- Healthcare Services

- U.S. Mobile Physician Practice Market

U.S. Mobile Physician Practice Market Size, Share, and Growth Forecast, 2026 - 2033

U.S. Mobile Physician Practice Market by Product Type (Emergency Medicine, Telehealth), Services Type (Primary Care, Short-term Episodic Care, Others), End-user (Home Healthcare, Nursing Care, Others), and Zone Analysis for 2026 - 2033

U.S. Mobile Physician Practice Market Size and Trends Analysis

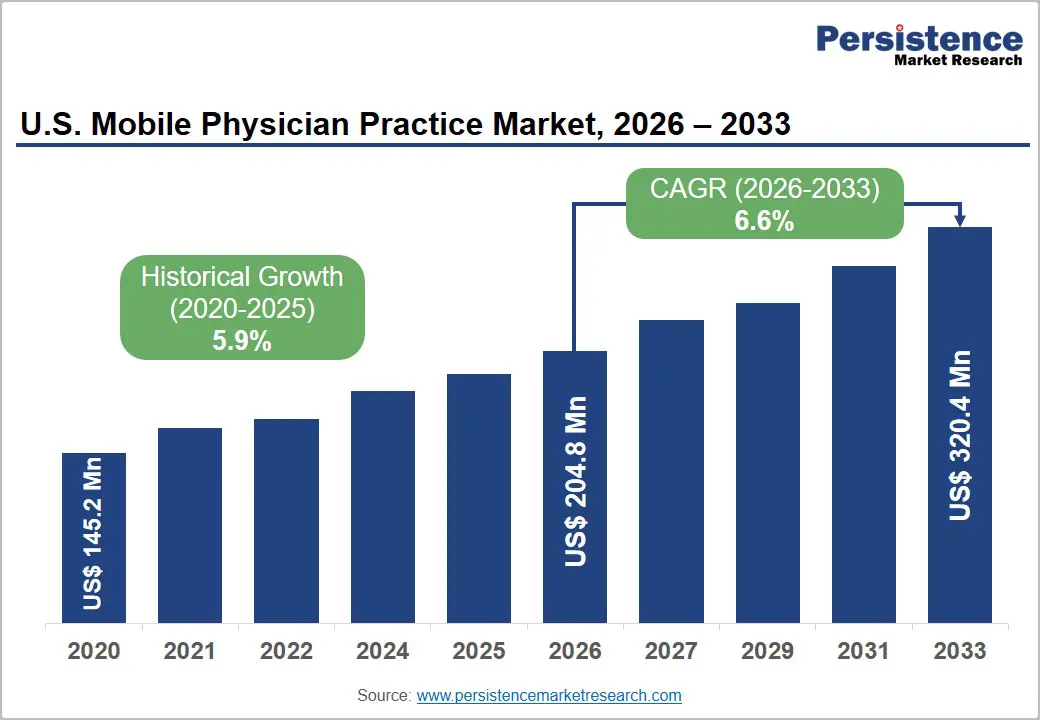

The U.S. mobile physician practice market size is likely to be valued at US$204.8 million in 2026 and is expected to reach US$320.4 million by 2033, growing at a CAGR of 6.6% during the forecast period from 2026 to 2033, driven by the shift toward home-based and value-based healthcare delivery.

Mobile physician practices provide primary, chronic, and urgent care services directly to patients in homes, assisted living facilities, and other community settings, improving access while reducing avoidable hospital utilization. Demand is supported by the nation's aging population and increasing prevalence of chronic diseases among older adults. Expanding telehealth reimbursement, remote patient monitoring adoption, and accountable care initiatives are accelerating market growth and care-at-home integration.

Key Industry Highlights:

- Leading Product Type: Emergency medicine is projected to represent the leading product type in 2026, accounting for 45% of the revenue share, driven by strong demand for urgent and on-site medical care.

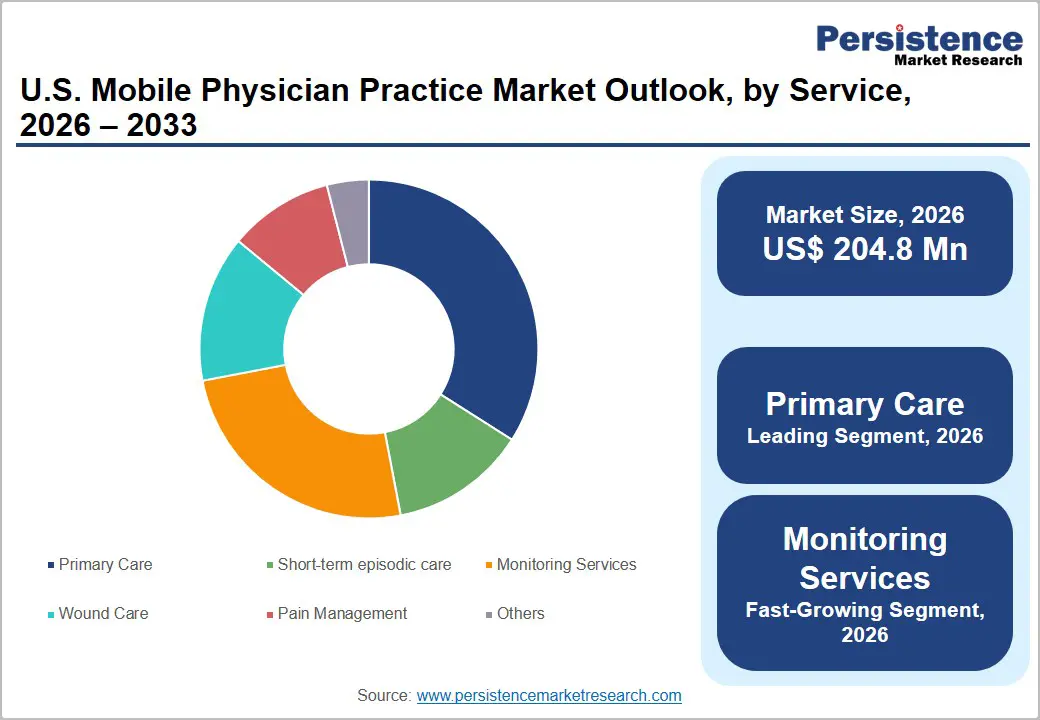

- Leading Services Type: Primary care is anticipated to be the leading services type, accounting for over 25% of the revenue share in 2026, owing to the increasing demand for preventive care, chronic disease management, and routine physician visits in home settings.

- Leading End-user: Home healthcare is projected to be the leading end-user segment in 2026, accounting for 50% of the market revenue, driven by increasing patient preference for receiving medical care in home settings and the growing aging population.

- Key Opportunity: The expanding demand for technology-enabled home-based healthcare presents a significant opportunity for mobile physician providers to deliver integrated primary, chronic, and preventive care through hybrid in-person and virtual care models across the U.S.

DRO Analysis

Driver - Technological Advancements and Telehealth Integration

Technological advancements and telehealth integration have become major growth drivers for the U.S. mobile physician practice market. Mobile physician providers increasingly utilize cloud-based electronic health records, artificial intelligence-assisted clinical documentation, remote patient monitoring devices, and secure telehealth platforms to deliver efficient care outside traditional healthcare facilities. These technologies allow physicians to assess patients remotely, monitor chronic conditions continuously, and coordinate treatment plans more effectively.

Enhanced connectivity between patients, caregivers, and healthcare professionals improves communication and clinical decision-making. As healthcare systems prioritize convenience, accessibility, and cost reduction, technology-enabled mobile physician services are becoming an essential component of modern healthcare delivery. The integration of telehealth with mobile physician services supports hybrid care models that combine virtual consultations with in-person visits when necessary.

This approach improves patient engagement, expands physician reach, and reduces unnecessary hospital admissions and emergency department utilization. Digital scheduling systems, mobile diagnostic tools, and wearable health monitoring devices strengthen care delivery capabilities in home-based settings. Growing acceptance of virtual healthcare among patients, providers, and payers has accelerated investment in digital infrastructure across the healthcare sector.

Restraint - Limited Rural Connectivity and Digital Divide

Many rural and underserved communities continue to experience inadequate broadband infrastructure, unreliable internet access, and limited availability of advanced communication technologies. Since telehealth platforms and remote monitoring systems depend heavily on stable connectivity, these limitations can restrict access to mobile physician services.

Patients living in remote regions face difficulties participating in virtual consultations, transmitting health data, or accessing digital healthcare resources. Healthcare providers often encounter operational challenges when attempting to deliver consistent and technology-enabled care across geographically dispersed populations. The digital divide also affects older adults, low-income households, and individuals with limited technological literacy.

Many patients may lack smartphones, computers, or the skills required to effectively utilize telehealth applications and remote monitoring tools. This can reduce patient engagement and hinder the effectiveness of hybrid care models. Healthcare organizations frequently need to invest additional resources in patient education, technical support, and alternative service delivery methods. Persistent disparities in digital access may slow market penetration in certain regions and populations.

Opportunity - Expansion of Hybrid Care Models and Medical Apps

Hybrid care combines virtual consultations, remote monitoring, and in-person physician visits to create a flexible and patient-centered healthcare experience. Mobile physician providers can leverage these models to serve larger patient populations while maintaining continuity of care. Medical applications enable appointment scheduling, medication reminders, symptom tracking, and secure communication between patients and healthcare professionals.

As consumers increasingly seek convenient healthcare solutions, digital platforms are becoming important tools for improving accessibility, patient satisfaction, and operational efficiency within mobile physician practices. Medical applications also create opportunities for enhanced chronic disease management, preventive care, and personalized treatment planning.

Through integration with wearable devices and remote monitoring systems, physicians can access real-time patient health information and intervene proactively when necessary. These capabilities support improved clinical outcomes and stronger patient engagement. Healthcare payers and providers are increasingly recognizing the value of hybrid care approaches in reducing healthcare costs and avoiding unnecessary hospital utilization.

Category-wise Analysis

Product Type Insights

Emergency medicine is expected to lead the U.S mobile physician practice market, accounting for approximately 45% of revenue in 2026, driven by the growing need for immediate medical intervention outside traditional hospital settings. Mobile emergency physician services are increasingly utilized for urgent care needs, post-discharge complications, acute illness management, and emergency evaluations in residential and community-based environments. A notable example includes TeamHealth, which provides mobile and urgent physician services through extensive clinical networks, enabling timely emergency-focused care in multiple community settings.

Telehealth is likely to represent the fastest-growing segment in 2026, supported by widespread digital health adoption, favorable reimbursement policies, and increasing consumer acceptance of virtual healthcare services. Mobile physician providers are increasingly integrating telehealth platforms into their service models to improve patient access, support chronic disease management, and enhance continuity of care. For example, Doctor On Demand by Included Health, which combines virtual physician consultations with broader care coordination services.

Services Type Insights

Primary care is projected to lead the market, capturing around 25% of the revenue share in 2026, supported by its essential role in preventive healthcare, chronic disease management, and routine medical services. Mobile primary care physicians deliver comprehensive care directly to patients in homes, assisted living facilities, and community-based settings, improving accessibility while reducing healthcare system burdens. For instance, Mobile Physician Services, Inc., which specializes in bringing primary healthcare directly to patients who have difficulty accessing conventional healthcare facilities. Its patient-centered approach reflects the broader market trend toward convenient and personalized home-based medical care.

Monitoring services are likely to be the fastest-growing service type in 2026, driven by increasing adoption of remote patient monitoring technologies and growing emphasis on proactive healthcare management. These services enable physicians to continuously track patient health indicators, identify early warning signs, and intervene before conditions worsen. Monitoring services align closely with value-based care initiatives that focus on preventing hospital admissions and reducing healthcare expenditures. A notable example includes PriveMD, which incorporates technology-enabled care coordination and patient monitoring as part of its physician-led healthcare delivery approach.

End-user Insights

Home healthcare is estimated to lead the U.S. mobile physician practice market, accounting for approximately 50% of revenue in 2026, due to strong patient preference for receiving medical care in familiar residential environments. The segment benefits from demographic trends, including population aging and increasing prevalence of chronic diseases requiring ongoing physician oversight. Mobile physician practices support home healthcare by delivering routine examinations, chronic disease management, medication reviews, and post-hospitalization follow-up services directly to patients. For example, Florida Mobile Physicians, LLC, which provides physician-led medical services to homebound and elderly patients throughout residential care settings.

Assisted living facilities are likely to represent the fastest-growing segment in 2026, driven by increasing collaboration between facility operators and mobile healthcare providers. These facilities house large populations of older adults who require ongoing medical supervision, chronic disease management, and preventive healthcare services. Mobile physician practices provide convenient on-site medical care, reducing the need for external appointments and minimizing disruptions for residents. For instance, SOS Doctor Housecall, which offers physician services that can support residents in assisted living and similar long-term care environments.

Competitive Landscape

The U.S. mobile physician practice market exhibits a moderately fragmented structure, driven by the presence of specialized mobile healthcare providers, telehealth companies, physician house-call networks, and integrated care organizations expanding home-based medical services. Market growth is being supported by increasing demand for physician-led care in residential settings, rising adoption of value-based healthcare models, and the growing need to manage chronic conditions outside traditional hospitals and clinics.

With key leaders, including Mobile Physician Services, Inc., TeamHealth, Doctor On Demand by Included Health, Inc., Florida Mobile Physicians, LLC, and SOS Doctor Housecall, competitive intensity continues to increase. These players compete through geographic expansion, telehealth integration, enhanced patient engagement capabilities, physician network development, and comprehensive home-based care offerings.

Key Industry Developments:

- In May 2026, Wellgistics Health, Inc. entered a pilot collaboration with Kare PharmTech and Kare Clinicals to expand chronic care management (CCM) and remote patient monitoring (RPM) services across provider networks, supporting the growing shift toward value-based and home-based physician care models.

- In May 2025, Apollo Home Healthcare launched its “Doctor at Home in 90 Minutes” service, enabling rapid physician consultations at patients’ homes through a technology-enabled logistics network. The initiative highlights the growing adoption of on-demand physician house-call models and home-based healthcare services.

- In December 2025, Included Health, Inc. announced the launch of “Dot,” an AI-powered personal health assistant designed to provide personalized healthcare guidance, support physician visits, answer benefits-related questions, and improve care coordination. The development strengthens hybrid care delivery and enhances virtual physician engagement capabilities within the mobile healthcare ecosystem.

Companies Covered in U.S. Mobile Physician Practice Market

- Mobile Physician Services, Inc.

- TeamHealth

- Doctor on Demand by Included Health, Inc.

- Florida Mobile Physicians, LLC

- PriveMD

- PatientPop, Inc.

- SOS Doctor Housecall

Frequently Asked Questions

The U.S. mobile physician practice market is projected to reach US$204.8 million in 2026.

The U.S. mobile physician practice market is driven by the growing aging population, rising prevalence of chronic diseases, and increasing adoption of telehealth-enabled home-based healthcare services.

The U.S. mobile physician practice market is expected to grow at a CAGR of 6.6% from 2026 to 2033.

Key opportunities lie in the expansion of hybrid care models, remote patient monitoring solutions, and mobile health applications that enhance physician-led home healthcare delivery.

Mobile Physician Services, Inc, TeamHealth, Florida Mobile Physicians, PriveMD, and PatientPop, Inc. are the leading players.