- Home Care & Utilities

- Mobile Pet Care Market

Mobile Pet Care Market Size, Share, and Growth Forecast, 2026 – 2033

Mobile Pet Care Market by Pet Type (Dogs, Cats, and Others), Service Type (Medical Care and Grooming), End-user (Individual, Commercial), and Regional Analysis 2026 – 2033

Mobile Pet Care Market Size and Trends Analysis

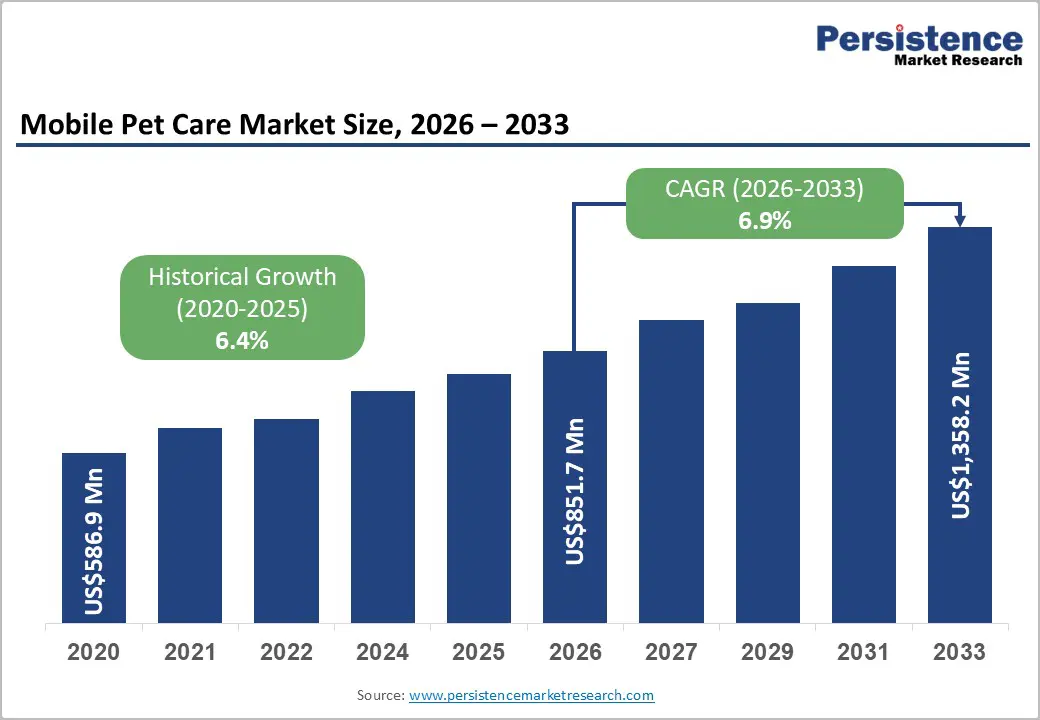

The global mobile pet care market size is likely to be valued at US$851.7 million in 2026 and is expected to reach US$1,358.2 million by 2033, growing at a CAGR of 6.9% during the forecast period from 2026 to 2033, driven by demand for convenient at-home services as urban pet owners prioritize flexibility. Telemedicine integrations enable rapid virtual consults that complement mobile fleets effectively. These dynamics position the market for sustained expansion amid rising pet ownership rates.

Technological advancements in scheduling software are projected to optimize fleet routing efficiency substantially globally. Rising veterinary service accessibility requirements are set to accelerate localized neighborhood clinic deployments consistently. Fuzzy with the Fuzzy Telehealth App is positioned to bridge critical diagnostic accessibility gaps immediately.

Key Industry Highlights:

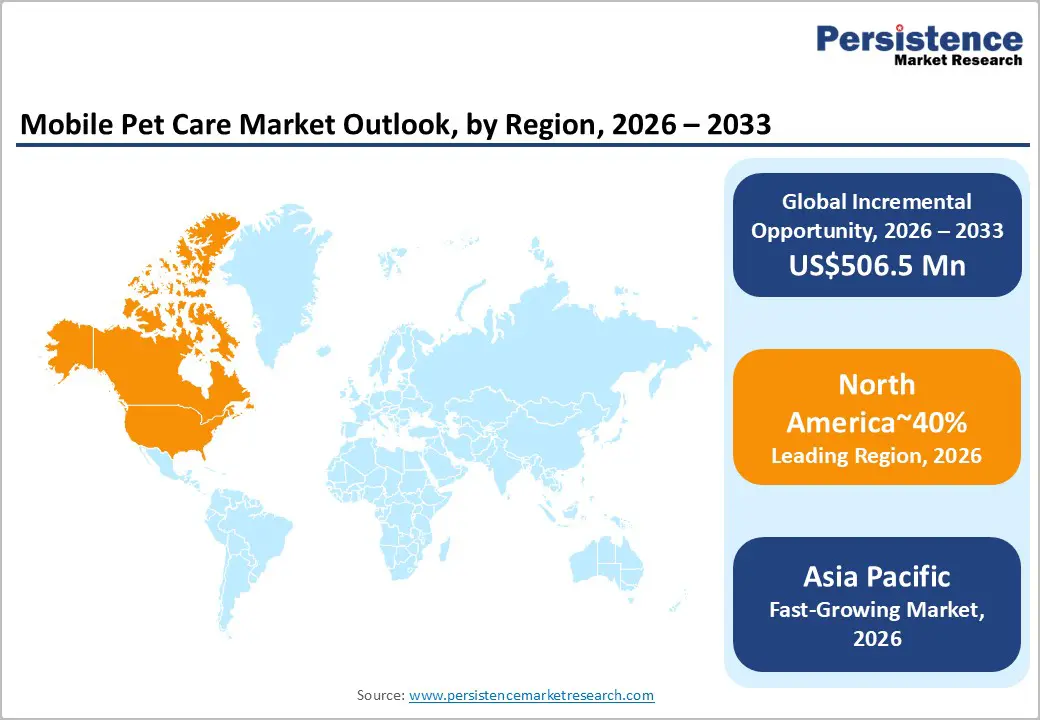

- Leading Region: North America is projected to lead, accounting for approximately 40% share in 2026, supported by mature telemedicine ecosystems, high pet insurance penetration, and dense urban consumer bases favoring on-demand care.

- Fastest-growing Region: Asia Pacific is anticipated to grow fastest, driven by rapid urbanization, expanding middle-class pet adoption, and government-backed veterinary mobility initiatives.

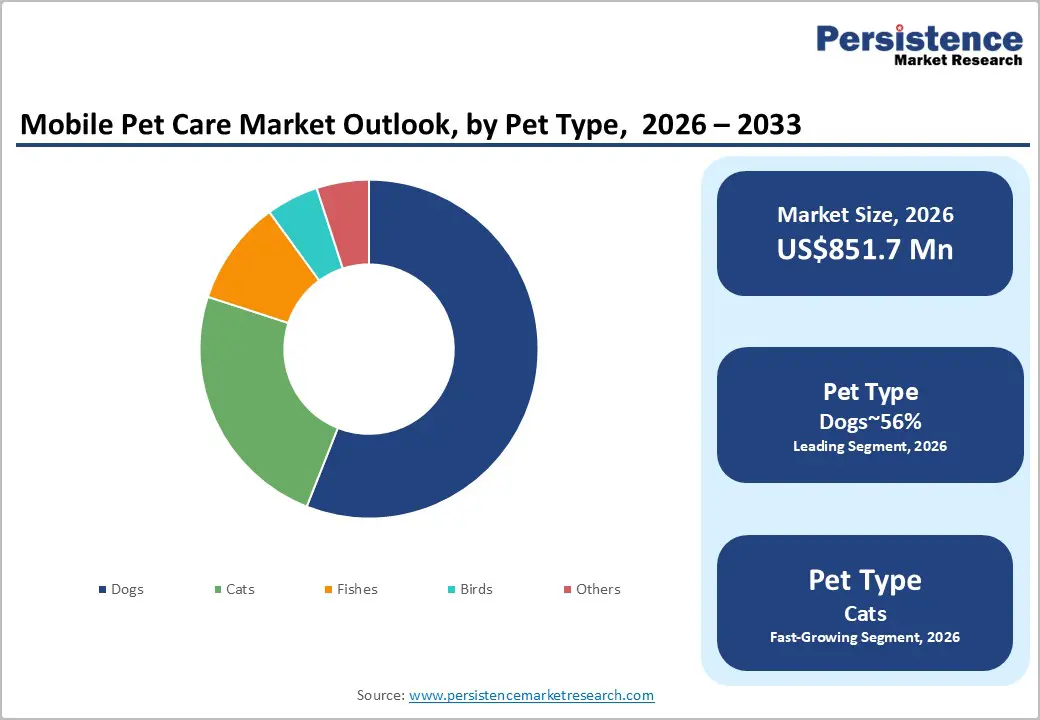

- Leading Pet Type: Dogs are expected to lead, accounting for approximately 56% share in 2026, anchored by a higher incidence of chronic conditions requiring frequent mobile interventions and established grooming routines.

- Leading Service Type: Medical care is projected to dominate, holding approximately 69% share in 2026, driven by telemedicine advancements and insurance reimbursements for at-home diagnostics.

| Key Insights | Details |

|---|---|

| Mobile Pet Care Market Size (2026E) | US$851.7 Mn |

| Market Value Forecast (2033F) | US$1,358.2 Mn |

| Projected Growth (CAGR 2026 to 2033) | 6.9% |

| Historical Market Growth (CAGR 2020 to 2025) | 6.4% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growth Analysis – Surging Suburban Demand for At-Home Preventive Veterinary Diagnostics

Suburban demographic redistribution is accelerating demand for decentralized preventive veterinary diagnostics infrastructure deployment. Remote work normalization is sustaining continuous residential availability, enabling consistent utilization of home-based services. Aging companion animal populations are intensifying requirements for recurring monitoring and chronic disease management interventions. Preventive care paradigms are reshaping traditional clinic visitation frequencies toward distributed, proximity-based service models. Consumer preference for personalized attention is reinforcing willingness to engage with premium mobile diagnostic subscriptions. These behavioral shifts are collectively strengthening long-term demand visibility for localized veterinary diagnostic ecosystems.

Technological advancements are reinforcing service feasibility and scalability across suburban operating environments. Diagnostic miniaturization is enabling the deployment of portable blood analysis and imaging capabilities within mobile units. Providers such as Vetco Total Care and BetterVet are expanding home-based diagnostic portfolios to capture preventive care demand. Algorithm-driven scheduling systems are optimizing route density, improving asset utilization, and service throughput efficiency. Integrated digital health records are enhancing interoperability across distributed care providers, ensuring longitudinal patient data continuity. These innovations are structurally anchoring suburban penetration strategies within technology-enabled veterinary service models.

Pet Humanization Fueling At-Home Convenience Demand

Increasing pet humanization is redefining service expectations, positioning companion animals within family-centric care frameworks. Urban pet owners are prioritizing convenience-driven solutions that eliminate logistical burdens associated with clinic visits. This behavioral shift is accelerating the adoption of mobile veterinary services integrated with app-based booking systems. Time-constrained professionals are increasingly valuing seamless scheduling interfaces that align with dynamic daily routines. Telemedicine platforms are expanding access by enabling immediate virtual triage before in-person interventions. These evolving preferences are collectively broadening service utilization across demographics seeking personalized, continuous pet wellness management.

Digital platform integration is strengthening customer retention and enabling premium service monetization. Providers such as Vetster and Airvet are leveraging telehealth and artificial intelligence-driven triage to optimize dispatch efficiency. Ecosystem models combining consultations, delivery partnerships, and diagnostics are reinforcing user engagement continuity. Wearable pet health technologies are further enabling predictive care interventions, integrating real-time data into service workflows. These technological advancements are enhancing pricing power while fostering loyalty through differentiated, convenience-centric service offerings. Competitive dynamics are increasingly defined by platform scalability and digital ecosystem depth.

Expanding Premiumization of Specialized Mobile Grooming Services

Humanization trends are expected to elevate specialized dermatological grooming treatments across urban demographics globally. Organic shampoo applications are projected to command substantial price premiums within affluent neighborhoods continually. Anxious animal behavioral considerations are anticipated to drive demand for isolated grooming environments strongly. Climate-controlled mobile facilities are likely to ensure optimal comfort during extreme weather conditions reliably. Specialized breed-specific styling capabilities are set to differentiate elite service providers from competitors significantly. These qualitative enhancements are positioned to expand aggregate market revenue realization trajectories incredibly consistently.

Aussie Pet Mobile with 150-Point Grooming Van is expected to standardize elite service protocols. Advanced hydrobath installations are projected to deliver superior therapeutic cleaning outcomes for pets consistently. HydroDog with Big Blue Dog Van is anticipated to capture significant visual branding advantages. Quiet motor technologies are likely to minimize auditory stress during intricate grooming procedures reliably. Integrated water recycling systems are set to improve daily operational sustainability metrics substantially globally. These premium equipment investments are positioned to capture highly lucrative recurring revenue streams continuously.

Barrier Analysis – Escalating Mobility and Maintenance Costs Constraining Mobile Veterinary Service Expansion

Rising fuel price volatility is materially increasing operating expenditures for mobile veterinary service fleets. Extensive geographic coverage, particularly across low-density regions, intensifies fuel consumption and route inefficiencies. Specialized onboard medical equipment introduces complex maintenance cycles requiring high-cost components and technical servicing. Inflationary pressures are compounding as operators gradually transition toward regulatory-compliant low-emission vehicle platforms. These cumulative cost burdens disproportionately impact smaller providers, limiting their ability to scale beyond concentrated urban demand clusters. Pricing pass-through strategies remain constrained by consumer sensitivity, particularly in cost-conscious pet owner segments. Consequently, operational economics are tightening across mobile service delivery models within the broader veterinary care ecosystem.

Cost inflation is redistributing margin pressures across service providers, equipment suppliers, and end-users. Fleet modernization initiatives are elevating capital intensity, with companies such as Bond Vet managing upgrade cycles that constrain profitability expansion. Simultaneously, operators, including VIP Petcare, are optimizing routing strategies to mitigate fuel expenditure volatility. Subscription-based pricing structures are emerging to stabilize revenue predictability amid fluctuating operational costs. Inventory turnover delays are increasing holding costs for distributors supplying mobile units with consumables and equipment. End-users increasingly exhibit selective purchasing behavior, prioritizing bundled service offerings over standalone interventions.

Acute Shortages of Qualified Mobile Veterinary Personnel

Intense industry-wide veterinary talent scarcity is expected to constrain rapid geographic fleet expansions globally. The solitary nature of mobile practice is projected to deter collaborative clinical practitioners completely. Unpredictable environmental working conditions are anticipated to complicate consistent technician retention rate metrics continually. Extensive daily vehicular navigation requirements are likely to accelerate practitioner burnout and fatigue significantly. Specialized, solitary diagnostic skillsets are set to demand prohibitive recruitment and training expenditures consistently. These structural labor deficits are positioned to throttle aggregate maximum service capacity limits profoundly.

The vets with an at-home veterinary fleet are expected to battle intense clinical recruitment competition. Comprehensive autonomous practitioner training programs are projected to require extensive institutional resource commitments continuously. BetterVet with BetterVet Mobile Care is anticipated to implement aggressive compensation packages for retention. Complex solo procedural safety protocols are likely to require highly experienced medical professionals constantly. Diminished collegiate veterinary graduation rates are set to exacerbate long-term regional staffing shortages profoundly. These formidable workforce limitations are positioned to dictate ultimate market penetration velocity constraints significantly.

Opportunity Analysis – Expanding Geriatric Pet Palliative and Hospice Care

Aging companion animal populations are expected to unlock profound localized end-of-life service demands globally. Sensitive localized palliative interventions are projected to minimize severe transit stress for geriatric animals. Compassionate home-based euthanasia procedures are anticipated to capture premium emotional value from pet owners. Continuous chronic pain management protocols are likely to establish highly recurring localized appointment schedules. Specialized hospice training credentials are set to differentiate elite empathetic practitioners from generalized providers. This emotional care segment is positioned to generate uniquely stable recession-resistant revenue streams continuously.

Lap of Love with In-Home Euthanasia Network is expected to dominate compassionate end-of-life transitions. Enhanced mobile pharmacy capabilities are projected to facilitate seamless, localized pain medication dispensations consistently. Peaceful Passage with Hospice Care Van is anticipated to pioneer holistic geriatric support frameworks. Grief counseling integration platforms are likely to deepen profound client loyalty and trust strongly. Advanced localized diagnostic monitoring is set to optimize continuous senior animal comfort protocols reliably. These specialized compassionate services are positioned to command unparalleled regional community goodwill profoundly globally.

Convergence of Subscription Pet Care Bundles across Grooming and Veterinary Services

Recurring subscription models integrating grooming with preventive veterinary services are restructuring pet care delivery frameworks. These bundled offerings address fragmentation in care workflows by synchronizing routine hygiene and health monitoring. Rising middle-class pet ownership is reinforcing demand for predictable, consolidated expenditure structures within household budgets. Direct-to-consumer digital platforms are enabling persistent engagement through scheduling automation and personalized service interfaces. Regulatory support for pet wellness reimbursements is further legitimizing preventive care adoption across organized service channels. This convergence enhances service frequency while embedding continuity across grooming and medical interventions within unified care pathways.

The subscription bundling is driving ecosystem consolidation across service providers and digital intermediaries. Platform-led integration enables cross-selling between consumables, diagnostics, and on-demand services within closed-loop engagement environments. Companies such as Wag! and Chewy are extending service portfolios to capture recurring revenue streams beyond transactional retail. These models increase customer lifetime value while structurally reducing churn through embedded service dependencies. Urban market penetration is accelerating due to logistical feasibility and higher digital adoption rates. Consequently, competitive intensity is shifting toward platform depth, service integration, and retention-driven monetization architectures.

Category–wise Analysis

Pet Type Insights

Dogs are anticipated to lead, accounting for approximately 56% share in 2026, driven by frequent preventative healthcare necessities. Robust canine outdoor activities are projected to drive continuous localized dermatological grooming requirements consistently. Larger breed transportation challenges are anticipated to accelerate at-home diagnostic service adoption rates profoundly. Aussie Pet Mobile with 150-Point Grooming Van is likely to capture escalating suburban demands.

Vetster with Vetster App dominates diagnostics for canine chronic conditions through app-based triage. Airvet with Airvet Platform deploys vans optimized for multi-dog households efficiently. PetDesk with PetDesk Mobile integrates scheduling for pack grooming routines seamlessly. Routine vaccination compliance mandates are set to necessitate regular veterinary mobile fleet dispatches reliably. The vets with an at-home veterinary fleet are positioned to dominate complex localized canine interventions.

Cats are expected to be the fastest-growing segment, driven by acute feline travel anxiety reduction needs. Severe clinical setting stressors are projected to catalyze unprecedented home-based feline diagnostic adoption globally. Feline-friendly handling protocols are anticipated to optimize localized therapeutic outcome efficacies and safety consistently. BetterVet with BetterVet Mobile Care is likely to pioneer specialized quiet-environment feline wellness exams. Vendor strategies emphasize compact tools for feline agility in tight spaces.

Pawp with Pawp Telehealth accelerates growth via AI behavior analysis tied to doorstep care. Vetsie with Vetsie Go targets unmet litter-related hygiene gaps effectively. Advanced portable ultrasound miniaturization is set to enable sophisticated home-based internal feline investigations profoundly. These localized feline interventions are positioned to unlock previously inaccessible veterinary care demographics completely.

Service Type Insights

Medical care is projected to dominate, holding approximately 69% share in 2026, driven by escalating preventative diagnostic priorities. Chronic disease management requirements are expected to establish rigorous, recurring, localized appointment schedules consistently. Aging companion animal demographics are anticipated to demand continuous, sophisticated, localized palliative interventions profoundly. Vetco Total Care with Mobile Clinic is likely to execute comprehensive regional vaccination campaigns.

Advanced miniaturized blood analysis technologies are set to empower immediate home-based diagnostic result generation. Petfolk with Petfolk Mobile Care is positioned to deliver unparalleled localized clinical excellence continuously. Vetster with Vetster App leads virtual-to-physical handoffs seamlessly. MobileVet with MobileVet Units excels in vaccine clinics, optimizing urban routes. Tech trends such as wearables bolster dominance through predictive alerts.

Grooming is anticipated to be the fastest-growing segment, driven by escalating premium humanization trend dynamics. Elaborate specialized breed styling preferences are projected to command substantial localized price premiums continually. Busy professional demographic lifestyles are expected to necessitate ultra-convenient residential aesthetic maintenance services reliably. Subscription models address recurring hygiene needs unmet by static salons effectively. Dial-a-Dog-Wash with Heated Hydrobath Van is likely to standardize elite aquatic cleaning methodologies significantly.

Chewy with Chewy Mobile Health ties kits to service fleets innovatively. Specialized anxiolytic handling techniques are set to differentiate premium localized operators from conventional salons. HydroDog with Big Blue Dog Van is positioned to leverage unmistakable visual branding strategies.

Regional Insights

North America Mobile Pet Care Market Trends

North America is expected to remain the leading regional market, accounting for approximately 40% share in 2026, supported by robust infrastructure. Affluent suburban demographic concentrations are projected to sustain premium localized service pricing models consistently. Widespread venture capital ecosystems are anticipated to accelerate sophisticated technological routing platform integrations profoundly. Aussie Pet Mobile with 150-Point Grooming Van is likely to maintain expansive regional fleets.

Comprehensive private pet insurance adoption is set to subsidize escalating preventative localized diagnostic expenditures. These formidable economic pillars are positioned to preserve unassailable regional industry leadership continuously today.

The U.S. is expected to function as the primary regional growth anchor globally. Progressive veterinary telemedicine legislation is projected to formalize comprehensive digital mobile care paradigms completely. The vets with at-home veterinary fleet are anticipated to scale aggressive national deployment strategies. Sprawling suburban architectural layouts are likely to necessitate heavy reliance on vehicular care delivery. Extensive private equity consolidation efforts are set to standardize fragmented independent regional fleet operations. This distinct regulatory environment is positioned to propel continuous operational market expansion efforts securely.

Asia Pacific Mobile Pet Care Market Trends

Asia Pacific is expected to register the fastest growth trajectory, as rapid urbanization expands incredibly profoundly and consistently. Unprecedented urban geographical densification is projected to strain traditional stationary clinical veterinary infrastructures profoundly. Aggressive localized digital platform integrations are anticipated to streamline sophisticated mobile service dispatch mechanisms. PetBacker with Pet Services App is likely to capture massive, unorganized regional market fragments.

Surging preventative healthcare awareness is set to drive initial mobile diagnostic adoption velocity metrics. These volatile demographic transformations are positioned to unlock unparalleled long-term industry expansion opportunities securely.

India shapes regional momentum via regulatory easing on doorstep care and rising disposable incomes in tier-1 cities. Industry structures emphasize app-first models for young owners. China is expected to shape the underlying regional acceleration momentum incredibly profoundly soon globally. Surging elite urban pet humanization is projected to fuel explosive, specialized, localized grooming demands. Comprehensive super-app ecosystem integrations are anticipated to monopolize regional client acquisition and scheduling channels.

PawSquad with Mobile Vet Network is likely to pilot aggressive, scalable urban deployment prototypes. Emerging governmental animal welfare initiatives are set to formalize historically fragmented regional and localized operations. This incredibly dynamic technological landscape is positioned to rewrite traditional global market penetration strategies.

Europe Mobile Pet Care Market Trends

Europe is expected to remain a mature and structurally stable regional market, with demand primarily anchored in premiumization. Sophisticated environmental emission standards are projected to force rapid localized electric vehicular fleet transitions. High urban residential densities are anticipated to complicate heavy commercial parking logistics for operators. FirstVet with the Digital Triage Platform is likely to dominate comprehensive regional digital health routing.

Elevated veterinary professional standards are set to mandate rigorous, specialized mobile practitioner credentialing processes. These entrenched structural characteristics are positioned to foster gradual premium-oriented market value increments consistently.

The U.K. is expected to serve as a critical regional stability anchor profoundly. Established companion animal humanization trends are projected to sustain continuous specialized preventative healthcare demands. Dial-a-Dog-Wash with Heated Hydrobath Van is anticipated to leverage extensive established national franchising networks. Stringent independent practitioner regulatory frameworks are likely to necessitate immense initial compliance capital expenditures.

Dense historic municipal architectures are set to prioritize compact agile vehicular deployment configurations exclusively. This rigorous operational environment is positioned to protect established localized market share fortresses consistently.

Competitive Landscape

The global mobile pet care market is expected to remain highly fragmented, continually driven by immense localized independent entrepreneurial operator participation. Dominant national entities are projected to leverage superior technological routing and sophisticated scheduling software. Unmatched procurement relationships are anticipated to grant massive structural capital advantages to capitalized networks.

Aussie Pet Mobile with 150-Point Grooming Van is likely to exemplify elite franchised standards. These formidable centralized organizations are positioned to shape aggregate long-term industry service quality expectations.

Aggressive vertical technological integration is expected to separate premium innovators from value-positioned independent competitors. Comprehensive digital health ecosystems are projected to construct insurmountable specialized client retention IP moats. Fuzzy with the Fuzzy Telehealth App is anticipated to pioneer seamless remote triage and dispatch. Sophisticated white-label software proliferation is set to empower smaller operators with advanced scheduling capabilities. This intensifying technological arms race is positioned to eradicate inefficient analogue localized service methodologies.

Key Industry Developments:

- In March 2026, Petco Health and Wellness Company announced plans to return to sales growth by prioritizing the expansion of its mobile vet and grooming offerings. By pivoting toward mobile services, Petco aims to leverage its 1,500+ physical locations as hubs for a growing fleet, directly challenging specialized mobile-only startups.

- In January 2026, GlocalMe debuted the PetPhone C-Plus Suite at CES, a rugged smartphone collar with a 1080p camera and two-way communication. This hardware enables mobile pet sitters and walkers to provide live, high-definition "adventure streams" to owners, increasing trust and transparency for remote services.

- In November 2025, Wag’n Tails introduced AI-based coat analyzers and digital skin assessment tools for its 2026 mobile grooming van models. These tools allow mobile groomers to detect early-stage dermatological issues, transforming a standard grooming appointment into a preventative health screening.

Companies Covered in Mobile Pet Care Market

- Chewy

- Rover

- Wag!

- Vetster

- Airvet

- Bond Vet

- BetterVet

- Vetco Total Care

- VIP Petcare

- PetDesk

- Pawp

- Modern Animal

- FirstVet

- BluePearl

- Fuzzy

Frequently Asked Questions

The mobile pet care market is estimated to be valued at approximately US$851.7 million in 2026 and is projected to reach around US$1,358.2 million by 2033, driven by the growing adoption of telemedicine services and increasing pet humanization trends.

Pet humanization fuels demand for convenient at-home services. Urban owners prioritize app-based mobile care. Telemedicine bridges virtual and physical delivery effectively.

The mobile pet care market is projected to grow at a CAGR of 6.9% from 2026 to 2033, supported by increasing adoption of pet insurance, expanding integration of digital technologies, and the growing use of sustainable mobile service fleets.

North America leads with approximately 40% share in 2026. Mature ecosystems and insurance drive dominance. Urban density optimizes fleet efficiency.

Key players in the market include Vetster (Vetster App), Airvet (Airvet Platform), and PetDesk (PetDesk Mobile), with Bond Vet (Bond Vet Van Service) and Pawp (Pawp Telehealth) also playing significant roles. These companies maintain a competitive edge through advancements in telehealth solutions and mobile service fleet innovations.