- Food Ingredients & Additives

- Liquid Eggs Market

Liquid Eggs Market Size, Share, and Growth Forecast 2026 - 2033

Liquid Eggs Market by Product Type (Whole Liquid Eggs, Liquid Egg Whites, Liquid Egg Yolks, Scrambled Egg Mix), by End Use (Food Service, Food Processing Industry, Household Retail, Pet Food, Others), by Sales Channel (B2B, B2C), and Regional Analysis, 2026 - 2033

Liquid Eggs Market Share and Trends Analysis

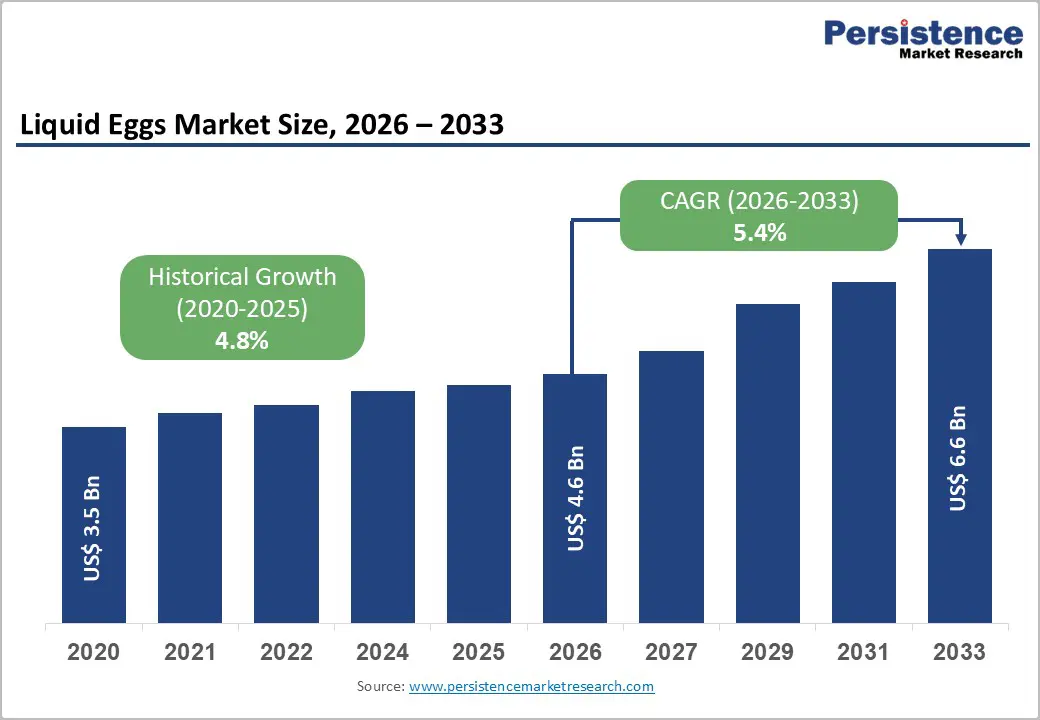

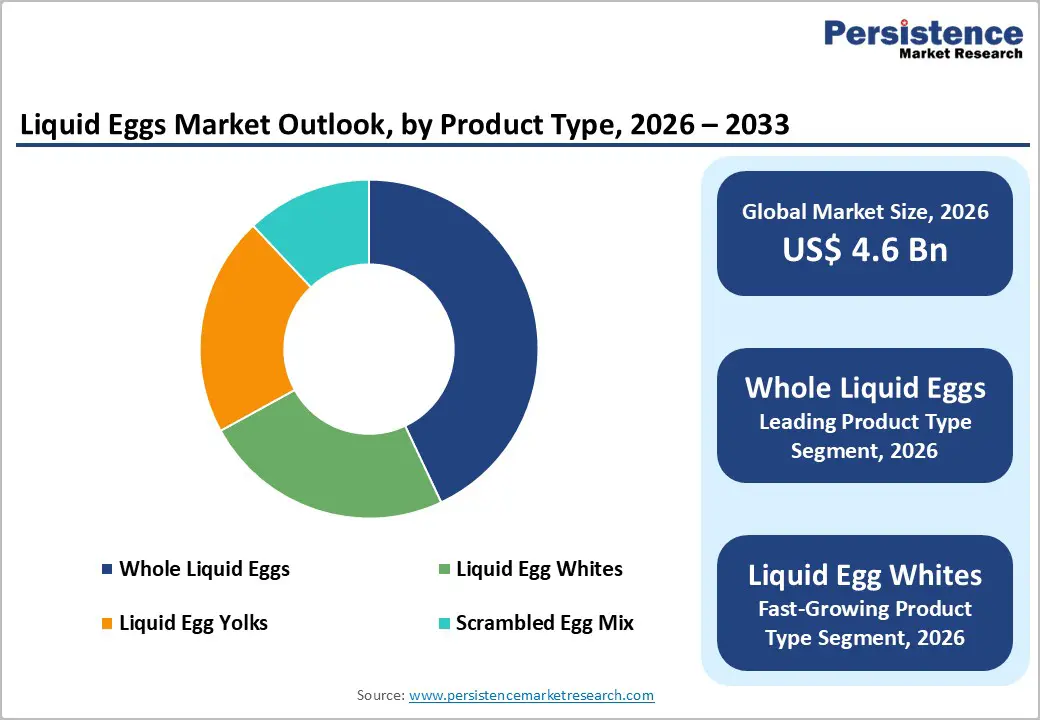

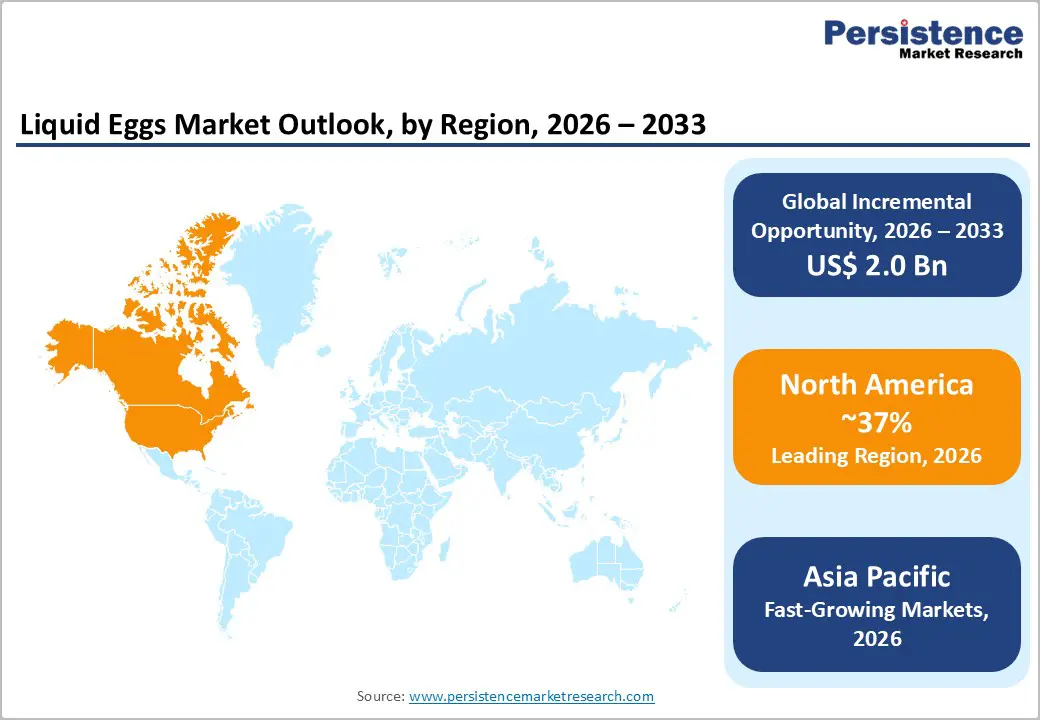

The global liquid eggs market size is expected to be valued at US$ 4.6 billion in 2026 and projected to reach US$ 6.6 billion by 2033, growing at a CAGR of 5.4% between 2026 and 2033.

The market is primarily propelled by the escalating demand for high-protein convenience foods and the rigorous food safety standards implemented by global regulatory bodies. As industrial food processors seek to minimize contamination risks associated with shell eggs, the adoption of pasteurized liquid egg products has become a standard protocol in large-scale bakery and confectionery manufacturing. Furthermore, the shift toward standardized ingredients in the Food Service sector ensures consistency in mass-produced meal solutions, effectively bridging the gap between nutritional requirements and operational efficiency.

Key Market Highlights

- Leading Region: North America remains the dominant market, holding a 37% share in 2025, driven by a mature food processing industry, high safety standards, and strong demand for convenience.

- Fastest Growing Regional Market: Asia Pacific is the fastest-expanding market, fueled by rapid urbanization, Westernization of diets, and significant investments in poultry supply chain modernization in China and India.

- Dominant Product Segment: Whole liquid eggs led the product category with a 43% market share in 2025 due to their indispensable role in universal food manufacturing and large-scale baking.

- Fastest Growing Product: Liquid egg whites represent the fastest-growing product type, capitalizing on the global "health and wellness" trend and the increasing demand for high-protein, fat-free dietary solutions.

- Opportunity: The development of plant-based liquid egg alternatives offers significant growth potential as manufacturers target the rising demographic of flexitarian and environmentally conscious consumers worldwide.

| Key Insights | Details |

|---|---|

| Liquid Eggs Size (2026E) | US$ 4.6 billion |

| Market Value Forecast (2033F) | US$ 6.6 billion |

| Projected Growth CAGR (2026 - 2033) | 5.4% |

| Historical Market Growth (2020 - 2025) | 4.8% |

DRO Analysis

Drivers - Rising Demand for Industrial Convenience and Food Safety Compliance

A fundamental driver for the market is the transition from traditional shell eggs to processed liquid formats within the global food supply chain. According to the United States Department of Agriculture (USDA), modern food safety regulations, such as the Egg Products Inspection Act, emphasize the necessity of pasteurization to eliminate Salmonella and other pathogens. Liquid eggs offer a sterile, ready-to-use alternative that significantly reduces labor costs and preparation time for industrial bakeries and large-scale caterers. The International Egg Commission (IEC) notes that the logistical ease of transporting bulk liquid egg containers compared to fragile shell eggs has led to a 15% improvement in supply chain efficiency for major food processors. This shift is particularly evident in the production of sauces, dressings, and pre-packaged baked goods, where precision in volume and consistency is paramount.

Evolution of High-Protein Dietary Trends and Functional Nutrition

The global surge in health consciousness has positioned liquid eggs, particularly Liquid Egg Whites, as a staple in the functional nutrition sector. Data from the World Health Organization (WHO) regarding the importance of high-quality protein sources has influenced consumer behavior, leading to increased retail demand for cholesterol-free egg products. The European Food Safety Authority (EFSA) has also recognized the bioavailability of egg proteins, encouraging their inclusion in specialized diets for athletes and the elderly. As a result, companies are innovating with fortified liquid egg variants, adding vitamins and minerals to cater to the growing "clean label" movement. This demand is further bolstered by the expansion of the Pet Food industry, where liquid eggs are utilized as a premium protein additive to enhance the nutritional profile of high-end pet meals.

Restraints - Volatility in Raw Material Pricing and Avian Flu Outbreaks

The primary barrier to market stability is the unpredictable nature of raw egg prices, often dictated by disease outbreaks such as Highly Pathogenic Avian Influenza (HPAI). In 2024 and 2025, major production hubs in North America and Europe experienced significant flock culls to contain the spread of the virus, leading to a temporary supply deficit. The World Organization for Animal Health (WOAH) monitors these trends closely, noting that even minor disruptions in the layer hen population can cause a 20-30% spike in liquid egg production costs. These fluctuations make long-term contract pricing difficult for B2B suppliers and can lead to temporary price hikes for end consumers in the Household Retail segment.

Logistical Challenges and Cold Chain Infrastructure Constraints

Unlike dried egg powder, liquid eggs require a rigorous and uninterrupted cold chain to maintain shelf life and biological safety. The necessity of maintaining temperatures between 0°C and 4°C throughout the distribution process poses a significant financial burden on manufacturers. In developing regions across the Middle East & Africa and parts of Asia Pacific, the lack of advanced refrigerated transport and storage facilities limits the market's geographic reach. According to the Global Cold Chain Alliance, infrastructure gaps in these regions can lead to a spoilage rate of up to 10% for liquid perishable products, acting as a deterrent for smaller food service operators who may lack the necessary on-site cooling capacity.

Opportunities - Expansion of Plant-Based and Sustainable Alternatives

A significant opportunity lies in the development of hybrid and plant-based liquid egg products to cater to the burgeoning flexitarian demographic. Leading entities like Cargill, Incorporated and various European food-tech firms are investing in research to create liquid egg substitutes derived from mung beans or chickpeas that mimic the leavening and binding properties of traditional eggs. The Good Food Institute highlights that the alternative protein market is expected to witness substantial growth, and liquid formats are uniquely positioned to capture this demand due to their versatility in industrial applications. By aligning with global sustainability goals and the United Nations Sustainable Development Goals (SDGs) regarding responsible production, manufacturers can tap into a high-growth niche that appeals to environmentally conscious consumers and reduces reliance on animal-based supply chains.

Category-wise Analysis

Product Type Insights

The whole liquid eggs segment remains the dominant force in the market, commanding a significant 43% market share in 2025. This dominance is attributed to the product's universal application across various food industries, serving as a critical ingredient for binding, leavening, and emulsification in everything from industrial bakery products to pasta manufacturing. The American Egg Board emphasizes that whole liquid eggs provide the complete nutritional profile of a shell egg without the operational hazards of shell fragments. Conversely, the Liquid Egg Whites segment is identified as the fastest-growing category, projected to expand at a robust CAGR between 2025 - 2032. This growth is fueled by the health and wellness sector, where egg whites are prized for being fat-free and high in protein, catering specifically to the bodybuilding and weight management communities.

Sales Channel Insights

The B2B (Business-to-Business) channel is the primary revenue generator, accounting for an estimated 58% of the market share in 2025. Bulk procurement by industrial food manufacturers and large restaurant chains defines this segment, characterized by long-term supply contracts and specialized logistics. Large players like Michael Foods, Inc. and Rembrandt Foods dominate this space by offering customized liquid egg blends tailored to specific client recipes. On the other hand, the B2C (Business-to-Consumer) channel is witnessing the fastest growth, particularly through e-commerce and specialty grocery retailers. Modern consumers are increasingly purchasing small-format liquid egg cartons for home use, driven by the convenience of measuring by volume rather than cracking shells, a trend most prominent in North America and Europe.

Regional Insights

North America Liquid Eggs Market Trends and Insights

North America holds the largest share of the global liquid egg market, accounting for 37% of total revenue in 2025. The region's leadership is anchored by the U.S. market, where a highly mature food processing industry and stringent USDA regulations regarding egg pasteurization create a stable demand environment. Innovation in this region is driven by consumer preferences for cage-free and organic liquid egg products. Major retailers like Walmart and Costco have committed to transitioning toward 100% cage-free egg supplies by 2030, forcing liquid egg processors to overhaul their sourcing strategies.

Furthermore, the U.S. is a hub for technological advancement in egg breaking and pasteurization machinery. Organizations like the United Egg Producers (UEP) provide a framework for animal welfare and food safety that influences global standards. The ecosystem is characterized by heavy investment in R&D, particularly in the development of long-shelf-life liquid eggs through ultra-pasteurization (UP) and aseptic packaging. This allows regional players like Cal-Maine Foods, Inc. and Rose Acre Farms to maintain a competitive edge through product differentiation and high-volume output.

Asia Pacific Liquid Eggs Market Trends and Insights

Asia Pacific is the fastest-growing region in the liquid egg market, fueled by rapid industrialization and the expansion of the middle class in China and India. The rise of organized retail and the proliferation of international fast-food chains have catalyzed the demand for pasteurized liquid eggs to ensure food safety in high-density urban areas. In China, the government’s focus on modernizing the poultry supply chain following various avian flu scares has incentivized producers to shift from wet markets to processed egg facilities.

The manufacturing advantage in the ASEAN region, particularly in Thailand and Vietnam, is another critical factor. Lower production costs and improving cold chain logistics are making these countries attractive hubs for liquid egg export. Industry associations like the Egg Industry Association of China are working to standardize processing methods to meet international export requirements. As dietary habits shift toward higher protein intake, the household consumption of liquid eggs is also gaining traction in Japan and South Korea, where convenience and food safety are top consumer priorities.

Competitive Landscape

The liquid eggs market is moderately consolidated, characterized by a mix of large-scale processors and regional suppliers competing on quality, pricing, and product innovation. Companies focus on offering pasteurized, safe, and convenient egg solutions to meet strict food safety regulations and rising demand from foodservice and industrial users. Innovation in packaging, extended shelf-life technologies, and clean-label formulations is a key competitive factor. Strategic partnerships with food manufacturers and the expansion of distribution networks strengthen market presence.

Key Developments:

- In March 2026, Australian Eggs expanded its “Easter OG” platform into a fully integrated, social-first campaign developed by Liquid Ideas, featuring a satirical hero film challenging the dominance of chocolate eggs. The campaign was supported by chef-led recipes, content partnerships, and multi-channel media across digital and social platforms.

- In May 2025, Sanguan Farm, a pioneering egg producer based in Thailand's Saraburi province, achieved a significant milestone by launching the country's first pasteurized cage-free liquid egg.

- In January 2025, Cal-Maine Foods, Inc. announced a $15 billion investment to expand its egg products processing facility in Blackshear, Georgia. The expansion will focus on producing extended shelf-life liquid egg products, catering to growing demand from the foodservice and ready-to-eat segments.

Companies Covered in Liquid Eggs Market

- Cal-Maine Foods, Inc.

- Cargill, Incorporated

- Ovostar Union NV

- Noble Foods

- Ovoteam

- Chino Valley Ranchers

- Michael Foods, Inc.

- Global Eggs

- Rembrandt Foods

- Rose Acre Farms

- NestFresh Eggs

- Eurovo srl

- Igreca

- Global Food Group

- Bumble Hole Foods Limited

Frequently Asked Questions

The global liquid eggs market is expected to reach a valuation of US$ 4.6 billion by 2026, following a steady growth trajectory from the historical period.

Demand is primarily driven by the need for enhanced food safety and convenience in the food service and processing sectors, as well as the rising global preference for high-protein diets.

North America is the leading region, accounting for approximately 37% of the global market share in 2025, supported by advanced food processing infrastructure and strict regulatory frameworks.

The most substantial opportunity lies in the innovation of plant-based liquid egg alternatives and the expansion into the rapidly urbanizing markets of Asia Pacific.

Major market participants include Cal-Maine Foods, Inc., Cargill, Incorporated, Michael Foods, Inc., Eurovo srl, and Rose Acre Farms, among others.