- Retail

- Mobile Fuel Delivery Market

Mobile Fuel Delivery Market Size, Share, and Growth Forecast, 2026 - 2033

Mobile Fuel Delivery Market by Product Type (Gasoline, Diesel, CNG, LNG), Service Type (On-Demand, Subscription), End-Use (Commercial, Industrial, Residential), and Regional Analysis for 2026-2033

Mobile Fuel Delivery Market Share and Trends Analysis

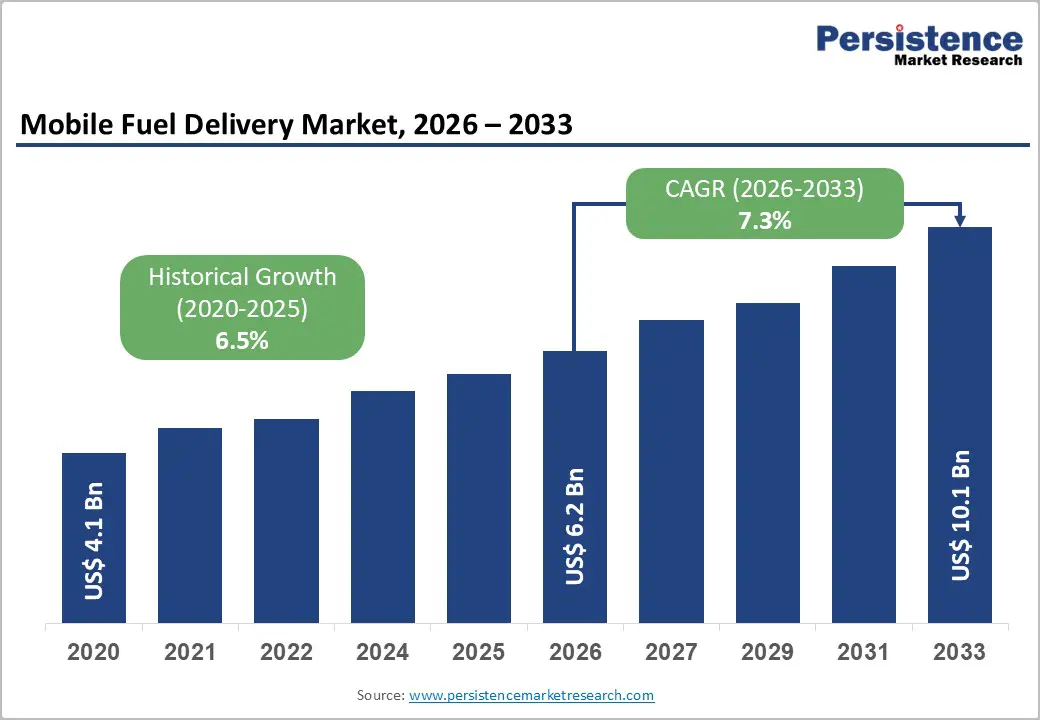

The global mobile fuel delivery market size is likely to be valued at US$ 6.2 billion in 2026, and is projected to reach US$ 10.1 billion by 2033, growing at a CAGR of 7.3% during the forecast period 2026−2033. Market expansion is being driven by rising demand for convenient, on-demand fuel delivery services, particularly among commercial fleet operators and consumers with time-sensitive mobility needs.

Businesses are increasingly prioritizing operational efficiency and downtime reduction, which is supporting the shift toward off-site refueling solutions. The growing penetration of digital platforms is continuing to reshape traditional fuel distribution models by enabling real-time ordering, route optimization, and transaction transparency through smartphone-based applications. Accelerating urbanization and evolving regulatory frameworks are reinforcing long-term adoption trends. Dense urban environments are increasing the value of last-mile fuel delivery by reducing congestion-related inefficiencies associated with conventional refueling. Environmental regulations are also promoting improved fuel management, emissions monitoring, and spill prevention, thereby encouraging the development of controlled, technology-enabled delivery models. Adoption is therefore expanding across both business-to-business and business-to-consumer segments, with fleet operators, construction sites, and emergency services acting as early adopters. As digital logistics capabilities mature and regulatory clarity improves, mobile fuel delivery is expected to become an increasingly embedded component of urban and commercial fuel supply chains.

Key Industry Highlights

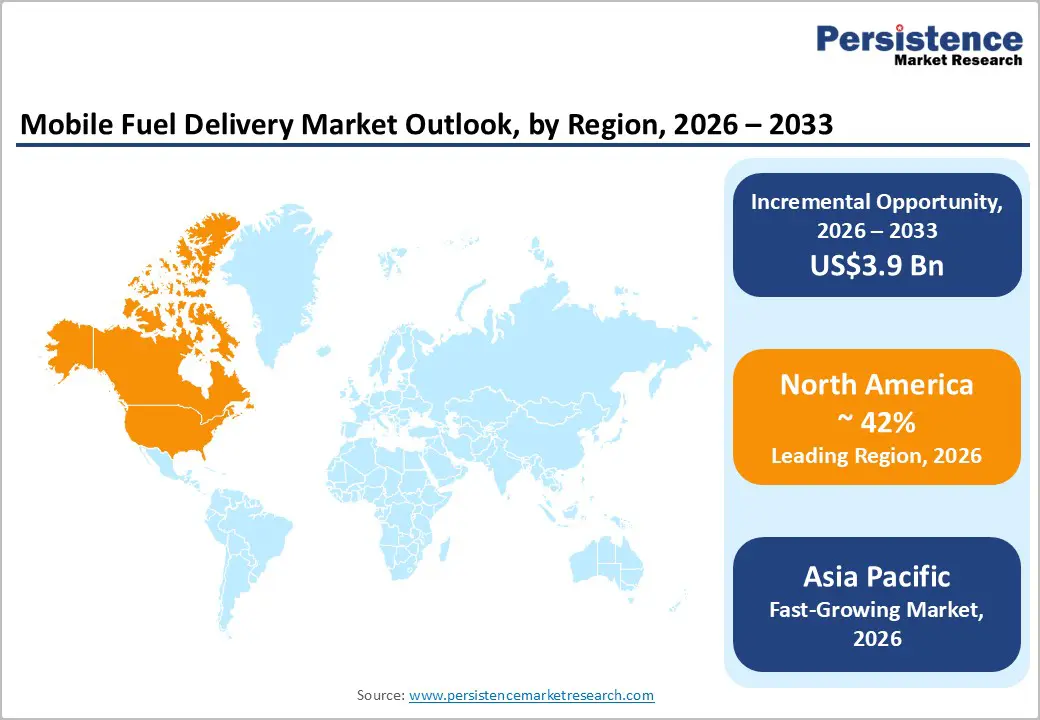

- Dominant Region: North America is expected to account for about 42% of the market in 2026, supported by extensive commercial transportation networks and a mature on-demand service economy.

- Fastest-growing Market: The Asia Pacific market is slated to be the fastest-growing between 2026 and 2033, fueled by rapid logistics infrastructure expansion.

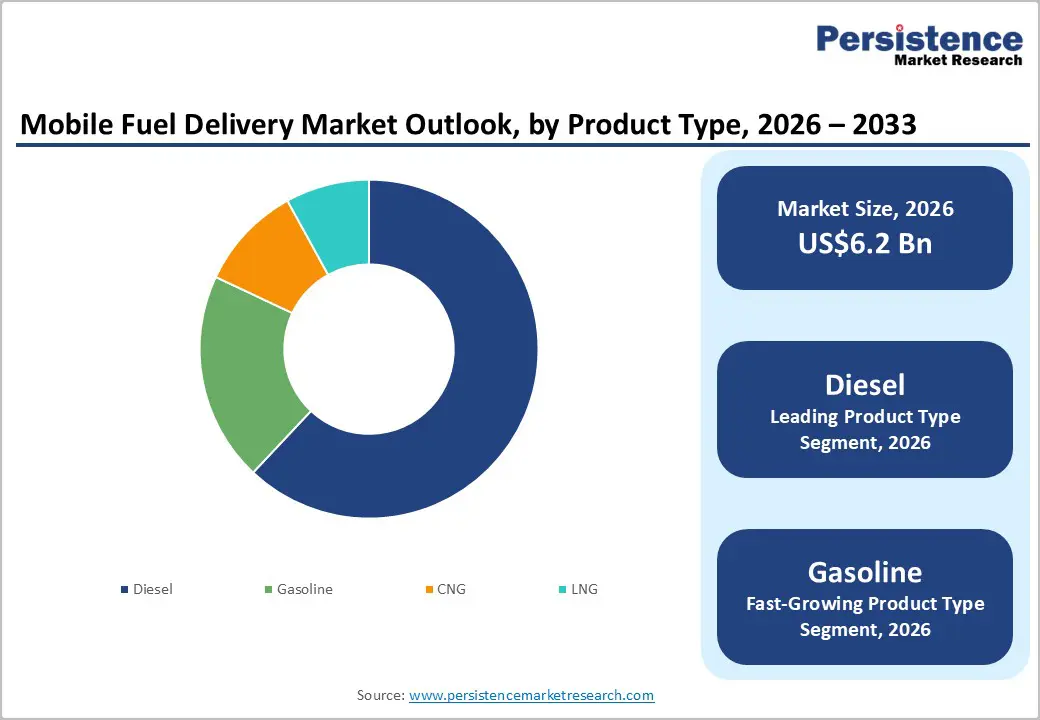

- Leading & Fastest-growing Product Type: Diesel is set to dominate, with an estimated 62% revenue share in 2026, while gasoline is likely to be the fastest-growing segment over the 2026-2033 forecast period.

- Leading & Fastest-growing Service Type: On-demand services are projected to account for approximately 65% of revenue in 2026, with subscription services recording the highest 2026-2033 CAGR.

- Key Driver: The global shift toward on-demand economy models is widening the adoption of mobile fuel delivery services, aiding market growth.

- October 2025: Anytime Diesel launched as Hyderabad's first government-authorized app for free doorstep diesel delivery via GPS-tracked, IoT-sealed trucks for vehicles/generators.

| Key Insights | Details |

|---|---|

| Mobile Fuel Delivery Market Size (2026E) | US$ 6.2 Bn |

| Market Value Forecast (2033F) | US$ 10.1 Bn |

| Projected Growth (CAGR 2026 to 2033) | 7.3% |

| Historical Market Growth (CAGR 2020 to 2025) | 6.5% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Shifting Preference for On-Demand Convenience Services

The global shift toward on-demand economy models is driving the adoption of mobile fuel delivery services across both commercial and consumer segments. Working professionals are facing increasing time constraints and actively seek solutions to reduce nonproductive activities in daily operations. Commercial fleet operators are increasingly prioritizing mobile fuel delivery to improve utilization rates across large vehicle networks, particularly in North America and Europe. Fleet management associations consistently highlight the scale of these fleets and reinforce the need for more streamlined, predictable refueling processes that minimize disruption to core transport and service activities.

Mobile fuel delivery services are directly eliminating downtime associated with traditional refueling at fixed stations and are enabling measurable productivity gains for operators. Service providers are increasingly integrating Global Positioning System (GPS) tracking and advanced route optimization tools to ensure timely delivery within narrow operational windows. This capability supports just-in-time fuel supply for sectors such as construction, logistics, and emergency response, where vehicle availability is critical to mission success. Businesses are gaining a strategic advantage by aligning fuel supply with operational rhythms, reducing idle time, and reallocating labor and capital toward higher-value activities. As competitive pressure intensifies, forward-looking organizations are increasingly viewing mobile fuel delivery as a foundational component of modern, efficiency-driven operational infrastructure rather than a discretionary convenience.

Capital Intensity and Fleet Infrastructure Investment

Mobile fuel delivery operations require substantial upfront capital to acquire specialized equipment and develop the fleet. Purpose-built vehicles feature U.S. Department of Transportation (DOT)-certified tanks, advanced safety systems, and precise metering technology. Operators invest heavily in these assets to ensure compliance and operational reliability. Urban market coverage demands coordinated fleets that achieve adequate service density. Service providers face ongoing working capital demands to finance fuel inventory across multiple locations. These financial requirements shape market entry dynamics and influence long-term competitive positioning.

Well-capitalized companies gain clear advantages in this capital-intensive environment. They scale operations efficiently and capture economies that drive sustainable profitability. Smaller independent operators face persistent challenges to match these scale benefits. Market consolidation accelerates as larger players acquire regional competitors to expand geographic footprints. Strategic investors recognize established operators as attractive acquisition targets due to their proven operational models and customer relationships. Entrants prioritize partnerships with equipment financiers or adopt asset-light models through third-party fleet leasing arrangements. Business leaders carefully assess capital structure to balance growth ambitions with financial risk exposure in this maturing industry sector.

Growing Emphasis on Sustainability and Alternative Fuels

A key opportunity in the mobile fuel delivery market centers on sustainability-focused services and the expanding adoption of alternative fuels. Rising environmental awareness is prompting businesses and consumers to prioritize cleaner energy options such as compressed natural gas (CNG), liquefied natural gas (LNG), and biofuels, which are supporting emissions reduction while aligning with tightening regulatory requirements. Mobile fuel delivery providers are increasingly positioning themselves strategically by expanding service portfolios beyond conventional petroleum products. This shift is enabling providers to address growing demand from fleet operators, construction companies, and industrial clients that are actively pursuing corporate sustainability targets and compliance with environmental standards.

Service providers are strengthening their competitive differentiation by offering a range of fuel options that align with customers' decarbonization strategies. Environmentally conscious clients are increasingly favoring suppliers that support green initiatives and provide measurable emissions benefits. Companies are integrating alternative fuel delivery into existing logistics platforms to capture premium pricing, improve customer retention, and build long-term partnerships with organizations committed to net-zero pathways. Electric vehicle (EV) charging integration is simultaneously emerging as a complementary growth avenue. Rapid EV adoption is creating infrastructure gaps that mobile services are increasingly filling through on-demand charging solutions. This convergence is enabling providers to develop integrated mobility ecosystems that serve mixed fleets and support a broader transition toward low-emission transport models.

Category-wise Analysis

Fuel Type Insights

Diesel is slated to maintain a dominant position in the market, with an estimated 2026 share exceeding 62%. Heavy commercial vehicles rely on diesel for its superior energy density and operational efficiency. Expanding industrial operations and construction projects worldwide drive sustained demand for reliable diesel supply. Mobile delivery services are essential in remote locations and on active construction sites, where traditional fuel stations remain scarce. Operators prioritize diesel delivery to support uninterrupted project timelines and equipment utilization. This segment maintains structural demand advantages that reinforce its market leadership position.

Gasoline is likely to be the fastest-growing segment during the 2026-2033 forecast period. Passenger vehicles and light commercial fleets depend on gasoline for everyday operations. Operators favor this fuel type due to its convenience and extensive existing infrastructure. Gasoline-powered vehicles form the backbone of global transportation networks, which sustains steady delivery requirements. Mobile services leverage established supply chains to efficiently serve urban consumers and small-business fleets. This segment benefits from unmatched market penetration and predictable consumption patterns, reinforcing its dominant position.

Service Type Insights

On-demand services are likely to hold the largest share of the mobile fuel delivery market, estimated to reach 65% in 2026. This segment drives the popularity of mobile fuel delivery through unmatched flexibility and customer convenience. Users request fuel exactly when needed, which suits individual drivers and commercial operations equally well. App-based platforms and refined logistics systems enhance accessibility across diverse customer segments. These services eliminate scheduling constraints and align delivery timing with actual operational requirements. Businesses and consumers alike value the responsiveness that transforms fuel procurement into seamless background operations. This segment captures premium positioning through superior user experience and operational alignment.

Subscription services are expected to be the fastest-growing segment during the 2026-2033 forecast period. These services are gaining strong traction among businesses managing large fleets. Subscription models deliver scheduled fuel supplies that keep vehicles refueled and operational continuously. Companies achieve cost control and efficiency gains through precise fuel consumption management. Predictable delivery patterns enable superior inventory planning and budgeting accuracy. Fleet operators favor subscriptions for their reliability and alignment with operational cycles. This segment appeals to enterprises seeking consistent performance without procurement disruptions.

End-Use Insights

The commercial segment is currently expected to dominate with an approximate 68% of the mobile fuel delivery market share in 2026, driven by intensive fuel needs across logistics, transportation, and fleet management sectors. Mobile fuel delivery addresses critical operational priorities by minimizing vehicle downtime and maximizing equipment utilization. Businesses streamline fuel procurement processes to enhance overall efficiency. Operators reduce idle periods that erode productivity while gaining precise control over consumption patterns. This segment reflects structural demand from enterprises prioritizing continuous operations over traditional refueling constraints. Companies achieve measurable performance improvements through integrated delivery solutions tailored to commercial scale requirements.

The industrial segment is expected to post the highest CAGR for the 2026-2033 forecast period. The industrial segment relies heavily on mobile fuel delivery to power equipment and machinery at construction sites, mining operations, and remote facilities. These services guarantee an uninterrupted fuel supply to locations beyond traditional station reach. Operators maintain project timelines through consistent energy availability in challenging environments. Expanding infrastructure projects and industrial expansion worldwide sustain a strong demand for this delivery model. Businesses eliminate logistical disruptions that threaten operational continuity.

Regional Insights

North America Mobile Fuel Delivery Market Trends

North America is expected to command the lion’s share of the mobile fuel delivery market, accounting for approximately 42% of global revenue in 2026. The United States is anchoring regional strength through its extensive commercial transportation networks and a well-established on-demand service economy. High smartphone penetration and advanced digital payment platforms are enabling seamless customer engagement and more efficient transactions. Mature logistics systems are enabling rapid service scaling across major urban centers, while fleet operators benefit from established infrastructure that facilitates efficient delivery coordination. Regulatory oversight from the DOT is providing consistent nationwide standards for hazardous materials handling, while state-level environmental regulations and fire codes are continuing to define localized compliance requirements. This regulatory structure is enabling controlled market expansion while maintaining safety and operational discipline.

The market in North America features balanced dynamics, with several significant operators typically active within each metropolitan area. This structure is avoiding monopolistic concentration while continuing to reward providers that demonstrate superior execution, reliability, and route efficiency. Operators are achieving margin stability by optimizing delivery density, leveraging data analytics, and maintaining strong compliance frameworks, rather than relying on aggressive pricing strategies. Strategic expansion is increasingly focusing on extending network coverage into secondary cities to complement core urban markets. These regional advantages are positioning North American mobile fuel delivery providers for international expansion as other markets gradually adopt similar digital, regulatory, and operational frameworks.

Europe Mobile Fuel Delivery Market Trends

Europe maintains a strong position in the market for mobile fuel delivery through 2033. Germany leads regional adoption through its robust logistics networks and advanced manufacturing infrastructure. Dense demand clusters emerge around key industrial regions and major transportation hubs. The United Kingdom achieves solid urban penetration, with congestion charges and emission zones encouraging fleet optimization. France generates rural demand through its extensive agricultural operations, which require reliable fuel access for equipment fleets. Spain presents growth potential through tourism-driven transportation needs in coastal areas and metropolitan centers.

European Union (EU) regulatory frameworks create operational consistency across member states. The Agreement concerning the International Carriage of Dangerous Goods by Road (ADR) standards and alternative fuels infrastructure directives simplify multi-country expansion for operators. National variations in environmental rules, fuel quality requirements, and safety certifications demand ongoing adaptation. The European Green Deal accelerates corporate decarbonization, prompting providers to expand renewable diesel and biofuel offerings to meet sustainability targets. Private equity firms pursue consolidation strategies to build pan-European service platforms.

Asia Pacific Mobile Fuel Delivery Market Trends

Asia-Pacific is projected to be the fastest-growing market for mobile fuel delivery from 2026 to 2033, driven by expanding commercial vehicle fleets and the rapid development of logistics infrastructure. China is continuing to dominate regional growth due to its extensive freight and delivery networks and its position as the world’s largest e-commerce market, which is generating sustained demand for efficient and time-sensitive fuel supply solutions. Japan is demonstrating more mature adoption patterns, where mobile fuel delivery services are increasingly integrated into comprehensive fleet management platforms. Corporate clients in Japan are prioritizing service reliability, delivery precision, and quality assurance, which is supporting acceptance of premium pricing models. India offers significant expansion potential, as commercial vehicle volumes are rising and conventional refueling infrastructure remains limited in secondary and tertiary cities.

Regional trade integration is further strengthening the development of the logistics sector across Asia-Pacific economies. Manufacturing scale and localized equipment production are supporting competitive cost structures and operational efficiency for service providers. Regulatory environments vary widely across countries, which requires flexible and market-specific operating models. Singapore and South Korea are providing clear and standardized compliance frameworks that support faster deployment, while markets such as Indonesia and India require localized licensing, safety protocols, and stakeholder coordination. Technology partnerships are accelerating across the region as regional operators collaborate with global logistics platforms to enhance routing, payment systems, and data analytics. Investment from Japanese trading houses, Chinese technology firms, and Southeast Asian conglomerates is continuing to strengthen platform development, positioning Asia Pacific as a long-term growth engine for mobile fuel delivery services.

Competitive Landscape

The global mobile fuel delivery market structure is characterized by moderate fragmentation. Top players such as Booster, Yoshi, Filld, WeFuel, and FuelGenie collectively account for approximately two-fifths of the total market share. Competitive intensity is being shaped by providers that are actively expanding geographic coverage, strengthening service reliability, and improving operational efficiency. Market leaders are investing consistently in technology-enabled service models to scale operations while maintaining safety and compliance standards. Competition is therefore shifting away from basic availability toward execution quality, customer experience, and operational discipline across business-to-business and business-to-consumer segments.

Technology adoption is increasingly defining competitive differentiation within the market. Leading operators are integrating advanced solutions such as IoT, AI, and blockchain-based platforms to enhance service precision and transparency. Data analytics supports predictive maintenance, demand forecasting, and route optimization, improving asset utilization and reducing delivery delays. Real-time inventory tracking is strengthening supply reliability and lowering operational risk for customers. These capabilities enable premium providers to offer guaranteed service windows and seamless digital interfaces, reinforcing their pricing power. As a result, strategic technology investment is becoming a key driver of defensible market positioning and long-term profitability in the mobile fuel delivery market.

Key Industry Developments

- In December 2025, Amazon UAE partnered with CAFU to offer Prime members 12 months of free fuel delivery subscription, enabling two standard and five overnight monthly deliveries for one vehicle at chosen locations such as parking areas or offices in Dubai.

- In October 2025, Vexxil Energy, a Gulf Coast fuel distributor, acquired Direct Fuel Transport (DFT) and McGuire Oil Company (MOCO), gaining one of the region's largest fuel transport fleets and expanding same-day delivery capabilities across new markets for industries like construction, utilities, and maritime.

- In September 2025, FuelBuddy launched operations in Zimbabwe and Zambia post-success in India, UAE, and Mozambique, offering digital doorstep fuel delivery for mining, agriculture, logistics, and construction amid Africa's 30% energy demand surge by 2040.

Companies Covered in Mobile Fuel Delivery Market

- Booster

- Yoshi, Inc.

- Filld

- WeFuel

- Cafu

- GOFLO

- MyFuelDirect

- EZFill Holdings

- Zebra Fuel

- FuelGenie

- TekFluid

- GasNinjas

Frequently Asked Questions

The global mobile fuel delivery market is projected to reach US$ 6.2 billion in 2026.

Fleet efficiency demands, urbanization pressures, and digital platform integration accelerate adoption across commercial and residential segments are driving the market.

The market is poised to witness a CAGR of 7.3% from 2026 to 2033.

Sustainability-focused alternative fuels, emerging Asia-Pacific growth, and electric vehicle charging integration are creating substantial expansion potential.

Booster, Yoshi, Filld, WeFuel, and FuelGenie are some of the key players in the market.