- Nutraceuticals & Functional Foods

- Coconut Oil Market

Coconut Oil Market Size, Share, and Growth Forecast, 2026 - 2033

Coconut Oil Market By Product Type (Virgin, Extra Virgin, Refined, Others), Source (Organic, Conventional), Application (Food & Beverage, Cosmetics, Others), Distribution Channel (Supermarket/Hypermarket, Others), and Regional Analysis for 2026 - 2033

Coconut Oil Market Size and Trends Analysis

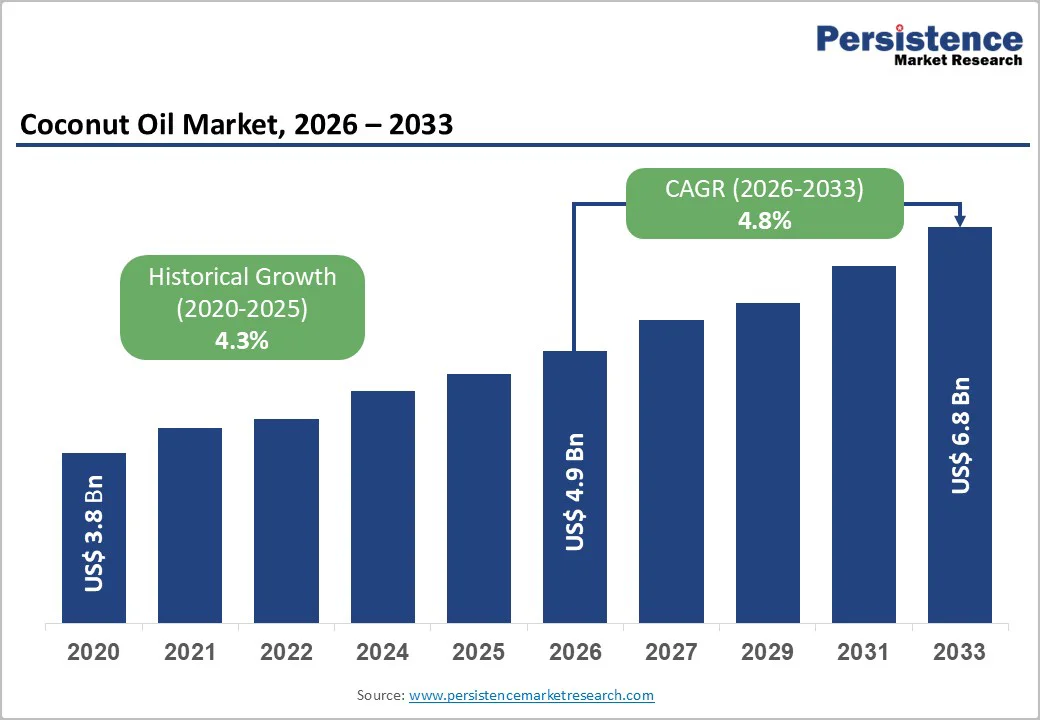

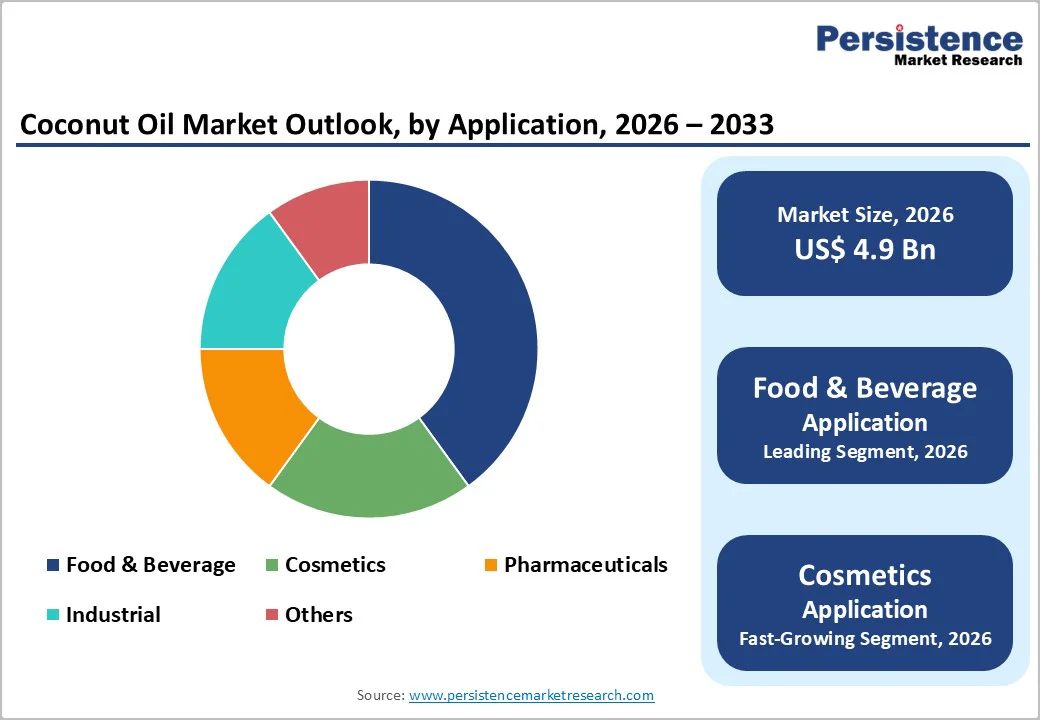

The global coconut oil market size is likely to be valued at US$4.9 billion in 2026, and is expected to reach US$6.8 billion by 2033, growing at a CAGR of 4.8% during the forecast period from 2026 to 2033, driven by the increasing prevalence of health-conscious consumption, rising demand for natural emollients in cosmetics, and advancements in cold-pressed extraction technologies.

Rising demand for multifunctional, antioxidant-packed coconut oil, particularly in food, beverage, and pharmaceutical applications, is driving widespread adoption. Innovations in virgin and extra virgin grades are enhancing appeal by providing cleaner, nutrient-rich options. The growing awareness of coconut oil’s role in promoting sustainable wellness, especially in tropical regions, continues to fuel market growth.

Key Industry Highlights:

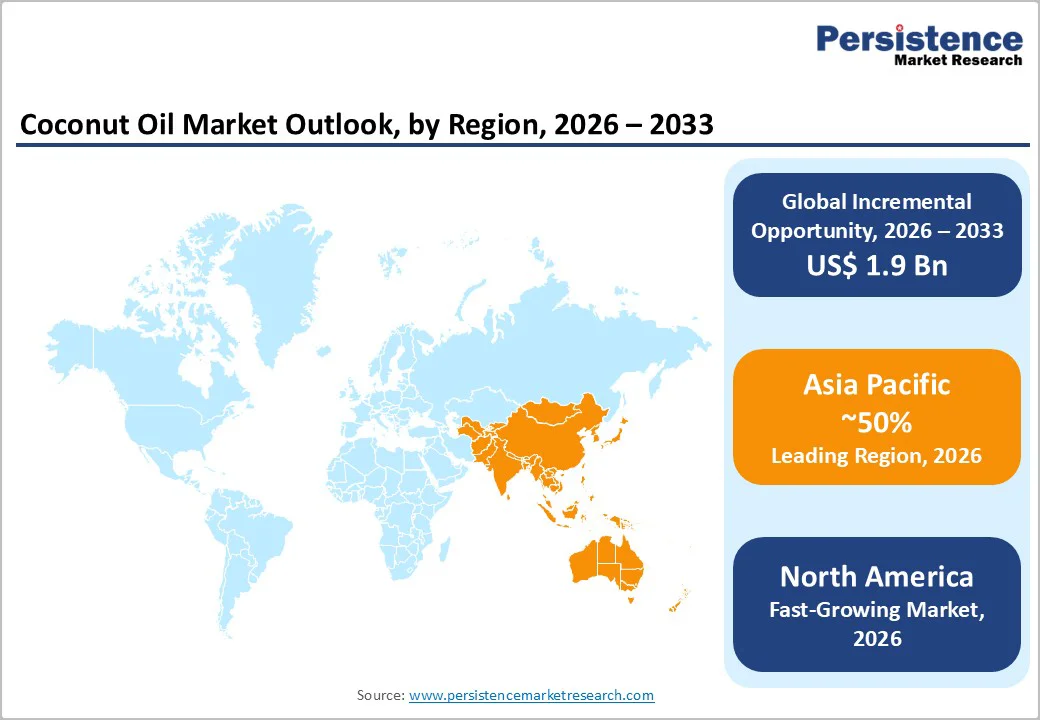

- Leading Region: Asia Pacific, anticipated to account for a 50% market share in 2026, driven by abundant production hubs, high culinary integration, and strong export growth in Indonesia and the Philippines.

- Fastest-growing Region: North America, fueled by wellness trends, rising vegan diets, and growing investments in organic sourcing in the U.S.

- Dominant Product Type: Virgin, to hold approximately 45% of the market share in 2026, as it generates strong, unrefined purity by closely mimicking natural extraction processes.

- Leading Application: Food & beverage, to account for over 40% of the market revenue, due to baking versatility, flavor enhancement, and widespread use in health foods.

- Leading Source: Organic, to contribute nearly 55% of the market revenue in 2026, due to its premium appeal, chemical-free certification, and capacity for clean-label products.

- Leading Distribution Channel: Supermarket/Hypermarket, to dominate with approximately 40% share in 2026, due to consumers requiring accessible shelf space as part of routine shopping, ensuring consistent demand.

| Key Insights | Details |

|---|---|

|

Coconut Oil Market Size (2026E) |

US$4.9 Bn |

|

Market Value Forecast (2033F) |

US$6.8 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

4.8% |

|

Historical Market Growth (CAGR 2020 to 2025) |

4.3% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Rising Demand for Natural, Multi-Use Coconut Oils

The rising preference for health-conscious consumption is quickly becoming a major opportunity for coconut oil producers, driven by growing consumer demand for nutrient-dense, multi-use oils and reduced synthetic alternatives. Traditional hydrogenated fats often create oxidation risks, especially in baking and skincare, leading to shorter shelf lives and health concerns. Natural technologies, including virgin coconut oil, extra virgin grades, organic variants, cold-pressed extracts, and fractionated forms, address these concerns by offering a stable, antioxidant-rich alternative. These formats simplify incorporation, reduce the need for preservatives, and are particularly effective during wellness booms or clean-label shifts where rapid integration is critical.

Coconut oil significantly lowers the risk of rancidity, inflammation, and filler additives, which remain major concerns in food and cosmetic settings. They also support improved bioavailability and easier storage, especially for virgin and refined types, making them ideal for tropical or export markets. As global wellness organizations push for broader nutritional coverage and user-friendly ingredients, demand continues to expand across food & beverage, cosmetics, and pharmaceuticals.

High Development and Extraction Costs

High development and extraction costs present a significant barrier for companies advancing next-generation coconut oil and novel processing systems. Developing innovative grades such as extra virgin organics, fractionated liquids, or nano-emulsified variants requires extensive research, specialized centrifuges, and advanced filtration technologies that are far more expensive than crude pressing. Purity is an even greater challenge: many premium oils, lauric acid-enriched lots, and preservative-free products are sensitive to moisture, light, and oxidation, requiring rigorous optimization to ensure they remain fresh throughout storage and blending. Achieving organic certification often involves costly soil audits, sophisticated GC-MS testing, and the use of high-grade dehumidifiers, which significantly increase R&D expenditures.

Meeting stringent regulatory expectations for microbial limits, peroxide values, and batch consistency requires multiple stability studies under various conditions and across several harvest batches. This adds both time and financial burden to development timelines. Scaling up manufacturing requires controlled dryers, specialized expellers, and quality-assurance systems, further driving up overall costs. For smaller co-ops, these challenges can limit grade diversification or delay commercialization.

Advancements in Cold-Pressed and Fractionated Delivery Platforms

Advancements in cold-pressed and fractionated coconut oil delivery platforms are transforming the global wellness landscape by addressing two major challenges: nutrient loss and application versatility. Cold-pressed oils are engineered to retain 90% bioactives, reducing reliance on heat extraction and enabling raw, enzyme-rich profiles for food use. Innovations, such as hydraulic pressing, enzymatic stabilization, lipid separation, and microencapsulation, significantly improve shelf life and reduce degradation, lowering waste costs for brands and consumer campaigns.

Progress in fractionated platforms, including MCT isolates, solid butters, liquid carriers, and hybrid blends, supports more targeted benefits by stimulating medium-chain triglycerides, the body’s first line of defense against energy slumps and skin dryness. These formats eliminate greasiness, enhance absorption, and allow versatile dosing without heating, making them highly suitable for mass cosmetic programs. New technologies such as nanoparticle emulsions, bio-adhesive gels, and VLP-based carriers further enhance delivery and efficacy response.

Category-wise Analysis

Product Type Insights

Virgin is anticipated to dominate the market, accounting for approximately 45% of the market share in 2026. Its dominance is driven by unrefined purity, antioxidant richness, and flavor retention, making it preferred for culinary drizzling. Virgin coconut oil provides lauric acid protection, ensures freshness, and contributes to a health halo, making it suitable for large-scale wellness campaigns. For example, the USDA National Nutrient Database lists unrefined/virgin coconut oil as having a high concentration of lauric acid (about 42–52% of total fatty acids) and notes that minimally processed oils retain natural antioxidants and phenolic compounds. This supports the preference for virgin coconut oil in culinary applications and wellness-focused products as these components remain intact only in unrefined oils, unlike in refined versions, where processing reduces bioactive compounds.

Extra virgin represents the fastest-growing segment, due to its superior cold-pressing and expanding use in premium cosmetics. Its nutrient-dense profile makes it ideal for targeted moisturizing and reducing irritation. Continuous innovations in low-temperature extraction are further strengthening its stability, driving rapid adoption across North America and Europe, where demand for ultra-pure, skincare-grade oils is accelerating. For example, the U.S. FDA has formally evaluated coconut oil and its derivatives, commonly sourced from cold-pressed extra virgin coconut oil, and concluded they are safe for use in cosmetics and personal care products.

Source Insights

The organic segment is anticipated to lead the market, holding approximately 55% of the share in 2026, driven by chemical-free appeal, large certification programs, and strong global demand for traceable sourcing. Their dominance continues as brands expand their use for baking, lotions, and supplements. Rising adoption of conventional blends and expanded pharma campaigns highlight the growing focus on premium wellness. For example, Marico launched a range of organic coconut oil products under its Coco Soul vegan gourmet brand, which includes 100% organic virgin coconut oil and other natural coconut-derived foods. This marks Marico’s entry into the organic products space and shows it sells certified organic coconut oil for food use.

The conventional segment is likely to be the fastest-growing segment, due to cost-efficiency and expanding inclusion of blended sources in industrial uses. The growing shift toward affordable, high-volume platforms, along with better scalability, accelerates adoption. Advancements in hybrid organics and continued progress of conventional refining entering efficiency trials drive market growth. For example, firms such as Dabur are developing conventional grades targeting soaps, enabling highly economical production and showing promising results in yield studies for bulk cosmetics.

Application Insights

The food & beverage is expected to dominate the market, contributing nearly 40% of revenue in 2026, due to remaining the primary hub for flavoring, large baking programs, and management of diverse recipes requiring versatile fats. Their strong integration, trained formulators, and ability to handle high-volume or specialty blends drive higher consumption. Food & beverage sectors are leading virgin oil rollouts as well as administering emerging fractionated trials. For example, coconut oil is widely used in the food industry owing to its pleasing flavor, easy melting behavior, resistance to oxidation, and good digestibility. The ingredient’s unique functional properties and quality position it as a versatile core component across culinary, bakery, and processed food applications, supporting its extensive use as a cooking medium and key formulation ingredient, and enabling manufacturers to enhance texture, flavor, and nutritional value in diverse food products.

The cosmetics segment represents the fastest-growing segment, driven by its strong beauty presence and expanding role in natural skincare. It offers convenient, quick, and accessible emollience, attracting users who prefer topical, low-irritant settings. Increased outreach programs, self-care focus, and wider availability of routine and luxury oils further accelerate uptake, boosting rapid adoption across both urban and semi-urban areas. For example, European imports of these natural cosmetic ingredients reached 470,561 tonnes, growing year over year as manufacturers increasingly incorporate plant-based oils and botanical extracts (e.g., aloe vera, rosehip, essential oils) into skincare and beauty products. This reflects rising consumer demand for natural, low-irritant formulations that focus on plant-derived emollients and accessible skincare benefits.

Distribution Channel Insights

The supermarket/hypermarket segment is likely to dominate the market, with approximately 40% share in 2026, due to the high volume of impulse buys and strong emphasis on accessible shelving. Shelf placements, promotional displays, and widespread access to branded aisles drive consistent demand. Rising focus on online hybrids, store exclusives, and convenience integrations further strengthens supermarket leadership. For example, Retail formats that offer one-stop shopping, wide product assortments, competitive pricing, and in-store promotions are being leveraged to drive impulse purchases, product discovery, and repeat sales. By incorporating large promotional displays and branded aisles, these channels strategically enhance visibility and engagement across both urban and suburban markets.

Online retail is the fastest-growing field, driven by the rising need for direct sourcing, vulnerability to stockouts, and expanding adoption of e-commerce bundles. Improved logistics, tailored recommendations, and stronger traceability for organic use support rapid uptake. The growing use of subscription models, flash sales, and others among remote populations further accelerates market growth. For example, e-tailers such as Amazon provide targeted online listings for extra virgin MCTs, protecting quality and reducing the risks of adulteration in shipped applications.

Regional Insights

North America Coconut Oil Market Trends

North America is likely to be the fastest-growing region, driven by the region’s advanced retail infrastructure, strong research and development capabilities, and high public awareness of wellness benefits. Distribution systems in the U.S. and Canada provide extensive support for consumption programs, ensuring wide accessibility of coconut oil across food, cosmetics, and pharma populations. Increasing demand for virgin, convenient, and easy-to-incorporate forms is further accelerating adoption, as these formats improve usability and reduce barriers associated with imports.

Innovation in coconut oil technology, including stable MCT profiles, improved fractionation delivery, and targeted antioxidant enhancement, is attracting significant investments from both public and private sectors. Government initiatives and health campaigns continue to promote use against dietary gaps, skin aging, and emerging clean-beauty threats, creating sustained market demand. The growing focus on organic blends and industrial uses, particularly for pharma and others, is expanding the target applications for coconut oil.

Europe Coconut Oil Market Trends

Europe is projected to lead with a market share of 25% in 2026, driven by increasing awareness of nutritional benefits, strong distribution systems, and government-led sustainability programs. Countries such as Germany, France, and the U.K. are leveraging well-established wellness frameworks to promote the routine adoption of innovative oil delivery methods, including coconut oil, across food and cosmetic applications. These natural formulations target health-conscious consumers, eco-aware populations, and cosmetic users, enhancing compliance, product adoption, and market coverage. According to official trade and market data from CBI (Centre for the Promotion of Imports from developing countries), an initiative supported by the European Commission and multiple European governments, Europe remains the world’s largest importer of vegetable and essential oils for cosmetic use, highlighting a key growth opportunity for ingredient suppliers.

Technological advancements in coconut oil development, such as enhanced MCT yield, source-targeted delivery, and improved refined grades, are further boosting market potential. European authorities are increasingly supporting research and trials for oils against both routine and specialized needs, strengthening market confidence. The growing emphasis on convenient, refillable options is aligned with the region’s focus on preventive health and reducing packaging waste. Public awareness campaigns and promotion drives are expanding reach in both urban and rural areas, while producers are investing in expellers and novel variants to increase efficacy.

Asia Pacific Coconut Oil Market Trends

Asia Pacific is likely to dominate the market for coconut oil in 2026, accounting for 50% of the market share, driven by rising wellness awareness, increasing government initiatives, and expanding application programs across the region. Countries such as India, Indonesia, the Philippines, and Sri Lanka are actively promoting oil campaigns to address culinary traditions and emerging beauty needs. Coconut oil is particularly attractive in these regions due to its local sourcing, ease of processing, and suitability for large-scale export drives in both urban and rural populations.

Technological advancements are supporting the development of stable, effective, and easy-to-extract coconut oil, which can withstand challenging tropical conditions and minimize waste dependence. These innovations are critical for reaching remote plantations and improving overall yield coverage. Growing demand for virgin, cosmetics, and industrial applications is contributing to market expansion. Public-private partnerships, increased agro expenditure, and rising investment in pressing research and manufacturing capacity are further accelerating growth. The convenience of coconut oil delivery, combined with improved purity and reduced risk of spoilage, positions coconut oil as a preferred choice.

Competitive Landscape

The global coconut oil market features competition between established agro-processors and emerging organic brands. In North America and Europe, Nutiva Inc. and Marico lead through strong R&D, distribution networks, and retail ties, bolstered by innovative grades and wellness programs. In Asia Pacific, Dabur advances with localized solutions, enhancing accessibility. Nutrient-enhanced delivery boosts efficacy, cuts oxidation risks, and enables mass formulations across regions. Strategic partnerships, collaborations, and acquisitions merge expertise, expand plantations, and speed commercialization. Organic formulations solve purity issues, aiding penetration in health-focused areas.

Key Industry Developments

- In July 2025, Onge Tribe introduced cold-pressed coconut oil, advancing economic empowerment aligned with the PM JANMAN Mission.

- In September 2025, Marico expanded its premium haircare portfolio with the launch of Parachute Advansed Olive Enriched Coconut Hair Oil, highlighting olive as a key ingredient for hair nourishment and strength while strengthening the brand’s lineup of natural haircare solutions.

Companies Covered in Coconut Oil Market

- Nutiva Inc.

- Spectrum Organic Products

- Barlean's Organic Oils

- Dr. Bronner's

- Windmill Organics Ltd.

- Connoils LLC

- Bioriginal Food & Science Corp.

- Luong Quoi Coconut Co. Ltd.

- AOS Products

- Serendipol

- Marico

Frequently Asked Questions

The global coconut oil market is projected to reach US$4.9 billion in 2026.

The rising prevalence of health-conscious consumption and demand for natural emollients are the key drivers.

The coconut oil market is poised to witness a CAGR of 4.8% from 2026 to 2033.

Advancements in cold-pressed and fractionated delivery platforms are the key opportunities.

Nutiva Inc., Spectrum Organic Products, Barlean's Organic Oils, Dr. Bronner's, and Luong Quoi Coconut Co. Ltd. are the key players.