- Medical Devices

- Medical Ultrasound Equipment Market

Medical Ultrasound Equipment Market Size, Share, and Growth Forecast, 2025 - 2032

Medical Ultrasound Equipment Market by Product Type (Compact, Handheld), End-Use (Hospitals, Clinics), Application (Radiology, Gynecology, Cardiology, Others), and Regional Analysis for 2025 - 2032

Medical Ultrasound Equipment Market Size and Trends Analysis

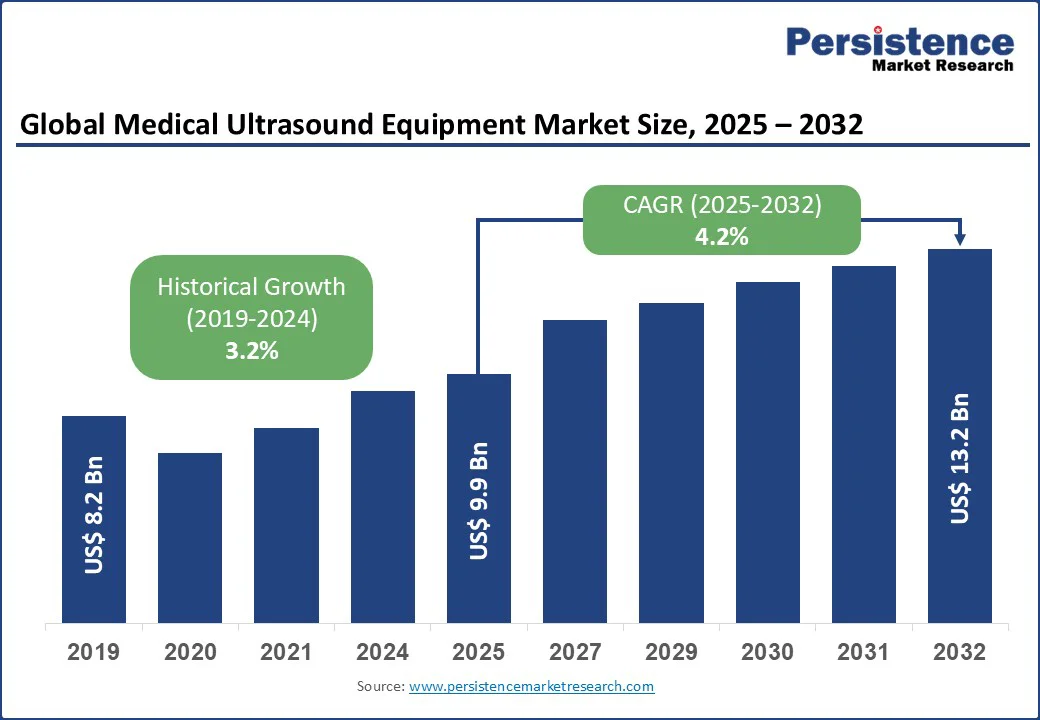

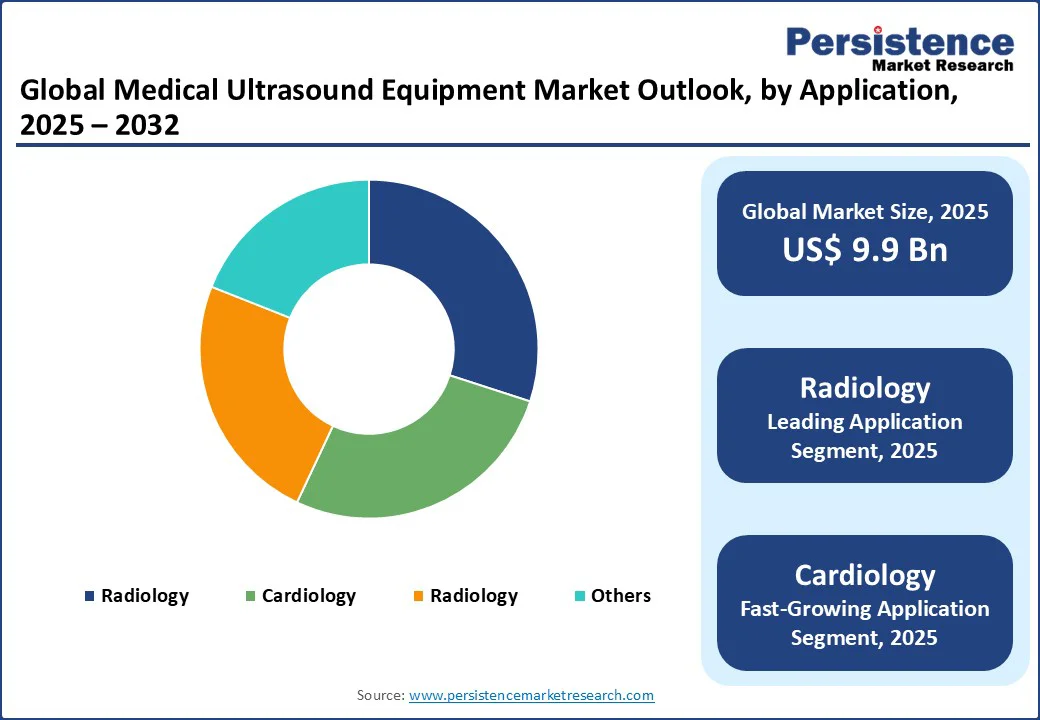

The global medical ultrasound equipment market size is likely to value at US$ 9.9 Bn in 2025 and is expected to reach US$ 13.2 Bn by 2032, registering a CAGR of 4.2% during the forecast period from 2025 to 2032.

The increasing prevalence of chronic conditions such as cardiovascular diseases, cancer, and gynecological disorders, coupled with an aging global population. The demand for effective ultrasound equipment is further fueled by advancements in imaging technologies, growing awareness of early diagnostic tools, and the expansion of healthcare infrastructure in emerging economies.

The sector is supported by the critical role ultrasound plays in non-invasive imaging and related applications, making it a cornerstone of diagnostics across various medical fields.

Key Industry Highlights:

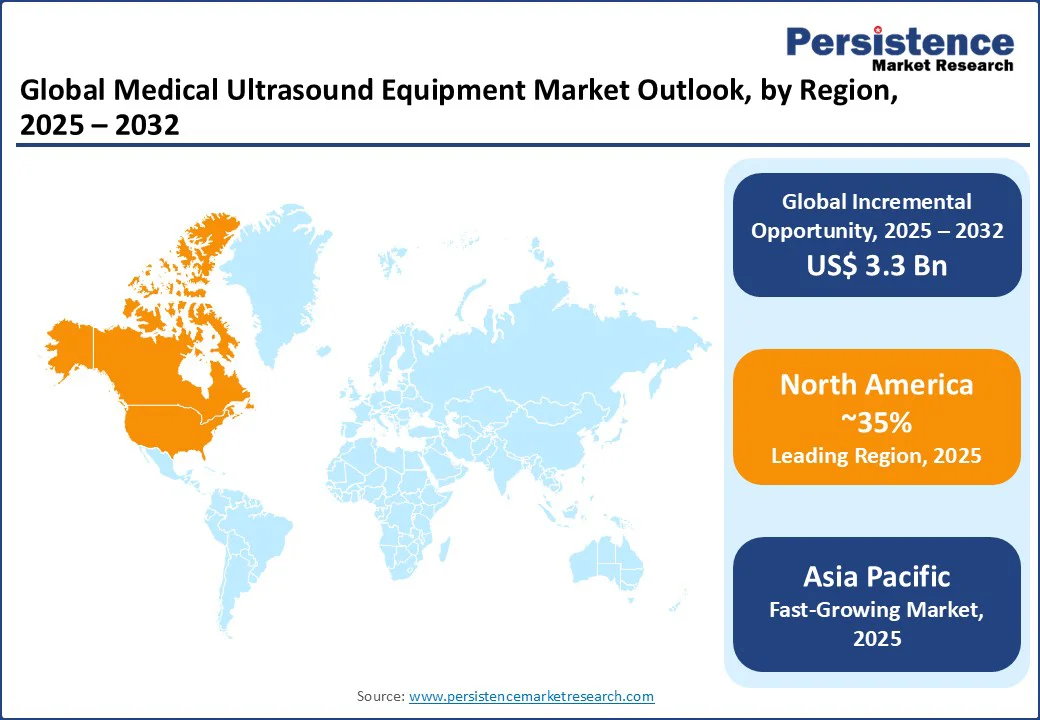

- Leading Region: North America, holding a 35% market share in 2025, driven by advanced healthcare systems, high prevalence of chronic diseases, and robust medical device R&D.

- Fastest-growing Region: Asia Pacific, fueled by rapid urbanization, increasing healthcare expenditure, and rising awareness of preventive diagnostics. Europe, advancing through initiatives such as the EU’s focus on digital health and increased funding for imaging research.

- Dominant Product Type: Compact, commanding nearly 47% market share, reflecting their widespread use in hospitals and comprehensive imaging capabilities.

- Leading Application: Radiology, accounting for over 30% of market revenue, driven by the global rise in diagnostic imaging needs.

- Historical Growth: The sector registered a CAGR of 3.2% from 2019 to 2024, driven by increasing demand for non-invasive diagnostic tools and improved access to healthcare.

|

Global Market Attribute |

Key Insights |

|

Medical Ultrasound Equipment Market Size (2025E) |

US$ 9.9 Bn |

|

Market Value Forecast (2032F) |

US$ 13.2 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

4.2% |

|

Historical Market Growth (CAGR 2019 to 2024) |

3.2% |

Market Dynamics

Driver - Rising prevalence of chronic diseases and aging population

The rising prevalence of chronic diseases and an aging population a major driver fueling the growth of the medical ultrasound equipment market. Conditions such as cardiovascular diseases, cancer, diabetes, and gynecological issues are increasing globally due to sedentary lifestyles, poor dietary habits, rising obesity rates, and longer life expectancies.

According to the World Health Organization (WHO), non-communicable diseases account for 74% of all deaths worldwide, with cardiovascular diseases alone causing 17.9 million deaths annually. The elderly population, projected to reach 1.5 billion by 2050 as per the United Nations, is particularly susceptible to these conditions, necessitating frequent diagnostic imaging.

Ultrasound equipment plays a crucial role in managing these conditions by providing real-time, non-invasive imaging for early detection, monitoring, and treatment planning, without the risks associated with radiation-based methods such as X-rays or CT scans. Its portability, cost-effectiveness, and inclusion in standard diagnostic guidelines make it a preferred choice among healthcare providers.

Moreover, the growing emphasis on preventive healthcare and early diagnosis, coupled with improved access in emerging markets, is expanding the user base. For instance, the U.S. Centers for Disease Control and Prevention (CDC) reports that heart disease affects over 18 million adults in the U.S., many of whom rely on ultrasound for echocardiography and vascular assessments. As the global burden of chronic diseases continues to rise, the demand for ultrasound equipment is expected to grow steadily.

Restraint - High initial costs and maintenance requirements

High initial costs and maintenance requirements pose a significant restraint to the growth of the medical ultrasound equipment market. While ultrasound devices are effective for diagnostics in fields such as radiology, cardiology, and gynecology, their acquisition can be expensive, often ranging from tens to hundreds of thousands of dollars depending on features such as 3D/4D capabilities or AI integration. Ongoing maintenance, software updates, and probe replacements add to the financial burden, particularly for smaller clinics or facilities in developing regions with limited budgets.

These costs can interact with economic factors, such as fluctuating healthcare reimbursements and supply chain disruptions, potentially delaying purchases or upgrades. Such financial concerns often lead to cautious adoption by healthcare providers, especially in resource-constrained settings or for facilities serving low-income populations.

For instance, handheld devices, while portable, may require frequent calibration to maintain accuracy, increasing operational expenses. Such high costs and maintenance needs can reduce accessibility and slow the sector’s growth potential.

Opportunity - Advancements in portable and AI-integrated technologies

Advancements in portable and AI-integrated technologies present a significant opportunity for the growth of the medical ultrasound equipment market. Medical device companies are increasingly focusing on developing innovative designs that enhance mobility, image quality, and diagnostic accuracy while reducing user dependency on expertise.

New approaches include wireless handheld devices, AI-powered image analysis for automated measurements, and integrations with telemedicine platforms. These innovations not only improve diagnostic outcomes but also extend usability to point-of-care settings, making imaging more accessible in remote or emergency scenarios.

Additionally, research into miniaturized probes and machine learning algorithms aims to address limitations associated with traditional equipment, such as operator variability or time-consuming scans.

For instance, AI-enhanced systems can detect abnormalities in real-time during cardiology or gynecology exams, improving efficiency and reducing errors. Such advancements can expand the sector by attracting more users in ambulatory care and emerging markets, ultimately driving sustained demand in both developed and developing regions.

Category-wise Analysis

Product Type Insights

Compact dominates the medical ultrasound equipment market, expected to account for approximately 47% of the sector share in 2025. Their dominance stems from their widespread use in hospitals and clinics due to their high-resolution imaging and versatility in various applications.

Compact ultrasound systems, such as cart-based units, are cost-effective and well-integrated into clinical workflows globally. Their compatibility with advanced features such as Doppler and 3D imaging further enhances their applicability across diverse patient populations.

The handheld segment is the fastest-growing, driven by increasing demand for point-of-care diagnostics in emergency and remote settings. Handheld devices offer portability and ease of use, making them ideal for quick assessments in cardiology or gynecology. The rise in telemedicine adoption, particularly in aging populations, and advancements in battery life and wireless connectivity are accelerating the adoption of handheld ultrasound, especially in North America and Europe.

End-use Insights

Hospitals hold the largest market share, accounting for approximately 41% of revenue in 2025. Their popularity is driven by the need for comprehensive diagnostic capabilities in inpatient and outpatient settings for chronic disease management. Hospital-based ultrasound equipment, such as compact systems, is essential for high-volume scanning, supporting their dominance in the industry.

Clinics are the fastest-growing segment, fueled by the shift toward ambulatory care and preventive diagnostics. Clinics benefit from portable handheld devices for quick, on-site imaging in applications such as gynecology and radiology. The increasing prevalence of outpatient procedures and advancements in affordable equipment are driving the rapid adoption of this segment, particularly in developed markets.

Application Insights

Radiology leads the medical ultrasound equipment market, holding a 30% share in 2025. The segment’s dominance is driven by the global surge in diagnostic imaging needs, with ultrasound being a cornerstone for abdominal, musculoskeletal, and vascular assessments due to its safety and real-time capabilities. Major clinical guidelines, such as those from the American College of Radiology, recommend ultrasound as a first-line tool, further boosting its adoption.

The cardiology segment is the fastest-growing, driven by the increasing incidence of cardiovascular diseases globally, particularly among aging populations. According to the American College of Cardiology, heart disease affects over 18 million adults in the U.S. alone, with ultrasound playing a critical role in echocardiography for monitoring heart function. The growing demand for effective diagnostics in acute and chronic cardiac settings is accelerating the adoption of ultrasound in this segment.

Regional Insights

North America Medical Ultrasound Equipment Market Trends

North America, holding a 35% market share in 2025, dominates the global medical ultrasound equipment market due to its advanced healthcare infrastructure, strong medical device industry, and high disease prevalence. The region has a significant burden of chronic diseases, cardiovascular conditions, and cancer, which are key indications for ultrasound use.

According to the Centers for Disease Control and Prevention (CDC), heart disease is the leading cause of death in the U.S., and chronic conditions affect six in ten adults, driving demand for diagnostic imaging.

The U.S. market benefits from robust R&D investments and favorable regulatory environments from the FDA, facilitating rapid adoption of innovations such as AI-integrated and handheld devices. Trends include a shift toward point-of-care ultrasound in emergency departments and telemedicine integration amid post-pandemic healthcare digitization.

Additionally, government programs such as Medicare support reimbursement for ultrasound procedures, enhancing accessibility. The growing aging population, sedentary lifestyles, and rising obesity rates continue to fuel the demand for ultrasound equipment, solidifying North America’s position as the leading market for this device category in the forecast period.

Europe Medical Ultrasound Equipment Market Trends

Europe holds a significant share in the global medical ultrasound equipment market, driven by strong healthcare systems, advanced medical device manufacturing, and growing adoption of digital health. Leading countries include Germany, the UK, and France. Germany benefits from its robust medtech industry and leadership in imaging research, with companies such as Siemens Healthineers investing heavily in AI-enhanced ultrasound systems.

The UK’s market is bolstered by the rising prevalence of chronic diseases and government initiatives promoting early diagnostics through the NHS. France’s market is supported by significant investments in healthcare infrastructure and a focus on sustainable medical practices.

The EU’s stringent regulations, such as the Medical Device Regulation (MDR), drive the adoption of high-quality ultrasound equipment, though compliance with complex standards poses challenges. Europe’s medical ultrasound equipment market is projected to grow steadily from 2025 to 2032.

Asia Pacific Medical Ultrasound Equipment Market Trends

Asia Pacific is emerging as one of the fastest-growing regions in the medical ultrasound equipment market, fueled by rapid urbanization, increasing healthcare expenditure, and rising awareness of preventive diagnostics. The region is witnessing a surge in lifestyle-related conditions such as cardiovascular diseases, diabetes, and gynecological disorders, driven by changing dietary habits, sedentary lifestyles, and aging populations.

Countries such as China, India, and Japan are investing heavily in healthcare infrastructure, improving access to diagnostics and treatment options. Growing government initiatives to promote early detection and management of chronic diseases are further driving demand for ultrasound equipment.

According to the World Health Organization (WHO), Asia is home to a large proportion of the global population with cardiovascular risks, making it a significant target market for ultrasound devices. Rising healthcare spending, expanding medtech manufacturing capabilities, and the availability of affordable portable systems are enhancing market accessibility.

Additionally, increasing patient education and awareness campaigns about the benefits of non-invasive imaging are encouraging adoption, positioning the Asia Pacific as a key growth engine for the medical ultrasound equipment market in the coming years.

Competitive Landscape

The global medical ultrasound equipment market is characterized by intense competition, regional strengths, and a mix of global and local medical device manufacturers.

In developed regions such as North America and Europe, large firms such as GE Healthcare, Koninklijke Philips N.V., and Siemens Healthineers dominate through scale, advanced R&D capabilities, and established partnerships with healthcare providers. In the Asia Pacific, rapid growth in healthcare infrastructure and cost-effective production is attracting significant investments from both local and international players.

Companies are focusing on innovation, cost-efficiency, and strategic alliances to gain a competitive edge. The development of novel portable systems and AI integrations has emerged as a key differentiator, enabling faster market penetration and improved diagnostic outcomes.

Strategic partnerships and acquisitions are further intensifying the competitive landscape. Overall, the sector shows a dual nature consolidated at the top by global giants such as GE Healthcare and Philips, while fragmented and scattered across numerous regional and specialized manufacturers such as Mindray Medical International Limited in China, which actively supplies affordable ultrasound equipment to emerging markets.

Key Developments

- In July 2023, Canon Medical Systems introduced two compact ultrasound systems, Aplio flex and Aplio Go, which combine AI-enhanced imaging (such as Auto IMT and Auto EF) with a lightweight, maneuverable design suited for both cart-based and mobile applications. These platforms are aimed at improving diagnostic efficiency in settings such as cardiology and radiology for hospitals and clinics.

- In January 2025, GE HealthCare received FDA 510(k) clearance for its Voluson Expert Series ultrasound systems, which incorporate high-resolution imaging, advanced technologies, and AI-based automation to enhance women’s health diagnostics and streamline clinical workflows.

Companies Covered in Medical Ultrasound Equipment Market

- Canon Medical Systems Corporation

- GE Healthcare

- Koninklijke Philips N.V.

- Terason

- Mindray Medical International Limited

- Hitachi Ltd.

- Siemens Healthineers

- Esaote S.p.A.

- Samsung Medison Co., Ltd.

- Fujifilm Holdings Corporation

- Neusoft Corporation

- CHISON Medical Technologies Co., Ltd.

- Others

Frequently Asked Questions

The global medical ultrasound equipment market is projected to reach US$ 9.9 Bn in 2025.

The rising prevalence of chronic diseases and an aging population a key driver.

The medical ultrasound equipment market is poised to witness a CAGR of 4.2% from 2025 to 2032.

Advancements in portable and AI-integrated technologies are a key opportunity.

Canon Medical Systems Corporation, GE Healthcare, Koninklijke Philips N.V., Siemens Healthineers, and Mindray Medical International Limited are key players.