- Food Ingredients & Additives

- Micronized Salt Market

Micronized Salt Market Size, Share, and Growth Forecast, 2025 - 2032

Micronized Salt Market By Purity (From 98% to 99.5%, Above 99.5%), Application (Bakery & Confectionery, Others), Product Type (Low-Sodium Salt, Potassium-Enhanced Salt, Functional Salt, Organic/Natural Salt, Specialty Therapeutic Salt, Others), and Regional Analysis for 2025 - 2032

Micronized Salt Market Share and Trends Analysis

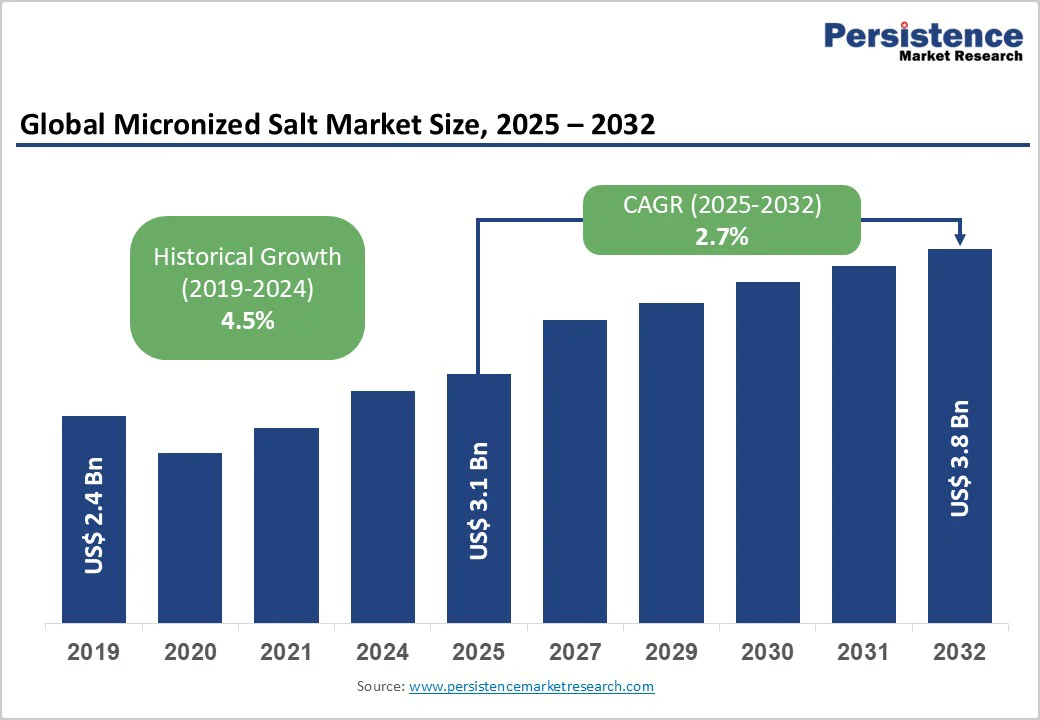

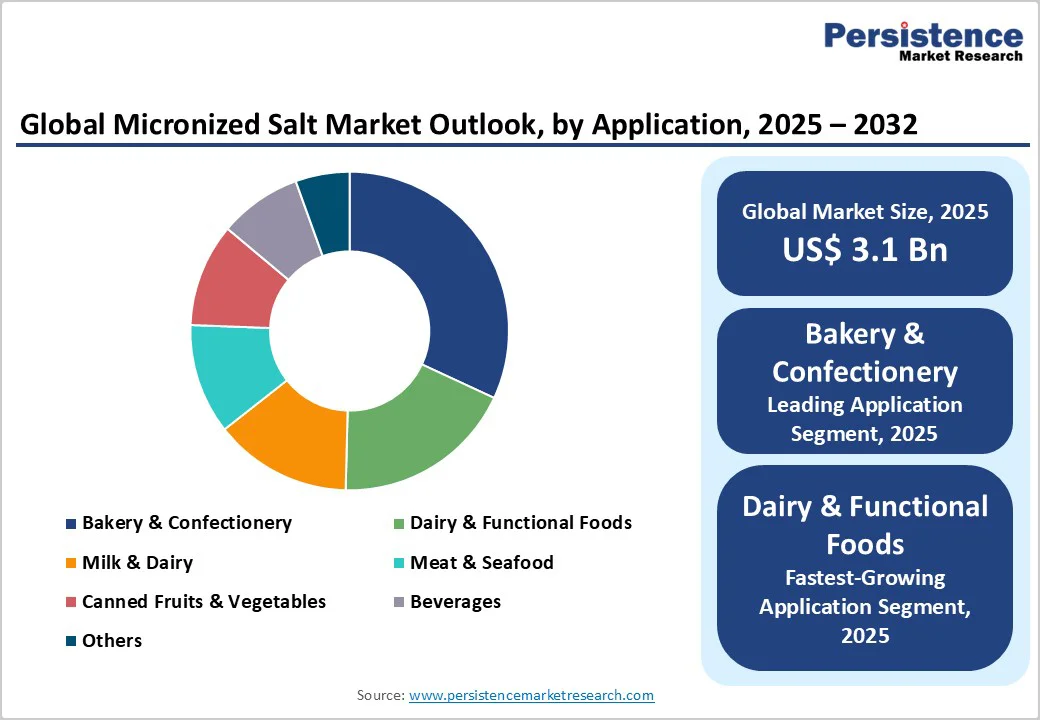

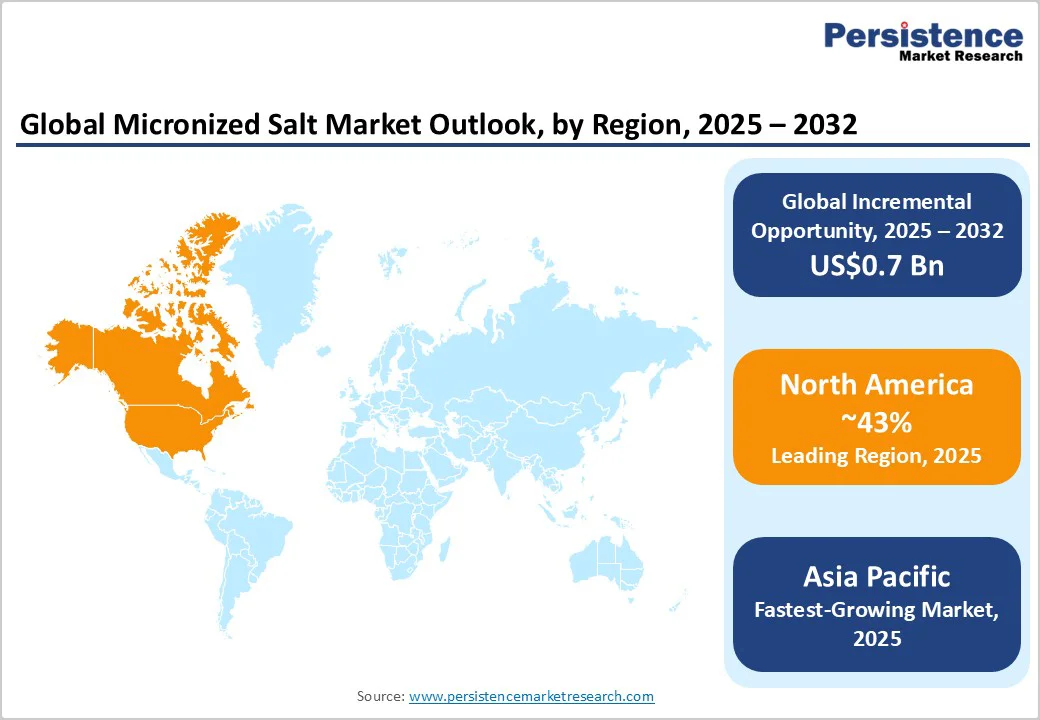

The global micronized salt market size is likely to be valued at US$3.1 Billion in 2025, and is estimated to reach US$3.8 Billion by 2032, growing at a CAGR of 2.7% during the forecast period 2025-2032, driven primarily by expanding applications in food processing, pharmaceutical, and water treatment sectors. The market growth is driven by rising demand for micronized salt in ready-to-eat foods, baking, and seasonings, valued for its fine particle size and purity. Global sodium-reduction initiatives spur innovation, while North America, Europe, and rapidly expanding Asia Pacific drive regional momentum.

Key Industry Highlights

- Dominant Purity Segment: The 98% to 99.5% segment is set to dominate with a 58.3% market share in 2025, supported by extensive use in food-grade and industrial applications.

- Leading Application: Bakery and confectionery applications are expected to account for nearly 32% market share in 2025, fueled by micronized salt’s role in product quality enhancement.

- Fastest-growing Regional Market: The Asia Pacific market is anticipated to showcase the highest growth potential from 2025 to 2032, powered by industrial expansion and widespread salt consumption.

- Dominant Region: North America is slated to command the largest market share of roughly 43% in 2025, led by the regulatory environment and innovation ecosystem of the U.S.

- Competitive Milieu: Industry movements have been focused on capacity expansions, product innovation, and technology partnerships.

- Emerging Opportunity: Health-focused salt variants (low-sodium and functional salts) are emerging as lucrative sub-segments during the 2025-2032 forecast period, aligning with sodium reduction initiatives globally.

| Key Insights | Details |

|---|---|

|

Micronized Salt Market Size (2025E) |

US$3.1 Bn |

|

Market Value Forecast (2032F) |

US$3.8 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

2.7% |

|

Historical Market Growth (CAGR 2019 to 2024) |

4.5% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Technological Advancements in Salt Micronization and Purity Optimization

The market is increasingly benefiting from refinements in milling and processing technologies that produce ultra-fine salt particles with high purity levels exceeding 98%. These technological improvements optimize salt solubility and dispersibility, crucial for food manufacturing and pharmaceutical applications that demand uniform salt distribution without compromising taste or texture. For instance, advancements in air-jet milling and controlled crystallization enable manufacturers to tailor salt particle size, with micronization consistently delivering particles smaller than 100 microns, enhancing product performance and consumer satisfaction.

Data from international regulatory agencies, such as the U.S. Food and Drug Administration (FDA) and the European Food Safety Authority (EFSA), emphasize stricter quality norms for food-grade salts, further driving adoption of technologically advanced micronized salts. The strategic alignment with sodium reduction guidelines set by the World Health Organization (WHO) is also influential, as micronized salts facilitate lower sodium content through enhanced saltiness perception, enabling product reformulation.

Raw Material Price Volatility and Supply Chain Constraints to Create Cost Pressures

The market growth faces structural challenges, mainly on account of fluctuations in rock salt prices, which constitute the raw material base. Pricing volatility linked to geopolitical tensions, mining disruptions, and transportation costs directly impacts production expenses for micronized salt manufacturers. For example, the International Trade Centre (ITC) reports that salt mining regions such as India and China experience seasonal variations affecting output volumes, thereby driving cost unpredictability.

Additional compounding factors include environmental regulations that increasingly restrict salt mining activities, aiming to reduce ecological impact and protect water resources. Compliance with these regulations introduces higher operational costs and capital expenditures related to sustainable mining practices and pollution controls. Furthermore, the supply chain complexity for micronized salt, which requires precision handling and specialized packaging to maintain particle integrity, amplifies distribution costs. These cost barriers translate into pricing pressures on end-product manufacturers, which can limit wider adoption in price-sensitive markets, especially in developing economies.

Rising Demand for Health-Focused Salt Variants to Open Lucrative Growth Avenues

The health and wellness trend is creating substantial growth opportunities within the micronized salt market, particularly for specialized salt variants such as low-sodium, potassium-enhanced, and functional salts fortified with essential minerals. These variants cater to the increasing consumer and regulatory push for sodium reduction, given WHO targets for a 30% cut in global sodium consumption by 2025. In addition to addressing dietary concerns, these segments provide manufacturers with differentiation potential through product innovation.

Policy-level support from agencies such as the U.S. FDA’s sodium reduction programs and the European Commission (EC)’s food reformulation frameworks amplifies this opportunity. Technological convergence in salt micronization facilitates the precise formulation of salt blends that maintain flavor while reducing sodium content, aligning with where consumer demand is shifting. Companies engaging in R&D for these health-oriented micronized salts are well-positioned to capitalize on unmet customer needs and regulatory incentives, enabling premium pricing and long-term revenue growth.

Category-wise Analysis

Purity Insights

The 98% to 99.5% segment currently leads the micronized salt market revenue share, commanding an estimated 58.3% in 2025. This dominance stems from its broad applicability across multiple industries, particularly food processing and water treatment, where moderate purity salt balances cost-effectiveness with quality standards. Operational efficiency in large-scale manufacturing, such as bakery and processed food production, benefits substantially from this segment’s consistent availability and favorable price points.

In contrast, the above 99.5% segment is demonstrating the fastest growth from 2025 to 2032. This growth is primarily fueled by stringent industry demands for ultra-pure micronized salts in pharmaceutical, medical-grade, and cosmeceutical applications. Advancements in purification and milling technologies are lowering costs, enabling wider adoption beyond premium sectors. The segment’s rising share reflects market value shifts toward specialized applications where impurity levels critically dictate product quality and safety compliance.

Application Insights

The bakery & confectionery segment is set to continue as the market leader in 2025, representing an estimated 31.9% of the revenue share. The consistent demand for micronized salt in this sector arises from its utility in enhancing taste uniformity, dough kneading processes, and prolonging shelf life. The fine micron size facilitates rapid dissolution and homogenous blending in complex bakery formulations, meeting industrial demands for quality and efficiency.

The dairy & functional food segment emerges as the fastest growing application over the 2025-2032 period. The expansion is driven by evolving consumer preferences for fortified and ready-to-eat dairy alternatives that require precise sodium regulation for health benefits. The central role of micronized salt in improving flavor without compromising nutritional goals aligns effectively with these demands. The segment also benefits from enhanced processing techniques where salt particle size directly impacts texture and preservation in high-moisture products.

Product Type Insights

The functional salts segment is identified as the fastest-growing category through 2032. Functional salts, often enriched with minerals such as magnesium, calcium, and trace elements beyond potassium, cater to expanding nutritional and wellness trends within the global population. Their multi-mineral composition targets multiple health benefits, including electrolyte balance and cardiovascular support, positioning them as superior to single-mineral potassium-enhanced options.

While potassium-enhanced salts maintain significant growth potential as a sodium substitute, the holistic health benefits of functional salts have driven broader adoption across premium food and pharmaceutical product segments. Advancements in micronization technologies have enhanced the bioavailability and sensory profiles of functional salts, making them attractive for product developers prioritizing wellness-oriented innovation.

Regional Insights

North America Micronized Salt Market Trends

North America is the dominant regional market for micronized salt, capturing an estimated 43% share in 2025. The U.S. serves as the epicenter of this leadership, with its advanced manufacturing infrastructure, pervasive food safety regulations, and robust health advocacy driving product innovation and adoption. The regulatory landscape is shaped by stringent FDA controls and sodium reduction mandates promoted by the Centers for Disease Control & Prevention (CDC), catalyzing demand not only for standard micronized salts but also for specialized low-sodium and functional variants.

Key growth drivers include a high level of consumer health awareness, continuous technological advancements in salt micronization, and integration of micronized salts into processed foods, pharmaceuticals, and specialty applications. The region’s strong R&D ecosystem encourages ongoing innovation, enabling companies to maintain a competitive advantage through product differentiation. Investment climate remains favorable, with capital influx toward capacity expansions and technology upgrades. Market participants are strategically forging collaborations and acquiring innovative startups to fortify their regional footprint.

Europe Micronized Salt Market Trends

Europe is likely to hold approximately 26% of the micronized salt market share in 2025. Countries including Germany, the U.K., France, and Spain drive this market with robust food and pharmaceutical industries underpinned by regulatory harmonization within the European Union (EU). The EFSA’s sodium reduction policies enforce consistent product reformulation requirements that favor micronized salt applications, particularly specialized low-sodium and functional variants.

Contributing growth factors include consumer inclination towards healthier diets, government incentives for food innovation, and environmental sustainability mandates affecting salt mining and processing. The competitive landscape of the market here emphasizes clean-label product lines and sustainable sourcing, with manufacturers innovating to comply with rigorous standards while enhancing product appeal.

Asia Pacific Micronized Salt Market Trends

Asia Pacific is poised to be the fastest-growing regional market through 2032. This growth is fueled by rapid expansion in China’s food processing and pharmaceutical sectors, India’s increasing production capabilities, and rising demand in ASEAN markets due to changing dietary patterns and urbanization. Key growth drivers include government initiatives aiming to improve food safety standards, sodium reduction awareness campaigns, and growing investments in technological upgrades for salt micronization. The regional market benefits from abundant raw material availability combined with cost advantages in manufacturing and distribution. This synergy supports rapid market penetration and scalability.

The expanding middle class with increasing health consciousness further propels the adoption of premium micronized salt types, including health-oriented variants. Foreign direct investments (FDI) and joint ventures are commonplace, establishing Asia Pacific as a strategic growth frontier. By 2032, the region is expected to rival traditional markets, supported by a dynamic regulatory environment encouraging product innovation and market expansion.

Competitive Landscape

The global micronized salt market exhibits a moderately consolidated competitive structure. The top five players collectively control most of the market share, reflecting the dominance of multinational firms such as Cargill Inc., K+S Aktiengesellschaft, Tata Chemicals, Morton Salt, and Compass Minerals. These companies leverage extensive production facilities, geographic reach, integrated supply chains, and proprietary micronization technologies to fortify market leadership. The remaining market consists of regional manufacturers and niche product specialists catering to localized demands or specific applications. Market fragmentation is evident in emerging geographies, where smaller entities sustain competitive viability through cost advantages and tailored product offerings.

Strategically, market leaders emphasize continuous innovation, sustainability, and expansion through mergers and acquisitions (M&A), establishing barriers to entry and enabling premium pricing strategies. Competitive dynamics reflect innovation in health-focused and environmentally sustainable products, technological investment for improved production efficiency, and aggressive geographic expansion.

Key Industry Developments

- In August 2025, University of Waterloo researchers found that increasing potassium intake from foods such as bananas, spinach, broccoli, and sweet potatoes lowers blood pressure by improving the potassium-to-sodium balance. Potassium supports kidney function, reduces sodium retention, and eases heart strain, offering a practical approach to preventing hypertension-related complications.

- In June 2025, researchers from Australia and Romania launched a Cochrane review assessing whether potassium- or magnesium-based salt substitutes lower blood pressure in adults with diabetes. Focusing on randomized trials, it aims to evaluate efficacy, safety, and adherence, providing evidence to guide dietary recommendations and hypertension management in diabetic populations.

- In January 2025, WHO issued new guidelines on lower-sodium salt substitutes (LSSS) to curb excessive sodium intake linked to 1.9 million deaths annually. Containing potassium chloride, LSSS helps lower blood pressure and cardiovascular risk while guiding national sodium reduction initiatives.

Companies Covered in Micronized Salt Market

- TATA Chemicals Ltd.

- Morton Salt, Inc. (A K+S Group Company)

- INEOS Ltd.

- Akzo Nobel N.V.

- British Salt Limited (A Tata Holdings Company)

- Compass Minerals America, Inc.

- Wilson Salt Company

- ICL Group

- J.C. Peacock & Co. Ltd.

- GHCL Ltd.

- Cargill Inc.

- Keya Foods

- Marico Limited

- Kutch Brine Chem Industries

- Other

Frequently Asked Questions

The global micronized salt market is projected to reach US$3.1 Billion in 2025.

The widening demand for micronized salt in ready-to-eat foods, baking, and seasoning, where its fine particle size and purity offer processing efficiencies and quality improvements, is driving the market.

The micronized salt market is poised to witness a CAGR of 2.7% from 2025 to 2032.

Regulatory initiatives globally to reduce sodium intake are catalyzing product innovation, favoring the uptake of low-sodium salt variants, and generating new market opportunities.

Cargill, Inc., K+S Aktiengesellschaft, and Tata Chemicals Limited are a few of the key players in the micronized salt market.