- Electric Mobility

- Micro Mobility Market

Micro Mobility Market Size, Share, and Growth Forecast 2026 - 2033

Micro Mobility Market by Vehicle Type (Bicycles, E-Bikes, E-Scooters / Electric Kick Scooters, Electric Skateboards / Hoverboards, Golf Carts, Quadricycles), Propulsion Type (Battery Electric Vehicles (BEVs), Pedal-Assist/Hybrid Electric, Fully Human-Powered), Sharing Type (Docked Sharing Systems, Dockless Sharing Systems, Hybrid Sharing Systems, Personal Ownership), End-user, and Regional Analysis, 2026 - 2033

Micro Mobility Market Size and Trend Analysis

The global micro mobility market size is expected to be valued at US$ 52.5 billion in 2026 and projected to reach US$ 150.9 billion by 2033, growing at a CAGR of 16.3% between 2026 and 2033. The market is propelled by accelerated urbanization, rapid electrification of last-mile transport, and supportive municipal regulation favoring lower-emission travel modes.

According to the International Energy Agency (IEA), electric two- and three-wheelers already outpace passenger EV adoption in unit terms globally, while UN-Habitat reports that 56% of the world population now lives in cities, intensifying demand for compact, congestion-free transit. Subsidies under the European Green Deal and India's FAME-II scheme further reinforce procurement pipelines across both shared-fleet operators and private buyers.

DRO Analysis

Drivers - Urban Congestion and Emission Mandates Reshape Last-Mile Travel

Heavy traffic congestion and tightening emission rules in dense metropolitan zones are pushing commuters toward compact electric mobility. The European Environment Agency (EEA) confirms that road transport contributes nearly 23% of total greenhouse gas emissions in the EU, prompting cities such as Paris, Madrid, and Milan to enforce low-emission zones. Data from INRIX shows London commuters lost 99 hours in 2024 to congestion, equating to a productivity cost of GBP 1,082 per driver. Such structural inefficiencies are accelerating the uptake of e-bikes and e-scooters as practical alternatives, especially for trips under five kilometers.

Battery Cost Reductions Enable Mass-Market Affordability

Sharp declines in lithium-ion battery prices are unlocking new affordability tiers across the micro mobility ecosystem. According to BloombergNEF, lithium-ion pack prices fell to US$ 115/kWh in 2024, down nearly 20% year-on-year, with cell-only prices below US$ 80/kWh. This reduction translates directly into lower retail prices for e-bikes and electric kick scooters, broadening consumer reach in price-sensitive economies. Manufacturers are simultaneously deploying LFP chemistries that improve cycle life beyond 3,000 cycles, enhancing fleet economics for shared-mobility operators. The combined effect is shorter payback periods and stronger total-cost-of-ownership advantages versus internal combustion two-wheelers.

Restraints - Fragmented Regulatory Frameworks Restrict Cross-Border Scaling

Inconsistent rules around speed limits, helmet usage, parking, and licensing remain a major bottleneck for operators seeking continental scale. The European Transport Safety Council (ETSC) documented that e-scooter speed caps vary from 20 km/h in Germany to 25 km/h in France, with several Italian cities outright banning rentals after a 13% jump in pedestrian-involved incidents. Such regulatory mosaics inflate compliance overheads and force fleet redesigns market by market, weighing on profitability for shared-service providers.

Safety Concerns and Insurance Gaps Limit User Confidence

Persistent safety concerns continue to dampen broader consumer adoption. The U.S. Consumer Product Safety Commission (CPSC) reported 360,000 emergency-room visits related to micro mobility devices between 2017 and 2022, with annual injuries climbing 21% on average. Insurance products specific to e-scooter and e-bike use remain underdeveloped in many jurisdictions, leaving riders exposed to liability. These factors discourage first-time users and elevate operating risk for fleet managers, slowing penetration in suburban and tier-2 markets.

Opportunities - Battery-Swapping Networks for Commercial Delivery Fleets

Last-mile logistics is emerging as a high-yield opportunity zone for micro mobility manufacturers and infrastructure providers. The International Post Corporation (IPC) notes that global parcel volumes surpassed 161 billion items in 2023, with last-mile costs accounting for over 53% of total delivery expenses. Battery-swapping networks pioneered by firms like Gogoro in Taiwan and Sun Mobility in India eliminate downtime for commercial e-bike and e-scooter fleets serving Amazon, Zomato, and Deliveroo. With swap stations costing a fraction of fast-charging hubs, scalable rollouts represent a substantial commercial pipeline through 2033.

E-Bike Tourism and Corporate Campus Programs

Tourism-led leisure cycling and structured corporate-campus mobility programs are opening fresh revenue pockets. According to the European Cyclists' Federation (ECF), cycling tourism contributes more than EUR 44 billion annually to the European economy, with e-bike rentals being the fastest-expanding segment. Simultaneously, large enterprises such as Google, Microsoft, and Infosys have deployed campus e-bike and e-scooter fleets to cut intra-site commute times by up to 40%. Public-private partnerships under EU CEF Transport funding are further subsidizing greenway infrastructure, creating a long-tailed opportunity for OEMs supplying purpose-built tourism and corporate models.

Category-wise Analysis

Vehicle Type Insights

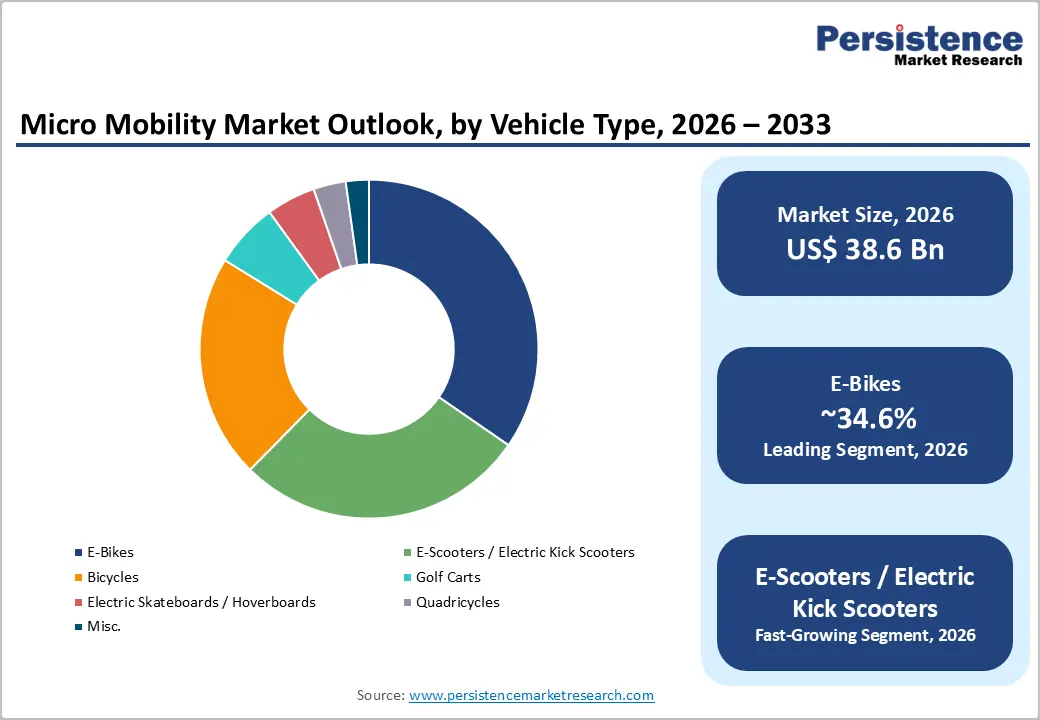

E-Bikes lead the global vehicle-type category with an estimated 35% market share in 2025. Their dominance reflects superior practicality for daily commuting distances of 5-15 km, regulatory acceptance across mature markets, and broad demographic reach spanning students to senior citizens.

According to Eurostat, e-bike sales in the EU exceeded 5 million units in 2023, outpacing conventional bicycles for the third consecutive year. Tax-incentive programs such as Germany's Dienstrad-Leasing and France's Bonus Velo have institutionalized purchases. Combined with rising health-consciousness and dense charging-free usage profiles, e-bikes are entrenched as the structural backbone of the micro mobility ecosystem.

Propulsion Type Insights

Battery Electric Vehicles (BEVs) hold the leading position in the propulsion-type category with a market share of approximately 58% in 2025. Pure-electric architectures dominate due to falling battery costs, simplified drivetrains, and consumer preference for zero-emission travel.

The International Energy Agency (IEA) reports that electric two- and three-wheelers represent over 60% of all electric vehicles in operation globally, with China alone hosting more than 350 million units. Improvements in motor efficiency, regenerative braking, and modular battery packs have made BEV-based scooters and e-bikes the default choice for shared-fleet operators worldwide. Emission-free operation also aligns directly with municipal procurement requirements under various clean-air programs.

End-user Insights

Individual Consumers represent the leading end-user segment, accounting for approximately 55% of global demand in 2025. The segment is anchored by daily commuters, students, and lifestyle riders prioritizing flexibility, cost savings, and emission-free travel.

According to the U.S. Bureau of Transportation Statistics, more than 60% of all urban trips are under 5 miles, a sweet spot for personal e-bikes and kick scooters. OECD surveys also reveal that 47% of millennials in advanced economies prefer non-car options for short trips. Backed by accessible retail financing from Klarna and Affirm, individual consumers will remain the central revenue driver.

Regional Insights

North America Micro Mobility Market Trends and Insights

North America holds a share of 20.7% in 2026, supported by structured city-level pilot programs in New York, Austin, and Los Angeles, and accelerated retail expansion through specialty bike chains and big-box channels. According to the U.S. Department of Transportation, over 230 cities operate active shared-mobility programs, while a maturing aftermarket and improving cycling infrastructure support strong replacement-cycle demand from urban commuters.

U.S. Micro Mobility Market Size

The U.S. Micro Mobility market size is likely to reach at US$ 9.3 Bbllion in 2026, driven by federal-state subsidies under the Bipartisan Infrastructure Law, which earmarks US$ 1.4 billion for active-transportation projects. The U.S. Bureau of Transportation Statistics confirms over 157 million annual shared-micro-mobility trips, with e-bike units sold growing nearly 20% year-on-year as Class-3 commuter models gain office-going adoption.

Europe Micro Mobility Market Trends and Insights

Europe holds a share of 28.6% in 2025, driven by a deeply embedded cycling culture, expanding low-emission zones, and structural funding under the European Green Deal. Eurostat data shows e-bike sales surpassed conventional bicycle sales in Germany, the Netherlands, and Belgium by 2024, while shared-scooter operators are progressively shifting toward swappable-battery fleets to comply with municipal sustainability mandates.

Germany Micro Mobility Market Size

Germany's Micro Mobility market size is likely to reach US$ 2.9 billion in 2026, propelled by the Dienstrad-Leasing salary-sacrifice scheme covering more than 1.5 million employees, and a national e-bike fleet exceeding 11 million units per the Zweirad-Industrie-Verband (ZIV). Robust cycling infrastructure spanning 100,000 km of bike paths, plus stringent low-emission-zone policies in 80 cities, sustains demand momentum across personal and corporate fleet ownership.

U.K. Micro Mobility Market Size

The U.K. Micro Mobility market size is poised to reach US$ 2.1 billion in 2026, supported by the Cycle to Work scheme benefiting over 1.6 million participants since inception, and an extended national e-scooter rental trial covering 30+ cities, per Transport for London. London's Ultra Low Emission Zone (ULEZ) expansion has driven a 26% jump in commuter e-bike registrations during 2024.

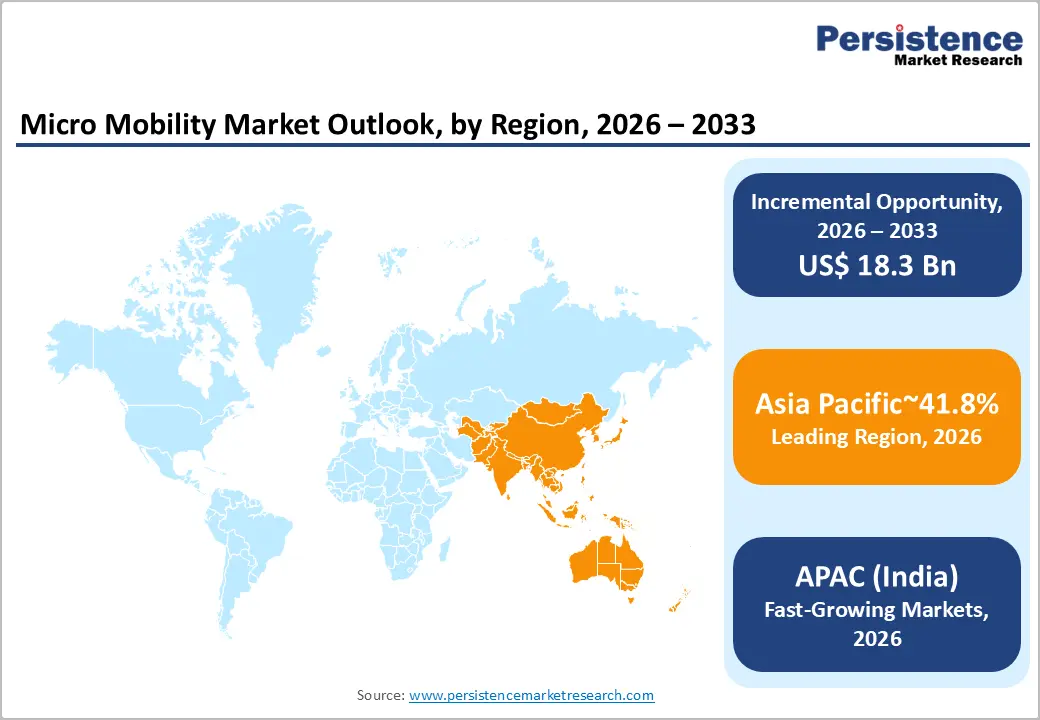

Asia Pacific Micro Mobility Market Trends and Insights

Asia Pacific holds a share of 41.8% in 2025, anchored by China's massive e-bike installed base of over 350 million units and rapid manufacturing scale-up across Southeast Asia. The region benefits from a dense urban population, lower per-trip economics, and supportive industrial policy under Made in China 2025 and India's FAME-II, positioning the Asia Pacific as the global epicenter of micro mobility production and consumption.

China Micro Mobility Market Size

China's Micro Mobility market value reaches US$ 9.7 billion in 2025, propelled by 440 million on-road two-wheelers per the Ministry of Public Security, and the GB 17761 e-bike technical standard, which has standardized over 120 million compliant units. Domestic giants Yadea, AIMA, and Niu Technologies collectively shipped beyond 30 million units in 2024, while Hello Inc. and Meituan Bike sustain shared-fleet leadership across 400+ cities.

India Micro Mobility Market Size

India's Micro Mobility market value reaches US$ 3.2 billion in 2025, driven by the FAME-II scheme disbursing over INR 11,500 crore in EV subsidies and PM E-DRIVE allocations of INR 10,900 crore for two-wheeler electrification. Society of Manufacturers of Electric Vehicles (SMEV) data confirms electric two-wheeler registrations crossed 1.1 million units in FY24, supported by Ola Electric, TVS, and Bajaj Auto expansions.

Japan Micro Mobility Market Size

Japan represents about 12% of the Asia Pacific market in 2025, with strong demand for Panasonic and Yamaha PAS pedal-assist e-bikes, supported by aging population mobility programs. Japan Bicycle Promotion Institute indicates the e-bike fleet exceeded 8.2 million units, while specially permitted electric kick scooter usage was launched nationwide under revised Road Traffic Act in 2023.

Competitive Landscape

The global micro mobility market is moderately fragmented, with the top ten OEMs collectively holding around 40% of revenue while regional and white-label players capture the remainder. Leaders like Yadea, Niu Technologies, Trek Bicycle, and Giant Manufacturing differentiate through proprietary battery technology, integrated IoT telematics, and direct-to-consumer omnichannel models. R&D investments target lighter alloys, fast-swap battery formats, and AI-enabled fleet management. Subscription-based ownership and B2B fleet leasing are emerging business model trends, particularly in Europe and North America.

Key Developments

- In September, 2025, Segway strengthened its leadership in the micro mobility market by hosting the 2025 Segway Micro Mobility Global Key Partners Conference in Changzhou, China, where it brought together global distributors and retail partners to advance collaboration and showcase its expanding portfolio of electric kick-scooters, e-bikes, and specialized SSV/UTV models, while reinforcing its innovation-led strategy focused on safer, smarter, and scenario-based mobility solutions supported by advanced R&D, intelligent manufacturing, and diversified product lines designed for urban commuting and off-road applications.

- In October 2025, Yadea announced at EICMA 2025 its next-generation micro mobility ecosystem, introducing an integrated electric mobility and charging solution featuring an intelligent battery-swapping network enabling 15-second swaps, a high-performance Polar Sodium 1 sodium-ion battery with over 100 km range and 1,500-cycle life, and a solar-powered charging system with energy storage, reinforcing its leadership in sustainable micro mobility infrastructure and expanding accessible, long-range electric two-wheeler usage globally.

Micro Mobility Market - Key Insights & Details

| Key Insights | Details |

|---|---|

| Historical Market Value (2020) | US$ 22.9 Billion |

| Current Market Value (2026) | US$ 52.5 Billion |

| Projected Market Value (2033) | US$ 150.9 Billion |

| CAGR (2026 - 2033) | 16.3% |

| Leading Region | Asia Pacific, 41.8% |

| Dominant Category-1 (Vehicle Type) | E-Bikes, 35% |

| Top-ranking Category-2 (Propulsion Type) | BEVs, 58% |

| Incremental Opportunity | US$ 98.4 Billion (2026 - 2033) |

Companies Covered in Micro Mobility Market

- Yadea Group Holdings Ltd.

- Segway-Ninebot

- Lime (Neutron Holdings, Inc.)

- Bird Global Inc.

- Gogoro Inc.

- Niu Technologies

- Tier Mobility / Dott

- Voi Technology AB

- Accell Group

- Giant Manufacturing Co., Ltd.

- Yamaha Motor Co., Ltd.

- Trek Bicycle Corporation

- Rad Power Bikes

- Ather Energy

- Ola Electric Mobility Ltd.

Frequently Asked Questions

The global Micro Mobility market is expected to be valued at US$ 52.5 billion in 2026 and is projected to reach US$ 150.9 billion by 2033, growing at a CAGR of 16.3%.

Demand is being propelled by urban congestion, tightening emission mandates, and the steady decline in lithium-ion battery prices to US$ 115/kWh in 2024, alongside subsidy programs such as FAME-II and the European Green Deal.

Asia Pacific leads the global market with a 41.8% share in 2025, anchored by China's installed base of over 350 million e-two-wheelers and India's rapidly expanding electric two-wheeler segment under FAME-II.

Battery-swapping infrastructure for last-mile delivery fleets is a transformational opportunity, especially given that last-mile logistics accounts for over 53% of parcel delivery costs as per International Post Corporation (IPC) data.

Key participants include Yadea, Niu Technologies, AIMA, Trek Bicycle, Giant Manufacturing, Lime, Bird Global, Ola Electric, and Segway-Ninebot.