- Non-food Packaging

- Packaging Machinery Market

Packaging Machinery Market Size, Share, and Growth Forecast, 2026 - 2033

Packaging Machinery Market By Machine Type (Filling, Labeling, Others), End-use Industry (Food & Beverage, Pharmaceuticals, Others), Technology, Packaging Type, and Regional Analysis for 2026 - 2033

Packaging Machinery Market Size and Trends Analysis

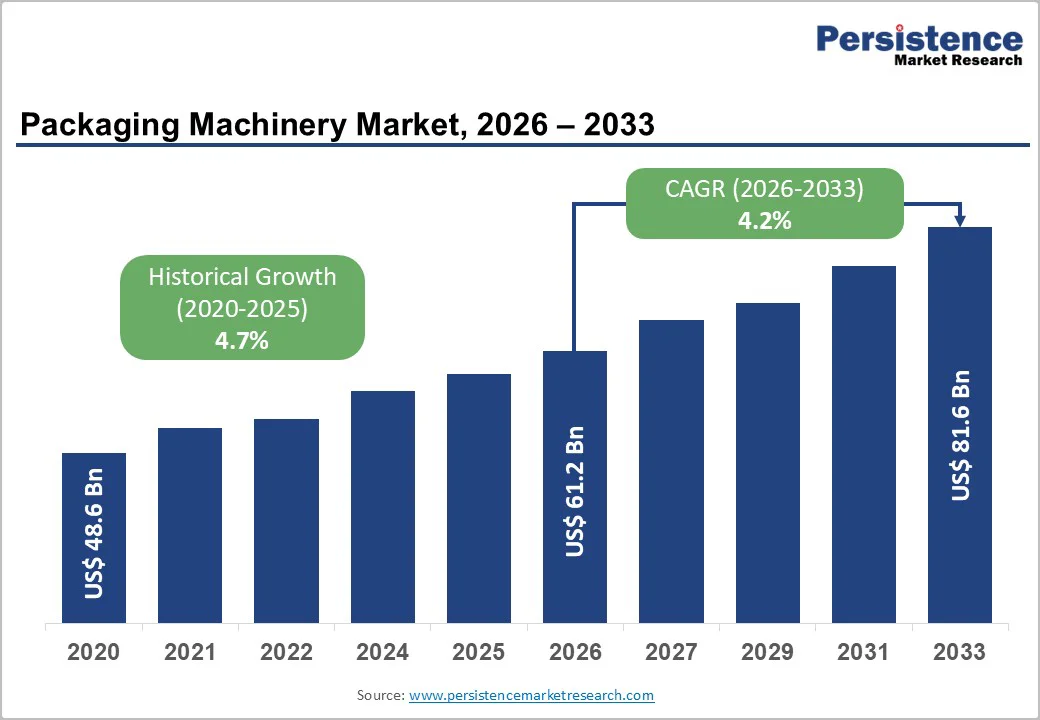

The global packaging machinery market size is likely to be valued at US$61.2 billion in 2026. It is expected to reach US$81.6 billion by 2033, growing at a CAGR of 4.2% between 2026 and 2033, driven by sustained automation investments across the food, beverage, and pharmaceutical sectors, rising adoption of flexible and sustainable packaging formats, and capacity expansion among contract packers in developing regions.

Increasing e-commerce shipment volumes and tightening pharmaceutical serialization requirements are accelerating equipment modernization. While capital intensity creates short-term constraints, robotics and integrated controls continue to improve throughput and reduce the total cost of ownership.

Key Industry Highlights

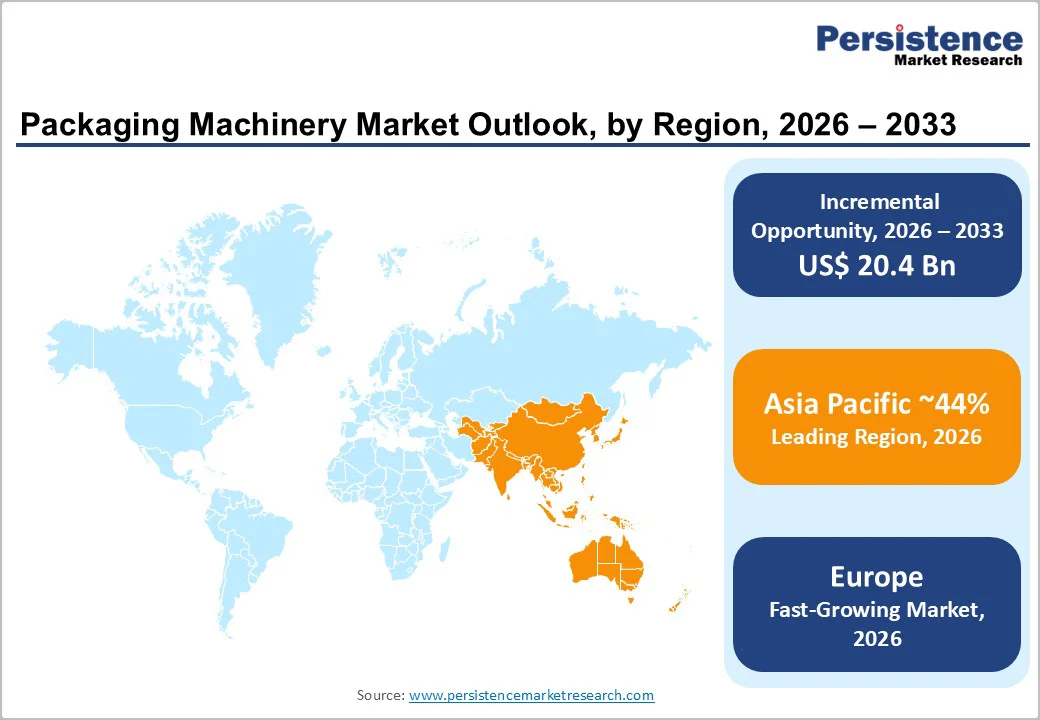

- Leading Region: Asia Pacific, to account for around 44% of global packaging machinery demand in 2026, driven by large-scale FMCG, beverage, and pharmaceutical production across China, India, Japan, and ASEAN.

- Fastest-growing Region: Europe, expanding at an accelerated pace due to sustainability-driven replacement cycles, modernization of filling and labeling lines, and enforcement of EU PPWR regulations.

- Investment Plans: Investment activity is strong worldwide, led by Asia Pacific and North America. Key examples include Hindustan Unilever’s automated packaging expansion in India (2024), Coca-Cola’s bottling upgrades in Florida (2024), and Sidel’s PET technology facility expansion in Parma (2025).

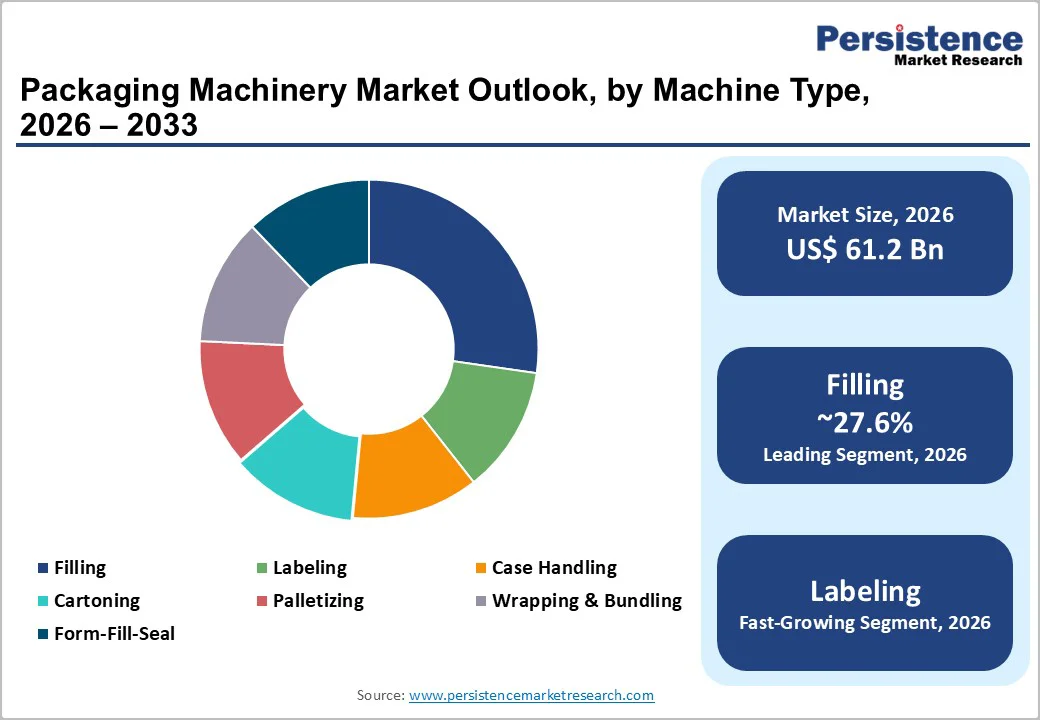

- Dominant Machine Type: Filling machines are expected to account for 27.6% of the market in 2026, driven by high utilization in beverages, dairy, processed foods, chemicals, and personal care, supported by the ongoing adoption of high-speed rotary, aseptic, and volumetric filling systems.

- Leading End-user Industry: The food & beverage segment is expected to account for approximately 34.8% of market share, driven by large production volumes, strict hygiene compliance requirements, and ongoing investments in automated filling, capping, and inspection.

| Key Insights | Details |

|---|---|

|

Packaging Machinery Market Size (2026E) |

US$61.2 Bn |

|

Market Value Forecast (2033F) |

US$81.6 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

4.2% |

|

Historical Market Growth (CAGR 2020 to 2025) |

4.7% |

Market Growth Drivers

Growth Analysis - Automation and Robotics Adoption

The global packaging machinery ecosystem is experiencing a notable shift toward highly automated production environments. Food, beverage, and pharmaceutical companies consistently prioritize robotic pick-and-place systems, automated end-of-line palletizers, and integrated inspection technologies. Industry surveys show rising investment in automation to address labor shortages and increase overall equipment effectiveness. Many automated packaging lines deliver payback periods of 2 to 5 years, supported by enhanced throughput, reduced labor dependency, and fewer product defects. This trend raises average selling prices for machinery and strengthens the competitive position of OEMs that offer integrated robotic, control, and monitoring capabilities.

Sustainability and Growth of Flexible Packaging

Sustainability goals and commitments to recyclability have accelerated the shift from rigid formats to flexible, lightweight packaging. Brand owners are adopting pouching, mono-material films, and recyclable laminates, driving demand for advanced form-fill-seal systems, sealing verification modules, and retrofit kits compatible with new materials. Flexible packaging continues to gain share in the food, beverage, household care, and personal care segments. Machinery that improves material efficiency, supports rapid film changeovers, and reduces waste is gaining momentum. This trend incentivizes OEMs to invest in R&D and creates opportunities for packaging lines optimized for low-carbon, circular-economy materials.

Regulatory and Serialization Requirements in Pharmaceuticals

Pharmaceutical and biologics packaging demand continues to intensify due to stricter serialization, tamper-evidence, and traceability standards globally. Regulated environments require validated, hygienic, contamination-resistant equipment that meets stringent documentation and inspection protocols. This has resulted in higher order volumes for aseptic filling, isolator-based systems, vision inspection, and integrated serialization solutions. Pharmaceutical projects typically yield higher margins and longer sales cycles, favoring OEMs with global service networks and compliance expertise. As biologics, injectables, and high-value therapeutics grow in volume, specialized pharmaceutical packaging machinery remains a core area of premium investment.

Barrier Analysis - High Capital Intensity and Extended Lead Times

Fully automated packaging lines require substantial capital expenditure, limiting adoption among smaller manufacturers, especially during periods of economic uncertainty or elevated interest rates. OEM delivery schedules can be lengthy due to engineering complexity, validation needs, and customization requirements. These factors can delay replacement cycles and shift investment toward semi-automatic solutions or leased equipment models. In constrained financial environments, capital allocation for automation may decrease by a mid-single-digit percentage, particularly in cost-sensitive end-markets.

Supply-Chain Volatility and Component Scarcity

Packaging equipment relies on a large number of precision components, including servo motors, PLCs, vision systems, and drives. Fluctuations in semiconductor availability, electronics lead times, and logistics bottlenecks increase procurement challenges for both OEMs and end users. Extended lead times can cause project delays, necessitate workarounds, and increase working-capital requirements. In some cases, OEMs must increase component inventories to maintain delivery reliability, raising operational costs and reducing margins. The impact is most pronounced for high-speed lines that depend on customized electronics and specialized motion systems.

Opportunity Analysis - Retrofit Solutions and Servitization

As automation complexity increases, manufacturers are turning to retrofit kits, controls upgrades, and IIoT-enabled monitoring systems to extend the life of installed machinery. Retrofitting supports improved energy efficiency, predictive maintenance, and compliance with new packaging material requirements. OEMs and integrators increasingly offer performance-as-a-service and multi-year lifecycle contracts, generating stable recurring revenue. If even one-third of the global installed base adopts structured retrofitting between 2026 and 2033, the resulting aftermarket opportunity would represent several billion dollars in service-driven value.

Emerging Market Expansion and Contract Packaging Growth

Emerging markets, especially in South Asia, Southeast Asia, Africa, and Latin America, are undergoing rapid industrialization and urbanization. These regions are investing in modern packaging lines for food, beverages, personal care, and pharmaceuticals. Contract-packaging companies in these markets are expanding capacity to meet demand from multinational brands and local FMCG players. OEMs with localized service, financing support, and modular equipment portfolios are best positioned to win market share.

Category-wise Analysis

Machine Type Insights

Filling machinery is projected to hold approximately 27.6% of the total market share, reflecting strong, ongoing capital investments across beverages, dairy, edible oils, condiments, personal care liquids, and industrial chemicals. High-speed rotary fillers, aseptic systems, and volumetric and net-weight fillers are core to bottling and processing operations. Large beverage producers often prioritize filling within complete bottling lines due to their high value and impact on throughput, precision, sanitation, and changeover efficiency.

Investments increasingly focus on lightweight containers, recycled PET, and shelf-stable formats. Applications range from carbonated soft drink fillers with CO2 integration to hygienic dairy fillers. As filling accuracy directly influences product quality and regulatory compliance, these units are replaced or upgraded more frequently than other line components, ensuring efficiency and consistency.

Labeling machinery is likely to be the fastest-growing segment, driven by SKU proliferation, private-label programs, and rising traceability and authentication requirements. Modern production demands labelers with variable data printing, serialization, RFID tagging, tamper-evident features, and integrated vision inspection. Digital print-and-apply systems enable cost-effective short-batch production, supporting craft beverages, boutique cosmetics, nutraceuticals, and direct-to-consumer brands with frequent design updates.

Stringent pharmaceutical and food labeling regulations and sustainability disclosures further fuel growth. Beverage producers increasingly adopt wraparound and pressure-sensitive labelers for lightweight PET containers, while premium beauty brands rely on servo-driven systems for precise alignment. OEMs integrating digital workflows, cloud verification, and camera inspection are capturing demand from both high-volume and small-to-mid-sized manufacturers.

End-use Industry Insights

The food and beverage sector is projected to hold around 34.8% of the market, making it the largest end-use segment. High consumption, strict hygiene standards, and frequent product turnover drive ongoing investment in automated packaging machinery. Meat and dairy processors use form-fill-seal, thermoforming, MAP, and inspection systems to ensure safety and shelf life. At the same time, snack and bakery manufacturers rely on automated bagging, cartoning, and case-packing for large-scale distribution. Beverage producers routinely upgrade bottling, capping, and secondary packaging lines for higher throughput and efficiency, with high-speed PET bottling and hygienic or aseptic filling lines supporting lightweight containers and extended-shelf-life products.

The pharmaceutical industry is likely to be the fastest-growing end-user segment, fueled by rising production of biologics, injectables, vaccines, OTC medicines, and personalized therapies. Demand for advanced packaging machinery is increasing as manufacturers expand sterile, high-precision, and contamination-controlled operations. Investments focus on aseptic filling lines, blister packaging, vial and ampoule filling, and track-and-trace–enabled cartoners to meet U.S. FDA, EMA, and WHO GMP regulations. Growth is also driven by pre-filled syringes, autoinjectors, and single-dose formats requiring specialized filling, sealing, and inspection technologies. Serialization mandates in the U.S. (DSCSA 2024) and EU (FMD) further accelerate upgrades in labeling, coding, and aggregation equipment.

Regional Insights

North America Packaging Machinery Market Trend - Automation, Regulatory-Driven Upgrades & Reshoring-Fueled Line Modernization

North America’s packaging machinery market is driven by strong demand across food, beverage, pharmaceutical, and contract packaging sectors. The U.S. leads regional spending, supported by advanced manufacturing infrastructure, high automation adoption, and stringent regulatory requirements. At the same time, Canada contributes through specialty food processing, and Mexico benefits from near-shoring strategies that expand local operations for beverages and consumer goods. Notable investments, such as Coca-Cola’s 2024 expansion in Florida with high-speed bottling and labeling lines, highlight the region’s focus on modernizing filling and packaging operations. Key growth drivers include automation to offset labor shortages, increased demand for validated pharmaceutical packaging lines, and e-commerce-driven needs for small-batch, flexible-format packaging.

Regulatory frameworks, including the FDA FSMA and cGMP requirements for pharma, push companies toward documented, integrated packaging systems. Manufacturers are rapidly adopting digital upgrades, robotics, and aftermarket services to improve reliability and reduce the total cost of ownership. From 2023 to 2025, ProMach, IMA North America, and Barry-Wehmiller expanded their service networks and implemented remote diagnostics programs to improve operational uptime. Strategic moves, such as Duravant’s acquisition of Pouch Pros Inc. in 2024, have bolstered its capabilities in flexible packaging.

Strategic acquisitions, such as Duravant’s 2024 purchase of Pouch Pros Inc., strengthen flexible packaging capabilities. Retrofit demand remains robust as food and beverage companies upgrade legacy lines to energy-efficient, servo-driven technology. Overall, North America is expected to sustain steady growth, underpinned by automation, reshoring, and continued expansion in specialized consumer-product manufacturing.

Europe Packaging Machinery Market Trend - Engineering Leadership, Sustainability-Driven Retrofits & Aseptic Technology Expansion

Europe is likely to be the fastest-growing region and remains one of the most influential hubs for high-quality packaging machinery manufacturing. Germany and Italy serve as global centers for machinery engineering, supplying advanced filling, labeling, aseptic, and thermoforming systems. This leadership is reinforced by developments such as Krones AG’s 2024 launch of the Contipure AseptBloc DN system, designed to enhance energy efficiency and aseptic filling performance for beverages.

France, Spain, and the U.K. contribute significant demand through dairy, beverage, and prepared-food industries. Sustainability is a defining factor across the region, with regulatory frameworks promoting recyclability, material reduction, and circular-economy practices. The EU Packaging and Packaging Waste Regulation (PPWR 2024 update) has prompted companies to adopt mono-material packaging lines and retrofit machines for lightweight films and recyclable PET.

Demand is supported by high automation penetration, robust engineering expertise, and strict adherence to hygiene and safety standards. European manufacturers are increasingly integrating digital platforms, advanced controls, and predictive maintenance into their equipment. The region is witnessing investments in modernization and energy efficiency, mirrored in actions such as Sidel’s 2025 expansion of its Parma-based facility focused on PET packaging and digital-ready filling technology. Strategic developments include partnerships with robotics companies, such as Syntegon’s 2023 collaboration with Stäubli Robotics, aimed at delivering faster pick-and-place solutions for confectionery and bakery lines.

Asia Pacific Packaging Machinery Market Trend - High-Volume Manufacturing, Smart Packaging Lines & Rapid Regional Capacity Growth

Asia Pacific is projected to be the largest market, accounting for around 44% of the global demand. The region’s leadership is driven by large-scale production in food, beverages, personal care, and pharmaceuticals across China, Japan, India, and Southeast Asia. China dominates in both consumption and domestic machinery production, exemplified by Newamstar’s 2024 commissioning of a smart beverage filling line in Jiangsu, featuring digital OEE analytics and aseptic capabilities.

Growth is further fueled by manufacturing expansion and local sourcing initiatives, such as Hindustan Unilever’s 2024 investment in a new automated packaging facility in Maharashtra, India, which incorporates robotics-assisted cartoning and high-speed flexible packaging lines. E-commerce expansion in India and Southeast Asia is driving demand for multi-SKU systems, particularly lightweight flexible formats. Regulatory improvements, including India’s FSSAI packaging standards and China’s GMP upgrades, are encouraging the adoption of validated, sophisticated machinery.

OEMs are strengthening regional footprints, with Bosch/Syntegon, IMA, Sidel, KHS, and several Japanese manufacturers expanding local assembly and after-sales service hubs in China, Thailand, and India to reduce lead times. Investment trends focus on aseptic packaging, recyclable material compatibility, and digital automation. Asia Pacific is set to remain the global growth engine through 2033, supported by industrialization, demographic expansion, and continuous modernization of consumer-goods manufacturing. Brands such as PepsiCo, Nestlé, and Amcor have announced 2023–2025 capacity expansions integrating advanced filling, labeling, inspection, and flexible packaging technologies.

Competitive Landscape

The global packaging machinery market is moderately fragmented, with major OEMs offering full-line solutions and numerous regional players focusing on specific machine types. High-value segments, such as aseptic filling, full bottling lines, and pharmaceutical-grade packaging, are more consolidated, dominated by a few global leaders. In contrast, commodity equipment, such as basic cartoners and case packers, remains highly competitive regionally. Top OEMs capture a large share of capital-intensive projects, whereas smaller specialists serve modular, retrofit, and custom solutions. Leading companies differentiate through automation, robotics, integrated controls, and digital services, while growth strategies emphasize geographic expansion, SME-focused modular designs, and specialization in regulated sectors.

Key Industry Developments

- In May 2025, ProMach expanded its portfolio by acquiring DJS Systems, a US-based automation specialist for disposable food service packaging, thereby broadening ProMach’s capabilities in fast-moving consumer goods automation.

- In March 2025, Packsize launched its new X6 automated right-sized packaging system, aiming to meet on-demand packaging needs and optimize shipping, especially for e-commerce, shipping optimization, and lower-waste operations.

Companies Covered in Packaging Machinery Market

- Krones AG

- Bosch Packaging Technology (Syntegon)

- Tetra Pak

- Sidel

- IMA Group

- KHS GmbH

- ProMach Inc.

- GEA Group

- Marchesini Group

- MULTIVAC

- Ishida Co., Ltd.

- Sacmi Group

- Barry-Wehmiller

- Arpac LLC

- Coesia Group

- Newamstar Packaging Machinery

- SIG Combibloc Group

- Hayssen Flexible Systems (now part of Barry-Wehmiller)

- Packsize International

- Bosch (Controls & robotics division integrated in packaging lines)

Frequently Asked Questions

The global packaging machinery market size is estimated to reach US$61.2 billion in 2026.

By 2033, the packaging machinery market is expected to reach US$81.6 billion.

Key industry trends include rising automation and robotics adoption to address labor shortages and improve throughput, and a strong regulatory push for sustainable packaging, boosting mono-material and recyclable-material compatible machinery.

The filling machines segment leads with a 27.6% share in 2025, driven by high demand from beverages, dairy, oils, sauces, and other liquid or viscous products.

The packaging machinery market is projected to grow at a CAGR of 4.2% between 2026 and 2033.