- Healthcare Services

- At Home Micronutrient Testing Market

At Home Micronutrient Testing Market Size, Share, and Growth Forecast 2026 – 2033

At Home Micronutrient Testing Market by Product Type (Strips, Cassettes, Kits, Others), Sample Type (Whole Blood, Urine), Micronutrient Type (Vitamins, Minerals, Others), Distribution Channel (Online pharmacies, Others), and Regional Analysis 2026 – 2033

At Home Micronutrient Testing Market Size and Trends Analysis

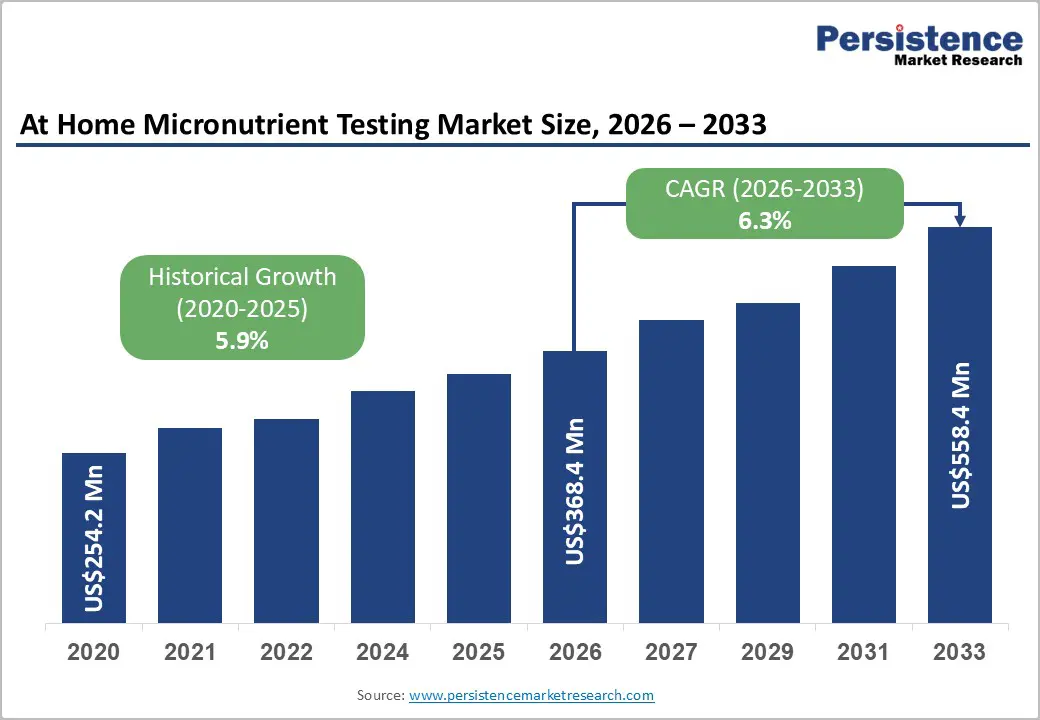

The global at home micronutrient testing market size is projected to be valued at US$368.4 million in 2026 and is expected to reach US$558.4 million by 2033, growing at a CAGR of 6.3% during the forecast period between 2026 and 2033, driven by the rising consumer adoption of preventive healthcare drives this growth, supported by widespread micronutrient deficiencies affecting over 1.6 billion people globally, including vitamin D insufficiency in more than one-third of adults. The post-pandemic landscape has normalized remote sample collection, positioning these tests as a cornerstone of preventative wellness strategies rather than just diagnostic tools for acute illness.

Key Industry Highlights

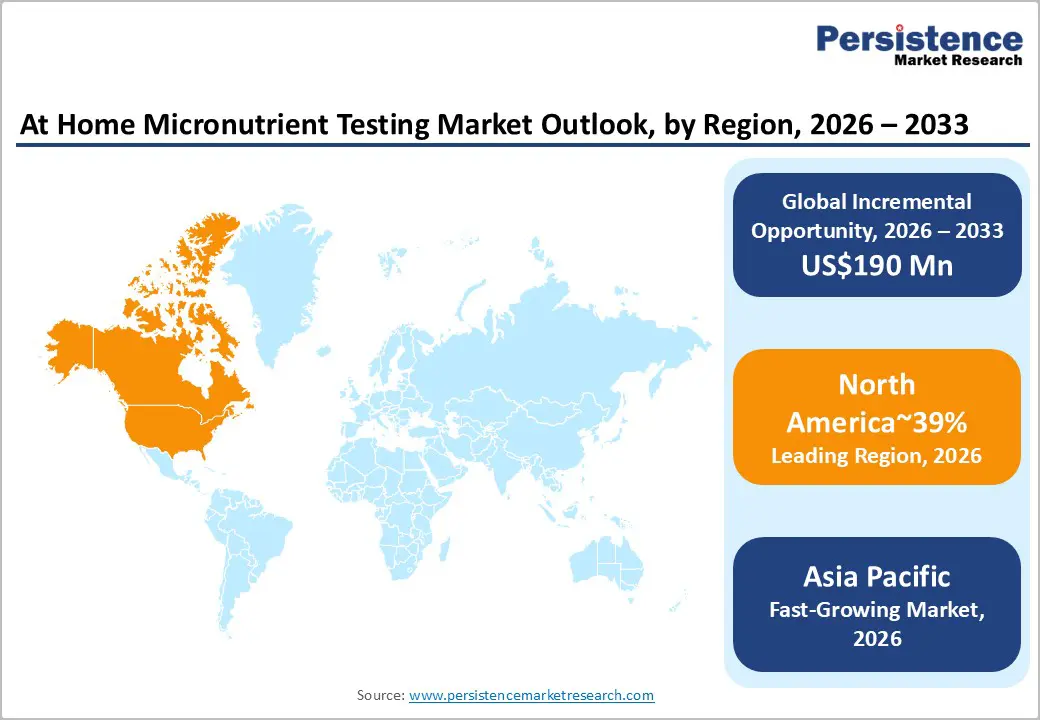

- Leading Market Region: North America is expected to dominate in 2026, accounting for around 39% of the market, with the U.S. at the forefront. The region’s leadership is supported by a well-established direct-to-consumer laboratory ecosystem, high consumer health awareness, CLIA-waived regulatory frameworks, and advanced logistics infrastructure, driving strength across test strips, kits, and comprehensive panel testing applications.

- Fastest-growing Region: Asia Pacific is projected to be the fastest-growing region, driven by rapid urbanization, a growing middle class, rising preventive health awareness, and strong adoption in China and India, fueled by cost-effective local manufacturing and integration with telemedicine and digital health platforms, enabling swift penetration across consumer and clinical wellness segments.

- Leading Product Type: Strips are expected to lead, accounting for approximately 42% of the market due to affordability, ease of use, and immediate results. They dominate routine vitamin D and B12 screening and support repeat testing behavior across wellness-focused consumers.

- Fastest-growing Product Type: Kits are expected to be the fastest-growing segment, benefiting from integrated home-to-lab workflows, higher analytical accuracy, and digitally delivered laboratory-grade results for complex vitamin and biomarker panels.

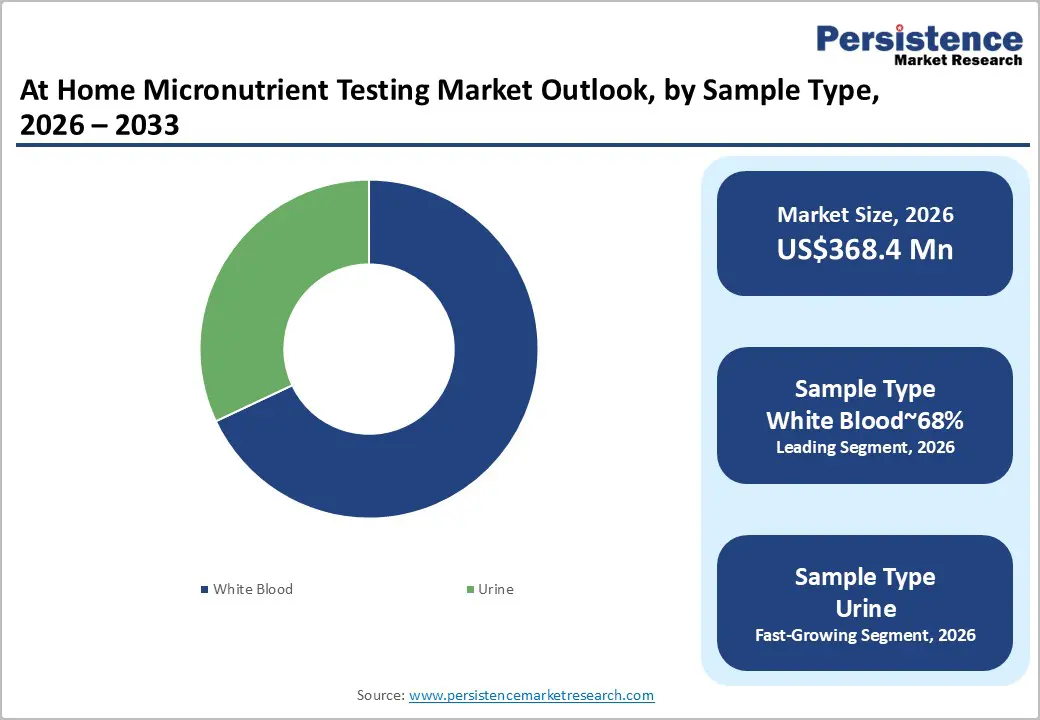

- Leading Sample Type: Whole blood is projected to lead with 68% market share, driven by finger-prick and dried blood spot methods validated for high-accuracy micronutrient measurement.

- Key Industry Development: In June 2025, Labcorp introduced whole health solutions with a comprehensive nutrient panel for at-home compatible testing. It offers providers and consumers access to micronutrient biomarkers, enhancing holistic care through convenient specimen collection and data-driven wellness.

| Key Insights | Details |

|---|---|

| At Home Micronutrient Testing Market Size (2026E) | US$368.4 Mn |

| Market Value Forecast (2033F) | US$558.4 Mn |

| Projected Growth (CAGR 2026 to 2033) | 6.3% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.9% |

Market Dynamics – Driver, Restraints, and Opportunities

Rising Micronutrient Deficiencies in Urban Populations

Shifts in urban lifestyles, dietary habits, and indoor-centric routines have led to a widespread phenomenon often described as “hidden hunger,” where calorie intake is sufficient, but micronutrient intake is inadequate. Even in economically developed regions, deficiencies in key nutrients such as vitamin D, iron, and magnesium are increasingly common due to processed diets, limited sun exposure, and high stress levels. Public health bodies and national surveys consistently flag micronutrient imbalance as a growing concern, positioning nutritional status as a core component of preventive health rather than a niche clinical issue.

Heightened consumer awareness, amplified by digital health content, wellness influencers, and employer-led health initiatives, is translating directly into demand for targeted micronutrient testing. Individuals experiencing non-specific symptoms such as fatigue, low immunity, or poor concentration are more inclined to seek confirmation through testing rather than clinical consultation. At-home diagnostic formats play a critical enabling role by removing time, access, and psychological barriers associated with physician visits. This convenience-driven shift is unlocking latent demand among urban, working-age consumers and driving sustained volume growth for focused micronutrient testing panels within the broader preventive diagnostics market. In August 2024, Quest Diagnostics launched 13 new consumer-initiated blood tests for micronutrient deficiencies. This initiative empowers individuals to identify nutrient gaps influenced by diet, medications, or chronic conditions, promoting proactive health management.

Persistent Trust Deficit around Sample Integrity and Diagnostic Accuracy

Despite ongoing advances in assay sensitivity and logistics, a structural credibility challenge continues to constrain the market. Capillary blood samples collected via finger-prick are still perceived by many clinicians as less reliable than venous blood draws, particularly for analytes sensitive to volume variation, clotting, or hemolysis. In home-collection settings, inconsistencies in user technique, such as inadequate blood flow, contamination, or improper sealing, can compromise sample integrity before laboratory analysis. Shipping-related factors, including temperature exposure and transit delays, further heighten the risk of degradation, increasing the likelihood of test rejection or result variability.

This perceived reliability gap limits acceptance beyond preventive wellness use cases and slows integration into formal clinical pathways. Physicians remain cautious about basing treatment decisions on home-collected samples, which restricts expansion into chronic disease monitoring or therapeutic management. For consumers, any experience of inconclusive or repeated testing erodes confidence and raises perceived effort, directly impacting repeat usage and subscription retention. Unless confidence in sample quality and analytical equivalence is firmly established across both medical professionals and end users, this trust deficit remains a serious brake on long-term market scalability.

AI-Enabled Convergence of At-Home Diagnostics with Wearable Health Ecosystems

A high-value growth opportunity is emerging at the intersection of biochemical testing platforms and consumer wearable ecosystems. By integrating at-home micronutrient and biomarker data with continuous biophysical signals captured by wearables such as sleep patterns, recovery metrics, heart rate variability, and activity load, companies can move beyond static test reports toward dynamic, longitudinal health insights. Strategic partnerships with established wearable leaders enable seamless data interoperability, allowing biochemical markers to be contextualized against real-world physiological performance rather than interpreted in isolation.

The application of AI across these combined datasets enables the creation of closed-loop health systems that deliver personalized feedback, trend detection, and adaptive recommendations over time. This model is particularly attractive to performance-driven consumers such as endurance athletes, quantified-self users, and biohackers, who value actionable insights over one-time results and demonstrate higher willingness to pay and stronger retention behavior. By shifting from episodic testing to integrated health intelligence, providers can expand addressable demand, deepen subscription stickiness, and reposition their offerings as core digital health companions rather than standalone diagnostic tools. In April 2025, Viome Life Sciences debuts an AI-powered full-body intelligence test for at-home health analysis. Using RNA sequencing from multiple samples, it delivers precision nutrition insights on micronutrients, supporting aging slowdown and disease prevention.

Category–wise Analysis

Product Type Insights

Strips are anticipated to lead with an approximate 42% market share, driven by their low cost, ease of use, and immediate result delivery for commonly monitored biomarkers such as Vitamin D and Vitamin B12. Their dominance reflects a strong consumer shift toward self-testing formats that eliminate sample shipping, laboratory wait times, and higher upfront expenses. Advances in lateral flow and semi-quantitative detection have improved reliability for routine screening use cases, making strips particularly attractive for repeat testing, wellness-focused consumers, and price-sensitive users. Retail and online channel penetration further reinforces strip adoption, positioning them as the most accessible entry point within the at-home diagnostics ecosystem.

Kits are expected to be the fastest-growing product segment, supported by integrated “home-to-lab” testing models that combine sample collection, controlled logistics, and digitally delivered laboratory-grade results. Their growth is closely tied to biomarkers requiring higher analytical accuracy, including ferritin, hormone panels, and complex vitamin assays, where rapid formats remain insufficient. Beyond kits, cassettes account for roughly 19% of the market, maintaining relevance in structured testing environments due to standardized handling and compatibility with reader-based systems. Other product formats contribute about 8%, encompassing niche or hybrid solutions that address specific clinical or research-oriented needs, but with limited scalability compared to strips and kits.

Sample Type Insights

Whole blood is expected to dominate the sample type landscape with an estimated 68% market share in 2026, and it is also the fastest-growing segment due to continued innovation in micro sampling technologies. Finger-prick and dried blood spot methods remain the gold standard for high-accuracy measurement of key micronutrients such as Vitamin D, Vitamin B12, iron, and folate, where serum-equivalent precision is essential for clinical relevance. The widespread validation of DBS stability during transport, combined with compatibility across centralized laboratory workflows, has entrenched whole blood as the default matrix for quantitative at-home and remote testing. Recent advances in painless lancets, low-volume capillary collection, and improved analyte recovery further strengthen adoption by reducing user discomfort without compromising analytical integrity.

Urine sampling is anticipated to be the fastest-growing, addressing use cases where non-invasive collection offers a clear advantage. It is particularly relevant for iodine assessment, hydration status, and water-soluble vitamin analysis, supporting screening-oriented and wellness-driven testing models. The appeal of urine-based kits is strongest among pediatric, geriatric, and compliance-sensitive populations, where ease of collection outweighs the need for broad micronutrient coverage. While urine remains limited by narrower biomarker applicability compared to blood, its role continues to expand in targeted diagnostic and preventive health applications.

Micronutrient Type Insights

Vitamins are anticipated to dominate the micronutrient testing landscape with an estimated 52% market share in 2026, anchored primarily by high-frequency screening of Vitamin D and Vitamin B12. Vitamin D functions as a gateway test for many consumers due to its strong association with immunity, bone health, mood regulation, and widespread deficiency awareness across regions. Seasonal testing spikes, physician recommendations, and routine wellness programs consistently reinforce testing volumes. Vitamin B12 further strengthens this segment, particularly among vegetarian populations, aging consumers, and individuals reporting fatigue-related symptoms. Together, these vitamins benefit from clear clinical reference ranges, standardized laboratory methods, and strong consumer familiarity, sustaining repeat testing behavior and making vitamins the most commercially reliable micronutrient category.

Comprehensive panels are expected to be the fastest-growing segment, driven by consumer preference for bundled testing that evaluates multiple vitamins and minerals in a single collection cycle. These panels align with preventive health behavior, offering broader nutritional insights while reducing per-marker cost and logistical effort. Minerals account for approximately 32% of the market, supported by demand for magnesium, zinc, iron, and ferritin testing tied to fitness recovery, energy optimization, and anemia screening. The Others or comprehensive category holds around 16% share, benefiting from personalized health platforms and subscription-based wellness models, where multi-marker assessments increasingly replace single-analyte testing as the default choice.

Distribution Channel Insights

Online pharmacies are anticipated to dominate the market segment, as it will lead by being the fastest growing market for approximately 43% of total market share. Their dominance is driven by direct-to-consumer convenience, seamless digital health integration, and expanding e-commerce penetration across urban and semi-urban markets. Online platforms enable consumers to order products discreetly, compare prices in real time, and access bundled offerings that combine diagnostics, prescriptions, and follow-up consultations. Integration with digital payment systems, telehealth platforms, and subscription-based refill models further strengthens customer retention. Online pharmacies benefit from lower operating overheads than brick-and-mortar outlets, allowing competitive pricing and aggressive promotional strategies.

Retail pharmacies account for roughly 34% of distribution, supported by strong consumer trust, immediate product availability, and pharmacist-led guidance at the point of sale. These outlets remain particularly relevant for urgent purchases and for consumers seeking reassurance through face-to-face interaction. Hypermarkets contribute about 23% of the market, leveraging high footfall and one-stop shopping convenience to drive impulse and routine purchases. However, limited product specialization and weaker advisory support constrain their ability to compete with pharmacy-centric channels, positioning them as complementary rather than primary distribution points.

Regional Insights

North America At Home Micronutrient Testing Market Trends

North America is expected to lead the global market, holding approximately 39% share, supported by a mature direct-to-consumer laboratory ecosystem and high consumer health literacy. The U.S. anchors regional dominance through an enabling regulatory framework that allows CLIA-waived laboratories to operate at scale, fostering rapid service deployment and innovation. High per capita healthcare spending and advanced digital infrastructure strengthen adoption, while efficient logistics networks support biological sample collection and processing. These structural factors position North America ahead of other regions in market maturity and consumer-driven utilization.

The region is likely to sustain leadership as demand expands through e-commerce–enabled healthcare delivery and a growing emphasis on personalized health monitoring and preventive diagnostics. Cultural shifts toward self-directed health optimization support recurring testing behavior, while regulatory oversight maintains quality and trust across decentralized testing models. Ongoing integration between traditional healthcare systems and consumer-oriented platforms reinforces operational scale and service accessibility. These demand-side and regulatory dynamics are expected to preserve North America’s dominant position, supporting stable expansion driven by utilization intensity rather than geographic reach.

Europe At Home Micronutrient Testing Market Trends

Europe is expected to account for approximately 30% of the global market, reflecting a mature and structurally stable regional position shaped by strong public healthcare systems and policy-led standardization. Germany, the U.K., and France anchor regional demand, while harmonization under the In Vitro Diagnostic Regulation is expected to progressively align quality and compliance requirements across member states. Preventative healthcare policies, including population-level screening and wellness initiatives, reinforce steady utilization, while pharmacy-led distribution channels expand access beyond hospital settings. These regulatory and demand-side dynamics support consistent adoption without signaling rapid acceleration.

The region is likely to remain stable as retail pharmacies continue to play a central role in test kit distribution, complementing established clinical pathways. Privacy and data governance requirements under GDPR actively shape product design, data handling, and consumer engagement models, reinforcing trust but moderating the speed of rollout. In the U.K., pharmacy-based testing and public health campaigns strengthen routine usage, while continental markets prioritize compliance and integration within public reimbursement systems. These structural characteristics are expected to preserve Europe’s mature market profile, balancing regulatory rigor with incremental penetration rather than volume-led growth.

Asia Pacific At Home Micronutrient Testing Market Trends

Asia Pacific is expected to account for approximately 20% of the global market, emerging as the fastest-growing region due to accelerating urbanization and expanding middle-class populations. China and India drive regional momentum as rising awareness of lifestyle-related conditions increases demand for preventive and at-home health testing. Shifts toward westernized diets and changing consumption patterns reinforce the need for targeted diagnostics, while rapid adoption of digital health platforms supports broader access. These demand-side dynamics position Asia Pacific ahead of mature regions in growth velocity, despite a smaller overall market base.

The region is likely to sustain rapid expansion as China and India leverage manufacturing scale to support cost-efficient production of test kits and related health products. Local manufacturers increasingly tailor diagnostic panels to regional needs, such as tests addressing vegetarian-specific nutritional deficiencies, improving relevance and uptake. Telemedicine platforms and mobile health applications further integrate testing into routine care pathways, particularly in urban centers. These structural, demand-driven, and digital enablers are expected to reinforce Asia Pacific’s fastest-growth profile, supporting deeper market penetration and sustained adoption.

Competitive Landscape

The global at home micronutrient testing market remains moderately fragmented but is clearly transitioning toward consolidation. The competitive set spans digital native wellness platforms such as Everlywell and LetsGetChecked, alongside incumbent diagnostics leaders like Quest Diagnostics and LabCorp that have extended into direct-to-consumer models.

The top five players collectively account for roughly 45% of market activity, with Everlywell leading, followed by LetsGetChecked and Thorne, while LabCorp and Quest Diagnostics leverage laboratory scale and clinical credibility. Competitive differentiation increasingly centers on analytical accuracy, digital reporting depth, and ecosystem integration, accelerating consolidation as scale becomes critical for trust, compliance, and subscription economics.

Key Industry Developments:

- In July 2025, Matrix Medical Network partnered with Molecular Testing Labs to enhance in-home diagnostics. The collaboration advanced molecular testing options, including potential micronutrient assessments, aimed at improving patient outcomes in home settings.

- In April 2025, Viome Life Sciences expanded its precision supplement platform into Europe with microbiome tests. This move broadened access to at-home testing for metabolic health, including micronutrient optimization, and promoted global preventive care.

- In October 2024, LetsGetChecked acquired Truepill to strengthen its at-home diagnostic and pharmacy services. The deal integrated digital pharmacy with micronutrient testing, enabling end-to-end care for improved health outcomes and accessibility.

Companies Covered in At Home Micronutrient Testing Market

- Everlywell

- LetsGetChecked

- Thorne

- Quest Diagnostics

- Labcorp

- ZRT Laboratory

- MyLabBox

- Genova Diagnostics

- Imaware

- GenePlanet

- Nutritional Testing Services

- Cerascreen

- OmegaQuant

- Vitl

- Baze

- Viome

Frequently Asked Questions

The global at-home micronutrient testing market is projected to be valued at US$368.4 million in 2026 and is forecast to reach US$558.4 million by 2033, driven by rising consumer adoption of preventive healthcare and widespread micronutrient deficiencies.

Demand is fueled by increasing consumer focus on preventive health, widespread deficiencies affecting over 1.6 billion people globally, and the post-pandemic normalization of remote sample collection, which positions these tests as convenient tools for personalized wellness management.

The global At-Home Micronutrient Testing market is expected to grow at a Compound Annual Growth Rate (CAGR) of 6.3% from 2026 to 2033, reflecting sustained adoption in urban populations and integration with digital health platforms.

Online Pharmacies are the leading and fastest-growing distribution channel, holding approximately 43% market share, due to direct-to-consumer convenience, seamless digital health integration, competitive pricing, and the ability to offer bundled diagnostic and consultation services.

Key players include Everlywell, LetsGetChecked, Thorne, Quest Diagnostics, Labcorp, Viome, and ZRT Laboratory, among others.