- Specialty & Fine Chemicals

- Natural Fatty Acids Market

Natural Fatty Acids Market Size, Share, and Growth Forecast 2026 - 2033

Natural Fatty Acids Market by Source (Vegetable Oils, Animal-Based, Others), Product Type (Saturated, Unsaturated), Form (Solid, Liquid), Application (Soaps & Detergents, Personal Care & Cosmetics, Food & Beverages, Pharmaceuticals, Lubricants, Rubber & Plastics, Textiles, Animal Feed), and Regional Analysis, 2026 - 2033

Natural Fatty Acids Market Size and Trend Analysis

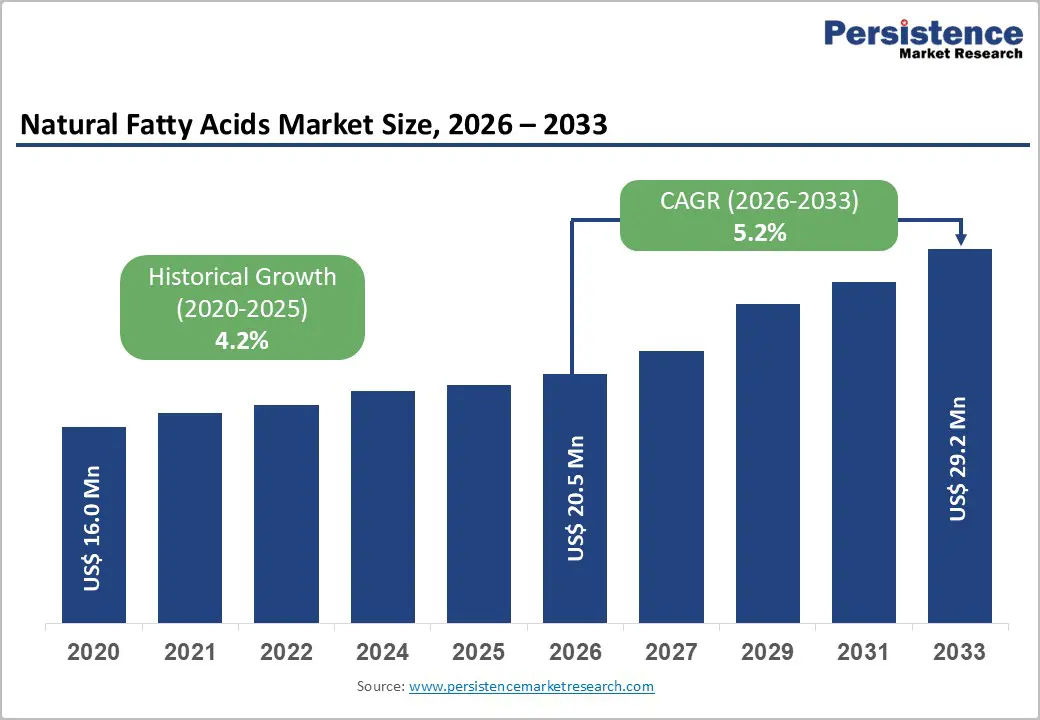

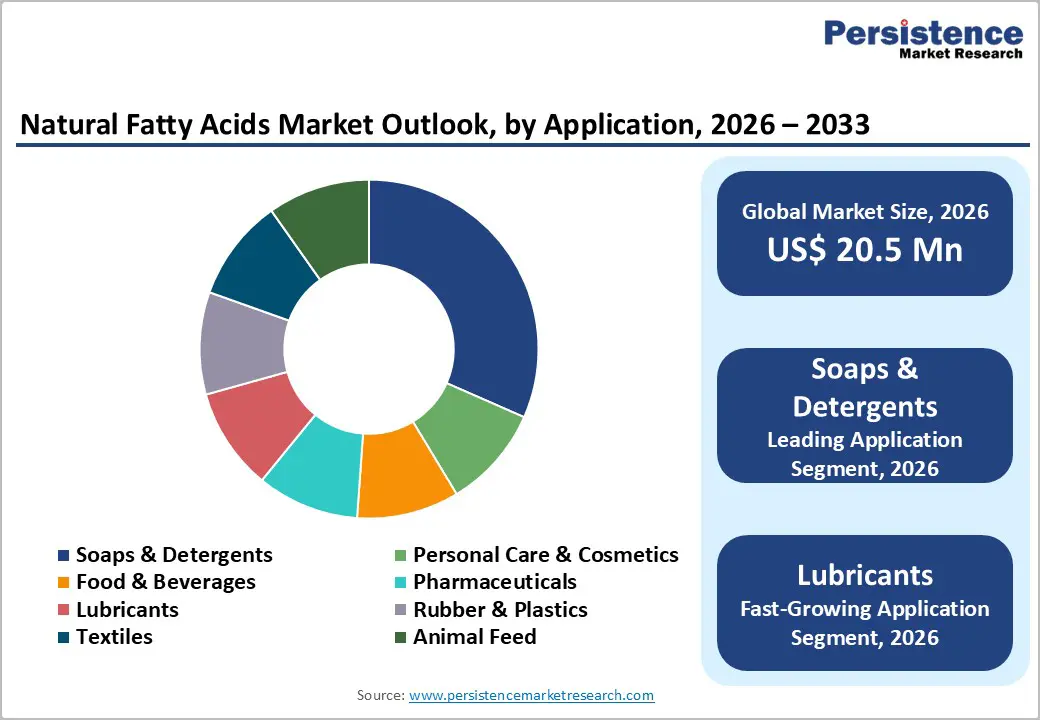

The global Natural Fatty Acids market size is expected to be valued at US$ 20.5 billion in 2026 and projected to reach US$ 29.2 billion by 2033, growing at a CAGR of 5.2% between 2026 and 2033. It is driven by accelerating demand from the oleochemicals industry, clean-label personal care reformulation trends, biobased lubricant adoption, and the global transition from petrochemical-derived surfactants to renewable, naturally-sourced fatty acid intermediates.

The market’s growth momentum is reinforced by the convergence of regulatory frameworks favoring bio-based chemicals, including the European Commission’s Chemicals Strategy for Sustainability (CSS) and the U.S. Biopreferred Program, alongside exponential growth in consumer demand for natural and sustainably sourced ingredients in soaps, cosmetics, pharmaceuticals, and food processing applications. Rapid industrialization and rising per-capita spending on personal care and hygiene products across Asia Pacific’s growing middle-income population, combined with robust palm and coconut oil production infrastructure in Indonesia and Malaysia, further consolidate the region’s position as the engine of global natural fatty acid supply and demand growth.

Key Industry Highlights:

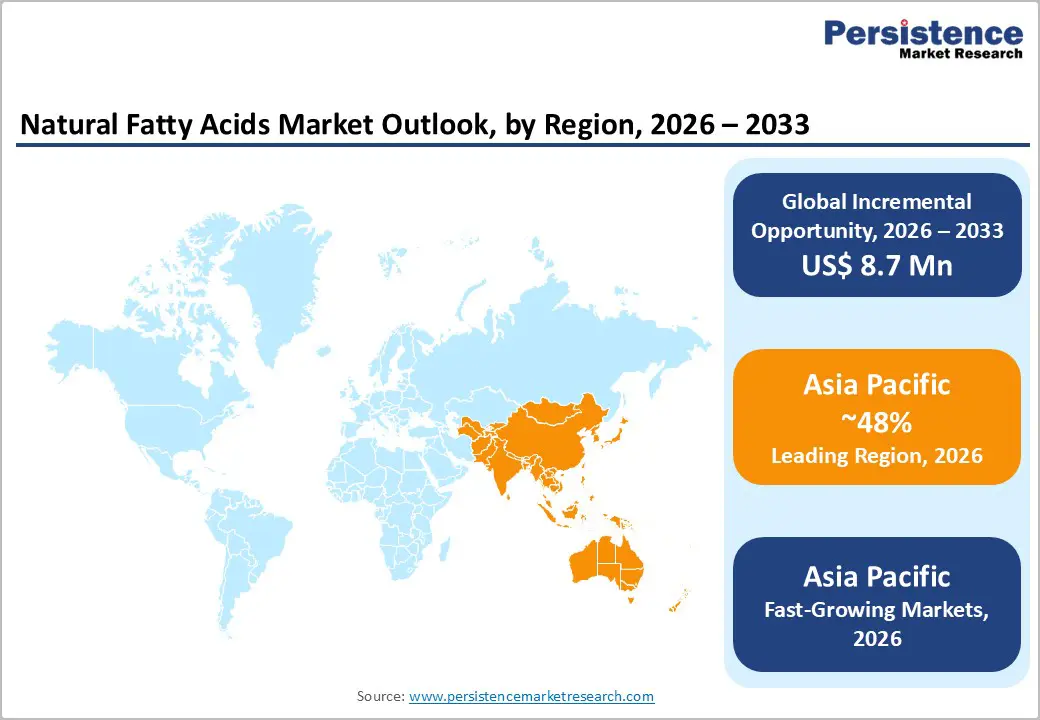

- Leading Region: Asia Pacific dominates the global Natural Fatty Acids market with approximately 48% revenue share in 2025, anchored by Malaysia and Indonesia’s world-scale palm oil-based oleochemical production infrastructure and China and India’s rapidly expanding soap, personal care, and food processing consumption sectors, driving both supply and demand leadership.

- Fastest Growing Region: Asia Pacific is also the fastest growing consumption region, projected to expand at approximately 6.5% CAGR through 2033, propelled by rising middle-class spending on personal care in China and India, expanding pharmaceutical manufacturing sectors, and robust downstream rubber, plastics, and animal feed industry growth across ASEAN economies.

- Dominant Product Segment: Vegetable oil-derived fatty acids dominate the source segment with approximately 72% market share in 2025, with palm oil’s extraordinary yield of approximately 3.8 tonnes per hectare per USDA FAS data making it the world’s most cost-efficient and highest-volume natural fatty acid feedstock across soaps, personal care, and industrial applications.

- Fastest Growing Product Segment: Bio-based lubricants represent the fastest growing application segment for natural fatty acids, driven by EU Ecolabel and USDA BioPreferred procurement mandates, ELGI-reported bio-lubricant market share gains in environmentally sensitive sectors, and strategic investments by Evonik Industries and Croda International in oleate ester-based high-performance lubricant platforms.

- Key Opportunity: The pharmaceutical and nutraceutical sector’s demand for high-purity natural fatty acids, including omega-3 fish oil concentrates endorsed by WHO cardiovascular guidelines and EFSA health claims, targeting a global dietary supplements market projected to exceed US$ 300 billion by 2030 per Nutrition Business Journal presents the highest-margin growth opportunity for specialty fatty acid producers.

| Key Insights | Details |

|---|---|

|

Natural Fatty Acids Market Size (2026E) |

US$ 20.5 Billion |

|

Market Value Forecast (2033F) |

US$ 29.2 Billion |

|

Projected Growth CAGR (2026–2033) |

5.2% |

|

Historical Market Growth (2020–2025) |

4.2% |

DRO Analysis

Drivers - Rising Global Demand for Bio-based Oleochemicals and Green Chemistry Initiatives

The global transition from petrochemical-derived intermediates to bio-based oleochemicals is a structural and policy-reinforced driver of natural fatty acid demand, as chemical manufacturers across surfactants, lubricants, and polymer additive sectors systematically seek to reduce their fossil fuel dependency. The European Commission’s Green Deal and Chemicals Strategy for Sustainability explicitly prioritize the substitution of hazardous petrochemical substances with bio-based alternatives, creating a regulatory mandate for oleochemical adoption across European chemical supply chains. The U.S. Department of Agriculture’s (USDA) BioPreferred Program, which lists over 14,000 certified bio-based products, provides federal procurement preference for natural fatty acid-derived products including bio-based lubricants, surfactants, and plasticizers, generating consistent government procurement demand. Evonik Industries and Croda International, both committed to expanding their bio-based specialty chemical portfolios, have explicitly cited natural fatty acid feedstock security as central to their long-term sustainability strategies, confirming the raw material’s strategic importance in next-generation green chemistry value chains.

Soaps, Detergents, and Personal Care Industry’s Shift to Natural Ingredients

The global soaps, detergents, and personal care industry represents the single largest end-use demand driver for natural fatty acids, underpinned by rapidly rising consumer preference for natural, biodegradable, and sustainably sourced formulations. The Cosmetics Europe industry association reports that natural and organic cosmetic product launches have grown at double-digit annual rates across European markets since 2019, with natural fatty acid derivatives, including lauric acid-derived sodium lauryl sulfate alternatives, stearic acid emulsifiers, and oleic acid conditioning agents, at the core of clean-beauty formulation architectures. The Personal Care Products Council (PCPC) in the United States similarly confirms growing formulator preference for fatty acid-based surfactants over synthetic ethoxylates. Global soap production, which relies on stearic and palmitic acid as primary feedstocks, is expanding in step with population growth and improving hygiene standards across Africa, South Asia, and Southeast Asia, where rising per-capita soap consumption is generating sustained incremental fatty acid volume demand.

Restraints - Sustainability and Deforestation Concerns Linked to Palm Oil Supply Chains

Palm oil, the dominant global feedstock for natural fatty acid production, faces intensifying reputational and regulatory scrutiny due to its historical association with tropical deforestation, biodiversity loss, and smallholder labor issues in Indonesia and Malaysia. The European Union Deforestation Regulation (EUDR), which took effect in 2023 and mandates due diligence verification that palm oil-derived products entering the EU market are deforestation-free, introduces substantial compliance complexity and cost for natural fatty acid producers reliant on palm-derived feedstocks. While certification frameworks including the Roundtable on Sustainable Palm Oil (RSPO) and ISCC (International Sustainability and Carbon Certification) provide pathways to deforestation-free supply chain compliance, the verification burden and premium cost of certified feedstocks constrain palm-derived fatty acid competitiveness in sustainability-sensitive European markets.

Vegetable Oil Price Volatility Driven by Climate and Geopolitical Disruptions

Natural fatty acid production costs are structurally exposed to the price volatility of vegetable oil feedstocks, particularly palm, soybean, and rapeseed oils, whose prices fluctuate significantly in response to weather events, crop disease outbreaks, energy price movements, and geopolitical disruptions. The Food and Agriculture Organization (FAO) Vegetable Oil Price Index recorded peak volatility in 2021–2022, with palm oil prices reaching record highs following COVID-19 logistics disruptions and Indonesia’s temporary palm oil export ban. Such feedstock price spikes compress fatty acid manufacturer margins and trigger downstream reformulation toward lower-cost synthetic alternatives in price-sensitive application segments, creating demand substitution risk that constrains market volume growth during periods of sustained feedstock price elevation.

Opportunities - Biobased Lubricants and Industrial Applications: An Expanding High-Value End-Market

The global transition toward bio-based lubricants and industrial fluids presents a high-growth, high-margin opportunity for natural fatty acid producers, as environmental regulations and corporate sustainability commitments drive systematic substitution of petroleum-derived mineral oils in industrial, automotive, and marine lubrication applications. The European Lubricants Industry Association (ELGI) reports that bio-lubricants, predominantly derived from oleic acid-rich vegetable oil esters and natural fatty acid-based synthetic esters, account for a growing share of the European industrial lubricants market, particularly in environmentally sensitive applications including forestry machinery, marine outboard engines, and food-grade machinery lubrication. The EU Ecolabel for lubricants and the USDA BioPreferred label for bio-based lubricants provide trusted specification frameworks that are increasingly referenced in public procurement tenders across municipal, defense, and infrastructure sectors. Leading specialty chemical producers, including Evonik Industries (via its ISOFOL® fatty alcohol platform) and Croda International’s lubricant additive division, have made strategic investments in oleochemical-derived ester lubricant platforms, indicating strong commercial conviction in the segment’s growth trajectory through the forecast period.

Pharmaceutical and Nutraceutical Sector Expansion Driving Demand for High-Purity Fatty Acids

The global pharmaceutical and nutraceutical industry represents a rapidly growing, premium-priced end-market for high-purity natural fatty acids, particularly omega-3 fatty acids from fish oil (EPA and DHA), medium-chain fatty acids (capric and caprylic acid from coconut oil), and pharmaceutical-grade stearic acid used as a tablet lubricant and excipient. The World Health Organization (WHO)’s updated guidelines on omega-3 fatty acid supplementation for cardiovascular disease prevention and the European Food Safety Authority (EFSA)’s scientific opinions validating omega-3 health claims have catalyzed global consumer demand for fish oil-derived fatty acid supplements. The global dietary supplements market is projected to exceed US$ 300 billion by 2030 per Nutrition Business Journal, with natural fatty acid-derived omega-3s representing one of the fastest-growing supplement categories. Corbion’s algae-derived DHA platform and BASF SE’s Pronova omega-3 pharmaceutical ingredient business exemplify the commercial opportunity at the premium end of the natural fatty acids market, commanding significant price premiums over commodity fatty acid grades.

Category-wise Analysis

Source Insights

Vegetable oils dominate the source segment of the natural fatty acids market, accounting for approximately 72% of total market revenue in 2025, with palm oil representing the single largest individual feedstock sub-segment. The global leadership of vegetable oil-derived fatty acids is fundamentally anchored by palm oil’s extraordinary productivity advantage, yielding approximately 3.8 tonnes of oil per hectare annually, compared to 0.7 tonnes/ha for soybean and 0.7 tonnes/ha for rapeseed per USDA Foreign Agricultural Service data, making it by far the most cost-efficient natural fatty acid feedstock globally. Malaysia and Indonesia collectively supply over 85% of global palm oil, with major oleochemical manufacturers including KLK OLEO, IOI Corporation, and Wilmar International operating integrated palm plantation-to-oleochemical complex value chains that deliver high cost and logistics advantages. Coconut oil, the primary feedstock for lauric acid and medium-chain fatty acids, represents the second-largest vegetable oil sub-segment, sourced predominantly from the Philippines, Indonesia, and India.

Product Type Insights

Saturated fatty acids lead the product type segment, representing approximately 58% of total market revenue in 2025, driven by the widespread industrial utility of palmitic acid, stearic acid, and lauric acid across soaps, personal care, food processing, and industrial application segments. Palmitic acid, the most abundant saturated fatty acid in palm oil at approximately 44% by weight, is a foundational ingredient in bar soap manufacturing, cosmetic emulsifiers, and food-grade emulsification systems, generating the highest absolute volume demand of any individual fatty acid globally.

Stearic acid’s dual utility as a soap feedstock and rubber processing aid, where it activates vulcanization in both natural and synthetic rubber compounds, makes it an indispensable industrial chemical with highly diversified and resilient demand across multiple end-use sectors. The American Oil Chemists’ Society (AOCS) provides globally recognized analytical standards for saturated fatty acid characterization, underpinning quality assurance across international fatty acid trade.

Form Insights

Liquid-form natural fatty acids lead the form segment with approximately 55% of total market revenue in 2025, reflecting the predominance of unsaturated fatty acids, particularly oleic acid and linoleic acid, which are liquid at ambient temperature, and the widespread industrial preference for liquid fatty acid handling in continuous manufacturing processes. Liquid fatty acids offer significant processing advantages in large-scale continuous saponification, esterification, and amidation reactions, as they can be metered, pumped, and mixed without the energy-intensive melting steps required for solid fatty acids.

The personal care and cosmetics industry, one of the fastest growing end-users of natural fatty acids, extensively utilizes liquid oleic acid as a skin-conditioning emollient and solubilizing agent in facial oils, serums, and hair care formulations, where its biocompatibility and penetration-enhancing properties are highly valued by formulators. Croda International’s SUPER REFINED™ oleic acid range exemplifies premium liquid fatty acid product positioning in pharmaceutical and cosmetic applications.

Application Analysis

Soaps and detergents represent the leading application segment for natural fatty acids, commanding approximately 32% of total market revenue in 2025, reflecting fatty acids’ foundational and irreplaceable role as the primary surfactant precursor in soap manufacturing through saponification of stearic and palmitic acid with alkali. Global soap production continues to grow in step with population expansion, urbanization, and improving hygiene standards, particularly across Sub-Saharan Africa, South Asia, and Southeast Asia, where per-capita soap consumption remains below global averages but is rising at above-average rates. The World Bank’s hand hygiene promotion programs, significantly accelerated by the COVID-19 pandemic, have provided sustained incremental demand stimulus for bar and liquid soap production in developing economies. Major global consumer goods companies, including Unilever, Procter & Gamble, and Henkel, collectively consume tens of thousands of tonnes of natural fatty acids annually for their soap and detergent product lines, making their procurement decisions a key demand barometer for the natural fatty acid supply chain.

Regional Insights

North America Natural Fatty Acids Market Trends and Insights

North America represents a mature and innovation-driven natural fatty acids market, holding approximately 18% of global revenue share in 2025, anchored by the United States’ well-developed oleochemical processing industry, world-class personal care and pharmaceutical manufacturing sectors, and robust regulatory support for bio-based chemical adoption. The USDA BioPreferred Program’s federal procurement mandate for bio-based products, covering natural fatty acid-derived lubricants, surfactants, and plasticizers, creates a sustained and institutionally guaranteed demand channel for oleochemical-derived products in government supply chains. Stepan Company’s Northfield, Illinois operations and Vantage Specialty Chemicals’ manufacturing network represent significant North American oleochemical processing capacity oriented toward personal care and industrial fatty acid derivative production.

Canada’s canola (rapeseed) oil industry, the world’s third-largest canola producer per Agriculture and Agri-Food Canada, provides a strategic domestic feedstock base for erucic acid and oleic acid production, supporting high-value applications in industrial lubricants, slip additives for plastics, and cosmetic emollients. The U.S. nutraceutical industry’s growing demand for omega-3 fatty acid concentrates, driven by the Council for Responsible Nutrition (CRN)’s data showing omega-3s as the most widely consumed dietary supplement category in the U.S., is generating above-average revenue growth in the fish oil-derived fatty acid sub-segment, with high-purity EPA/DHA concentrates commanding substantial pricing premiums over commodity fatty acid grades.

Europe Natural Fatty Acids Market Trends and Insights

Europe is a leading regional market for natural fatty acids with approximately 22% of global revenue share in 2025, driven by the continent’s advanced oleochemical processing industry, stringent sustainability regulations, and the world’s highest per-capita consumption of premium personal care, pharmaceutical, and bio-based specialty chemical products. Germany hosts major oleochemical production facilities operated by BASF SE, Evonik Industries, and Oleon NV (a Avril Group subsidiary), serving both domestic and pan-European demand for specialty fatty acid derivatives in cosmetics, pharmaceuticals, and industrial applications. The EU’s REACH regulation and the Chemicals Strategy for Sustainability are creating structural pressure for the substitution of petrochemical surfactants with natural fatty acid-derived alternatives in household and industrial cleaning product formulations, benefiting European oleochemical producers with established sustainable supply chain certifications.

The European Deforestation Regulation (EUDR) is reshaping European fatty acid supply chains, compelling manufacturers to diversify feedstocks beyond conventional palm oil toward RSPO-certified palm, ISCC-certified rapeseed, and alternative bio-based sources. France, the EU’s leading rapeseed oil producer, and Spain’s sunflower oil sector provide strategic European-origin feedstock alternatives to palm oil for fatty acid manufacturers seeking deforestation-free supply chain compliance. The European Oleochemicals and Allied Products Group (ERRMA), an industry body representing European oleochemical manufacturers, actively engages with EU regulators on sustainability standards and trade policy affecting fatty acid feedstock imports, playing a key role in shaping the region’s evolving regulatory landscape for bio-based chemical supply chains.

Asia Pacific Natural Fatty Acids Market Trends and Insights

Asia Pacific is both the dominant producing region and the fastest growing consumption market for natural fatty acids, commanding approximately 48% of global revenue share in 2025 and projected to expand at a CAGR of approximately 6.5% through 2033. The region’s market leadership is structurally anchored by Malaysia and Indonesia, collectively supplying over 85% of global palm oil, and their large-scale, vertically integrated oleochemical industries. KLK OLEO, IOI Corporation, Wilmar International, and Ecogreen Oleochemicals operate world-scale fatty acid fractionation and distillation facilities in Malaysia and Indonesia, supplying natural fatty acids to global markets at highly competitive price points. China’s rapidly expanding personal care, food processing, and rubber manufacturing sectors are the region’s fastest growing demand drivers, with domestic oleochemical production supplemented by significant fatty acid imports from Malaysian and Indonesian producers.

India’s natural fatty acids market is growing strongly, driven by the world’s largest soap manufacturing industry, with Hindustan Unilever, ITC, and Godrej Consumer Products among the world’s largest soap producers by volume, alongside expanding personal care, pharmaceutical, and animal feed sectors. Godrej Chemicals’ oleochemical complex in Mumbai is one of South Asia’s largest integrated fatty acid production facilities, serving both domestic FMCG giants and export markets. Japan’s highly specialized oleochemical industry, led by Kao Corporation and NOF Corporation, focuses on ultra-high-purity pharmaceutical and cosmetic-grade fatty acid derivatives, where Japan’s technical precision manufacturing culture creates globally recognized quality benchmarks. The ASEAN market is growing rapidly across personal care, food processing, and industrial sectors, with Vietnam, Thailand, and the Philippines emerging as increasingly significant fatty acid consumption markets.

Competitive Landscape

The global natural fatty acids market exhibits a moderately consolidated structure at the commodity production level, supported by large, vertically integrated producers with strong control over feedstock sourcing, processing, and refining operations. These players benefit from economies of scale and established supply chains, particularly in palm- and vegetable oil-based production. In contrast, the specialty and high-purity segment remains relatively fragmented, with a diverse set of manufacturers focusing on value-added and application-specific fatty acid solutions.

Competition is increasingly driven by sustainability and product differentiation strategies. Leading participants are emphasizing certified sustainable sourcing, diversification into non-palm feedstocks, and expansion of high-margin specialty derivatives for personal care, pharmaceuticals, and food applications. Additionally, companies are investing in digital traceability systems to ensure compliance with evolving environmental regulations and deforestation-free supply chains. Strategic collaborations with downstream industries, particularly FMCG and healthcare, are also gaining importance to co-develop customized solutions and strengthen long-term customer relationships.

Key Developments

- March 2025: Innovaoleo (Natac Group) launched Omega-3 Star, a high-quality fish oil designed for food, nutraceutical, and pet nutrition applications, offering high EPA and DHA content with enhanced purity, stability, and neutral sensory characteristics.

- February 2025: Everwell Health acquired proprietary cetylated fatty acid technology and the Celadrin brand to expand its portfolio of science-backed functional ingredients for human, pet, and cosmetic applications, supporting innovation in joint health and skin care solutions.

Companies Covered in Natural Fatty Acids Market

- KLK OLEO

- Wilmar International

- IOI Corporation

- Emery Oleochemicals

- Oleon NV (Avril Group)

- Ecogreen Oleochemicals

- Godrej Chemicals

- Croda International

- Kao Corporation

- Vantage Specialty Chemicals

- Evonik Industries

- Stepan Company

- Pacific Oleochemicals

- VVF LLC

- Corbion

- BASF SE

- Cargill Incorporated

- Berg + Schmidt GmbH & Co. KG

Frequently Asked Questions

The natural fatty acid market is likely to be valued at US$ 20.5 billion in 2026.

Growth is driven by the shift toward bio-based chemicals and rising demand for sustainable ingredients.

Asia Pacific leads the market with the highest revenue share.

Opportunities lie in bio-based lubricants and high-purity applications in pharma and nutraceuticals.

Leading companies in the global Natural Fatty Acids market include Wilmar International, KLK OLEO, IOI Corporation, Emery Oleochemicals, Oleon NV, Croda International, Evonik Industries, Kao Corporation, BASF SE, Stepan Company, Godrej Chemicals, etc.