- Medical Devices

- Medical Electrodes Market

Medical Electrodes Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Global Medical Electrodes Market by Product (Diagnostics and Therapeutics), by Usage (Disposable Electrodes and Reusable Electrodes), by Application (Cardiology, Neurology, Home Healthcare, and Others) by End User (Hospitals & Clinics, Home Healthcare Providers, Ambulatory Care Centers, Research & Academic Institutes, and Others), and Regional Analysis from 2026 to 2033

Medical Electrodes Market Size and Share Analysis

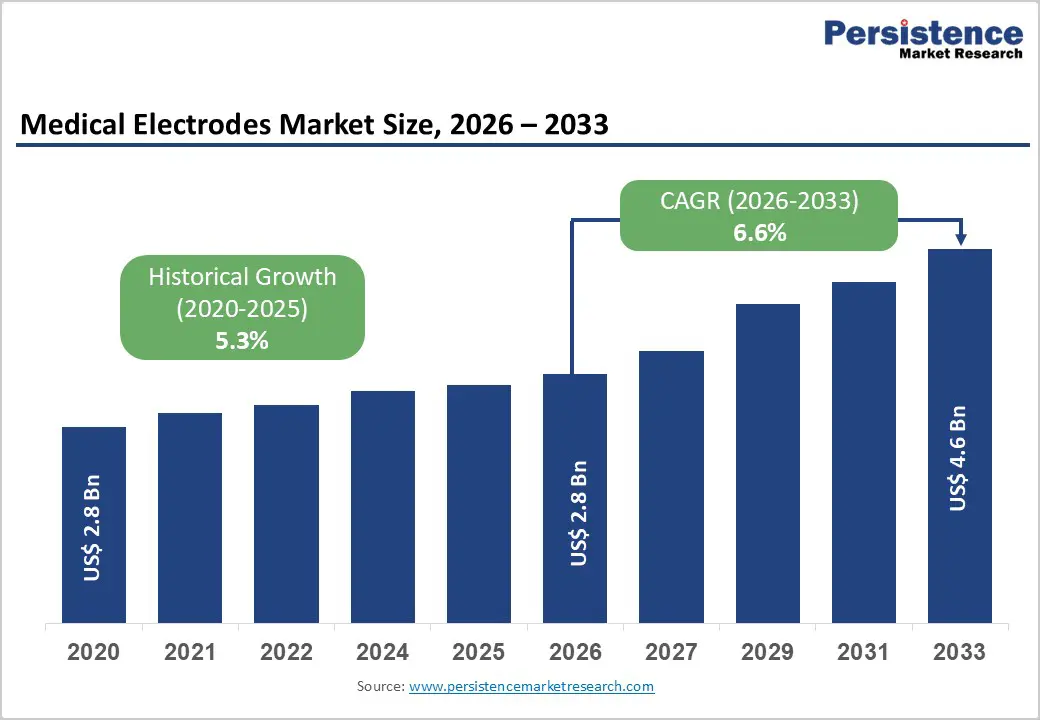

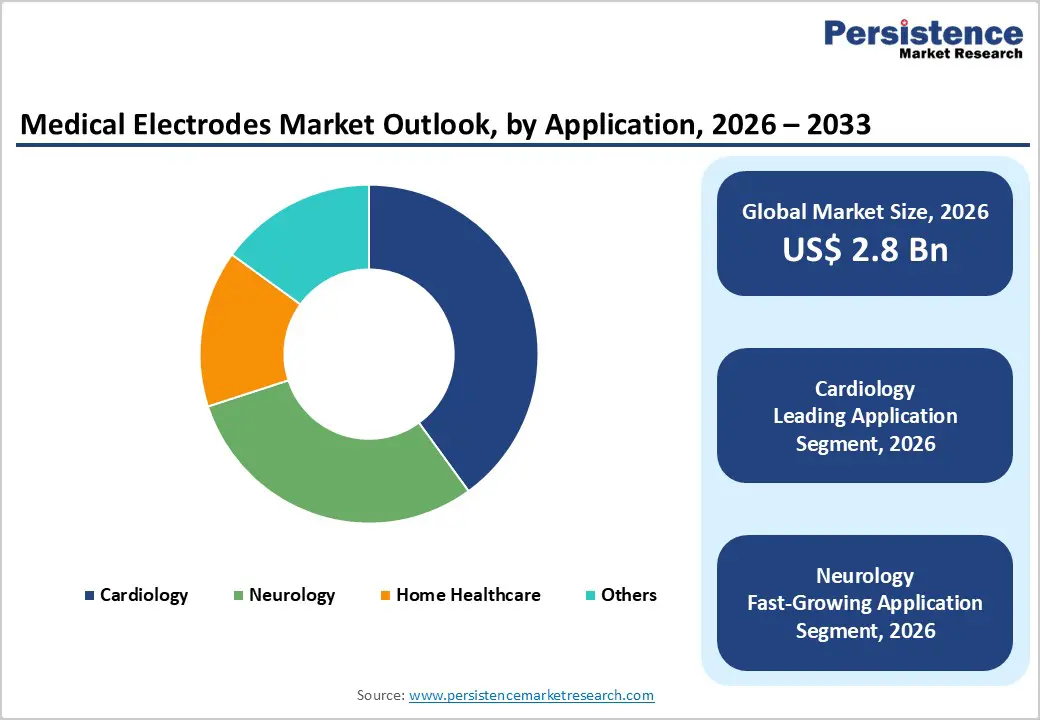

The global medical electrodes market size is estimated to grow from US$ 2.8 Bn in 2026 to US$ 4.6 Bn by 2033. The market is projected to record a CAGR of 6.4% during the forecast period from 2026 to 2033.

Global demand for medical electrodes is increasing steadily, driven by the rising prevalence of cardiovascular and neurological disorders, growing need for continuous patient monitoring, and expanding adoption of diagnostic and therapeutic electrophysiology procedures. Increasing use of ECG, EEG, and EMG systems across hospitals, ambulatory care, and home healthcare settings is supporting sustained market growth. Higher volumes of chronic disease management, emergency care monitoring, and elective diagnostic assessments, coupled with rising healthcare expenditure and improved access to monitoring technologies, are further accelerating demand. Continuous innovation in electrode materials, including skin-friendly adhesives, flexible substrates, and high-signal conductive coatings, is improving signal accuracy, patient comfort, and clinical reliability. Additionally, the growing focus on wearable devices, remote patient monitoring, and digitally integrated healthcare workflows is further propelling the global medical electrodes market.

Key Industry Highlights

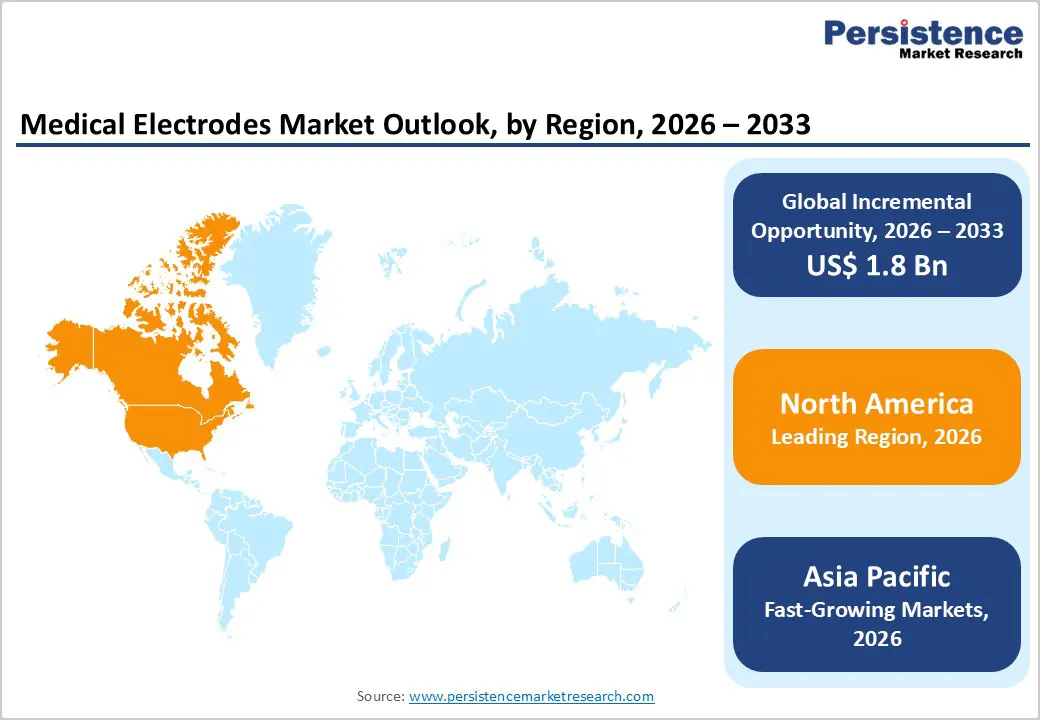

- Leading Region: North America holds the largest share at 46.7%, supported by advanced healthcare infrastructure, high adoption of cardiac and neurological monitoring technologies, early uptake of wearable and remote monitoring solutions, and the strong presence of leading medical device manufacturers.

- Fastest-Growing Region: Asia Pacific is expanding fastest due to a large chronic disease patient base, rapid growth in diagnostic and monitoring centers, improving healthcare infrastructure, and rising investments in digital and home-based care.

- Leading Product Segment: Diagnostics dominate the market due to their broad applicability across ECG, EEG, EMG, routine screening, and continuous patient monitoring applications.

- Fastest-Growing Product Segment: Therapeutics are expanding rapidly as adoption increases for neurostimulation, pain management, and rehabilitation-related electrode-based therapies.

- Leading Application Segment: Cardiology remains the top application, driven by widespread use of electrodes in cardiac monitoring, arrhythmia detection, and emergency care.

- Fastest-Growing Application Segment: Neurology is scaling quickly as demand rises for EEG monitoring, epilepsy diagnosis, neurocritical care, and long-term neurological assessments.

| Report Attribute | Details |

|---|---|

|

Medical Electrodes Market Size (2026E) |

US$ 2.8 Bn |

|

Market Value Forecast (2033F) |

US$ 4.6 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

6.4% |

|

Historical Market Growth (CAGR 2020 to 2025) |

5.2% |

Market Dynamics

Driver – Rising Prevalence of Cardiovascular and Neurological Disorders Coupled with Advancements in Electrode Technologies

The global medical electrodes market is strongly driven by the rising prevalence of cardiovascular and neurological disorders, which require continuous and accurate physiological monitoring. Conditions such as coronary artery disease, arrhythmias, epilepsy, stroke, and neurodegenerative disorders are increasing globally due to aging populations, sedentary lifestyles, and growing metabolic disease burden. According to global health agencies, cardiovascular diseases remain the leading cause of mortality worldwide, significantly increasing demand for ECG-based diagnostics and long-term cardiac monitoring. Medical electrodes serve as a core component in ECG, EEG, EMG, and patient monitoring systems used across hospitals, ambulatory care, and emergency settings.

Additionally, technological advancements in electrode materials and design are accelerating market adoption. Innovations such as silver/silver chloride (Ag/AgCl) coatings, hydrogel-based adhesives, and dry electrode technologies are improving signal quality, skin compatibility, and patient comfort. The emergence of wireless, wearable, and flexible electrodes is further expanding applications in remote monitoring and home healthcare. These advancements reduce motion artifacts, enable longer monitoring durations, and support integration with digital health platforms. Together, the increasing clinical need for continuous monitoring and rapid technological evolution is driving sustained growth of the global medical electrodes market.

Restraints – High Device Costs, Reusability Concerns, and Risk of Skin-Related Complications

High costs associated with advanced medical electrodes and monitoring systems represent a key restraint limiting broader market adoption. Premium disposable electrodes with enhanced materials, long-wear capabilities, and wireless compatibility are significantly more expensive than conventional alternatives. In large-volume hospital settings, recurring expenditure on disposable electrodes adds substantial operational costs, particularly in resource-constrained healthcare systems. Reusable electrodes, while cost-efficient over time, require strict cleaning and sterilization protocols, increasing labor and compliance burdens for healthcare providers.

Additionally, reimbursement policies for diagnostic monitoring procedures vary widely across regions, limiting adoption in price-sensitive markets and low- and middle-income countries. Inconsistent coverage for long-term or preventive monitoring further restricts penetration of advanced electrode solutions. Clinical concerns also remain regarding skin irritation, allergic reactions, and contact dermatitis caused by prolonged electrode use, especially among elderly and critically ill patients. Poor adhesion, signal degradation, and motion-related artifacts can compromise diagnostic accuracy and clinician confidence. These challenges may lead to frequent electrode replacement or reliance on lower-cost alternatives. Collectively, cost pressures, operational challenges, and patient safety considerations act as moderating factors on the growth trajectory of the global medical electrodes market.

Opportunity – Expansion of Wearable, Home-Based, and Digitally Integrated Monitoring Solutions

The medical electrodes market presents strong growth opportunities driven by the rapid expansion of wearable health technologies, home-based monitoring, and digitally enabled care models. Increasing adoption of remote patient monitoring for chronic disease management, post-operative care, and elderly populations is significantly expanding demand for compact, comfortable, and long-duration electrodes. Wearable ECG patches, ambulatory EEG devices, and continuous cardiac monitoring systems rely heavily on advanced electrode designs optimized for extended use outside clinical settings.

Advancements in flexible electronics, textile-based electrodes, and dry electrode technologies are enabling seamless integration into wearable devices, improving patient compliance and data reliability. These innovations reduce the need for conductive gels and frequent replacement, enhancing usability in home healthcare environments. Furthermore, integration of medical electrodes with artificial intelligence, cloud-based analytics, and telehealth platforms is improving early disease detection and clinical decision-making. Growing investments in digital health infrastructure and increasing acceptance of telemedicine across both developed and emerging markets are accelerating adoption. As healthcare systems shift toward value-based care and preventive monitoring, next-generation medical electrodes compatible with digital ecosystems represent a significant long-term growth opportunity for manufacturers.

Category-wise Analysis

By Product, Diagnostics Lead Due to High Volume Use in Continuous Monitoring and Imaging Procedures

The diagnostics segment is projected to dominate the global medical electrodes market in 2026, accounting for a revenue share of 52.0%. This leadership is primarily attributed to the extensive use of diagnostic electrodes across electrocardiography (ECG), electroencephalography (EEG), electromyography (EMG), and other routine and critical monitoring applications. Diagnostic electrodes are widely utilized in cardiology, neurology, emergency care, and perioperative monitoring due to their non-invasive nature, cost-effectiveness, and compatibility with a broad range of monitoring systems. Rising prevalence of cardiovascular and neurological disorders, increasing hospital admissions, and growing demand for real-time patient monitoring are reinforcing segment dominance. In addition, the expanding adoption of wearable diagnostic devices, remote patient monitoring solutions, and home-based diagnostic systems is further accelerating demand. Continuous innovation in skin-friendly materials, enhanced signal quality, and single-use disposable formats continues to support sustained leadership of the diagnostics segment.

By Application, Cardiology Dominates Due to Extensive Use in Cardiac Monitoring and Emergency Care

The cardiology segment is projected to dominate the global medical electrodes market in 2026, accounting for a revenue share of 40.0%. This dominance is driven by the widespread use of medical electrodes in ECG monitoring, cardiac stress testing, arrhythmia detection, and continuous cardiac surveillance across acute and chronic care settings. Cardiovascular diseases remain one of the leading causes of mortality globally, resulting in consistently high procedure volumes and routine monitoring requirements. Medical electrodes are essential components in both inpatient and outpatient cardiology workflows, including emergency departments, intensive care units, and ambulatory diagnostic centers. Increasing adoption of long-term cardiac monitoring devices, such as Holter monitors and wearable ECG systems, further supports segment growth. Technological advancements focused on improved signal accuracy, reduced motion artifacts, and enhanced patient comfort are also strengthening adoption. High repeat usage rates and integration with digital cardiac monitoring platforms continue to reinforce cardiology’s leading market position.

By End User, Hospitals Lead Due to High Patient Throughput and Advanced Monitoring Infrastructure

The hospitals segment is projected to dominate the global medical electrodes market in 2026, accounting for a revenue share of 45.0%. This dominance is largely driven by the high volume of diagnostic and therapeutic procedures performed in hospital settings, including cardiac monitoring, neurological assessments, and critical care surveillance. Hospitals are equipped with advanced patient monitoring systems, intensive care units, and emergency departments that rely heavily on continuous electrode-based monitoring. Availability of skilled clinicians, access to sophisticated diagnostic equipment, and capacity to manage complex and high-acuity cases further reinforce hospital leadership. In addition, hospitals typically maintain long-term procurement contracts with electrode manufacturers, enabling large-scale and recurring purchases. The increasing burden of chronic diseases, rising surgical admissions, and growing emphasis on patient safety and continuous monitoring are further strengthening demand. Adoption of disposable electrodes to reduce infection risk and support hospital hygiene protocols also contributes significantly to revenue generation.

Region-wise Insights

North America Medical Electrodes Market Trends

North America is expected to dominate the global medical electrodes market with a value share of 46.7% in 2026, led primarily by the United States. The region benefits from a well-established healthcare infrastructure, high adoption of advanced patient monitoring technologies, and strong prevalence of cardiovascular and neurological disorders. Hospitals and diagnostic centers across North America routinely deploy ECG, EEG, and EMG systems, driving consistent demand for high-quality medical electrodes. The region also demonstrates early adoption of wearable health technologies and remote patient monitoring solutions, further expanding electrode utilization beyond traditional hospital settings.

Favorable reimbursement frameworks for diagnostic and monitoring procedures support widespread use of premium and disposable electrodes. Additionally, the strong presence of leading medical device manufacturers, continuous product innovation, and rigorous quality standards enhance market penetration. Ongoing investments in digital health, telemedicine expansion, and home healthcare services are further reinforcing market growth. Well-defined regulatory pathways and strong clinician awareness ensure sustained dominance of the North American market.

Europe Medical Electrodes Market Trends

The Europe medical electrodes market is expected to grow steadily, supported by an aging population, increasing prevalence of chronic cardiovascular and neurological conditions, and rising demand for diagnostic monitoring. Countries such as Germany, the U.K., France, Italy, and the Nordic nations exhibit consistent utilization of medical electrodes due to strong public healthcare systems and broad access to diagnostic services. Growing awareness of preventive healthcare and early disease detection is driving routine ECG and neurological monitoring across hospitals and outpatient settings.

Europe is also witnessing increased adoption of disposable electrodes to meet stringent infection control and patient safety standards. Technological advancements in electrode materials, including hypoallergenic and long-wear designs, are improving patient compliance and clinical outcomes. Supportive regulatory policies for medical device innovation, combined with expanding healthcare budgets, continue to facilitate market growth. Integration of digital monitoring platforms, standardized clinical protocols, and expanding home healthcare services further enhance adoption across the region.

Asia Pacific Medical Electrodes Market Trends

The Asia Pacific medical electrodes market is expected to register a relatively higher CAGR of around 8.7% between 2026 and 2033, driven by rapid expansion of healthcare infrastructure and increasing diagnostic volumes. Large patient populations, rising incidence of cardiovascular diseases, and growing awareness of neurological disorders are fueling demand across China, India, Japan, and South Korea. Improving access to hospital-based diagnostics, expanding private healthcare facilities, and rising penetration of diagnostic imaging and monitoring equipment are accelerating electrode adoption.

Government initiatives aimed at strengthening healthcare delivery, increasing insurance coverage, and modernizing hospitals are further supporting market growth. In addition, cost-sensitive markets are driving demand for affordable and locally manufactured electrode solutions. Growing adoption of telemedicine, remote patient monitoring, and wearable health devices is expanding use in home healthcare settings. Strategic expansion by global manufacturers, localization of production, and increasing clinician training are strengthening long-term growth prospects across the Asia Pacific region.

Market Competitive Landscape

The global medical electrodes market is highly competitive, with strong participation from companies such as 3M Company, Medtronic, GE HealthCare, Abbott Laboratories, and Cardinal Health. These players leverage extensive global distribution networks, strong brand recognition, and continuous innovation across electrode materials, signal acquisition technologies, and device compatibility to address a wide range of diagnostic and therapeutic requirements.

Rising demand for cardiovascular and neurological monitoring, long-term patient surveillance, and home-based care is driving product innovation and portfolio expansion. Manufacturers are increasingly focusing on disposable and wearable electrode designs, improved skin-friendly materials, and integration with digital and wireless monitoring platforms. Strategic priorities include strengthening hospital and diagnostic center partnerships, expanding presence in emerging markets, and investing in R&D to support advanced monitoring solutions and sustain long-term market growth.

Key Industry Developments:

- In January 2026, Enterra Medical, Inc. announced the launch of Enterra ReliaStim®, a next-generation stimulation lead developed to improve the precision, consistency, and efficiency of Gastric Electrical Stimulation (GES) lead placement. Designed and manufactured in-house, Enterra ReliaStim underscores the company’s continued investment in advancing GES technology. The product represents a key step in Enterra Medical’s strategic evolution from a single-therapy provider toward a broader platform of innovative treatment solutions aimed at improving outcomes for patients suffering from chronic nausea and vomiting.

- In January 2026, AliveCor announced that it received FDA clearance for the next generation of its AI-powered technology integrated into the Kardia 12L ECG system. The enhanced AI capabilities are designed to improve diagnostic accuracy and streamline ECG interpretation for clinicians across hospital and outpatient settings.

- In January 2026, Naox Technologies received U.S. Food and Drug Administration (FDA) 510(k) clearance for NAOX LINK (NX01). This regulatory approval represents a significant advancement in the delivery and accessibility of electroencephalography (EEG), enabling more efficient, flexible, and scalable EEG monitoring across clinical practice.

Companies Covered in Medical Electrodes Market

- 3M Company

- Medtronic

- GE HealthCare

- Abbott Laboratories

- Cardinal Health

- Nihon Kohden Corporation

- Philips Healthcare

- Natus Medical Incorporated

- Boston Scientific Corporation

- ConMed Corporation

- BD

- Compumedics Limited

- VectraCor

- Others

Frequently Asked Questions

The global medical electrodes market is projected to be valued at US$ 2.8 Bn in 2026.

The global medical electrodes market is driven by the rising prevalence of chronic diseases (especially cardiovascular and neurological disorders), growing geriatric population requiring continuous monitoring, and rapid technological advancements including wearable, miniaturized, and wireless electrodes that enhance diagnostic and therapeutic capabilities.

The global medical electrodes market is poised to witness a CAGR of 6.4% between 2026 and 2033.

Expanding adoption of wearable and remote monitoring solutions for home healthcare and telemedicine presents significant growth opportunities.

3M Company, Medtronic, GE HealthCare, Abbott Laboratories, Cardinal Health, are some of the key players in the medical electrodes market.