- Specialty & Fine Chemicals

- Natural Zeolite Market

Natural Zeolite Market Size, Share, and Growth Forecast, 2026 - 2033

Natural Zeolite Market by Product Type (Clinoptilolite, Chabazite, Mordenite, Others), Application (Agriculture & Soil Amendments, Animal Feed Additives, Water Treatment & Filtration, Construction & Building Materials, Others), End-Use (Industrial, Municipal, Commercial, Residential), and Regional Analysis for 2026 - 2033

Natural Zeolite Market Share and Trends Analysis

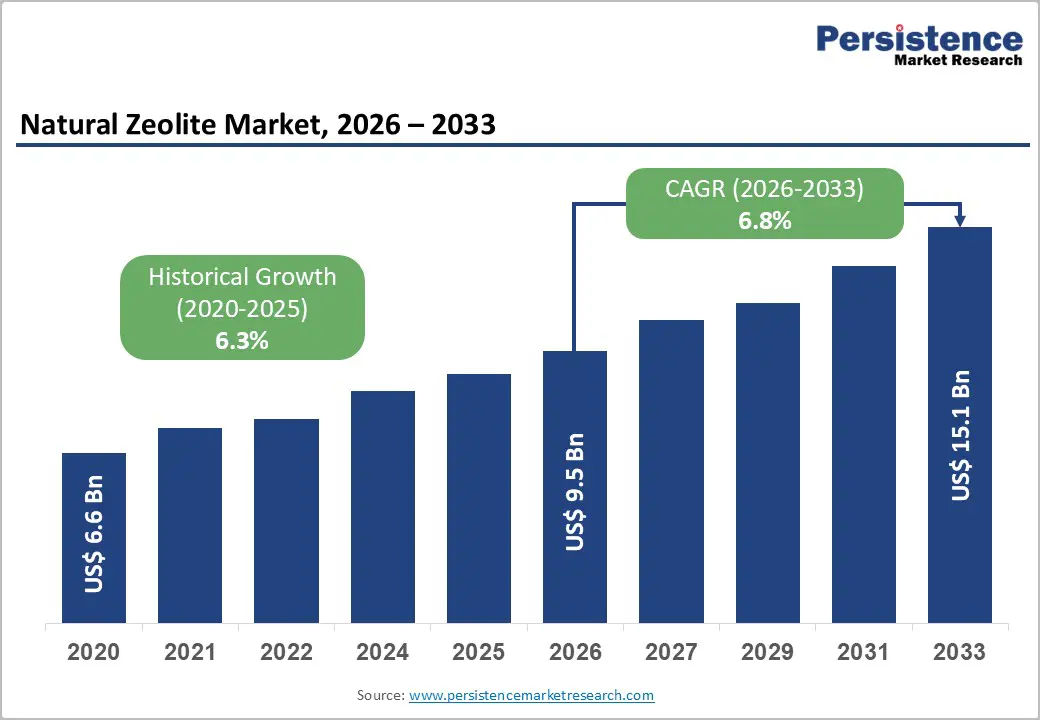

The global natural zeolite market size is likely to be valued at US$ 9.5 billion in 2026, and is projected to reach US$ 15.1 billion by 2033, growing at a CAGR of 6.8% during the forecast period 2026 - 2033.

Sustained demand across environmental remediation, sustainable agriculture, municipal water treatment, and industrial filtration underpins market expansion. Rising regulatory emphasis on water quality compliance, soil health restoration, and emission control positions natural zeolite as a cost-effective and environmentally compatible material. Governments and municipalities increasingly adopt mineral-based filtration solutions aligned with circular economy frameworks and low-carbon infrastructure development.

Agricultural producers are increasingly relying on zeolite for nutrient retention, ammonia control, and yield stability, driven by fertilizer cost inflation and soil degradation risks. Industrial end users are expanding use in petrochemical separation, odor control, and waste gas adsorption, supported by stricter environmental discharge norms.

Key Industry Highlights

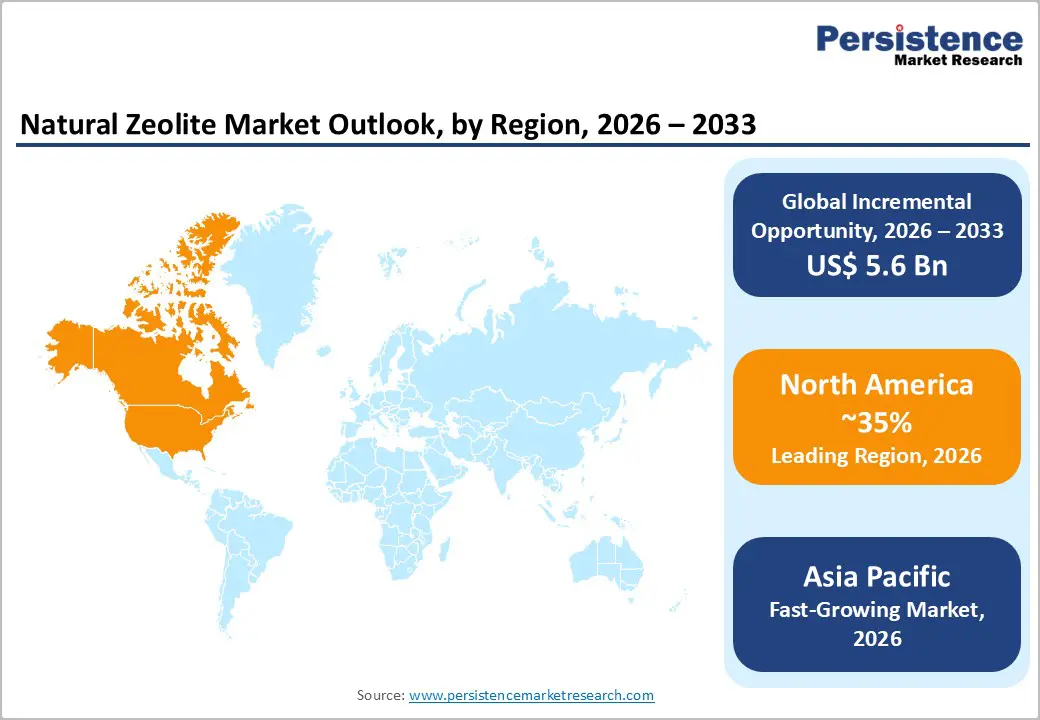

- Dominant Region: By 2026, North America is expected to hold about 35% market share, driven by well-established mining infrastructure and high domestic production capacity.

- Fastest-growing Market: Asia Pacific is projected to be the fastest-growing market during 2026 - 2033, supported by rapid urbanization and modern retail expansion.

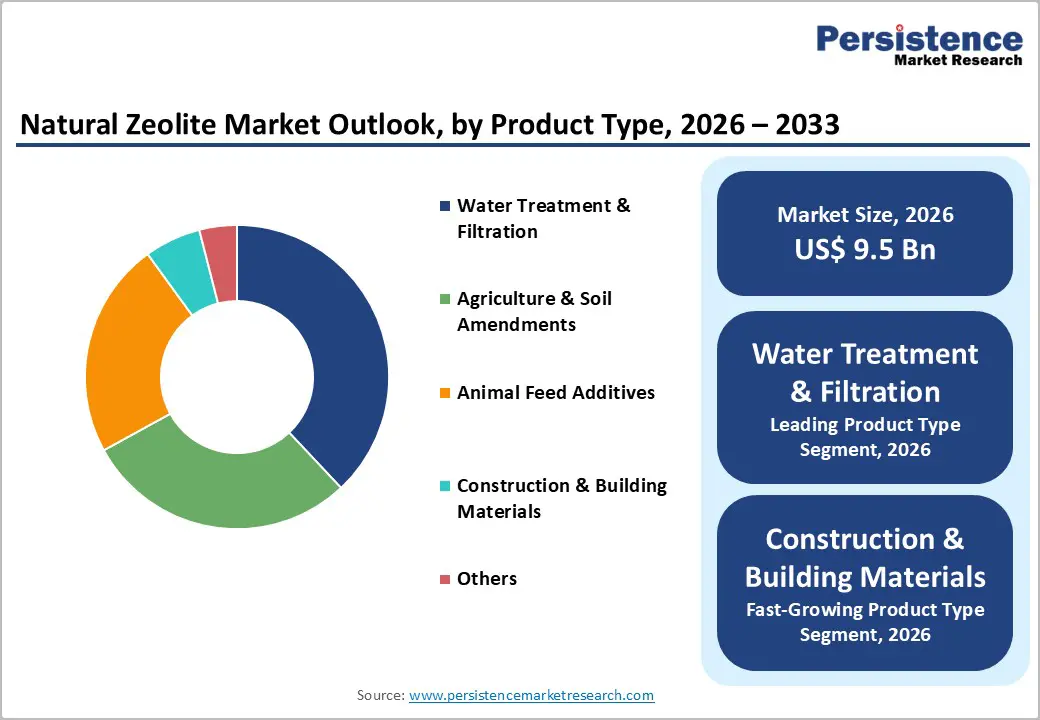

- Leading Application: Water treatment and filtration are anticipated to lead with over 38% revenue share in 2026, owing to strong regulatory enforcement and widespread adoption for contaminant removal solutions.

- Fastest-growing Application: Construction & building materials are forecasted to be the fastest-growing segment from 2026 to 2033, propelled by government incentives for low-carbon infrastructure.

- April 2025: Chalmers University and Umicore researchers developed an AI-powered machine learning force field for copper-chabazite zeolites, revealing ammonia-copper complex diffusion mechanisms to enhance low-temperature NOx reduction catalysts.

| Key Insights | Details |

|---|---|

| Natural Zeolite Market Size (2026E) | US$ 9.5 Bn |

| Market Value Forecast (2033F) | US$ 15.1 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.8% |

| Historical Market Growth (CAGR 2020 to 2025) | 6.3% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Expansion of Water Treatment and Environmental Remediation Infrastructure

Enhancements across water treatment and environmental remediation infrastructure stand as a primary factor fueling the natural zeolite market growth due to rising pressure on governments and industries to deliver measurable improvements in water quality and environmental compliance. Urbanization, industrial discharge, and tighter regulatory thresholds are forcing operators to adopt materials that combine performance reliability with operational efficiency.

Natural zeolites align with these priorities through their strong ion-exchange capacity, selective adsorption of contaminants, and compatibility with modern treatment systems. These characteristics support removal of ammonium, heavy metals, and nutrients in municipal and industrial facilities where treatment consistency and cost control remain strategic priorities. Environmental remediation infrastructure further reinforces demand by addressing legacy pollution in soil and groundwater from mining, petrochemicals, and manufacturing activities.

Remediation projects prioritize materials that immobilize or extract contaminants without introducing secondary environmental risks. Natural zeolites meet these requirements through physical and chemical stability, predictable performance across variable site conditions, and alignment with sustainability objectives set by regulators and funding agencies. Public investment programs and private environmental liability initiatives are expanding remediation project pipelines, increasing the use of adsorption-based technologies within engineered cleanup systems.

Variability in Mineral Quality and Deposit Characteristics

Variability in mineral quality and deposit characteristics acts as a structural restraint due to the inherent geological diversity of naturally occurring formations. Deposits differ widely in purity, crystal structure, cation exchange capacity, adsorption efficiency, and contaminant presence. These differences translate into inconsistent performance outcomes across end-use applications such as water treatment, agriculture, animal nutrition, and industrial filtration.

Buyers operating under strict technical specifications face difficulty in securing uniform material quality at scale, which weakens confidence in long-term supply agreements. Quality inconsistency also raises qualification timelines, testing costs, and rejection rates, placing pressure on operating margins and procurement efficiency.

Deposit-specific characteristics further constrain commercial scalability and cost competitiveness. Variations in depth, hardness, moisture content, and proximity to infrastructure influence extraction complexity and processing yield. Some deposits require extensive beneficiation to meet application-grade standards, increasing capital expenditure and energy consumption. Transportation economics remain sensitive to deposit location, especially for low-value bulk uses, limiting addressable demand radius. Regulatory compliance adds another layer of complexity when trace elements exceed permissible thresholds for environmental or feed-related uses.

Promising Developments in Sustainable Construction Materials

Progress in the formulation of sustainable construction materials over the past few years has been encouraging, and for the natural zeolite market, this presents a pivotal opportunity due to the growing alignment between performance efficiency and environmental accountability in the built environment. Green building standards increasingly prioritize materials that deliver durability, energy efficiency, and lower lifecycle emissions.

This material offers inherent advantages such as high porosity, thermal insulation support, moisture regulation, and ion-exchange capability, which directly enhance concrete performance, indoor air quality, and structural longevity. Construction stakeholders seek solutions that reduce cement dependency, optimize resource utilization, and support circular economy objectives.

The construction sector is undergoing a structural shift toward materials that balance technical reliability with environmental stewardship. Urbanization, infrastructure modernization, and green housing programs are accelerating demand for inputs that enhance strength, fire resistance, and chemical stability without increasing environmental risk. This material supports these requirements by improving compressive strength, reducing shrinkage, and enhancing resistance to chemical degradation in concrete applications. Developers and contractors value materials that improve long-term asset performance while supporting sustainability disclosures and environmental, social, and governance benchmarks.

Category-wise Analysis

Product Type Insights

Clinoptilolite is projected to capture approximately 64% of the natural zeolite market revenue share by 2026. This leadership position has stemmed from superior cation exchange capacity (CEC), exceptional thermal stability, and broad regulatory acceptance across multiple jurisdictions. The mineral has found extensive application in water treatment, agriculture, and animal nutrition, where proven performance data and reliable availability have reinforced adoption patterns. Operators have prioritized clinoptilolite because it aligns with potable water standards and livestock feed regulations, which has strengthened its penetration in highly regulated markets and created barriers for alternative materials.

For example, the Site Ion Exchange Effluent Plant (SIXEP) at Sellafield, England, has been using clinoptilolite to remove over 99.9% of radioactive cesium and strontium from nuclear wastewater since 1985, processing over 30 million cubic meters while keeping discharges safe.

Chabazite is emerging as the fastest-growing product type through the 2026-2033 period, driven by accelerating demand in industrial gas separation, carbon capture, and specialized catalysis applications. Its higher selectivity for specific ions and gases has enhanced suitability for advanced industrial processes where precision matters. Investment in industrial decarbonization initiatives has supported adoption, particularly across developed economies that have been pursuing ambitious emission reduction targets. As carbon pricing mechanisms mature and process efficiency becomes more critical, chabazite's unique properties will have positioned it as a strategic material for companies seeking to optimize separation processes while meeting sustainability commitments.

Application Insights

Water treatment and filtration applications are projected to secure over 38% of the natural zeolite market share by 2026, driven by regulatory enforcement, infrastructure upgrades, and efforts to mitigate contamination risks. Municipal utilities have been using zeolite for the removal of ammonia, heavy metals, and radionuclides, while industrial facilities have been integrating zeolite to meet discharge compliance standards and minimize chemical usage in wastewater management. This segment's resilience has stemmed from the essential role of zeolite in safeguarding water quality and supporting public health, with operators increasingly prioritizing solutions that combine regulatory alignment with operational efficiency.

Construction and building materials are anticipated to have emerged as the fastest-growing segment between 2026 and 2033, as the industry shifts toward eco-friendly and sustainable infrastructure solutions. Zeolite-enhanced cement and lightweight aggregates have been delivering improved durability, thermal insulation, and lower carbon footprints, positioning them as key enablers of green building initiatives. Rapid urbanization, especially in the Asia Pacific and Latin America regions, combined with government incentives for low-carbon construction materials, has created substantial growth opportunities for zeolite suppliers. As sustainability targets become more stringent, stakeholders in the construction sector are expected to have deepened their reliance on advanced zeolite-based products to balance performance, compliance, and environmental responsibility.

End-Use Insights

Water treatment and filtration end uses are projected to hold over 38% of the zeolite market share by 2026, driven by regulatory enforcement, infrastructure upgrades, and efforts to mitigate contamination risks. Municipal utilities have been using zeolite for the removal of ammonia, heavy metals, and radionuclides, while industrial facilities have been integrating zeolite to meet discharge compliance standards and minimize chemical usage in wastewater management. This segment's resilience has stemmed from the essential role of zeolite in safeguarding water quality and supporting public health, with operators increasingly prioritizing solutions that combine regulatory alignment with operational efficiency.

Construction and building materials are anticipated to have emerged as the fastest-growing segment between 2026 and 2033, as the industry shifts toward eco-friendly and sustainable infrastructure solutions. Zeolite-enhanced cement and lightweight aggregates have been delivering improved durability, thermal insulation, and lower carbon footprints, positioning them as key enablers of green building initiatives. Rapid urbanization, especially in Asia Pacific and Latin America, combined with government incentives for low-carbon construction materials, has created substantial growth opportunities for zeolite suppliers. As sustainability targets become more stringent, stakeholders in the construction sector are expected to have deepened their reliance on advanced zeolite-based products to balance performance, compliance, and environmental responsibility.

Regional Insights

North America Natural Zeolite Market Trends

By 2026, North America is expected to hold a 35% share of the natural zeolite market share, supported by well-established mining infrastructure and high domestic production capacity. The United States and Canada contribute significantly through rich clinoptilolite reserves and advanced processing facilities, ensuring consistent supply for diverse industrial and municipal applications. Strong regulatory frameworks for environmental protection and water treatment create sustained demand, as natural zeolite is widely adopted for soil conditioning, wastewater management, and air filtration. Industrial sectors such as chemical manufacturing, agriculture, and construction increasingly utilize zeolite for performance enhancement and sustainability compliance.

North America benefits from high-value, diversified end-use adoption. In agriculture, zeolite enhances soil moisture retention and nutrient management, supporting precision farming practices and optimizing crop yields in high-cost operational environments. Industrially, its ion-exchange and adsorption properties make it indispensable for wastewater treatment and emissions control, creating long-term contracts with municipalities and corporations. Cross-sector integration amplifies its demand, as applications in feed additives, construction materials, and environmental remediation interact to form compound growth drivers.

Europe Natural Zeolite Market Trends

Europe is expected to maintain a significant position in the market, driven by sustained focus on sustainable agriculture, water treatment, and industrial applications. Countries such as Germany, France, and Italy are projected to lead through high-quality domestic production and advanced processing capabilities, ensuring reliable supply for industrial, municipal, and agricultural requirements. Tightening environmental regulations and stricter compliance standards are encouraging adoption across wastewater treatment, soil conditioning, and eco-friendly construction materials. Precision farming practices, including nutrient management and soil moisture optimization, are anticipated to further stimulate demand for natural zeolite as an efficient, eco-friendly solution.

Functional animal feed applications and soil enhancement initiatives are expected to expand, particularly in high-value livestock sectors. Circular economy initiatives and government-backed sustainability programs will create additional avenues for zeolite adoption in industries seeking cost-effective, environmentally safe alternatives. Technological advancements in processing methods will improve product consistency, purity, and application versatility, enabling zeolite to meet complex industrial and agricultural requirements. Rising awareness among manufacturers and municipalities regarding long-term environmental and operational benefits will strengthen procurement and adoption strategies.

Asia Pacific Natural Zeolite Market Trends

Asia Pacific is poised to be the fastest-growing market for natural zeolite during the 2026-2033 forecast period, driven by rapid urbanization, expanding modern retail channels, and increasing adoption of convenience-oriented food products. Countries such as India, China, and Australia are experiencing rising demand for dairy, bakery, and confectionery applications that rely heavily on milk powder, where natural zeolite enhances shelf stability and nutrient retention. Rising disposable incomes, evolving dietary preferences, and growing awareness of protein-rich and functional foods among health-conscious consumers are further fueling consumption across households and foodservice sectors.

Regional market growth finds additional support from government initiatives promoting dairy sector modernization, investments in cold chain logistics, and subsidies for milk producers, ensuring consistent supply for industrial and household applications. Large-scale processing facilities and robust dairy farming infrastructure enable high production capacity and export potential. Increasing penetration of processed and fortified foods creates new avenues for zeolite adoption, positioning Asia Pacific as the fastest-growing natural zeolite market with strong opportunities across agriculture, food processing, and industrial applications.

Competitive Landscape

The global natural zeolite market structure has achieved moderate consolidation, with leading multinational suppliers such as IMERYS, KMI Zeolite Inc., St. Cloud Mining, Zeotech International Co., Ltd., Clariant, and BASF commanding a significant share of worldwide supply. These companies have built extensive production capacities, advanced processing facilities, and robust procurement networks, which enable them to efficiently serve diverse industrial, agricultural, and municipal requirements. Their scale has supported consistent quality standards across regional and international markets, allowing operators to access reliable, high-performance zeolite products for a wide range of applications.

Market leaders have leveraged integrated supply chains and global distribution channels to ensure dependable delivery to end-users in water treatment, agriculture, construction, and animal feed sectors. Strategic partnerships, investments in processing technology, and ongoing capacity expansion have enhanced operational efficiency and lowered costs for these suppliers. Their influence has facilitated long-term contracts and reinforced strong brand recognition, enabling them to capture opportunities in emerging applications such as wastewater management, sustainable construction materials, and feed supplementation.

Key Industry Developments

- In January 2026, Blue Pacific Minerals opened a zeolite processing plant in Tokoroa, New Zealand, creating 20 jobs and supplying clinoptilolite for agriculture, water treatment, and construction. The facility processes locally sourced zeolite to meet growing demand in sustainable industries.

- In November 2025, he Bureau of Land Management (BLM) approved St. Cloud Mining's 43-well clinoptilolite exploration project east of Death Valley Junction, California, with less than 1 acre disturbance in an Area of Critical Environmental Concern. Environmental groups have filed intent to sue over alleged Endangered Species Act violations affecting protected plants and groundwater.

- In August 2025, Asahi Kasei successfully demonstrated a zeolite-based biogas purification system in Japan, achieving biomethane yield of over purity >97% from sewage sludge. The pressure vacuum swing adsorption (PVSA) technology separates CO2 and methane, enabling global licensing for renewable energy applications.

Companies Covered in Natural Zeolite Market

- IMERYS

- KMI Zeolite Inc.

- St. Cloud Mining

- Zeotech International Co., Ltd

- Clariant

- BASF

- Jingdezhen Jiayuan Activated Carbon Co., Ltd

- Honeywell International Inc.

- Silkem d.o.o.

- ZEO, Inc.

Frequently Asked Questions

The global natural zeolite market is projected to reach US$ 9.5 billion in 2026.

Rising demand for sustainable water treatment, agriculture, and industrial applications drives the market.

The market is poised to witness a CAGR of 6.8% from 2026 to 2033.

Expansion in sustainable construction materials, eco-friendly agriculture, and advanced wastewater treatment presents key market opportunities.

Some of the key market players include IMERYS, KMI Zeolite Inc., St. Cloud Mining, Zeotech International Co., Ltd, Clariant, and BASF.