- Food Ingredients & Additives

- Liquid Butter Alternative Market

Liquid Butter Alternative Market Size, Share and Growth Forecast, 2026 - 2033

Liquid Butter Alternative Market by Product Type (Plant-based oils, Nuts & Seeds Derived), Source (Vegetable- Based, Nut-Based), Application (Food Industry, Cosmetics, Personal Care), and Regional Analysis for 2026 - 2033

Liquid Butter Alternative Market Size and Trends Analysis

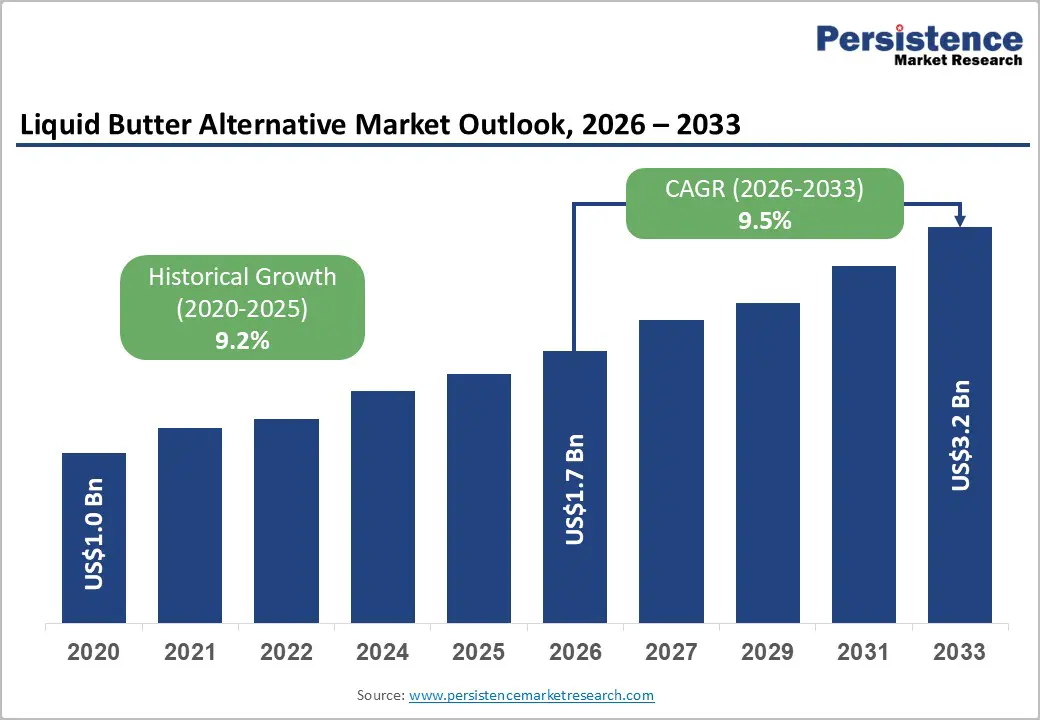

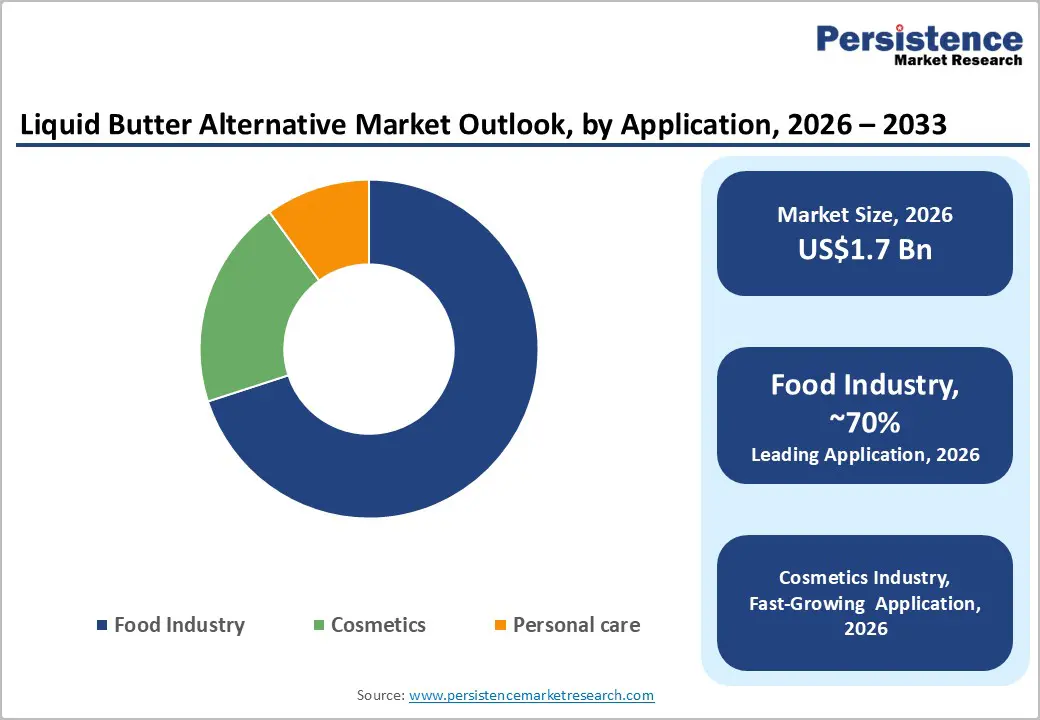

The global liquid butter alternative market size is likely to be valued at US$1.7 billion in 2026 and is projected to reach US$3.2 billion by 2033, growing at a CAGR of 9.5% during the forecast period from 2026 to 2033, driven by changing dietary habits, greater industrial use in food processing, and rising demand for functional fat alternatives in cosmetics and personal care products.

Heightened regulatory focus on trans fats, alongside advancements in plant-based oil processing technologies, is influencing product development strategies. From a business standpoint, long-term growth prospects remain robust, supported by scalable applications, diversified supply chains, and consistent consumer acceptance across both developed and emerging markets.

Key Industry Highlights:

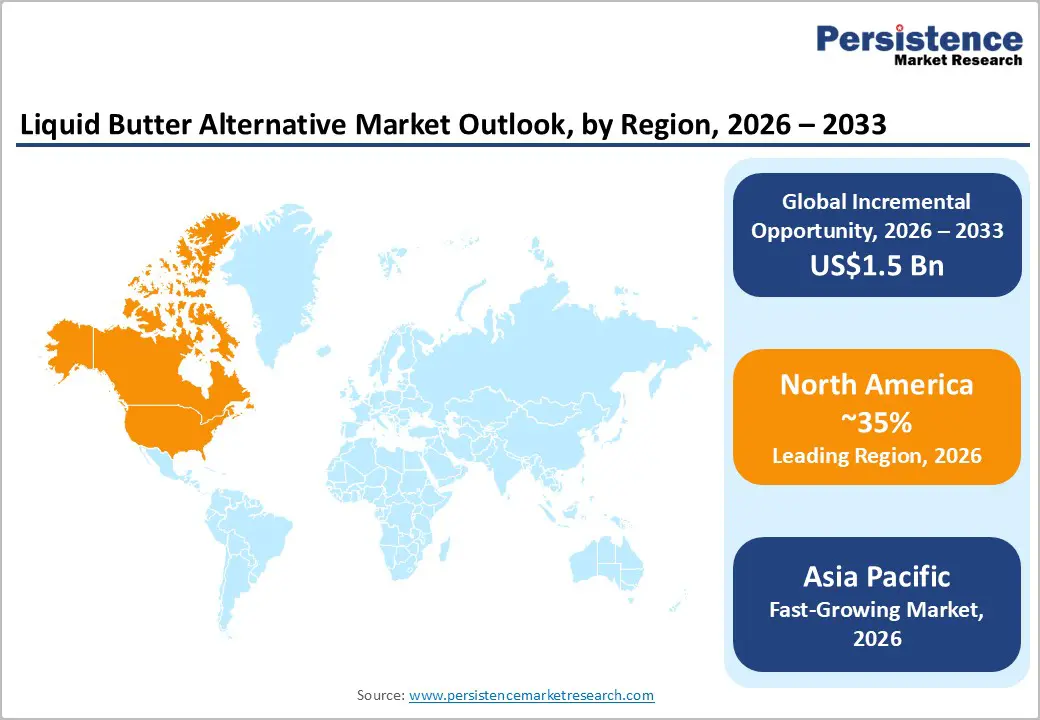

- Leading Region: North America is projected to dominate the market, accounting for approximately 35% in 2026, due to its maintaining the largest established demand base and a mature innovation ecosystem that supports broad commercial adoption and high-value applications.

- Fastest-growing region: Asia Pacific is the fastest-growing region, driven by rapid industrialization of food processing, rising packaged food consumption, and cost-competitive manufacturing in China, India, and ASEAN.

- Dominant Product Type: Plant-based oils, accounting for approximately 53% in 2026, driven by their reliable supply, strong regulatory acceptance, and versatile formulation properties, making them the preferred choice for manufacturers across regions.

- Leading Application: The food industry, including industrial bakeries, confectioneries, and prepared food manufacturers, will be the largest users of liquid butter alternatives, representing approximately 61% of the market, as these formats enhance processing efficiency, shelf life, and dosing accuracy.

| Key Insights | Details |

|---|---|

| Liquid Butter Alternative Market Size (2026E) | US$1.7 Bn |

| Market Value Forecast (2033F) | US$3.2 Bn |

| Projected Growth (CAGR 2026 to 2033) | 9.5% |

| Historical Market Growth (CAGR 2020 to 2025) | 9.2% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Rising Shift toward Plant-Based and Functional Ingredients

The accelerating shift toward plant-based food systems is a major growth driver for the Liquid Butter Alternative market. Health authorities such as the World Health Organization and the U.S. Food and Drug Administration continue to recommend reducing saturated fat intake and eliminating industrial trans fats, prompting large-scale food reformulation initiatives. In response, bakery, snack, and ready meal manufacturers are replacing dairy butter and partially hydrogenated fats with plant-based liquid oil systems derived from sunflower, canola, and other vegetable sources. Quick service restaurant chains and packaged food brands have adopted these alternatives to meet compliance standards while aligning with consumer demand for heart-healthy, cholesterol-free products. Growing awareness around long-term wellness, flexitarian diets, and clean label positioning further strengthens market expansion.

From an industrial perspective, liquid butter alternatives deliver functional and operational advantages. Their superior emulsification, thermal stability, and uniform fat dispersion support consistent product texture in cakes, pastries, sauces, and processed foods. Unlike solid butter, liquid formats enable automated dosing, reduce energy costs associated with melting, and improve production efficiency in high-volume facilities. These performance benefits make them particularly attractive for expanding food manufacturing hubs in emerging economies.

Regulatory Reforms Accelerating Healthier Fat Innovation and Market Expansion

Regulatory pressure has become a decisive growth catalyst for liquid butter alternatives as governments tighten restrictions on trans fats and partially hydrogenated oils. The World Health Organization has called for the global elimination of industrial trans fats, while the U.S. Food and Drug Administration formally banned partially hydrogenated oils in processed foods. These measures have compelled snack, bakery, and quick service restaurant (QSR) operators to reformulate products using high oleic sunflower and canola-based liquid oil systems. McDonald's transitioned to high oleic cooking oils for its fries in the U.S., significantly reducing trans-fat content while maintaining texture and frying performance. Such large-scale reformulations demonstrate how regulatory mandates directly stimulate demand for compliant liquid lipid solutions.

In emerging markets, similar trends are accelerating adoption. India’s Food Safety and Standards Authority has progressively reduced permissible trans-fat limits in vanaspati and bakery fats, pushing manufacturers toward healthier vegetable oil alternatives. As a result, food processors are replacing traditional hydrogenated shortenings with liquid blends to meet compliance and consumer expectations. These regulatory shifts are driving estimated annual demand growth of 6% in developing economies, reinforcing long-term structural expansion.

Barrier Analysis - Regulatory Compliance and Labeling Complexity

Regulatory compliance and labeling complexity remain significant restraints in the Liquid Butter Alternative market. Authorities such as the U.S. Food and Drug Administration and the European Food Safety Authority impose strict guidelines on ingredient declarations, allergen disclosure, and permissible health claims. Nut- and seed-derived liquid butter alternatives must comply with mandatory allergen labeling laws in the U.S. and the European Union, requiring dedicated production lines and cross-contamination controls. In Europe, palm-based variants may also face sustainability certification scrutiny, while certain emulsifiers permitted in one region may require reformulation in another. These variations force manufacturers to adapt packaging language, nutritional panels, and ingredient nomenclature for each export destination.

Such regulatory differences increase documentation burdens, third-party audits, and product approval timelines. A company launching a nut-based formulation in North America and Asia may need separate safety dossiers, labeling translations, and compliance testing before commercialization. These added costs disproportionately affect smaller producers and startups, creating higher entry barriers. Although these regulations enhance food safety, transparency, and consumer confidence, they slow innovation cycles and complicate global market expansion strategies.

Allergen Compliance and Cost Burden Restraining Market Expansion

Nut and seed-derived liquid butter alternatives face stringent allergen management requirements that increase operational complexity and costs. Regulatory bodies such as the U.S. Food and Drug Administration and the European Food Safety Authority mandate clear allergen declarations, bold on-pack labeling, and strict cross-contamination controls. Manufacturers using almond, coconut, or sesame-based lipid systems must often establish segregated production lines, dedicated storage, and enhanced sanitation protocols. For small and mid-sized processors, these infrastructure adjustments can increase operational expenses by an estimated 20%. In addition, third-party certification audits and compliance documentation may extend product launch timelines by six to twelve months, delaying commercialization in competitive markets.

In Asia, regulatory oversight further complicates exports. The Ministry of Food and Drug Safety (MFDS) requires detailed ingredient disclosure and safety validation, particularly for omega-3 fortified or functional nut oil blends. A Southeast Asian manufacturer exporting almond-based liquid fats to South Korea may need reformulation or additional testing to meet disclosure standards. These regulatory burdens raise entry barriers, slow innovation cycles, and disproportionately impact smaller firms seeking international expansion.

Opportunities - Penetration in Emerging Food Manufacturing Markets

Penetration into emerging food manufacturing markets presents a major growth opportunity for the liquid butter alternative industry. Rapid urbanization across countries such as India, Indonesia, Vietnam, and Brazil is accelerating demand for packaged bakery products, ready-to-eat meals, and confectionery items. As modern retail chains and quick service restaurants expand, food processors are shifting toward standardized liquid lipid systems that ensure consistent texture, taste, and shelf stability. Industrial bakeries in India are increasingly replacing traditional dairy butter with vegetable oil-based liquid blends to improve scalability and reduce production costs. Similarly, Southeast Asian snack manufacturers are adopting liquid fat systems to support automated mixing and continuous production lines.

Government-led initiatives further strengthen this trend. Programs such as “Make in India” and food-processing modernization schemes across ASEAN encourage investment in advanced manufacturing infrastructure and quality control systems. As countries tighten food safety regulations and adopt labeling standards aligned with international norms, manufacturers prefer compliant, plant-based fat solutions that simplify export approvals. The combination of expanding processing capacity, rising middle-class consumption, and regulatory alignment positions emerging economies as high-volume growth engines for liquid butter alternatives.

Health - Focused Fortification Creating Premium Growth Opportunities

Rising lifestyle diseases, including diabetes and cardiovascular disorders, are encouraging food manufacturers to adopt fortified liquid butter alternatives enriched with functional nutrients. Regulatory frameworks such as those issued by the Food Safety and Standards Authority of India support controlled fortification with vitamin D, plant sterols, and omega-3 fatty acids, provided labeling and dosage standards are met. This creates an opportunity for producers to develop value-added lipid blends that combine functionality with health positioning. For instance, omega-3-enriched liquid fats derived from algal oils are increasingly used in snack seasonings and bakery applications to support “heart-friendly” claims while maintaining processing stability.

In India, branded snack manufacturers such as Haldiram's are exploring fortified edible oil blends in namkeens and baked snacks to appeal to urban, health-conscious consumers, enabling premium pricing and margin expansion. Similarly, Vietnamese Ready-to-Eat meal producers are incorporating sterol-enriched liquid fat bases into instant pho products targeted at working professionals seeking convenient yet healthier options. These innovations allow manufacturers to differentiate offerings, strengthen brand positioning, and capture higher value segments in competitive food markets.

Category-wise Analysis

Product Type Insights

Plant-oil-based products are anticipated to hold 53% share in 2026. Manufacturers are innovating through water-in-oil micro-emulsions that replicate butter’s sizzle, upcycled seed oils targeting sustainability-focused consumers, and hybrid oil blends that balance high smoke points with gourmet flavor. Performance improvements such as enhanced smoke point parity with butter, micronized salt suspension for flavor consistency, and stronger Oxidative Stability Index (OSI) using natural antioxidants such as rosemary extract and mixed tocopherols are strengthening industrial appeal. Leading players, including Upfield (Professional), Bunge (Creative Solutions), Ventura Foods (Phase Gold), and Stratas Foods (Whirl), compete through heat stability, low-saturated-fat formulations, proprietary flavor-release systems, and high-end patisserie replacements. Ultimately, the segment’s dominance is driven less by plant-based positioning and more by total cost of ownership advantages, eliminating refrigeration, improving yield, extending shelf life, and enhancing process efficiency across large-scale food manufacturing.

The seed-derived liquid butter alternative segment is accelerating through bio-mimicry and functional customization, using seed proteins such as hemp and sunflower to emulsify oils into creamy, butter-like liquids while fortifying blends with flax or chia for Omega-3 RDA positioning. Upcycled sourcing from tomato and cranberry seed by-products further enhances sustainability credentials. Industrial innovation focuses on lower viscosity for superior spray coverage, phospholipid recovery to improve Maillard browning, and natural colorants such as turmeric and annatto to meet the critical “yellow” consumer expectation while adding antioxidant benefits. Key seed-specialist brands include Frylight, Whirl, Avonmore, and Spectrum Organics, each targeting niches from ultra-low-calorie sprays to professional baking and organic retail. Ultimately, the segment’s rapid growth is driven by the chemical versatility of seed oils, allowing customized blends such as high-oleic sunflower, rapeseed, and flax to deliver lower saturated fat, higher smoke points, reduced cost per gallon, and ambient liquid stability outperforming traditional butter across regulatory, culinary, economic, and logistical metrics.

Application Insights

The food industry is expected to be the primary driver of liquid butter alternative demand, holding about 61% share in 2026, supported by technical innovation and regulatory advantages. Industrial bakeries are increasingly adopting hybrid blends of vegetable oils and nut-derived fats to balance cost efficiency with premium labeling claims. Advanced formulations now include Maillard-reaction enhancers to improve browning and specialized emulsifier systems that minimize oil migration in long-shelf-life snack products. Regulatory frameworks, including compliance requirements from the U.S. Food and Drug Administration and the European Food Safety Authority, along with acrylamide mitigation standards under Regulation (EU) 2017/2158, are accelerating the transition toward plant-based liquid systems with lower microbial risk and reduced saturated fat content. From an operational standpoint, liquid butter alternatives enhance manufacturing efficiency through precise automated dosing, improved thermal stability, lower VOC emissions, and minimized cross-contamination downtime. Key industry players such as Bunge, Cargill, Stratas Foods, and AAK continue to reinforce market leadership with application-specific, high-performance formulations designed for large-scale food production.

Personal care is likely to be the fastest-growing application for liquid butter alternatives, driven by sustainability, sensory appeal, and advanced formulation benefits. Trends such as upcycled beauty oils, microbiome-friendly lipid systems, and anhydrous (waterless) products are accelerating adoption. Liquid seed oils outperform solid butters due to low comedogenic ratings, better spreading ability, and enhanced glow from favorable refractive index properties. Consumers prefer lightweight, non-greasy textures, improved stability without crystallization, and innovative delivery formats such as fine-mist sprays that position liquid alternatives ahead of traditional solid fats in modern beauty formulations.

Regional Insights

North America Liquid Butter Alternative Market Trends

North America’s liquid butter alternative market is anticipated to account for approximately 35% in 2026, driven by foodservice labor optimization, clean-label demand, and plant-based mainstreaming. Rising kitchen labor costs have made pumpable formats the operational standard, eliminating meltdown time and improving efficiency across chains such as Buffalo Wild Wings and AMC Theatres. The growing consumer skepticism toward GMO ingredients is accelerating the adoption of Non-GMO verified liquid oils across retail and industrial applications. The expansion of flexitarian diets in the U.S. and Canada further supports demand, integrating liquid butter alternatives into sprays, frozen meals, and QSR products. Industrial trends such as RTD butter-coffee commercialization, upcycled grain oils, and propellant-free Bag-on-Valve packaging are reinforcing innovation and sustainability positioning.

The U.S. Food and Drug Administration's 2024 “Healthy” redefinition favors unsaturated fats, benefiting liquid alternatives over dairy butter, while California Prop 65 has pushed advanced refining standards. The U.S.-Mexico-Canada Agreement streamlines cross-border oilseed trade, maintaining cost competitiveness. Additional factors such as cinema-driven R&D (popcorn economy), cold-climate viscosity innovation, strict sustainability audits, early trans-fat bans, and dairy price volatility collectively reinforce the region’s industrial scale, automation advantage, and sustained dominance.

Europe Liquid Butter Alternative Market Trends

Europe’s liquid butter alternative market is characterized by premium positioning, sustainability leadership, and stringent regulatory standards. A major trend is the development of “cultured-style” flavor systems, where fermented plant extracts replicate the tangy, lactic notes preferred in traditional European butter. The region is also advancing sustainable packaging solutions, including compostable bag-in-box formats and glass-based spray dispensers aligned with circular economy objectives. Strong emphasis on hyper-local sourcing, such as EU-grown rapeseed and sunflower oils, supports reduced food miles and origin-based branding. Additionally, Europe’s strict clean-label framework, including the elimination of E-numbers and tight glycidyl ester limits, has pushed manufacturers toward natural stabilizers like citrus fibers and lower-temperature refining methods.

Market stability is supported by regulatory clarity and well-established oilseed infrastructure. Europe functions as an effectively non-GMO market, resulting in a structured but relatively higher-cost supply chain. Key players such as Upfield, AAK, Saputo (Frylight), and Vandemoortele drive innovation across plant-sterol fortification, specialty fats, calorie-controlled sprays, and bakery-grade liquid formulations. Long-term agricultural policy alignment, dense rapeseed crushing capacity, and a consumer base willing to pay premiums for organic and sustainably sourced products collectively position Europe as a stable, high-value market leader.

Asia Pacific Liquid Butter Alternative Market Trends

Asia Pacific is emerging as the fastest-growing liquid butter alternative market, driven by plant-based innovation, health-focused reformulation, and digital retail expansion. Rising veganism in countries such as Australia and India is accelerating demand for nut-, seed-, and specialty oil-based alternatives. Manufacturers are introducing clean-label variants fortified with Omega-3s and probiotics to appeal to increasingly health-conscious consumers. At the same time, e-commerce platforms have become a dominant distribution channel post-pandemic, enabling both artisanal and large-scale brands to expand rapidly across urban and semi-urban markets.

Regulatory clarity and trade integration further reinforce regional growth. Stricter labeling standards from bodies such as the Food Safety and Standards Authority of India and evolving Chinese dairy-alternative regulations are enhancing transparency while raising compliance benchmarks. Trade facilitation under the Regional Comprehensive Economic Partnership supports the cross-border movement of vegetable fats, while the Singapore Food Agency is advancing novel food and precision-fermentation approvals. Major players, including Cargill, Bunge, AAK, and Wilmar International, dominate supply chains, while structural advantages, massive population scale, and limited legacy cold-chain infrastructure make shelf-stable LBAs a cost-efficient and industrially preferred fat alternative across modernizing Asian food systems.

Competitive Landscape

The global liquid butter alternative market is moderately fragmented, with leadership concentrated among global ingredient suppliers such as Cargill, Bunge, AAK, Ventura Foods, Wilmar International, and Upfield. These leaders play a decisive role in shaping industry standards through advanced oil-processing technologies, proprietary fat-blending systems, and globally integrated sourcing networks. Their functional influence extends beyond scale; they drive formulation innovation, regulatory alignment, and application-specific customization across food manufacturing, cosmetics, and personal care segments.

Market leadership is reinforced by technological footprint and procurement depth. Large players maintain vertical integration from oilseed crushing and refining to finished lipid systems, ensuring supply stability and compliance across multiple jurisdictions. Their R&D capabilities enable the development of high-oleic blends, emulsifier-free clean-label systems, and fortified lipid matrices tailored to bakery, snack, QSR, and beauty applications. Long-term supply contracts with multinational food processors and retail brands strengthen customer retention, while regulatory expertise facilitates cross-border commercialization in highly controlled markets such as North America and Europe.

Key Industry Developments:

- In March 2025, Savor announced the commercial launch of its "animal-and-plant-free" butter, which is uniquely produced by taking carbon dioxide from the air and hydrogen from water to create fat molecules. This innovative product is being introduced in select high-end restaurants and bakeries.

- In May 2025, Maison Linotte, a French luxury pastry brand, launched a new plant-based butter made from organic, palm oil-free ingredients, targeted specifically at chefs and pastry lovers.

Companies Covered in Liquid Butter Alternative Market

- Cargill

- Bunge

- Conagra Brands

- Ventura Foods

- AAK

- Wilmar International

- Upfield

- Earth Balance

- Miyoko’s Creamery

- Nutiva, Inc.

- Pure Blends

- Blue Diamond Growers

- Kraft Heinz/Country Crock

Frequently Asked Questions

The global liquid butter alternative market is projected to reach US$ 1.7 billion in 2026.

Market growth is driven by the shift toward plant-based diets, regulatory pressure to reduce animal-derived fats, and functional advantages such as processing efficiency and shelf stability.

The liquid butter alternative market is anticipated to grow at a CAGR of 9.5% from 2026 to 2033.

Major opportunities lie in emerging food manufacturing markets, clean-label and specialty formulations, and expanding use in cosmetics and personal care products.

The liquid butter alternative market is shaped by established global ingredient suppliers and regional processors with strong formulation expertise, regulatory compliance capabilities, and diversified sourcing networks.