- Non-food Packaging

- Aerosol Packaging Market

Aerosol Packaging Market Size, Share, and Growth Forecast 2026 - 2033

Aerosol Packaging Market by Product Type (Cans, Bottles & Cylinders, and Jars), Material (Aluminum, Tin Plated Steel, Plastic, and Steel), Cap Type (Actuators, Trigger Sprayer, Trigger Sprayer, and Other Dispensing Caps), End-user (Food and Beverages, Personal Care & Cosmetics, Aerated Desserts, Home Care, and Others), and Regional Analysis for 2026 to 2033

Aerosol Packaging Market Size and Share Analysis

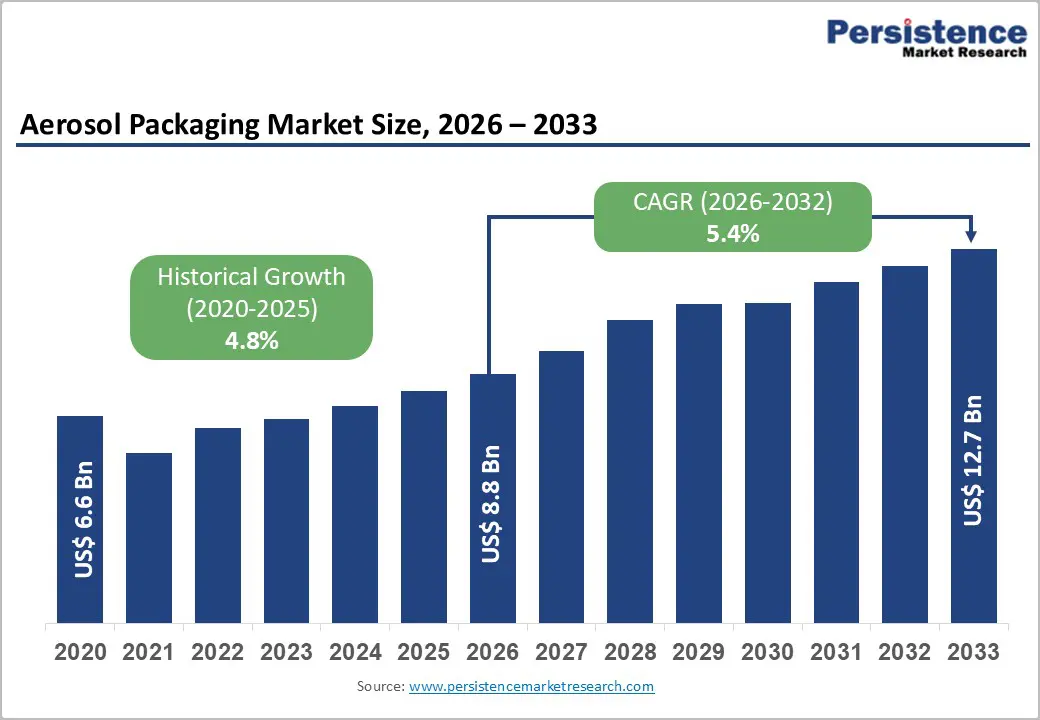

The global aerosol packaging market size is likely to be valued at US$ 8.8 billion in 2026 and is projected to reach US$ 12.7 billion by 2032, growing at a CAGR of 5.4% between 2026 and 2033.

Market expansion is driven by accelerating demand for personal care and cosmetics products, rapidly growing food and beverage applications, including convenience foods and ready-to-use dessert toppings, and escalating adoption of home care products across residential and commercial settings.

Key Industry Highlights:

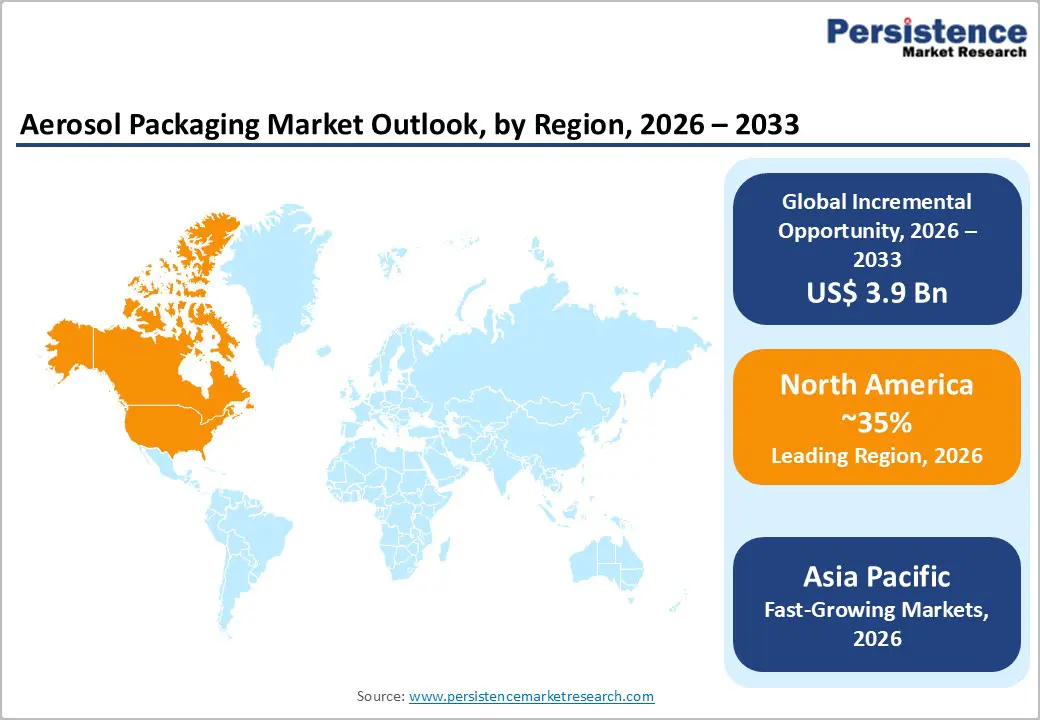

- Leading Region: North America dominates the global aerosol packaging market with a commanding 35% market share, anchored by the United States' substantial demand across personal care, household, food and beverages, and pharmaceutical applications.

- Fastest-Growing Region: Asia-Pacific emerges as the fastest-growing regional market, with a 7.8% CAGR through 2033, propelled by India's cosmetics industry, China's manufacturing dominance, urbanization in emerging economies, and the expansion of middle-class consumer demographics, which drive personal care and household product demand.

- Dominant End Use: Personal care and cosmetics represent the dominant application segment, commanding a 40% market share and experiencing accelerated growth driven by rising demand for grooming and hygiene products and clean beauty movement trends.

- Growing Cap Type: Food and beverage aerosol applications experience the fastest growth, with a 6.2% CAGR through 2033, driven by expansion of the convenience food market, growth in the whipped cream segment, and greater accessibility of e-commerce platforms, which enhance consumer product discovery and purchase behavior.

- Key Market Opportunity: Sustainable aerosol packaging innovations represent a significant growth opportunity, driven by global environmental commitments, circular-economy initiatives, emerging bio-based propellant technologies, and refillable-system development that addresses regulatory requirements and consumer sustainability preferences.

| Key Insights | Details |

|---|---|

| Aerosol Packaging Market Size (2026E) | US$ 8.8 Bn |

| Market Value Forecast (2033F) | US$ 12.7 Bn |

| Projected Growth CAGR(2026 - 2033) | 5.4% |

| Historical Market Growth (2020 - 2025) | 4.8% |

Market Dynamics

Drivers - Surging Personal Care and Cosmetics Product Consumption

The personal care and cosmetics sector is the largest and fastest-growing end-use category for aerosol packaging, driven by accelerating consumer demand for grooming, hygiene, and cosmetic products that use aerosol delivery systems. Deodorants, hair sprays, shaving creams, sunscreen, dry shampoo, body lotions, and facial mists increasingly use aerosol formats due to their superior convenience, precise application, single-handed dispensing, and product protection. The Indian cosmetic industry alone is projected to expand to USD 20 billion by 2025, exemplifying rapid emerging market growth in this category.

Consumer preference for premium personal care products, coupled with rising disposable incomes across developing economies and growing awareness of personal hygiene standards, is generating unprecedented demand for aerosol-packaged grooming and cosmetic solutions. The clean beauty movement is further accelerating the adoption of aerosol technology for delivering natural ingredient formulations, allergen-free options, and preservative-free products requiring advanced containment and preservation characteristics. Aerosol technology's ability to protect sensitive formulations while enabling precise dosage application positions it as the optimal packaging solution for premium cosmetic segments, supporting sustained market growth across diverse consumer demographics and geographic regions.

Rising Demand for Convenience-Oriented Consumer Products

The accelerating demand for convenience-oriented, ready-to-use consumer products across personal care, household, healthcare, and food applications is a key driver of the global aerosol packaging market. Aerosol packaging offers precise dispensing, uniform spray patterns, extended shelf life, and superior product protection, making it highly attractive for modern consumers seeking ease of use and consistent performance. Rapid urbanization, rising disposable incomes, and increasingly time-constrained lifestyles, especially in emerging economies, have significantly boosted the consumption of aerosol-based products such as deodorants, hair sprays, shaving foams, air fresheners, disinfectants, insect repellents, and automotive sprays. The personal care and cosmetics sector remains a key growth engine, as grooming and hygiene awareness continue to rise globally, supported by social media influence and premiumization trends.

Rising focus on sanitation and infection control following global health events, guided by organizations such as the World Health Organization, has accelerated demand for aerosolized disinfectants and medical sprays. From a packaging standpoint, aerosols provide tamper resistance, controlled dosage, and contamination prevention, which are critical attributes for both healthcare and household cleaning products. Advancements in valve systems, propellant technologies, and lightweight aluminum and steel cans have improved perceptions of safety, portability, and sustainability, thereby further strengthening adoption. Leading FMCG manufacturers are leveraging aerosol formats to differentiate products and enhance user experience, particularly in competitive retail environments.

Restraint - Stringent Regulatory Compliance Requirements and Sustainability Mandates

Regulatory frameworks across major markets are imposing increasingly complex compliance requirements impacting aerosol packaging manufacturers' operational costs and market access strategies. The European Union's Packaging and Packaging Waste Regulation (EU) 2025/40 establishes ambitious sustainability requirements mandating 30% recycled aluminum and 50% recycled steel in aerosol containers by 2030, alongside aggressive recycling targets requiring 80% ferrous metals and 60% aluminum recycling by 2030. These regulatory mandates necessitate substantial capital investments in advanced manufacturing technologies, recycling-infrastructure partnerships, and supply-chain optimization to achieve compliance within specified timelines.

The EU Aerosol Dispensers Directive (ADD) 75/324/EEC and its amendments establish rigorous safety, labeling, and pressure-resistance standards that require manufacturers to conduct costly compliance testing and validation procedures. Equivalent regulatory frameworks in North America, including CPSIA restrictions on certain aerosol products and Extended Producer Responsibility (EPR) programs in five states (California, Colorado, Maine, Minnesota, and Oregon), create additional compliance burdens. These regulatory complexities increase operational costs, disproportionately affecting smaller regional manufacturers that lack scale economies, thereby consolidating market participation around larger, well-capitalized companies capable of absorbing compliance costs.

Environmental Concerns Regarding Propellants and Propellant Transitions

Environmental concerns regarding conventional aerosol propellants are driving regulatory restrictions and manufacturers' voluntary transitions toward alternative propellant technologies, creating market uncertainty and requiring significant research and development investments. Traditional hydrofluorocarbon propellants used in pharmaceutical respiratory products and cosmetic aerosols face phase-out requirements, necessitating transition to low-global-warming-potential alternatives, including dimethyl ether and hydrofluoro-olefins (HFO-1234ze(E)), which require extended manufacturing scale-up periods and validation testing before market-wide adoption.

AstraZeneca's commitment to convert its respiratory portfolio to HFO-1234ze(E) by 2030 exemplifies the propellant transition timelines of large pharmaceutical manufacturers, creating near-term supply disruptions and manufacturing complexity. The propellant transition requirement imposes substantial costs on formulation development, manufacturing process modifications, and regulatory approvals, disproportionately affecting smaller aerosol product manufacturers that lack dedicated research capabilities. Uncertainty regarding future propellant restrictions and potential regulatory changes creates planning challenges for manufacturers, potentially delaying product launches and market expansion initiatives.

Opportunity - Expansion of Pharmaceutical and Medical Aerosol Applications

The increasing use of aerosol delivery systems in pharmaceutical and medical applications is a significant opportunity for the aerosol packaging market. The global healthcare sector is witnessing sustained growth driven by aging populations, rising prevalence of chronic respiratory diseases such as asthma and COPD, and increasing demand for home-based and self-administered therapies. Aerosol packaging plays a critical role in these treatments by enabling accurate, metered, and contamination-free drug delivery, which is essential for patient safety and therapeutic effectiveness. Pressurized metered-dose inhalers (pMDIs), nasal sprays, wound-care sprays, antiseptics, and topical pain-relief products rely heavily on advanced aerosol containers, valves, and actuators. Continuous innovation in precision valves and dose-control mechanisms is improving drug efficacy while reducing medication wastage, creating strong value propositions for pharmaceutical manufacturers.

Furthermore, rising healthcare access in emerging economies and expanding insurance coverage are increasing the penetration of aerosol-based medical products across both urban and semi-urban markets. Regulatory bodies such as the U.S. Food and Drug Administration and the European Medicines Agency continue to emphasize stringent packaging standards for sterility, dosage accuracy, and patient safety. This regulatory focus raises entry barriers but also creates opportunities for specialized aerosol packaging suppliers to provide compliant, high-performance solutions. Growth in telemedicine and home-care treatment models is accelerating demand for portable, easy-to-use aerosol devices that support patient adherence and convenience. As pharmaceutical companies invest in advanced drug-delivery platforms and expand product pipelines, the medical aerosol segment offers long-term, high-margin growth opportunities for packaging manufacturers capable of meeting complex regulatory and technical requirements.

Sustainable Packaging Innovation and Circular Economy Initiatives

Sustainable aerosol packaging represents a significant market opportunity driven by global focus on environmental protection and circular economy principles, creating demand for innovative materials and refillable system technologies. The sustainable aerosol packaging market is projected to grow substantially, exceeding overall market growth rates and reflecting accelerating corporate and consumer commitment to environmental sustainability. Leading companies, including Ball Corporation and Crown Holdings, are advancing material science innovations, including Ball's ReAl alloy technology, which reduces can body carbon footprint by 50% while maintaining structural strength, and Crown's tamper-resistant child-safe packaging designs, addressing both environmental and safety requirements.

Emerging innovations in bio-based polymers, lightweight metal alloys, and refillable aerosol systems are enabling the development of fully recyclable and carbon-neutral packaging solutions. Companies are increasingly establishing closed-loop supply chain relationships with recycling partners, developing bag-on-valve systems that achieve 99% product evacuation and propellant volume reduction, and integrating digital printing and smart labeling technologies to enhance traceability and sustainability communication. Emerging markets across Asia-Pacific and Latin America, where sustainability awareness is rapidly expanding, present profitable expansion opportunities for multinational manufacturers by establishing local, eco-friendly production facilities and supporting supply chain partnerships aligned with circular economy principles.

Category-wise Analysis

Product Type Insights

Cans represent the leading product type, accounting for the largest share of global demand. Aerosol cans, primarily manufactured from aluminum and steel, are widely preferred for their excellent pressure resistance, durability, lightweight, and compatibility with a broad range of applications. They are widely used in personal care, household, automotive, industrial, and pharmaceutical products, including deodorants, air fresheners, sprays, lubricants, and medical inhalers. The ability of cans to provide uniform dispensing, extended shelf life, and strong product protection has made them the industry standard for mass-market aerosol formulations. In addition, high recyclability rates and well-established collection infrastructure further reinforce their dominance, particularly in mature markets.

Bottles & cylinders are emerging as the fastest-growing product type, driven by rising adoption in pharmaceuticals, medical sprays, specialty chemicals, and premium personal care products. These formats are gaining traction due to their suitability for compressed gas systems, high-pressure medical applications, and reusable or refillable designs. Growth is also supported by increasing demand for portable, precise-dose delivery systems and expanding healthcare access in emerging economies. As innovation in materials and valve technologies continues, bottles and cylinders are expected to experience accelerated growth, gradually expanding their market share alongside traditional aerosol cans.

Material Insights

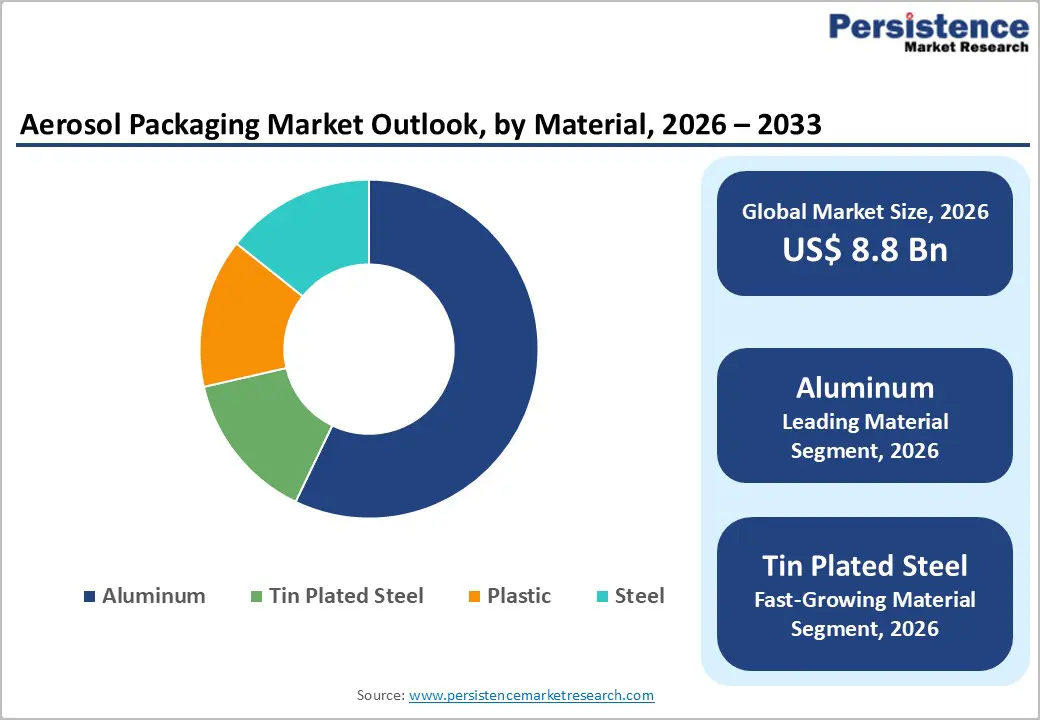

Aluminum represents the dominant material in the aerosol packaging market, commanding approximately 55% market share due to its superior properties, including infinite recyclability, lightweight characteristics, corrosion resistance, and established global recycling infrastructure. Aluminum aerosol containers serve diverse applications across personal care, food and beverages, pharmaceuticals, and industrial sectors, with manufacturers preferring aluminum for premium personal care and cosmetics products where material aesthetics, product protection, and sustainability credentials provide competitive differentiation. The International Organisation of Aluminium Aerosol Container Manufacturers (AEROBAL) reported a 6.6% increase in global aluminum aerosol deliveries in the first half of 2023, with deliveries exceeding 3.2 billion units, indicating strong underlying demand.

Aluminum's environmental advantages, including that 75% of aluminum ever produced remains in active circulation through established recycling markets, position it as a sustainable material choice aligned with evolving regulatory requirements and corporate environmental commitments. Manufacturing advancements enabling reduced material thickness and lightweight designs have lowered costs while maintaining structural integrity and product protection capabilities. Leading manufacturers including Ball Corporation emphasize aluminum aerosol sustainability credentials, with the company achieving 85% recycled content in aluminum cans and obtaining FDA approval for food-grade aluminum aerosols, establishing aluminum's dominance across premium and regulated applications.

Cap Type Insights

Actuator caps represent the traditional and largest cap type segment in aerosol packaging, maintaining dominance across conventional spray application categories. Trigger sprayers have emerged as a fast-growing cap-type category, gaining market share through improved ergonomic designs, enhanced user control, and reduced propellant consumption relative to traditional actuators. Trigger sprayer adoption is accelerating in household cleaning products, personal care applications, and food product categories where consumer preference for controlled dispensing and reduced waste drives specification updates.

Fine mist sprayers, while representing a smaller market segment, are experiencing rapid growth in premium personal care, fragrance, and pharmaceutical applications where precise, uniform mist patterns deliver superior product efficacy and user experience. Fine mist sprayer technology is particularly valued in cosmetic and pharmaceutical aerosol applications, where precise dosage delivery and minimal propellant consumption are critical performance requirements. Emerging smart cap technologies with integrated sensors for expiry tracking and personalized usage recommendations represent innovation frontiers, with commercial deployment anticipated in 2026 - 2027 timeframes as companies develop cost-effective sensor integration methodologies.

End-user Insights

Personal care & cosmetics, with 40% market share stands out as the leading end-user segment, accounting for the largest share of global consumption. This dominance is driven by the widespread use of aerosol formats in products such as deodorants, body sprays, hair sprays, shaving foams, dry shampoos, and skincare mists. Aerosol packaging offers controlled dispensing, uniform application, hygiene protection, and enhanced user convenience, features that strongly align with consumer expectations in grooming and beauty products. Rising disposable incomes, urban lifestyles, premiumization trends, and growing awareness of personal hygiene across both developed and emerging economies continue to sustain demand for this segment.

Food and Beverages is emerging as the fastest-growing end-user segment, particularly within niche categories such as non-dairy whipping creams, aerated desserts, edible oils, salad dressings, and cocktail foam toppings. Aerosol packaging enables precise portion control, extended shelf life without preservatives, and improved product texture and presentation, making it increasingly attractive for both household and foodservice applications. Growth in café culture, premium home cooking, plant-based alternatives, and convenience foods is accelerating the adoption of these products. As food brands innovate with value-added and experiential products, aerosol packaging is gaining momentum, positioning the food and beverage segment as a key growth engine for the market.

Regional Insights

North America Aerosol Packaging Market Trends

North America represents the world's largest aerosol packaging market, commanding approximately 40% global market share, with the United States representing the dominant regional economy. The U.S. market demonstrates robust demand across personal care, household products, food and beverage, pharmaceutical, and industrial applications, with North America experiencing 11% delivery growth in aerosol packaging volumes. The regulatory framework, including CPSIA restrictions on certain aerosol products intended for children and FDA food-grade approvals for specific aerosol applications, establishes comprehensive safety standards while creating market access barriers protecting established suppliers capable of achieving compliance.

The U.S. represents a global innovation epicenter for aerosol technology, with leading companies including Ball Corporation, Crown Holdings, and Aptar Group headquartered in North America and maintaining cutting-edge research and development facilities supporting next-generation aerosol technologies. Established recycling infrastructure and growing consumer demand for sustainable packaging solutions are driving the adoption of aluminum and steel aerosol containers with elevated recycled content and circular economy designs. The emergence of Extended Producer Responsibility (EPR) programs in five states (California, Colorado, Maine, Minnesota, and Oregon) is creating regulatory momentum for comprehensive packaging management systems, encouraging aerosol container design optimization and return infrastructure development.

Europe Aerosol Packaging Market Trends

Europe represents a significant aerosol packaging market, valued at approximately 30% of global aerosol packaging demand, with Germany maintaining leadership through advanced manufacturing capabilities and innovation in sustainable aerosol technologies. Germany's strong tradition in precision engineering, combined with chemical manufacturing expertise, supports leadership in aerosol innovation and specialty container development. The European Union's Packaging and Packaging Waste Regulation (EU) 2025/40 establishes the world's most stringent aerosol packaging sustainability requirements, mandating a 30% minimum recycled aluminum content and a 50% minimum recycled steel content by 2030, alongside 80% ferrous metals and 60% aluminum recycling targets by 2030. These requirements are driving European manufacturers to invest heavily in advanced recycling partnerships, design optimization for recyclability, and sustainable material innovation. The United Kingdom, France, and Spain markets are experiencing steady growth driven by residential construction, commercial property development, and expanding household and personal care product categories.

Regulatory harmonization efforts around REACH (Registration, Evaluation, Authorisation and Restriction of Chemicals) and the EU Aerosol Dispensers Directive (ADD) 75/324/EEC create unified market standards that enable efficient manufacturing and distribution across European member states, while establishing competitive advantages for suppliers that demonstrate comprehensive regulatory compliance and sustainability leadership. Environmental sustainability initiatives and corporate carbon-neutral commitments are accelerating adoption of lightweight aluminum containers with elevated recycled content, driving premium pricing and market share gains for sustainability-focused suppliers.

Asia Pacific Aerosol Packaging Trends

Asia Pacific is the fastest-growing regional aerosol packaging market, with growth rates substantially exceeding those of developed market, delivering a CAGR of 7.8% or higher through 2033. China maintains the largest production base and consumption market in Asia-Pacific, leveraging cost-competitive manufacturing, established supply chain networks, and enormous domestic demand from the expanding personal care, household, and food industries. India represents the fastest-growing economy within the region, with the Indian cosmetic industry reaching USD 20 billion in 2025 and expanding at accelerated growth rates driven by rising middle-class demographics, increasing disposable incomes, and growing personal care product consumption.

India's competitive manufacturing cost structure and labor availability are attracting multinational manufacturer investment in local aerosol production capacity and contract manufacturing partnerships. Japan and South Korea maintain steady market positions leveraging technological expertise and advanced manufacturing capabilities in precision aerosol components and specialty container development. ASEAN countries, including Thailand, Vietnam, and Indonesia, are emerging as flexible manufacturing hubs for aerosol production, supporting both regional and global market supply. Government-sponsored manufacturing incentive programs, infrastructure modernization investments, and rising urbanization across the Asia Pacific are generating structural demand growth for personal care, household, and food beverage aerosol products throughout the forecast period.

Competitive Landscape

The aerosol packaging market exhibits a moderately consolidated competitive structure dominated by global conglomerates and specialized packaging manufacturers possessing significant production capacity and distribution networks. Tier 1 companies including Ball Corporation, Crown Holdings, and Trivium Packaging collectively command approximately 38% market share through economies of scale, modern manufacturing infrastructure, and well-established global distribution capabilities. Tier 2 manufacturers including AptarGroup Inc., Coster Group, and Lindal Group collectively manage approximately 36% market share, differentiating through product customization, sustainable material innovation, and high-efficiency dispensing systems.

Competitive strategies emphasize research and development investments in sustainable propellants, refillable aerosol systems, and lightweight material alloys. Market consolidation trends include Colep Packaging's acquisition of ALM Envases in December 2024, reflecting mid-tier converters' pursuit of scale and expanded technology portfolios. Supply chain resilience and raw-material pricing flexibility are emerging as critical competitive differentiators, as inflationary pressures and supply volatility create natural filters deterring under-capitalized entrants.

Key Developments:

- In September 2025, Ball Corporation, a global leader in sustainable aluminum packaging, collaborated with Brazilian brands Soffie and Aeroflex to introduce the world’s first aluminum aerosol cans certified by the Aluminium Stewardship Initiative (ASI). This certification ensures that the aluminum used meets rigorous environmental, social, and governance (ESG) standards throughout the value chain—from raw material extraction to finished packaging.

- In December 2025, Metal Press S.p.A. and Ferrari Meccanica S.p.A. announced their merger to establish New Box Aerosol, a specialized division focused on delivering fully customizable, sustainable, high-performance, and reliable aerosol packaging solutions to a wide range of industries across global markets.

- In April 2024, Crown Holdings, Inc. launched tamper-resistant, child-safe aerosol packaging that incorporates advanced safety mechanisms and ergonomic design features, meeting evolving regulatory requirements and brand safety standards while differentiating its product portfolio through enhanced consumer protection capabilities.

Companies Covered in Aerosol Packaging Market

- Berry Global, Inc.

- Crown Holdings, Inc.

- Ball Corporation

- CCL Industries Inc.

- Aptar Group Inc.

- Silgan Holdings Inc.

- Montebello Packaging Inc.

- Exal Corporation

- Graham Packaging Company

- Allied Cans Limited

- Euro Asia Packaging

- Nampak Ltd.

- ARYUM Metal

- TUBEX GmbH

- Bharat Containers

Frequently Asked Questions

The global aerosol packaging market is projected to reach US$ 12.7 billion by 2033, expanding from US$ 8.8 billion in 2026 at a CAGR of 5.4%, driven by personal care product demand, home care segment expansion, food and beverage application growth, and increasing adoption of sustainable aerosol packaging solutions.

Market demand growth is driven by multiple converging factors including surging personal care and cosmetics product consumption, rapid home care segment expansion, accelerating food and beverage aerosol adoption, and growing corporate sustainability commitments driving adoption of recyclable aluminum and steel containers.

Personal care and cosmetics represent the dominant application segment, commanding approximately 40% market share of global aerosol packaging demand, reflecting increasing grooming and hygiene product consumption, clean beauty movement trends.

North America commands market leadership with approximately 35% global aerosol packaging market share, anchored by the United States, which dominates through substantial personal care, household, food and beverage, and pharmaceutical application demand.

Major market opportunities include food and beverage aerosol expansion driven by convenience food growth, with whipped cream and cooking spray segments robust growth, packaging innovation, driven by circular economy initiatives and bio-based propellant development.

Leading market players include Crown Holdings, Inc. commanding approximately 18% global market share; Ball Corporation holding 15% market share, CCL Industries Inc., Aptar Group Inc. differentiating through high-efficiency dispensing systems; and Silgan Holdings Inc. providing sustainable rigid packaging solutions.