- Automation & Robotics

- Mobile Robot (AGV and AMR) Market

Mobile Robot (AGV and AMR) Market Size, Share, and Growth Forecast, 2026 - 2033

Mobile Robot (AGV and AMR) Market by Product (Latent Jacking Robot, Forklift Robot, Assembly Robot, Tugger / Towing Robot, Sorting Robot, Tote/Bin Robot, Others), Navigation (Laser Guidance, Vision-Based, SLAM, Magnetic Guidance, Others), End-user and Regional Analysis for 2026 - 2033

Mobile Robot (AGV and AMR) Market Size and Trends Analysis

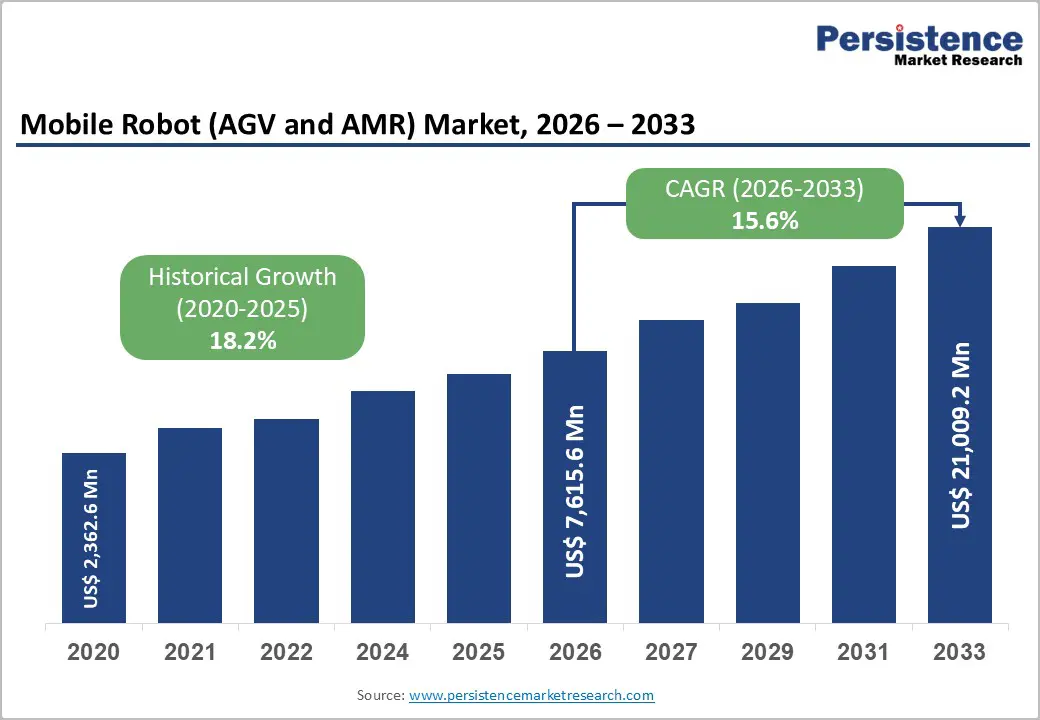

The global mobile robot (automated guided vehicle [AGV] and autonomous mobile robot [AMR]) market size is valued at US$ 7,615.6 million in 2026 and is projected to reach US$ 21,009.2 million by 2033, growing at a CAGR of 15.6% between 2026 and 2033. Historically, the market demonstrated robust expansion with a CAGR of 18.2%, rising from US$ 2,362.6 Mn in 2020.

The market is undergoing a pivotal transformation driven by intensifying global labor shortages and the growing need for interoperability enabled by Industry 4.0. There is a rapid shift from fixed automation to flexible, autonomous solutions, especially in high-velocity environments such as automotive manufacturing and e-commerce fulfillment. While North America and Europe remain mature innovation hubs, the Asia-Pacific region is emerging as the global volume leader, supported by large-scale expansion in manufacturing sectors.

Key Industry Highlights:

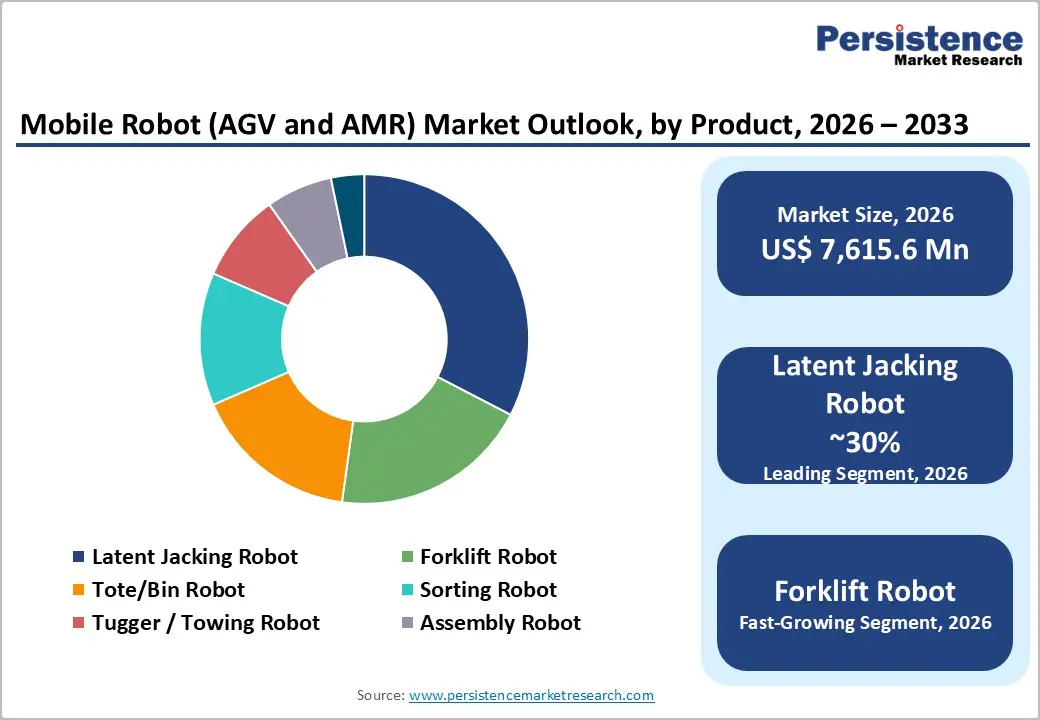

- Leading Product: Latent jacking robots dominate with over 30% market share by 2026, optimizing space utilization in e-commerce fulfillment centers. Forklift robots are rapidly growing in use to automate pallet handling in high-bay warehouses, improving safety and operational efficiency.

- Leading Navigation: SLAM holds over 36% market share by 2026, providing precise mapping in dynamic warehouses. Vision-based navigation is the fastest-growing segment, enabling cost-efficient, adaptive operations in human-centric environments.

- Leading End-user: Manufacturing is leading with over 65% market share by 2026, driven by automotive ~30% share, EV/battery production, and precision material handling needs. Warehousing & logistics are the fastest-growing segment, with 3PL adoption projected to account for over 25% of market share by 2026 and e-commerce fulfillment growing at a CAGR of 20% between 2026 and 2033.

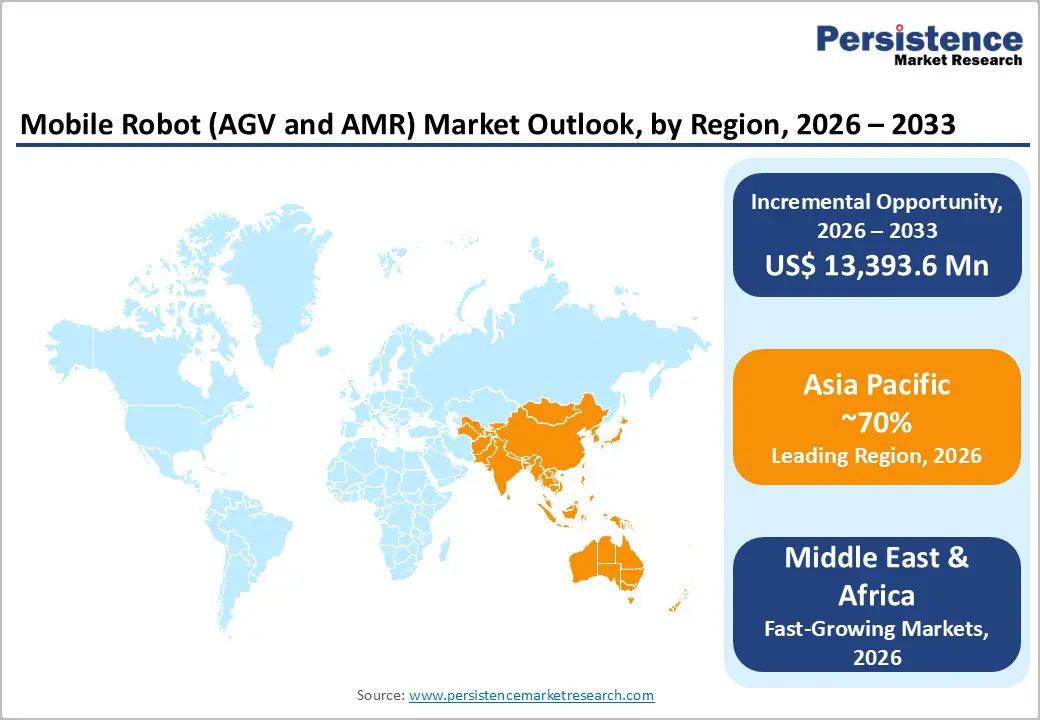

- Leading Region: Asia Pacific dominates with 70% of market value and 75% of volume by 2026, China’s market is projected to reach over US$ 3.5 billion. North America is a mature market with the U.S. projected to surpass US$ 3,500 million by 2033, driven by automotive, EV/battery, and electronics sectors. Europe’s market is projected to surpass US$ 1,500 million by 2026, led by Germany, with strong emphasis on collaborative robotics and CE-compliant solutions.

- Leading Driver: E-commerce sales in the U.S. rose to 16.3% of total retail in Q2 2025, up from 15.5% YoY, highlighting the push for order fulfillment automation. Labor shortages in manufacturing and logistics, and supply chain diversification strategies like China Plus One, are accelerating adoption.

| Key Insights | Details |

|---|---|

| Mobile Robot (AGV and AMR) Market Size (2026E) | US$ 7,615.6 Mn |

| Market Value Forecast (2033F) | US$ 21,009.2 Mn |

| Projected Growth (CAGR 2026 to 2033) | 15.6% |

| Historical Market Growth (CAGR 2020 to 2025) | 18.2% |

Market Dynamics

Driver - E-commerce Expansion and Last-Mile Automation

The rapid expansion of e-commerce and direct-to-consumer models is driving unprecedented demand for order fulfillment automation, with U.S. e-commerce sales rising to 16.3% of total retail in Q2 2025, up from 15.5 % a year earlier. Mobile robots (AGVs and AMRs) enable high-velocity, high-accuracy operations, achieving picking accuracy above 99.9% in optimized warehouses. Over 50% of major logistics hubs globally, particularly in North America and the Asia Pacific, have adopted robotic automation. The push for same-day and next-day delivery, coupled with the rise of urban micro-fulfillment centers, makes compact, agile mobile robots essential for dense storage environments without major infrastructure changes.

Critical Labor Gap in Manufacturing & Logistics

The global shortage of skilled labor in manufacturing and logistics operations has become a critical catalyst for mobile robot adoption. For instance, the U.S. manufacturing sector is expected to face 2.1 million unfilled jobs by 2030, posing significant operational risks. Mobile robots mitigate this gap by automating intralogistics material handling tasks, reducing reliance on manual labor, and allowing existing employees to focus on higher-value activities. By taking over repetitive, non-value-added processes, mobile robots ensure operational continuity and optimize workforce utilization.

China Plus One Strategy & Supply Chain Resilience

Global manufacturers are diversifying supply chains away from single-source dependencies, driving new Greenfield factory projects in India, Vietnam, and Mexico designed with AMR-friendly layouts, wider aisles, fiducial markers, and dedicated charging zones, accelerating AMR adoption. In North America and Europe, reshoring initiatives use high automation, including AMRs, to offset higher labor costs. Sectors like electronics, automotive, textiles, pharma, and FMCG are increasingly adopting robotics-native material handling over traditional conveyors. Policy support through the U.S. CHIPS Act, EU Critical Raw Materials Act, and friend-shoring incentives further boost AMR deployment.

Restraint

Interoperability & The VDA 5050 Challenge

Interoperability remains a key restraint, as mixed-vendor fleets create automation islands due to proprietary software and communication protocols. Standards like VDA 5050 aim to unify operations, but varying manufacturer implementations cause deadlocks and traffic conflicts and require complex middleware integration. Upgrading existing AGVs to support VDA 5050 often demands both hardware and software modifications, increasing deployment time, technical risk, and costs, particularly in brownfield sites with established fleets. For example, a pallet mover from vendor A conflicts with a bin-picking robot from vendor B if protocols are not applied consistently.

Opportunity

Robotics-as-a-Service (RaaS) Democratization

Robotics-as-a-Service (RaaS) is democratizing automation by replacing high upfront costs with flexible monthly subscriptions, enabling SMEs and smaller warehouses to deploy AGVs and AMRs affordably. This pay-as-you-go model allows businesses to scale fleets based on demand, accelerate ROI, and benefit from bundled maintenance, updates, and performance monitoring. Vendors gain recurring revenue streams, fueling faster innovation. Global adoption is strong, with nearly 200,000 professional service robots sold in 2024, up 9% YoY, and RaaS fleets growing 31% according to IFR, highlighting rapid subscription-based deployment across retail, logistics, manufacturing, and healthcare.

AI and Autonomous Navigation Unlocking Mobile Robot Potential

Advancements in autonomous navigation and AI, such as enhanced SLAM, 3D LiDAR, and vision-based systems, enable AMRs to operate safely in dynamic, unstructured environments, improving obstacle avoidance, path optimization, and task allocation. Cloud-based AI and edge processing enhance real-time fleet coordination and predictive maintenance, reducing integration complexity and enabling scalable multi-facility deployments. Industries like e-commerce, automotive, semiconductors, and FMCG are rapidly adopting AMRs to boost productivity, flexibility, and ROI. For example, in June 2025, ABB launched the Flexley Mover P603, an ultra-compact AMR with 1500 kg payload capacity, AI-driven Visual SLAM, integrated load sensing, and AMR Studio 4.0 for no-code fleet management.

Category-wise Analysis

Product Insights

Latent Jacking Robots Optimizing Space Utilization & Boosting Operational Efficiency

Latent jacking robots, often referred to as shelf-to-person robots, are projected to account for over 30% of the mobile robot market by 2026. Their dominance is driven by widespread adoption in e-commerce fulfillment centers, where they transport high-density storage racks directly to picking stations. Their compact design, high speed, and proven ROI in Amazon-style warehouses make them the preferred solution for large-scale retail logistics.

Forklift Robots Growing Rapidly with Automation Demand

Forklift robots are expected to grow rapidly due to the critical need to automate pallet handling in high-bay warehouses. With manual forklift operations accounting for a significant portion of warehouse accidents and labor costs, the shift toward autonomous solutions is accelerating. These robots perform high-precision operations, such as double-deep racking and seamless interaction with conveyor systems, effectively bridging production and shipping operations. They also offer greater environmental flexibility and compatibility with diverse load configurations, making them a key driver of adoption in modern warehouses.

Navigation Insights

SLAM (Simultaneous Localization and Mapping) Optimizing Layouts & Boosting Accuracy

SLAM is projected to hold over 36% of the market share by 2026. LiDAR-based SLAM has become the industry standard for indoor navigation, providing high accuracy and reliability without requiring physical infrastructure. Its ability to dynamically map environments makes it particularly suitable for the constantly changing layouts of manufacturing plants and busy warehouses. Technology offers several key advantages, including reduced deployment time, seamless integration with existing facilities, and flexibility to adapt to evolving operational needs.

Vision-Based Navigation Driving Smarter & Cost-Efficient Deployments

Vision-based navigation is the fastest-growing segment, powered by advances in camera technology and AI. Unlike LiDAR, V-SLAM captures both where and what objects are, enabling smarter navigation in human-centric environments. Camera sensors are cheaper than high-end LiDAR, making large-scale deployments cost-effective. Companies such as Geek+ have demonstrated the technical viability of camera-based navigation in warehouse operations. Technology is particularly strong in dynamic settings, where layouts and equipment frequently change, as computer vision inherently adapts to visual changes without requiring markers or infrastructure modifications.

End-user Insights

Mobile Robots Driving Manufacturing Efficiency & Precision Handling

The manufacturing sector is the leading, projected to account for over 65% market share by 2026. Manufacturing's dominance is reinforced by established automation investment budgets, documented productivity benefits, and mature technology integration methodologies. Within this sector, the Automotive industry is the primary driver, expected to hold around 30% market share, fueled by widespread adoption of automation, the development of new electric vehicle platforms, and the expansion of battery production. Photovoltaic cell and lithium-ion battery manufacturing are also critical growth engines, demanding contamination-free, high-precision transport solutions.

Warehousing & Logistics Revolutionizing Micro-Fulfillment and Delivery Speed

Warehousing and logistics are the fastest-growing segment, driven by the rapid expansion of 3PL (Third-Party Logistics) providers. Flexible AMRs enable high-mix, high-velocity fulfillment, while AGVs streamline pallet movement and docking, improving operational efficiency and reducing errors. The 3PL/supply chain sub-segment is projected to account for over 25% of the market share by 2026. The e-commerce and retail sector is expected to grow at a CAGR of over 20% between 2026 and 2033, as retailers increasingly automate micro-fulfillment centers to meet same-day delivery demands.

Regional Insights

North America Mobile Robot (AGV and AMR) Market Trends

North America is a mature, high-value market, with manufacturing driving over 70% of demand, particularly in automotive, new energy (EV/battery), and electronics sectors. High labor costs, severe workforce shortages, and reshoring initiatives are accelerating the adoption of AMRs and AGVs, especially in warehouse operations. Favorable regulations, such as ANSI/RIA R15.08, support safe human-robot collaboration, while regional technology leadership in AI, SLAM, and safety systems positions North America as an innovation hub. The U.S. mobile robot (AGV and AMR) market alone is projected to surpass US$ 3,500 million by 2033, growing at a 14% CAGR from 2026, reflecting strong demand for advanced autonomous solutions.

Asia Pacific Mobile Robot (AGV and AMR) Market Trends

Asia Pacific dominates the global mobile robot (AGV and AMR) market, expected to account for 70% of value and 75% of volume by 2026, with China Mobile Robot (AGV and AMR) market projected to reach at US$ 3.5 billion. Manufacturing accounts for over 65% of China’s demand, led by companies such as Geek+ (vision-based AMRs) and Hai Robotics (case-handling AMRs), supported by government Industry 4.0 initiatives and modernization subsidies. India and Southeast Asia are emerging as fast-growing markets due to supply chain diversification and Make in India incentives. Japanese players such as OMRON innovate with medium-payload MD Series AMRs, while Chinese firms compete on cost and Western firms on technological sophistication. Supply chain localization and rising labor costs in developed Asian markets further accelerate automation adoption.

Europe Mobile Robot (AGV and AMR) Market Trends

Europe’s mobile robot (AGV and AMR) market is projected to surpass US$ 1,500 million by 2026, led by Germany with over 20% share, followed by the U.K. and France. The growth is driven by a strong industrial base, particularly the automotive sector, and investments in lights-out manufacturing across Eastern and Central Europe. The region emphasizes high-safety, collaborative robotics, with strict CE compliance, HMI safety, and collision risk protocols shaping product design. European operators favor human-robot collaborative systems, creating distinct requirements and higher regulatory costs that protect established players. Strategic moves like ABB’s acquisition of Sevensense Robotics highlight the focus on AI-enabled SLAM integration and fully autonomous logistics fleets.

Competitive Landscape

The market is currently moderately fragmented but undergoing a period of strategic consolidation. Leading players command significant market shares, particularly in the high-volume manufacturing and logistics segments. The top tier is comprised of diversified industrial automation giants that have acquired specialized AMR startups to expand their portfolios. Market concentration is higher in the Asia Pacific region due to the dominance of domestic Chinese manufacturers, while Western markets display a mix of pure-play robotics firms and legacy automation providers competing for enterprise contracts.

Key Industry Developments:

- In October 2025, HOJ Innovations launched a new Autonomous Mobile Robots (AMR) division to integrate AMRs seamlessly with its WarehouseOS inventory management software. The company will offer turnkey, custom-designed warehouse automation solutions, with full offerings available by Q2 2026 and standalone AMRs already on the market.

- In April 2025, OMRON Robotics and Safety Technologies launched the OL-450S, a low-profile, omnidirectional AMR with a 450kg payload and integrated lifting plate, designed to streamline material handling across industries.

- In November 2024, Geekplus and Intel introduced the world’s first Vision Only Robot Solution, featuring Intel’s Visual Navigation Modules and RealSense depth camera for advanced perception and navigation. The system delivers highly accurate positioning, obstacle avoidance, and intelligent robot following, boosting efficiency in complex logistics environments.

Companies Covered in Mobile Robot (AGV and AMR) Market

- ABB

- KUKA AG

- OMRON Corporation

- Locus Robotics

- Daifuku Co., Ltd.

- Geekplus Technology Co., Ltd.

- Zebra Technologies Corp.

- Dematic

- Yaskawa America, Inc.

- Vecna Robotics

- Toyota Industries Corporation

- Rockwell Automation

- Hai Robotics

- Hikrobot Co., Ltd.

- Others

Frequently Asked Questions

The global mobile robot (AGV and AMR) market is projected to be valued at US$ 7,615.6 Mn in 2026.

Rising automation needs, supported by labor shortages and e-commerce growth, are a key driver of the market.

Asia Pacific is expected to dominate due to large-scale manufacturing expansion, strong government support for automation.

The market is expected to witness a CAGR of 15.6% from 2026 to 2033.

Rapid adoption of Robotics-as-a-Service (RaaS) and growing demand for flexible, scalable automation driven by AI-enabled navigation and interoperability standards are creating strong growth opportunities.

ABB, KUKA AG, OMRON Corporation, Locus Robotics, Daifuku Co., Ltd., Geekplus Technology Co., Ltd., Zebra Technologies Corp. are among the leading key players.