- Specialty & Fine Chemicals

- Liquid Sodium Silicate Market

Liquid Sodium Silicate Market Size, Share, and Growth Forecast 2025 - 2032

Liquid Sodium Silicate Market By Molar Ratio (1.6 to 2.8 (Alkaline), 2.8 to 3.3 (Neutral)), Application (Cement & Binder, Cleaning and Detergents, Water Treatment, Paper Production, Petroleum Processing, Others), and Regional Analysis for 2025 - 2032

Liquid Sodium Silicate Market Size and Trends Analysis

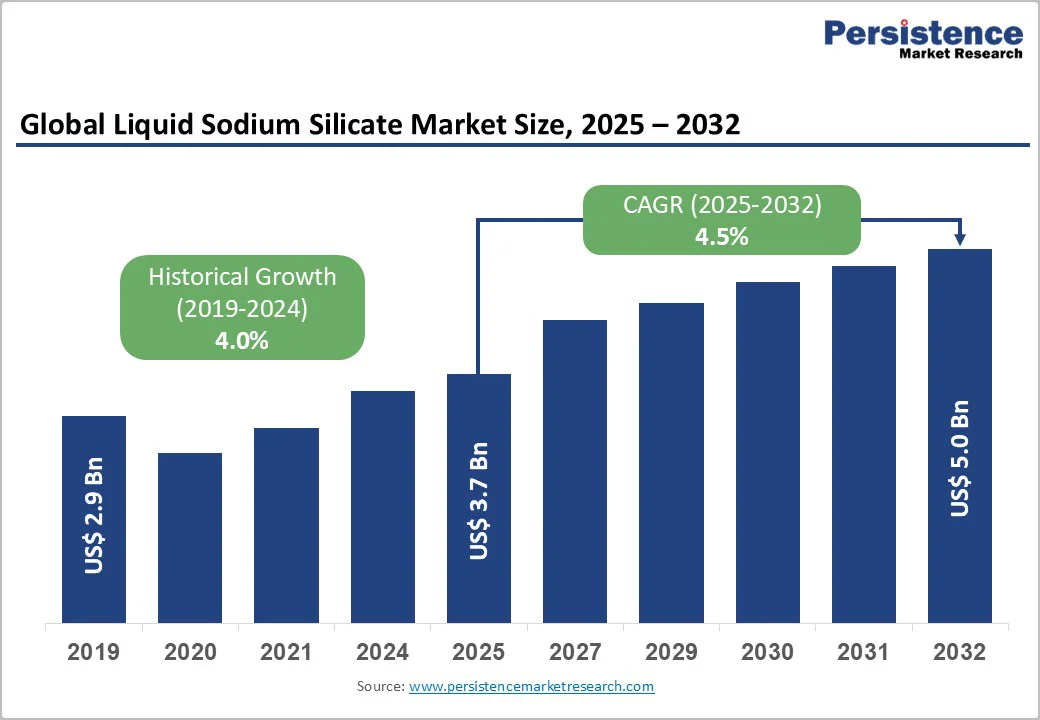

The global liquid sodium silicate market size was valued at US$3.7 Billion in 2025 and is projected to reach US$5.0 Billion by 2032, growing at a CAGR of 4.5% between 2025 and 2032, driven by increasing demand from construction and infrastructure development activities, expanding applications in cleaning and detergent industries, and rising adoption in water treatment processes for industrial and municipal applications. The market is boosted by rising environmental awareness, advances in sodium silicate technology, and growing demand in the petroleum and metal industries for high-performance binding and sealing solutions.

Key Market Highlights

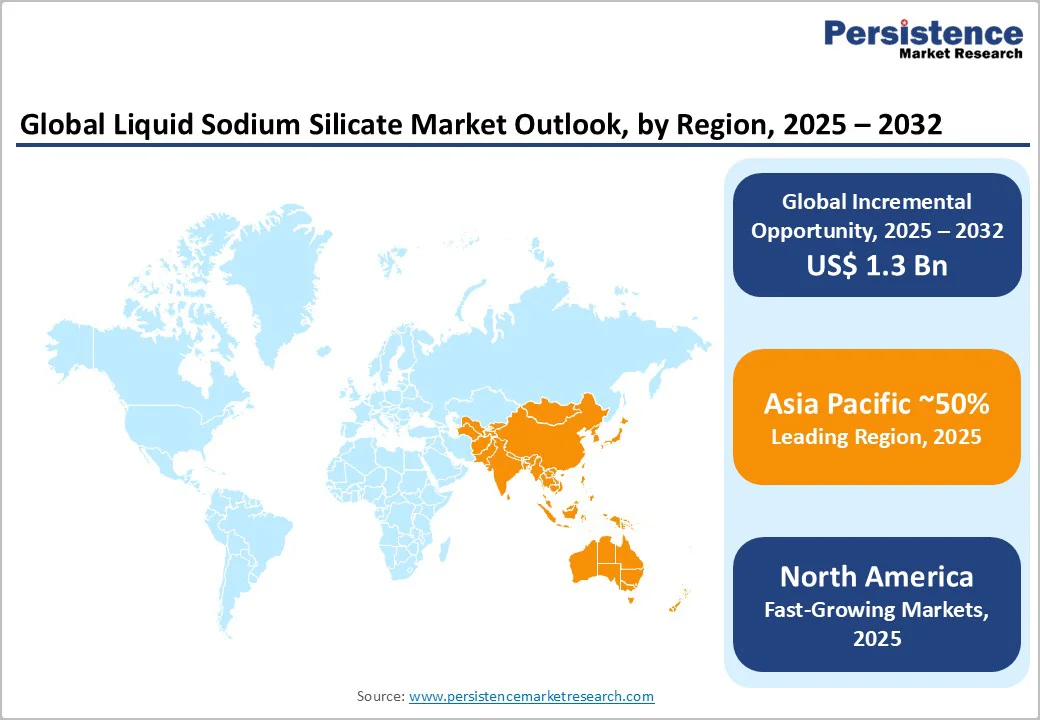

- Leading Region: Asia Pacific leads global liquid sodium silicate consumption with 50% market share, driven by rapid industrialization, infrastructure development, and expanding manufacturing capabilities across China, India, and ASEAN countries.

- Growing Region: North America emerges as the fastest-growing regional market supported by infrastructure investments, environmental regulations, and advanced manufacturing technologies, creating new demand opportunities across multiple industrial sectors.

- Dominant Molar Ratio: 1.6 to 2.8 (Alkaline) molar ratio dominates market segments with 65% share due to optimal alkalinity balance providing superior performance across construction, detergent, and industrial applications.

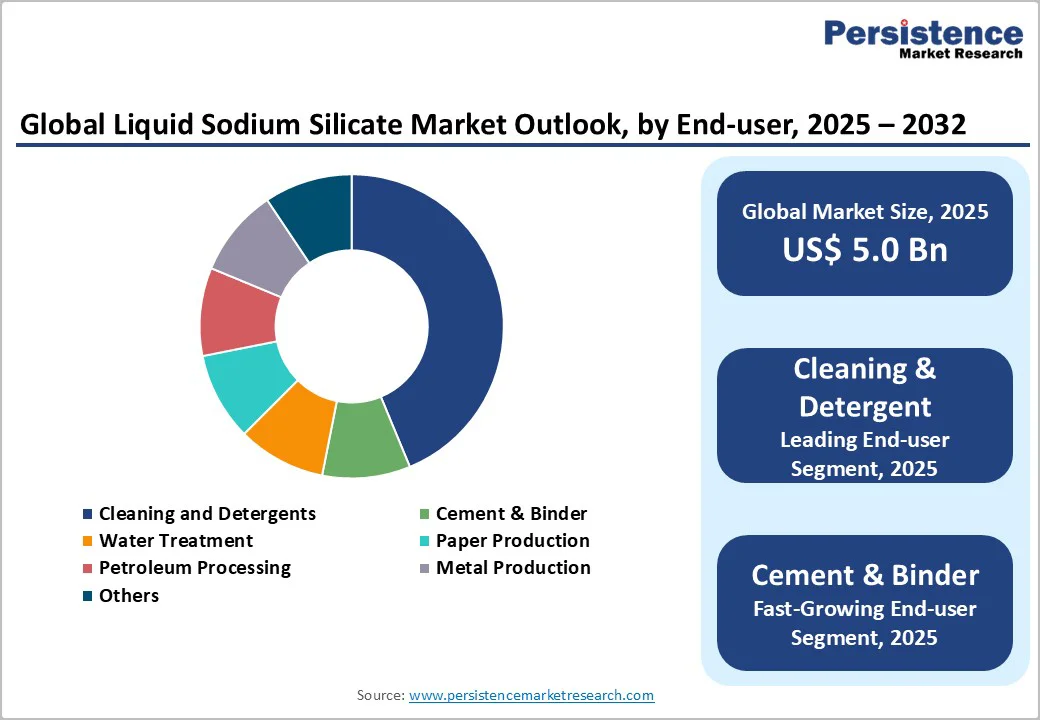

- Dominant Application: Cleaning and Detergents represents the dominant application segment with 40% share driven by rising hygiene awareness, urbanization trends, and increasing adoption of phosphate-free detergent formulations.

- Key Opportunity: Water treatment applications offer a major growth opportunity supported by global water scarcity concerns, environmental regulations, and expanding industrial treatment requirements across multiple sectors.

| Key Insights | Details |

|---|---|

|

Liquid Sodium Silicate Market Size (2025E) |

US$3.7 Bn |

|

Market Value Forecast (2032F) |

US$5.0 Bn |

|

Projected Growth CAGR(2025-2032) |

4.5% |

|

Historical Market Growth (2019-2024) |

4.0% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Rapid Expansion of Construction and Infrastructure Development Activities

The global construction industry’s unprecedented growth is fundamentally driving liquid sodium silicate demand, with infrastructure investments reaching US$94 Trillion globally by 2040, according to the Global Infrastructure Outlook. Liquid sodium silicate serves as a crucial binding agent and concrete hardener in construction applications, with the compound’s alkaline properties providing superior strength enhancement and acid resistance to cement and mortar formulations. The United States Infrastructure Investment and Jobs Act allocates US$1.2 Trillion for infrastructure improvements, creating substantial demand for construction chemicals, including liquid sodium silicate products.

China’s 14th Five-Year Plan emphasizes urban development and green construction practices, with investments exceeding US$4.2 Trillion in infrastructure projects requiring high-performance binding agents and waterproofing solutions. The compound’s ability to reduce concrete permeability by up to 30% while increasing compressive strength makes it essential for modern construction applications, including high-rise buildings, bridges, and underground structures.

Growing Demand from Cleaning and Detergent Industries

The detergent chemicals market is expanding rapidly due to rising hygiene awareness, urbanization, and higher disposable incomes in emerging economies, driving liquid sodium silicate demand. Serving as a key alkaline builder, it enhances grease removal, soil suspension, and anti-redeposition properties in detergents. Asia Pacific, led by India and Southeast Asia, records 6–8% annual growth fueled by growing middle-class populations. Liquid sodium silicate’s ability to soften hard water and support phosphate-free formulations aligns with environmental regulations and sustainability trends, expanding its adoption across residential and industrial cleaning applications in both developing and developed markets.

Barrier Analysis - High Production Costs and Energy-Intensive Manufacturing Processes

Liquid sodium silicate manufacturing faces significant cost pressures from energy-intensive production processes requiring furnace temperatures exceeding 1,400°C for melting silica sand and sodium carbonate, resulting in substantial energy consumption representing 60-70% of total production costs. Global energy price volatility has increased manufacturing costs by 15-25% since 2020, particularly impacting European and North American producers facing supply chain disruptions and regulatory compliance requirements. The production process demands specialized equipment, continuous furnace operations, and skilled technical personnel, creating barriers for new market entrants and limiting production scalability in regions with high energy costs or inadequate infrastructure.

Environmental Regulations and Handling Safety Concerns

The liquid sodium silicate industry faces increasing regulatory scrutiny due to the compound’s highly alkaline nature, with pH levels ranging from 11 to 13, requiring specialized handling procedures and safety protocols that increase operational complexity and compliance costs. OSHA regulations in the U.S. mandate extensive worker protection measures, specialized storage requirements, and emergency response protocols for alkaline solutions, increasing operational costs and liability concerns for manufacturers and end-users. Growing environmental awareness regarding industrial chemical disposal and water contamination creates regulatory pressures that may limit market expansion in regions with stringent environmental protection standards.

Opportunity Analysis - Expanding Water Treatment Applications and Environmental Compliance Requirements

The water & wastewater treatment chemicals market presents significant growth opportunities for liquid sodium silicate, driven by increasing global water scarcity, stricter environmental regulations, and expanding industrial water treatment requirements. Liquid sodium silicate functions as an effective coagulant and flocculant in water treatment processes, helping remove suspended particles, heavy metals, and organic contaminants while providing corrosion protection for treatment equipment.

According to the World Health Organization, over 2 billion people lack access to safely managed drinking water, creating substantial demand for effective water treatment solutions that can operate in diverse geographic and economic conditions. Municipal water treatment facilities are increasingly adopting liquid sodium silicate for pH adjustment, corrosion control, and metal sequestration applications, with typical dosage rates ranging from 1-10 mg/L for drinking water treatment and 15-50 mg/L for industrial applications. The compound’s effectiveness in removing iron, manganese, and other heavy metals at concentrations four to five times the contamination levels makes it particularly valuable for treating challenging water sources in emerging markets.

Emerging Applications in Petroleum Processing and Advanced Industrial Processes

The petroleum and petrochemical industries represent high-growth application areas for liquid sodium silicate, driven by increasing energy demand, complex processing requirements, and enhanced oil recovery techniques requiring specialized chemical solutions. Liquid sodium silicate serves multiple functions in petroleum processing, including drilling fluid stabilization, wellbore strengthening, corrosion inhibition, and emulsion breaking applications that are essential for modern oil and gas extraction operations. The shale oil and gas industry utilizes liquid sodium silicate in hydraulic fracturing fluids and wellbore consolidation applications, with the U.S. shale production reaching 11.9 million barrels per day in 2024, creating substantial demand for specialized chemical additives.

Advanced applications in geothermal energy extraction and carbon capture and storage technologies present emerging opportunities where liquid sodium silicate’s unique properties provide superior performance in extreme temperature and pressure conditions. The compound’s effectiveness as a sealant and stabilizing agent in underground applications, combined with its environmental compatibility compared to synthetic alternatives, positions it favorably for expansion in sustainable energy applications requiring reliable chemical performance under challenging operational conditions.

Category-wise Analysis

Molar Ratio Insights

The 1.6 to 2.8 (Alkaline) molar ratio segment dominates the liquid sodium silicate market with 65% market share in 2025, primarily due to its optimal balance between alkalinity and silica content that provides superior performance across diverse industrial applications. This molar ratio range offers the ideal combination of strong alkaline properties with pH levels between 12-13 while maintaining adequate silica content for effective binding and sealing applications. The segment’s dominance stems from its widespread adoption in detergent formulations where alkaline sodium silicate provides excellent grease emulsification, soil suspension, and anti-corrosion properties essential for high-performance cleaning products.

Construction applications favor this molar ratio due to its ability to enhance concrete strength by 25-30% while providing superior acid resistance and waterproofing capabilities compared to neutral formulations. The alkaline segment benefits from growing demand in water treatment applications where higher alkalinity levels enable effective metal sequestration, pH adjustment, and coagulation enhancement processes. Manufacturing efficiency advantages include lower energy requirements for dissolution and improved storage stability compared to higher ratio formulations, reducing operational costs for end-users while maintaining consistent product performance across diverse application requirements.

Application Insights

Cleaning and detergents represent the dominant application segment with approximately 40% market share in 2025, reflecting the essential role of liquid sodium silicate in modern detergent formulations and cleaning product development. This leadership position stems from liquid sodium silicate’s multifunctional benefits, including alkaline buffering, soil suspension, anti-redeposition properties, and corrosion protection for washing equipment and metal surfaces.

The detergent chemicals market continues expanding globally, with household and industrial cleaning products incorporating liquid sodium silicate at concentrations ranging from 5-15% by weight to optimize cleaning performance and product stability. The segment benefits from increasing consumer awareness of hygiene and cleanliness, particularly following the COVID-19 pandemic impacts that elevated demand for effective cleaning solutions across residential, commercial, and industrial sectors.

Industrial and institutional cleaning applications represent high-growth subsegments where liquid sodium silicate provides superior degreasing capabilities, alkaline cleaning power, and equipment protection essential for food processing, healthcare, and manufacturing facilities. The segment’s growth is further supported by regulatory trends favoring phosphate-free detergent formulations, where liquid sodium silicate serves as an effective builder and stabilizing agent that maintains cleaning efficacy while meeting environmental compliance requirements.

Regional Insights

North America Liquid Sodium Silicate Market Trends

North America demonstrates robust market growth as the fastest-growing regional market, supported by advanced industrial infrastructure, comprehensive regulatory frameworks, and substantial investments in infrastructure development and environmental protection initiatives. The U.S. leads regional consumption through diverse industrial applications, including construction, detergents, water treatment, and petroleum processing, with market leadership reinforced by the presence of major manufacturers such as OxyChem Corporation, PQ Corporation, and W.R. Grace & Company.

The Infrastructure Investment and Jobs Act provides substantial federal funding for construction and water treatment projects that will drive liquid sodium silicate demand across multiple applications, including concrete enhancement, corrosion protection, and water purification systems. Advanced manufacturing technologies and Industry 4.0 implementations enable North American producers to maintain competitive advantages through improved production efficiency, quality control, and custom product development capabilities.

Europe Liquid Sodium Silicate Market Trends

European liquid sodium silicate markets exhibit consistent growth driven by comprehensive EU regulatory frameworks promoting sustainable chemistry, environmental protection, and worker safety across member states. The European Chemicals Agency (ECHA) provides harmonized registration and evaluation procedures under REACH regulations that ensure high safety standards while facilitating market access for compliant products. Germany, France, and the U.K. lead regional consumption through well-established chemical industries, advanced manufacturing sectors, and a strong emphasis on environmental sustainability and circular economy principles.

The region’s focus on green chemistry and sustainable industrial processes encourages liquid sodium silicate adoption due to its biodegradable nature, non-toxic properties, and effectiveness as an alternative to more hazardous chemical formulations. European manufacturers are investing in renewable energy integration and carbon footprint reduction initiatives that align with EU Green Deal objectives while maintaining competitive production capabilities. Progressive environmental standards, including water quality directives and industrial emissions regulations, create opportunities for liquid sodium silicate applications in pollution control, water treatment, and sustainable manufacturing processes that contribute to environmental protection goals.

Asia Pacific Liquid Sodium Silicate Market Trends

Asia Pacific dominates the market with 50% market share in 2025, driven by rapid industrialization, massive infrastructure development, and expanding manufacturing capabilities across China, India, Japan, and ASEAN countries. China represents the largest regional market, contributing over 35% of Asia Pacific consumption through extensive construction projects, industrial chemical production, and growing detergent manufacturing that requires substantial liquid sodium silicate input.

India’s rapidly expanding economy and infrastructure development programs, including Smart Cities Mission and Make in India initiatives, drive substantial demand for liquid sodium silicate across construction, textiles, and water treatment applications. The region’s manufacturing cost advantages, including competitive raw material access, lower labor costs, and established supply chain networks, support both domestic consumption and export capabilities to global markets. ASEAN countries demonstrate strong growth potential driven by economic development, urbanization trends, and increasing adoption of modern industrial processes that favor liquid sodium silicate applications in diverse manufacturing sectors, including automotive, electronics, and consumer goods industries.

Competitive Landscape

The global liquid sodium silicate market exhibits a moderately consolidated competitive structure with several established multinational players dominating through extensive production capabilities, technological expertise, and comprehensive distribution networks. BASF SE, Evonik Industries AG, and PQ Corporation maintain market leadership through diversified product portfolios, advanced manufacturing technologies, and strong customer relationships across multiple industrial sectors.

Market concentration is driven by significant capital requirements for production facilities, technical expertise in chemical processing, and established supply chain relationships that create barriers for new entrants. Companies pursue growth strategies through capacity expansion, geographic market penetration, strategic acquisitions, and development of specialized formulations serving specific customer requirements.

Key Industry Developments

- In January 2024, Evonik Industries announced plans to construct a new production line for precipitated silica at its Charleston site in South Carolina, USA. The construction is scheduled to begin in mid-2024, with operations expected to start in early 2026. This expansion is driven by strong market demand for silica in green tires in the U.S.

- In April 2024, PQ Corporation initiated an expansion of its Augusta, Georgia facility, which produces industrial-grade liquid sodium silicate, commonly known as "liquid glass." The company selected a Pennsylvania-based contractor to design and build the new production line, aiming to meet growing demand in construction and industrial applications.

- In October 2024, Evonik Industries commenced a significant expansion at its Charleston site in South Carolina, USA. This development aims to boost the production capacity of precipitated silica by 50%, catering to the increasing demand from the tire industry, particularly for green tires in the U.S.

Companies Covered in Liquid Sodium Silicate Market

- BASF SE

- Evonik Industries AG

- Glassven C.A.

- Kiran Global Chem Limited

- Nippon Chemical Industrial CO., LTD.

- Comfia Industries Pvt. Ltd

- MALPRO SILICA PRIVATE LTD.

- Solvay

- Aroma Chimie Company Limited

- Cerberus and Koch

- OxyChem Corporation

- W.R. Grace & Company

- Tokuyama Corporation

- PQ Corporation

- Occidental Petroleum Corporation

Frequently Asked Questions

The liquid sodium silicate market was valued at US$3.7 Billion in 2025 and is projected to reach US$5.0 Billion by 2032, representing a compound annual growth rate of 4.5% during the forecast period.

Key growth drivers include rapid expansion of construction and infrastructure development activities, growing demand from cleaning and detergent industries, expanding water treatment applications, and increasing adoption in petroleum processing and metal production industries.

The 1.6 to 2.8 (Alkaline) molar ratio segment dominates the market with 65% market share in 2025, driven by its optimal balance between alkalinity and silica content, providing superior performance across diverse industrial applications.

Asia Pacific leads the liquid sodium silicate market with 50% market share in 2025, primarily driven by rapid industrialization, massive infrastructure development, and expanding manufacturing capabilities across China, India, and ASEAN countries.

Water treatment applications represent a significant growth opportunity, supported by global water scarcity concerns, stricter environmental regulations, and expanding industrial water treatment requirements, creating demand for effective coagulation and corrosion protection solutions.

Major market players include BASF SE, Evonik Industries AG, PQ Corporation, OxyChem Corporation, W.R. Grace & Company, Tokuyama Corporation, Solvay, Nippon Chemical Industrial CO., LTD., and Glassven C.A.