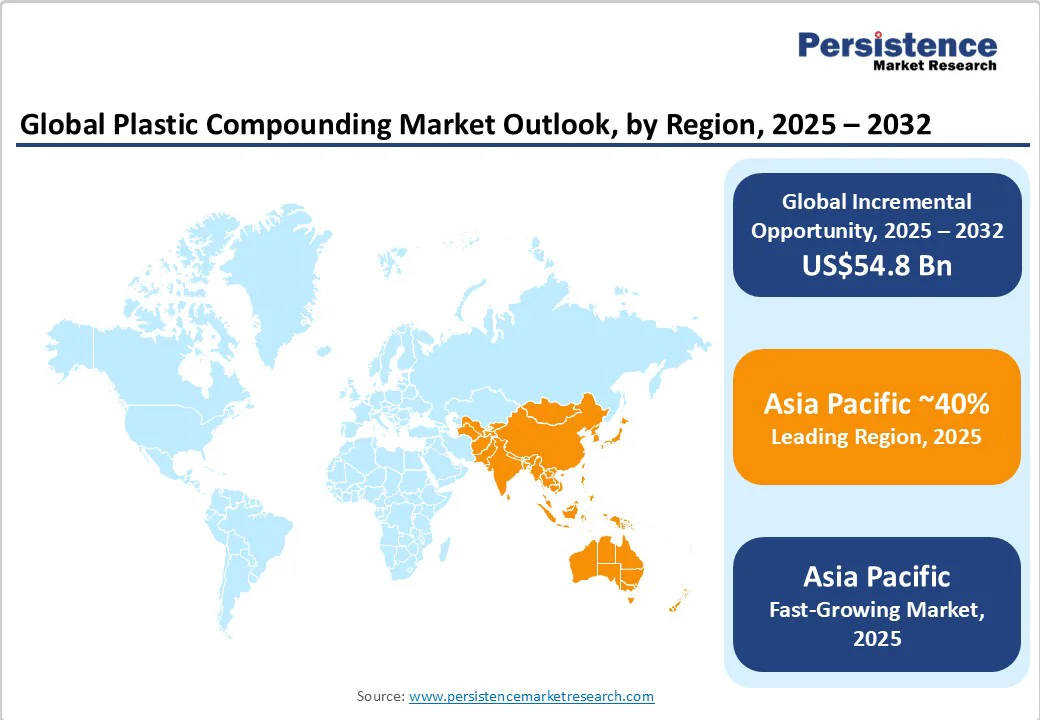

- Dominant & Fastest-growing Regional Market: Asia Pacific is expected to dominate with nearly 40% share in 2025 and a CAGR of approximately 8.6%, led by China’s manufacturing and regulatory incentives.

- Regional Dynamics: Europe is slated to command about 29% market share, supported by EU sustainability frameworks, whereas North America will hold around 27% market share on the back of a strong innovation ecosystem.

- Competitive Environment: Market consolidation continues as top 10 players account for roughly 60% market share, positioning innovation and sustainability compliance as core competitive differentiators.

- September 2025: Supreme Industries commissioned new Acrylonitrile Butadiene Styrene (ABS) compounding production lines, aiming to meet the growing demand in sectors such as automotive, consumer electronics, and appliances, where high-quality ABS compounds are essential.

| Key Insights | Details |

|---|---|

| Plastic Compounding Market Size (2025E) | US$77.7 Bn |

| Market Value Forecast (2032F) | US$132.5 Bn |

| Projected Growth (CAGR 2025 to 2032) | 8.0% |

| Historical Market Growth (CAGR 2019 to 2024) | 10.7% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Electrification of Transportation as a Leading Growth Catalyst

The transition toward electric vehicles (EVs) is a potent driver shaping the demand dynamics of plastic compounding. The automotive sector has been integrating increasingly advanced polymer compounds to meet lightweighting, thermal management, and battery safety standards essential for EV performance.

According to the International Energy Agency (IEA), global EV stock surpassed 20 million units in 2024 and is forecast to exceed 150 million by 2030, accelerating compounding demand for specialty polymers such as thermoplastic elastomers and engineering plastics such as polyamide (PA) and polycarbonate (PC) used in battery housings, connectors, and motor components.

This trend is supported by stringent regulatory tailwinds, including emission reduction mandates of the European Union (EU) and U.S. infrastructure investments totaling over US$7 Billion toward EV supply chains. The vehicle lightweighting imperative, key for extending driving range, stimulates the substitution of metals with reinforced plastic compounds, which also facilitate enhanced safety through flame retardancy and thermal conductivity additives.

Raw Material Price Volatility as a Structural Challenge

Price volatility in base polymer feedstock and additive raw materials represents a material restraint, with amplified risk due to geopolitical and supply chain complexities. For instance, fossil-fuel-linked polymer costs such as polypropylene and polyethylene have seen fluctuations exceeding 20% intra-annually since 2022 amid global energy market upheavals and the production policies of the Organization of the Petroleum Exporting Countries (OPEC).

Specialty additives, including glass fibers and flame retardants, have also experienced supply deficits due to raw material scarcities originating from China and Southeast Asia, regional compounding hubs. Such volatility translates into upward cost pressure on compounders, squeezing margins, complicating contract pricing reliability, and propagating supply unpredictability. The compounded effect restrains market accessibility, particularly for mid-sized players lacking hedging infrastructure, thereby skewing competitive dynamics toward larger, vertically integrated companies.

Emergence of High-Performance Sustainable Biocomposites

Biocomposites incorporating bio-based polymers reinforced with natural fibers, such as hemp, jute, and cellulose, present an emerging, lucrative niche within plastic compounding. Developments in polymer chemistry enabling enhanced compatibility between bio-polymers such as PLA and natural fibers have opened applications across automotive interiors, packaging, and consumer goods, where carbon footprint reduction is paramount.

Lifecycle assessments show these biocomposites reduce greenhouse gas emissions by up to 50% compared to traditional compounded plastics. Policy incentives are also accelerating uptake. For example, the EU’s Green Deal allocates over €2 Billion (US$2.34 Billion) for sustainable materials innovation, complemented by mandates requiring minimum recycled or bio-content in packaging and automotive parts by 2030.

Manufacturers aligning with this transition report value premium capture of up to 15% relative to baseline compounds due to differentiated sustainability credentials. For market entrants and established players, investing in biocomposite R&D and scaling pilot production affords entry into this fast-growing space, supported by favorable policy, consumer sentiment, and evolving technical performance.

Category-wise Analysis

Polymer Type Insights

The thermoplastics segment is slated to remain the market leader in 2025 with an estimated share of 63%, predominantly driven by the demand for polypropylene (PP) that accounts for an estimated 31% of total polymer compounding volumes. PP’s versatility in packaging, automotive, and consumer goods applications underpins its market dominance, supported by cost-effectiveness and recyclability.

The fastest growing sub-segment is polyethylene terephthalate (PET), with its growth fueled by its increasing use in packaging and fiber applications, leveraging its recyclability and barrier properties. Engineering plastics such as polyamide (PA) are also expanding rapidly at a promising CAGR due to their adoption in automotive lightweighting and high-performance electrical components, reflecting market demand for durability and chemical resistance.

Source Insights

Fossil-based polymers are expected to hold the leading revenue share at approximately 52% in 2025. Their dominance is visibly eroding due to regulatory mandates and consumer demand. Recycled polymers, comprising post-consumer recycled (PCR) and post-industrial recycled contents, are poised to be the fastest-growing source segment during 2025 - 2032. This rapid expansion is catalyzed by escalating circular economy regulations in Europe and North America, imposing recycled content minimums especially in the packaging and automotive sectors.

Bio-based polymers constitute a niche but fast-emerging segment, projected to grow at a notable pace owing to environmental incentives and advances in polymer technology, reducing cost and improving mechanical properties. Source diversification strategies are increasingly critical for compounding companies to mitigate supply and cost volatility, while aligning with the evolving sustainability frameworks, making recycled and bio-based materials key investment priorities.

Application Insights

The automotive & transportation sector is well-positioned to lead application demand, representing an estimated 29.6% of the revenue share in 2025. This leadership stems from the sector’s early adoption of high-performance compounds to enable materials lightweighting, safety enhancement, and battery integration, particularly driven by the meteoric rise in EV adoption globally.

Packaging is set to be the fastest-growing application from 2025 to 2032. The segment growth is propelled by the rising requirements for lightweight, recyclable, and bio-based packaging solutions, aligned with global plastic waste reduction initiatives. Interactive collaboration between compounders, original equipment manufacturers (OEMs), and regulators is emerging to accelerate innovation adoption and regulatory compliance, affirming the strategic importance of these applications to future market share capture.

Regional Insights

Asia Pacific Plastic Compounding Market Trends

Asia Pacific is anticipated to dominate the market, expected to hold an estimated 40% share in 2025, growing at the fastest through 2032. China headlines regional growth due to extensive manufacturing infrastructure investment, massive EV production and adoption, and government policy incentives for sustainability and plastic recycling.

India and ASEAN countries are swiftly expanding their market base through infrastructural modernization, unprecedented urbanization, and active implementation of policies targeted toward sustainable utilization of plastic compounds.

For the Asia Pacific market, major advantages include cost-effective manufacturing, integrated supply chain clusters, widespread distribution networks, and a growing consumer base requiring packaged goods and electric mobility. Top economies in the region are also attracting international capital inflows into compounding systems, elevating their influence on global supply chains and innovation diffusion.

Europe Plastic Compounding Market Trends

Europe is forecast to account for roughly 29% of the market in 2025. Countries such as Germany, the U.K., France, and Spain are playing an especially influential role due to regulatory harmonization under the EU’s Green Deal and mainstream adoption of recycled polymers. Regional market growth is aided by aggressive sustainability targets set by the EU that mandate minimum recycled content, robust automotive manufacturing focusing on lightweighting, and the presence of key compounders emphasizing green product portfolios.

The building & construction sector also supports growth through energy efficiency and flame retardancy requirements. The expansion of the Europe market is mainly founded on regional regulatory stability and consistency and the integration of EU circular economy directives in industrial processes, positioning it as a global model for sustainable plastic compounding.

North America Plastic Compounding Market Trends

North America is projected to hold an estimated 27% of the market share in 2025. The United States leads, supported by a sophisticated innovation ecosystem and regulatory frameworks such as the U.S. Environmental Protection Agency (EPA)’s circular economy policies. Key growth drivers include expanding EV manufacturing facilities, investments in recycled content infrastructure, and increasing demand in the healthcare and packaging sectors.

The region’s regulatory stringency accelerates demand for low-smoke zero-halogen (LSZH) compounds and bioplastics.

Competitive landscape features major global players’ regional R&D centers and capacity expansions. Investments in breakthrough recycling technologies and additive manufacturing compounding are creating high-value niches, offering multiple avenues for strategic positioning until 2032. The growth prospects of the North America market during 2025 - 2032 are bolstered by a gradual but consistent innovation-driven expansion supported by strong environmental policies.

Competitive Landscape

The global plastic compounding market structure is moderately fragmented, with the top 10 players collectively accounting for approximately 55-60% market share. Key players include industry-leading multinationals with integrated production and R&D capabilities driving innovation, scale, and sustainability compliance.

Large-scale compounders such as BASF, LyondellBasell, and SABIC maintain leadership through diverse product portfolios, geographic reach, and technology partnerships. Smaller and regional players compete by specializing in niche polymers and custom compounding services.

Market concentration is increasing due to capacity expansions, M&A, and strategic partnerships aimed at technology acquisition, geographic growth, and sustainability engagement, reflecting a maturing but innovation-driven market environment.

Key Industry Developments

- In September 2025, Westlake Corporation acquired ACI Compounding Solutions, boosting its polymer compounding capabilities, expanding specialty product offerings, and strengthening its position in the automotive, industrial, and consumer markets while reinforcing innovation and customer-focused solutions in the compounding sector.

- In September 2025, Borealis invested over €100 Million (US$116.9 Million) to expand its polypropylene compounding facilities in Schwechat, Austria, with production starting in H2 2026. The expansion boosts the supply of high-quality, recyclable PP compounds for consumer, mobility, and infrastructure sectors.

- In July 2025, HydroGraph launched the Compounding Partner Program to collaborate with partners on graphene-enhanced plastic compounds, enhancing thermal, electrical, and mechanical properties for electronics and automotive applications, supporting innovation, tailored solutions, and market-ready composite materials.

Companies Covered in Plastic Compounding Market

- BASF SE

- LyondellBasell Industries Holdings B.V.

- SABIC (Saudi Basic Industries Corporation)

- Clariant AG

- The Dow Chemical Company

- Lanxess AG

- Evonik Industries AG

- RTP Company

- PolyOne Corporation (Avient Corporation)

- Mitsubishi Chemical Holdings Corporation

- DuPont de Nemours, Inc.

- Covestro AG

- Celanese Corporation

- Solvay S.A.

- Arkema S.A.

Frequently Asked Questions

The plastic compounding market is projected to reach US$77.7 Billion in 2025.

The integral role of plastic compounding in diverse industries requiring specialized polymers with tailored properties and the accelerating electrification in transportation are driving the plastic compounding market.

The plastic compounding market is poised to witness a CAGR of 8.0% from 2025 to 2032.

Packaging innovation driven by sustainability mandates, regional industrialization advances, particularly in Asia Pacific, and technological advancements in recycled content enhancement and performance-by-design polymer compounds are key market opportunities.

BASF SE, LyondellBasell Industries Holdings B.V., and SABIC (Saudi Basic Industries Corporation) are some of the key players in the plastic compounding market.