- Non-food Packaging

- Consumer Packaging Market

Consumer Packaging Market Size, Share, and Growth Forecast 2026 - 2033

Consumer Packaging Market by Product Type (Rigid, Flexible), Material Type (Plastic, Paper, Metal, Others), End-user (Food & Beverages, Personal Care & Hygiene, Pharmaceuticals, Consumer Electronics, Others), and Regional Analysis, for 2026 - 2033

Consumer Packaging Market Size and Trends Analysis

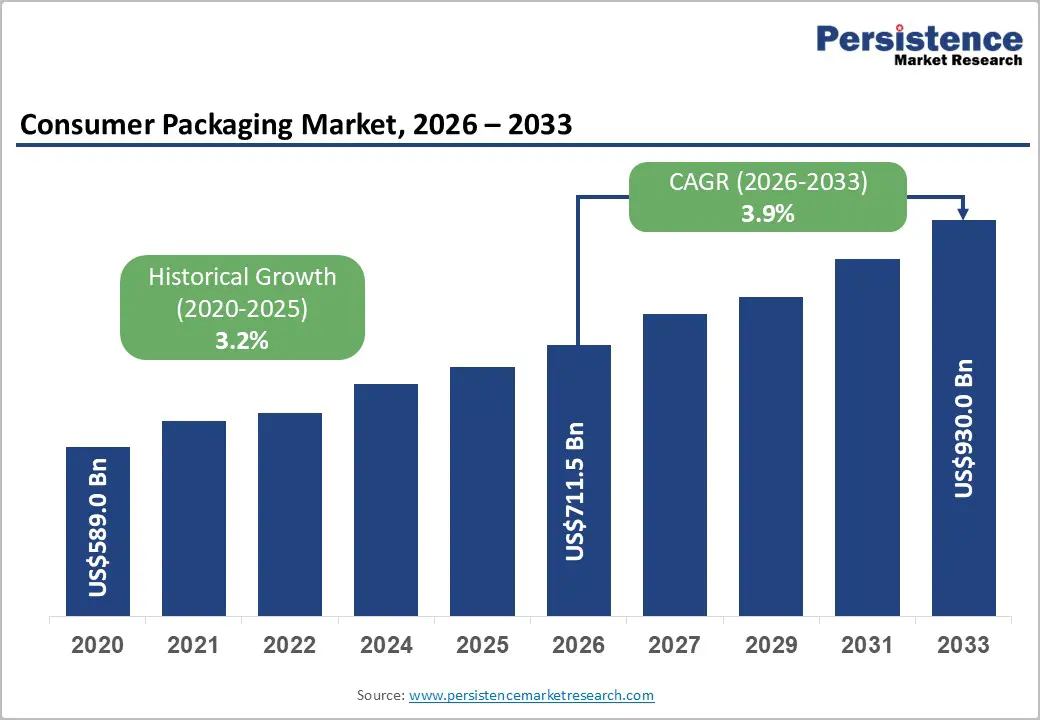

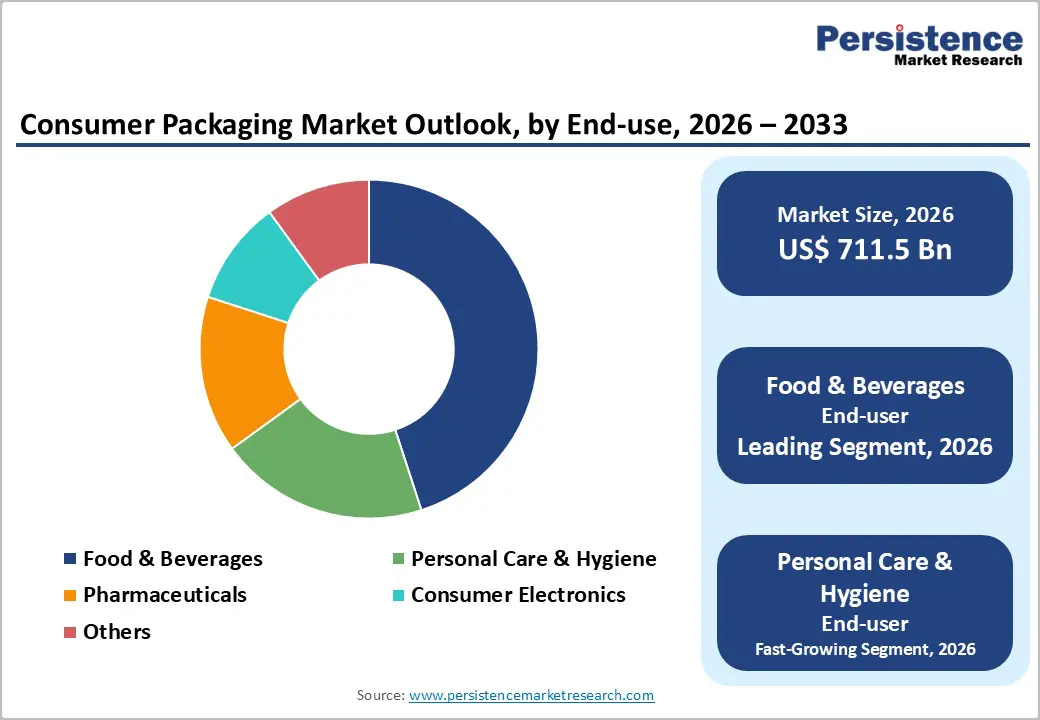

The global consumer packaging market size is expected to be valued at US$711.5 billion in 2026 and projected to reach US$930.0 billion by 2033, growing at a CAGR of 3.9% during forecast period 2026 - 2033, driven by the rapid expansion of e-commerce and tightening sustainability regulations, both of which are accelerating demand for lightweight, recyclable packaging solutions across global supply chains.

Rising urbanization is further increasing consumer preference for convenient and easy-to-handle packaging formats, while stringent food safety standards imposed by regulatory bodies such as the U.S. FDA and European authorities continue to drive innovation in compliant and high-performance packaging materials.

Key Industry Highlights:

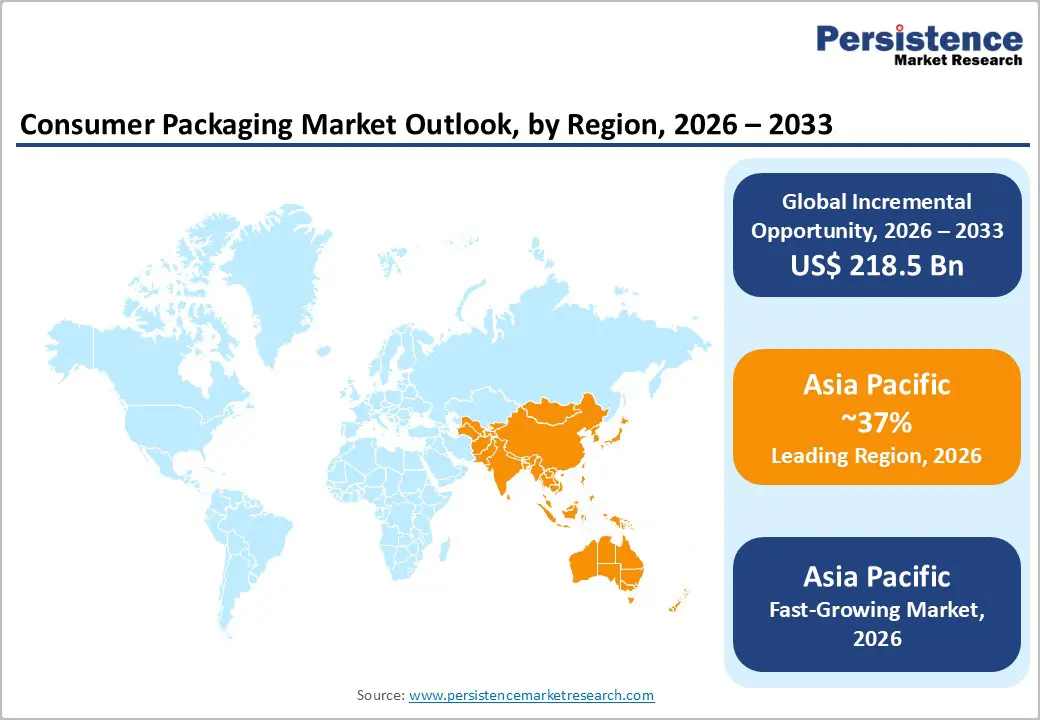

- Dominant Region: Asia Pacific is projected to lead the market with 37% of revenue in 2026, supported by rapid economic growth, urbanization, and rising disposable incomes, driving demand for packaged food, personal care, and household products.

- Fastest-growing Region: Asia Pacific is expected to be the fastest-growing region, driven by the rapid expansion of online shopping and direct-to-consumer sales, which is accelerating demand for durable, protective, and sustainable packaging solutions.

- Leading Product Type: Flexible packaging is expected to lead the market with over 50% share in 2026, as lightweight films, pouches, and bags help reduce transportation costs and material usage while supporting sustainability objectives.

- Dominant Material Type: The plastic segment is projected to lead the market with a 40% share in 2026, as formats such as films, bottles, tubs, and pouches provide strong barrier protection against moisture, oxygen, and contamination, making them essential for food, beverage, personal care, and household products.

| Key Insights | Details |

|---|---|

| Consumer Packaging Market Size (2026E) | US$711.5 Bn |

| Market Value Forecast (2033F) | US$930.0 Bn |

| Projected Growth CAGR (2026 - 2033) | 3.9% |

| Historical Market Growth (2020 - 2025) | 3.2% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - E-commerce and Direct-to-Consumer Surge

According to government data, accelerated online shopping and direct-to-consumer (D2C) sales have reshaped India’s retail landscape, significantly boosting demand for consumer packaging. In FY 2025, India’s e-commerce market was valued at approximately INR15.7 lakh crore (US$ 182 billion) and is projected to keep growing rapidly with wider internet access, smartphone penetration, and rising online shoppers across Tier II and Tier III cities. Internet subscriptions reached 969 million by March 2025, supporting expanding online orders and digital purchase frequency. This surge in online retail increases the volume of packaging required at every touchpoint from product fulfillment to delivery, driving investments in protective, branded, and sustainable packaging solutions tailored for e-commerce logistics.

Consumers increasingly expect safe, high-quality packaging for doorstep delivery, stimulating innovation in lightweight, durable, and visually appealing materials that enhance brand experience and reduce transit damage. As online retail continues to penetrate deeper into regional markets, packaging formats that support efficient handling, tracking, and returns have become essential for direct-to-consumer and online sellers adapting to evolving consumer behaviors and fulfillment models.

Sustainability Regulations and Consumer Preferences

Sustainability regulations and shifting consumer preferences are significantly influencing the consumer packaging market by accelerating demand for eco-friendly materials and circular packaging solutions. Governments around the world, including in India, are enacting stricter regulations on single-use plastics and mandating higher recycled content in packaging. For example, India’s Plastic Waste Management (Amendment) Rules require phased reduction and eventual elimination of specified single-use plastics, while promoting extended producer responsibility (EPR) frameworks that hold manufacturers accountable for post-consumer waste collection and recycling. These regulations push brands to redesign packaging formats, use recyclable or compostable materials, and invest in infrastructure to meet compliance targets.

Consumers are increasingly valuing sustainability as a purchase driver. Surveys and shopping behavior indicate that shoppers are willing to choose products with recyclable packaging, minimal environmental impact, and clear sustainability labeling. This preference is especially strong among younger demographics and urban consumers, prompting brands to adopt renewable materials like bio-based plastics, paper, and molded fibers. Retailers also emphasize sustainability in private-label offerings and marketing campaigns, reinforcing the trend.

Barrier Analysis - Fluctuating Raw Material Prices

Fluctuating raw material prices create significant challenges for the consumer packaging market because packaging costs are closely tied to the price of key input materials such as polymers, paperboard, aluminum, and glass. These commodities are influenced by global supply chain dynamics, energy costs, and trade policies, leading to volatility that can quickly change production costs for packaging manufacturers. When crude oil prices rise, for example, the cost of plastic resins used in flexible and rigid packaging tends to increase, squeezing margins for converters and brand owners.

This volatility complicates contract negotiations between suppliers and buyers, as forward pricing becomes risky and inventory carrying costs may rise. Smaller packaging firms with limited hedging capabilities are especially exposed to sudden cost shifts. To manage this unpredictability, companies explore material substitution, long-term supplier agreements, and design optimization to reduce material use and maintain competitiveness without transferring full cost increases to end consumers.

Complex Recycling Infrastructure Gaps

Recycling infrastructure gaps pose a major challenge for the consumer packaging market because many regions lack the collection, sorting, and processing capacity needed to recover materials effectively. Inadequate curbside pickup, limited access to material recovery facilities, and inconsistent waste segregation at the source mean that a large portion of packaging, especially multi-layer plastics and composites, ends up in landfills or informal waste streams.

These infrastructure shortfalls also discourage investment in recyclable or reusable packaging formats, since manufacturers and retailers worry that end-of-life systems cannot handle new materials at scale. Gaps in standardized labeling and consumer awareness further reduce recycling rates and contaminate material streams, complicating downstream processing.

Opportunity Analysis - Paper-Based Packaging Transition

The steady shift toward paper-based packaging presents a major opportunity for the consumer packaging market as brands and regulators align on sustainability and circularity. In November 2025, a trusted study reported that in India, the paper packaging segment reached INR 167,110 crore (approximately US$19.07 billion) as of August 2025 and is projected to grow strongly toward INR 406,866 crore (US$49 billion) by 2030, indicating robust demand for renewable packaging formats. This expanding segment offers converters and brand owners a chance to tap into growing requirements for recyclable and biodegradable materials, reducing reliance on plastics and enhancing environmental credentials in the eyes of consumers and policymakers.

Growth in paper packaging is supported by a well-established domestic paper and paperboard ecosystem, with India’s mills producing around 25 million tonnes annually and high utilization levels reflecting both scale and resilience. Sustainability initiatives such as the National Mission on Sustainable Packaging Solutions aim to foster innovation in materials and recycling, further strengthening the appeal of paper-based formats. As consumer demand favors recyclable, low-impact packaging for everything from FMCG to e-commerce deliveries, paper alternatives create value-added opportunities for differentiated products and drive market expansion.

Growing Demand from the Food & Beverages Sector in India

India’s expanding food & beverages (F&B) sector is creating a strong opportunity for the consumer packaging market as rising consumption and packaged food demand increase the volume and diversity of packaging requirements. According to a report published by a trusted industry source in 2025, the food processing industry in India was valued at INR 3,049,800 crore (US$354.5 billion) in 2024 and is projected to grow further, with overall food consumption expected to reach US$1.2 trillion by 2026, due to urbanization and evolving dietary patterns that emphasize convenience and safety. Such growth boosts demand for packaging formats that preserve quality, extend shelf life, and support supply chain logistics across fresh, processed, and ready-to-eat categories.

Packaged segments such as snacks, beverages, dairy, and ready meals are increasingly purchased through retail and quick-commerce channels, reinforcing the need for innovative, sustainable, and functional packaging solutions. With more consumers opting for packaged options for on-the-go lifestyles, packaging manufacturers can expand offerings in barrier materials, portion-controlled packs, and recyclable formats that meet both convenience and environmental expectations. This end-use expansion drives greater investment in advanced packaging technologies and materials, enhancing the overall consumer packaging market’s growth trajectory.

Category-wise Analysis

Product Type Insights

Flexible packaging is anticipated to dominate with over 50% of the share in 2026, fueled by its versatility, cost-effectiveness, and performance advantages across food, beverage, personal care, and household segments. Lightweight films, pouches, and bags reduce transportation costs and material use, supporting both economic and sustainability goals. Their excellent barrier properties help extend shelf life and preserve product quality, which is especially valued in packaged foods and perishable goods. Chobani shifted products such as Chobani Savor squeezable yogurt and Chobani Gimmies into inverted resealable pouches and other flexible formats to better meet consumer convenience and storage needs. These flexible packages helped the brand offer easier use and improved portability compared with rigid containers, aligning packaging with modern lifestyle preferences.

Rigid packaging is likely to be the fastest-growing product type, propelled by brands seeking durable, protective solutions for higher-value and sensitive products such as premium beverages, electronics, cosmetics, and pharmaceuticals. Consumers increasingly associate rigid formats like PET bottles, glass jars, and metal cans with quality and safety, driving adoption in both retail and e-commerce channels. Rigid packaging also enhances brand differentiation through printing, shaping, and structural design options that support premium positioning. For instance, in 2024, Amcor launched a new lightweight rigid container targeted at the personal care market to reduce material use and improve recyclability, broadening its rigid packaging portfolio and meeting rising consumer and sustainability demands.

Material Type Insights

The plastic segment is expected to lead, hold 40% share in 2026, due to its combination of light weight, durability, versatility, and cost efficiency. Plastic formats such as films, bottles, tubs, and pouches offer excellent barrier properties that protect products from moisture, oxygen, and contamination, which is critical for food, beverage, personal care, and household goods. Their low transportation weight helps reduce logistics costs, while ease of molding and printing supports brand differentiation. For instance, Manjushree Technopack, which specializes in producing rigid plastic bottles, containers, and PET preforms with a converting capacity of over 175,000 MT of PET, HDPE, and PP plastics per year to serve FMCG, food, dairy, and personal care sectors, highlights the strong demand and scale of plastic packaging solutions in major consumer categories.

The paper segment is likely to be the fastest-growing material type, as brands and consumers increasingly prioritize sustainability, recyclability, and reduced environmental impact. Paperboard, cartons, and molded fiber products offer renewable feedstock and widespread recycling infrastructure, making them attractive for food, beverage, and consumer goods packaging that needs to balance performance with eco-credentials. Consumer demand for recyclable and responsibly sourced materials has pushed companies to redesign packaging away from hard-to-recycle composites toward mono-material paper formats. For example, Mondi Group developed recyclable paper bags for chemical powders in partnership with Evonik to replace plastic-coated packaging. This two-ply paper bag reduced overall packaging weight by about 30% and lowered its carbon footprint, while remaining fully recyclable under CEPI and 4evergreen standards.

Regional Insights

North America Consumer Packaging Market Trends

North America is evolving rapidly due to strong sustainability pressure and shifts in consumer preferences toward environmentally responsible solutions. U.S. states such as California have introduced Extended Producer Responsibility (EPR) mandates aimed at reducing single-use plastics and increasing recyclable content, prompting brands to rethink materials and packaging design to comply with stricter rules.

E-commerce growth continues to influence packaging formats, with online retail driving demand for lightweight, durable, and sustainable mailers and protective cartons tailored for shipping and handling. Flexible and smart packaging technologies, such as QR codes and RFID for traceability, are gaining traction to enhance consumer engagement and freshness monitoring. Circular economy initiatives and expanded recycling infrastructure further bolster the region’s shift toward eco-friendly packaging models, while companies increasingly invest in material innovation and reusable formats to align with both regulatory requirements and eco-conscious consumers.

Europe Consumer Packaging Market Trends

Europe sustainability and regulatory action are the strongest trends shaping growth and innovation. The Packaging and Packaging Waste Regulation (PPWR) entered into force to make all packaging recyclable in an economically viable way by 2030, curb the use of virgin materials, and boost recycled content in plastic packaging, aligning with broader circular economy goals. These rules also restrict certain single-use plastics and set life-cycle requirements covering design, reuse, and waste handling. Member states are required to increase recycling targets; for example, all packaging recycling is set to rise toward higher thresholds for paper/cardboard and glass while encouraging clearer consumer information and sorting systems.

European consumers strongly value recyclable packaging, with a large majority actively seeking recyclability instructions on products and making such claims influential in purchasing decisions. This consumer preference pushes brands to adopt eco-friendly materials and to rethink designs toward materials that are easier to recycle or reuse.

Asia Pacific Consumer Packaging Market Trends

Asia Pacific is projected to dominate and be the fastest-growing, capturing the 37% revenue in 2026, driven by rapid economic growth, urbanization, and rising disposable incomes, which are driving strong demand for packaged goods across food & beverages, personal care, and household products. China’s large base of online shoppers and extensive industrial infrastructure underpin broad adoption of diverse packaging formats that meet both protective and aesthetic needs.

E-commerce expansion and rising digital penetration are reshaping packaging requirements, as more products are shipped directly to consumers, increasing the need for protective, lightweight, and customized packaging solutions. Consumer awareness about sustainability and government support for eco-friendly materials further stimulate demand for recyclable and biodegradable packaging across the region.

Competitive Landscape

The global consumer packaging market is highly fragmented, with multinational giants such as Amcor coexisting alongside numerous regional and local players. The top five companies collectively account for roughly 30% of the market, highlighting a competitive landscape where scale, innovation, and supply chain integration are critical for differentiation. Leading players focus heavily on research and development in mono-material packaging, which simplifies recycling and supports sustainability commitments. Traceability certifications, such as FSC (Forest Stewardship Council) for paper-based packaging, provide additional value by verifying responsible sourcing and appealing to environmentally conscious consumers.

Circular economy initiatives are becoming central to competitive strategy, with retailers exploring leasing and reusable packaging models to reduce waste and encourage returns. These models allow brands to enhance consumer engagement while minimizing material consumption. Investment in lightweighting, sustainable materials, and digital monitoring technologies further strengthens market position, enabling leaders to meet regulatory requirements, satisfy growing eco-conscious consumer demand, and maintain cost efficiency across increasingly complex supply chains.

Key Industry Developments:

- In February 2026, Indorama Ventures and AMB Spa launched fully recyclable PET trays in Europe, combining recycled PET cores with virgin outer layers to ensure food safety and recyclability, supporting circular packaging and EU compliance.

- In February 2026, Legrand announced a major sustainability initiative by transitioning the packaging for its standard wall plates to a compostable, bio-based material called NatureFlex. The company projected that this change would eliminate 117 tons of single-use fossil-fuel-based plastic from the waste stream annually, reducing environmental impact and advancing its commitment to sustainable packaging practices.

Companies Covered in Consumer Packaging Market

- Amcor plc

- Sonoco Products Company

- Berry Global Inc.

- Huhtamaki

- DS Smith

- Smurfit Kappa

- Stora Enso

- Graphic Packaging International, LLC

- ITC Limited

- Constantia Flexibles

- TCPL Packaging Limited

- UFlex Limited

- Mayr-Melnhof Karton AG

- Bekum Group

- Altium Packaging

Frequently Asked Questions

The global consumer packaging market size is expected to be valued at US$711.5 billion in 2026.

Growing consumer and regulatory demand for sustainable and recyclable packaging is pushing companies to adopt eco-friendly materials, reduce single-use plastics, and invest in circular packaging solutions.

The consumer packaging market is anticipated to grow at a CAGR of 3.9% during 2026 - 2033.

Expansion of e-commerce and direct-to-consumer channels creates demand for innovative, durable, and protective packaging formats, enabling brands to differentiate products while improving supply chain efficiency and consumer convenience.

Leading key players are Amcor plc, Sonoco Products Company, Berry Global Inc., Huhtamaki, DS Smith, and Smurfit Kappa.