- Food Ingredients & Additives

- Natural Food Additives Market

Natural Food Additives Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Natural Food Additives Market by Form Analysis (Dry, Liquid), Functionality Type (Flavor, Enhancer, Other), Consumer Use (Conventional Products, Others), Application (Bakery & Confectionery, Others), and Regional Analysis 2026 - 2033

Natural Food Additives Market Share and Trends Analysis

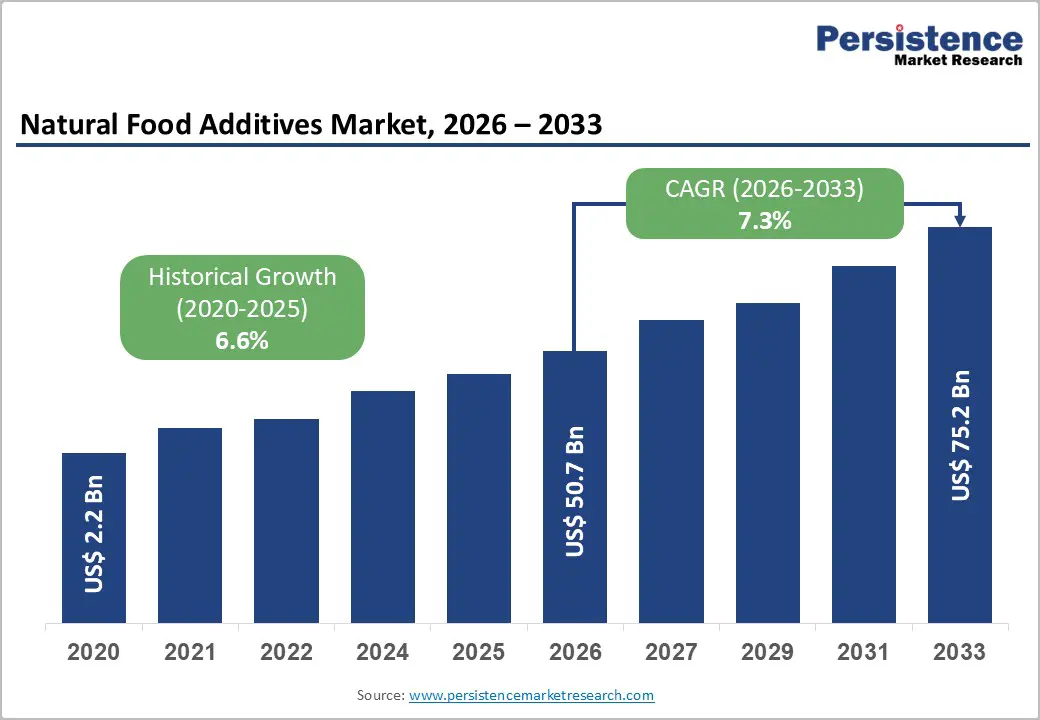

The global natural food additives market size is projected to be valued at US$50.7 billion in 2026 and is expected to reach US$75.2 billion by 2033, growing at a CAGR of 7.3% during the forecast period between 2026 and 2033, driven by a fundamental shift in global consumer behavior toward clean-label products and heightened transparency in ingredient sourcing.

Heightened awareness of the health implications of artificial preservatives and colorants has accelerated the development of plant-based and naturally derived additives across the food and beverage sector. Technological advancements in extraction and micro-encapsulation are further bridging the performance gap between natural and synthetic additives, ensuring stability across diverse food matrices.

Key Industry Highlights:

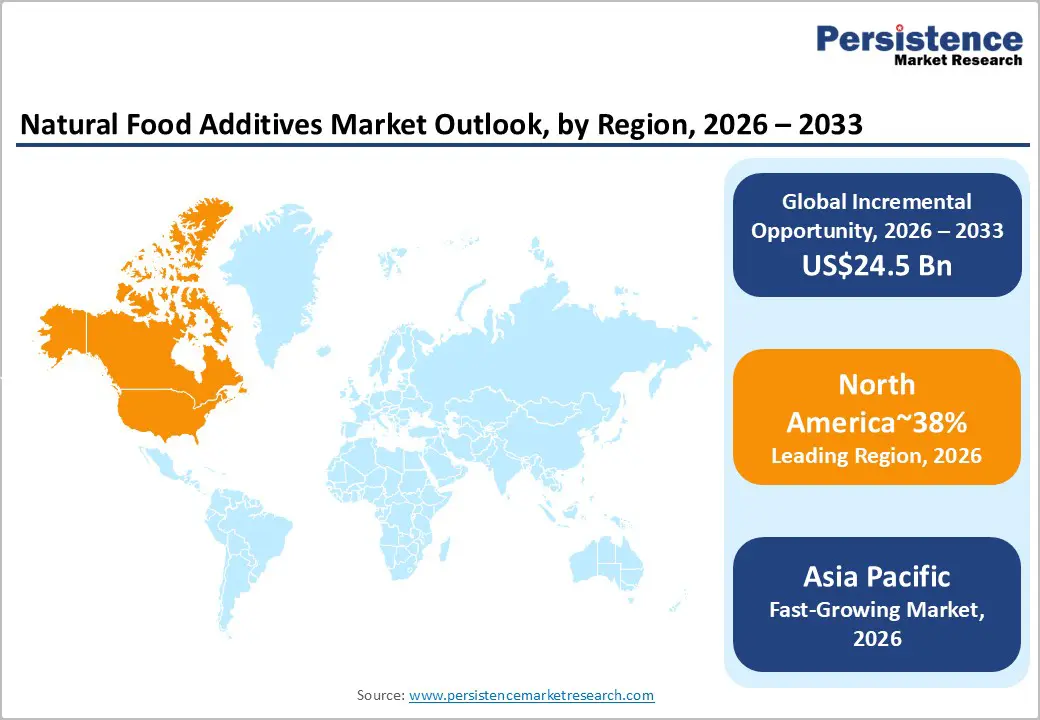

- Leading Region: North America is expected to lead the natural food additives market with an estimated 38% share in 2026, supported by mature processed food sectors, high consumer awareness, and advanced manufacturing infrastructure.

- Fastest-growing Region: Asia Pacific is projected to be the fastest-growing region, driven by rapid urbanization, expanding middle-class consumption, and rising packaged food volumes in China, India, and Southeast Asia.

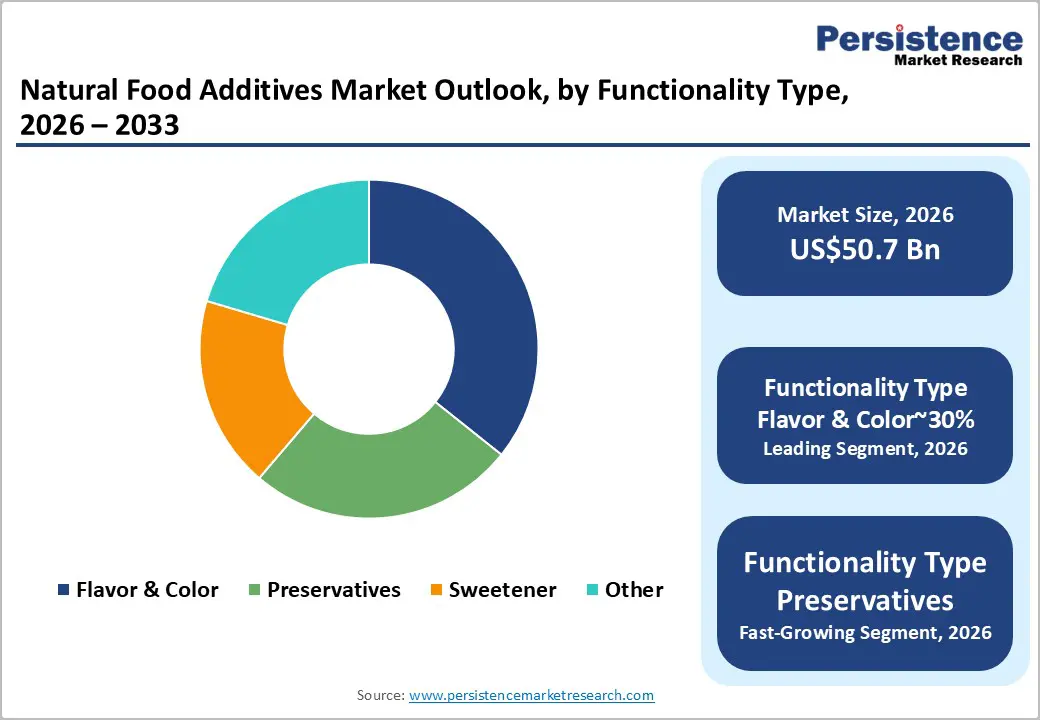

- Leading Functionality Type Segment: Natural flavors and colors are expected to lead with approximately 30% share in 2026, anchored by fruit-derived flavors, carotenoids, and anthocyanins that deliver sensory appeal and regulatory-compliant clean-label solutions.

- Leading Consumer Use Segment: Conventional products are projected to dominate with 31% share in 2026, supported by entrenched consumption, brand familiarity, and high-volume daily use across snacks, bakery, and staple foods.

- Key Industry Developments: In May 2024, DSM-Firmenich & Indena debuted pioneering botanical and biotic combination concepts for the functional food market. By integrating standardized botanical extracts with probiotics, this partnership enables food manufacturers to claim "functional health benefits" without using synthetic fortification agents.

| Key Insights | Details |

|---|---|

| Natural Food Additives Market Size (2026E) | US$50.7 Bn |

| Market Value Forecast (2033F) | US$75.2 Bn |

| Projected Growth (CAGR 2026 to 2033) | 7.3% |

| Historical Market Growth (CAGR 2020 to 2025) | 6.6% |

Market Dynamics - Growth, Barrier, and Opportunity Analysis

Technological Advancements in Extraction

Technological advancement in extraction and biosynthesis is structurally reshaping the performance economics of natural additives. Techniques such as supercritical CO2 extraction and precision fermentation are narrowing historical gaps in color stability, flavor intensity, and shelf life relative to synthetic incumbents.

These technologies directly improve cost-in-use metrics by enhancing yield efficiency, reducing solvent dependence, and improving batch-to-batch consistency. As a result, natural colors and flavors are increasingly meeting the functional thresholds required for large-scale food and beverage applications, reinforcing regulatory-driven substitution dynamics rather than discretionary adoption.

In parallel, biotech-enabled production platforms are addressing long-standing scalability and supply reliability constraints. Fermentation-derived preservatives and non-animal chitosan are achieving industrial volumes with controlled quality parameters, thereby mitigating risks associated with agricultural volatility and seasonality.

This shift is recalibrating value-chain economics, favoring suppliers with fermentation infrastructure, IP depth, and compliance-ready processes. While capital intensity and process validation timelines remain structural headwinds, the convergence of extraction efficiency and bio-manufacturing is positioning natural additives for sustained penetration across regulated end markets.

Stability & Sensory Challenges

Stability and sensory performance limitations remain significant constraints on substituting synthetic additives with natural alternatives. Natural colorants are highly sensitive to thermal exposure, light intensity, and pH variability, increasing the risk of fading, browning, or hue drift over the product's shelf life.

These degradation dynamics complicate the consistency of formulations in processed foods and beverages, where thermal processing and extended storage are unavoidable. As a result, manufacturers face narrower formulation tolerances and a greater risk of rejection, particularly in mass-market applications with stringent visual standards.

In parallel, natural preservation systems introduce pronounced sensory challenges that directly affect consumer acceptance. Fermentation-derived acids, botanical extracts, and bio-preservatives often impart herbal, bitter, or acidic off-notes that disrupt delicate matrices such as dairy, ready-to-drink beverages, and confectionery.

Addressing these effects requires multi-layered reformulation, including flavor masking, encapsulation, and system-level optimization. This elevates R&D intensity, lengthens validation cycles, and raises development costs, reinforcing structural entry barriers despite favorable regulatory and demand-side momentum.

Functional Ingredients Convergence

Functional convergence between natural and performance-enhancing ingredients is reshaping additive value propositions across food and beverage formulations. Natural additives are increasingly evaluated not only for replacement efficacy but for their ability to deliver ancillary health-linked benefits.

This shift is driven by clean-label regulation, rising consumer literacy, and the growing overlap between nutrition, wellness, and formulation science. Ingredients such as acerola-derived preservatives or turmeric- and spirulina-based color systems illustrate how antioxidant or anti-inflammatory attributes are being embedded into core functional roles.

The functionality plus dynamic is structurally altering pricing power and portfolio strategies. Multifunctional additives support premium positioning by reducing ingredient counts while enhancing label claims, reinforcing margin resilience despite higher input costs.

However, commercialization is uneven, as regulatory substantiation, bioavailability validation, and claim compliance vary by jurisdiction. Suppliers with application expertise and clinical alignment are therefore better positioned to capture value, while others face dilution risks as functional expectations become standardized rather than differentiated.

Category-wise Analysis

Functionality Type Insights

Natural flavors and colors are expected to lead the natural additives market, accounting for an estimated 30% share in 2026, as they form the foundation of product appeal across beverages, dairy, and confectionery applications. Their dominance is reinforced by versatility and sensory impact: fruit-derived flavors dominate the flavor category, while carotenoids and anthocyanins remain preferred for color enhancement.

Key industrial players such as Givaudan, Sensient Technologies, and Oterra are leveraging biotransformation and precision fermentation technologies to deliver stable, authentic, and regulatory-compliant solutions. For instance, Sensient’s BioSymphony platform enables natural flavor production aligned with clean-label standards, while GNT Group’s EXBERRY pigments provide consistent plant-based coloring year-round.

The structural reliance of mainstream and premium products on vibrant natural flavors and colors, combined with growing consumer demand for clean-label and vegan formulations, is likely to sustain this segment’s leading status.

Natural Preservatives are anticipated to be the fastest-growing segment, driven by the urgent industrial need for shelf-life extension in clean-label formats. Antioxidants such as rosemary extract and antimicrobial agents lead adoption, with companies such as Cargill and Kerry Group developing liquid and solid preservation solutions for dairy, beverages, and plant-based products.

Startups, including Chinova Bioworks, are innovating through waste valorization, converting mushroom stalks into natural antimicrobials. Rising regulatory pressures from the FDA, EFSA, and India’s FSSAI, combined with growing health consciousness and the expansion of plant-based foods, are expected to accelerate the transition from synthetic to natural preservatives across global markets.

Consumer Use Insights

Conventional products are expected to lead the consumer food market, holding approximately 31% share in 2026, supported by entrenched purchasing habits and high-volume daily consumption across snacks, bakery items, and staple groceries. Their dominance is reinforced by established distribution networks, trusted formulations, and brand familiarity, which together sustain repeat purchases and maintain margin stability.

Companies such as Cargill, ADM, and Kerry Group are leveraging both legacy product portfolios and strategic acquisitions to maintain leadership; for example, Cargill’s Palsgaard acquisition strengthens conventional emulsifier capabilities, while Kerry Group facilitates gradual reformulation toward cleaner labels without disrupting taste.

The combination of consistent sensory performance, regulatory compliance, and widespread availability is most likely to preserve this segment’s structural advantage, ensuring continued revenue stability across mass-market applications.

The health and wellness segment is anticipated to be the fastest-growing category, driven by rising consumer demand for organic, non-GMO, and functionally positioned foods. Growth is reinforced by trends in trust and transparency, with non-GMO and certified organic claims serving as key loyalty drivers.

Functional ingredient adoption, such as inulin for gut health and algal-derived Omega-3s in beverages, yogurt, and cereals, is expected to accelerate penetration, while plant-based alternatives leverage natural emulsifiers, colors, and flavors to replicate conventional sensory profiles. Regulatory frameworks such as USDA Organic and EU Bio certification, combined with innovations in targeted fortification and “free-from” positioning, are likely to expand market uptake.

Companies including ADM, Cargill, and Kerry Group are positioned to capture this expansion by aligning product portfolios with evolving wellness priorities, making this segment a strategic driver of future category growth. The resulting segmentation reflects a bifurcated market, where conventional products anchor volume, health-driven offerings capture incremental growth, and premium lines occupy a selective, brand-led niche within the broader consumption landscape.

Regional Insights

North America Natural Food Additives Market Trends

North America is projected to remain the leading market, accounting for 38% of global share in 2026, supported by a mature processed food sector and a highly informed consumer base that prioritizes clean-label products. Leadership is reinforced by high disposable incomes, advanced manufacturing infrastructure, and a robust innovation ecosystem that accelerates the adoption of natural additives across beverages, bakery, and dairy applications. Regulatory clarity from the FDA regarding “GRAS” status for natural ingredients facilitates faster product approvals, enabling manufacturers to scale plant-based and functional solutions efficiently while maintaining compliance and consumer trust.

The region’s market strength is further underpinned by sustained investment in R&D and technological capabilities that enhance ingredient performance, stability, and sensory properties. Consumer-driven demand for transparency and functional benefits drives adoption across mainstream and niche segments, solidifying North America’s position as the benchmark for natural additive integration. Combined structural, regulatory, and economic advantages ensure the region sustains leadership while supporting predictable growth trajectories across high-volume and premium applications.

Europe Natural Food Additives Market Trends

Europe is projected to remain a mature and steady market, underpinned by a highly regulated environment and a structurally advanced natural additives sector. Leadership is supported by strong consumer adoption of organic and “free-from” products, particularly in Germany, France, and the U.K., where demand for clean-label solutions consistently drives formulation adjustments.

Regulatory oversight, including EFSA mandates and the Titanium Dioxide E171 ban, reinforces compliance-driven adoption while compelling multinational manufacturers to implement natural formulations that often extend beyond the region’s borders.

Harmonization of regulations across the EU member states further stabilizes market operations by facilitating cross-border trade and reducing compliance complexity for natural ingredients. Combined with established production infrastructure and high-quality supply chains, these factors sustain steady growth despite stringent oversight.

Consumer preference for transparent labeling, coupled with structural incentives for organic and functional products, positions Europe as a benchmark for regulatory alignment and premium adoption within the global natural additives landscape.

Asia Pacific Natural Food Additives Market Trends

Asia-Pacific is projected to be the fastest-growing regional market, driven by rapid urbanization, rising disposable incomes, and the expansion of packaged and processed food consumption in key markets such as China and India. Unlike Western markets, where growth is primarily replacement-driven, APAC’s adoption of natural additives is volume-led, reflecting broader food market expansion and increasing demand for processed and convenience products.

Structural advantages, including abundant local availability of spices, herbs, and botanicals, provide cost efficiencies that support scalable production and competitive pricing for domestic manufacturers.

The region’s growth trajectory is further reinforced by a growing middle class and shifting dietary preferences toward Westernized, ready-to-eat, and fortified foods. Investment in local manufacturing infrastructure and improvements in supply chain logistics enhance accessibility of natural additives across urban and semi-urban markets.

Combined demand-side expansion and input-cost advantages position Asia Pacific to capture a disproportionate share of incremental market volume while gradually maturing in quality and regulatory compliance relative to established Western markets.

Competitive Landscape

The global natural food additives market is moderately consolidated, with the top five players, Givaudan, IFF, Kerry Group, ADM, and Symrise, controlling approximately 45-50% of the total market revenue, primarily within high-value flavor and functionality segments.

Competitive advantage is driven by extensive R&D capabilities, global distribution networks, and the ability to deliver consistent quality and formulation support, enabling sustained market influence and margin stability. High entry barriers in product development and regulatory compliance reinforce the dominance of leading multinationals, while scale and technical expertise remain critical for maintaining strategic positioning.

The broader market remains fragmented at the regional and niche level, where suppliers focus on botanical extracts, natural colors, specialized and localized flavor profiles, offering differentiated functional or sensory solutions. These smaller players capture incremental value in application-specific segments, contributing to diversity in competitive dynamics. Forward-looking trends indicate continued consolidation in premium additive segments, innovation-led differentiation, and expanding adoption of natural, clean-label ingredients across food and beverage categories globally.

Key Industry Developments

- In May 2025, Givaudan secured U.S. FDA approval for Everzure™ Galdieria, a phycocyanin-rich natural blue additive. As the first acid-stable natural blue derived from microalgae, this approval allows for the total replacement of synthetic Blue 1 in acidic beverages, a previously unattainable technical milestone.

- In January 2025, ADM published the 2025 global consumer trend report, highlighting "Age Hacking" via natural additives. This intelligence shift directs market investment toward "longevity-focused" additives such as natural polyphenols and antioxidants, which are seeing a 12% YoY increase in consumer pull.

- In November 2024, Kerry Group released the "2025 Health and Nutrition Report," which prioritizes natural sodium-reduction technologies. The report outlined the 2025 R&D roadmap for natural flavor modulators that enable a 30% reduction in salt without the metallic aftertaste of traditional synthetic substitutes.

Companies Covered in Natural Food Additives Market

- Givaudan

- International Flower and Fragrance (IFF)

- Symrise AG

- Kerry Group

- DSM-Firmenich

- Archer Daniels Midland Company ADM

- Sensient Technologies

- Corbion

- Ingredion

- Tate & Lyle PLC

- Cargill

- Chr. Hansen

- BASF SE

- Ajinomoto Co, INC.

- Takasago

Frequently Asked Questions

The global natural food additives market is projected to be valued at US$50.7 billion in 2026 and is expected to reach US$75.2 billion by 2033, reflecting strong clean-label driven demand.

The shift is accelerating due to growing consumer preference for clean-label foods, regulatory pressure to phase out synthetic additives, and rising awareness of health risks associated with artificial preservatives and colorants.

The natural food additives market is expected to grow at a CAGR of 7.3% between 2026 and 2033, supported by advances in extraction, encapsulation, and precision fermentation technologies.

Asia Pacific is the fastest-growing regional market, propelled by rapid urbanization, expanding middle-class consumption, rising volumes of packaged food, and abundant local availability of spices and botanicals in China and India.

Key players include Givaudan, IFF, Symrise AG, Kerry Group, DSM-Firmenich, Archer Daniels Midland, Sensient Technologies, Corbion, Ingredion, Tate & Lyle PLC, Cargill, Chr. Hansen, BASF SE, Ajinomoto Co., and Takasago.