- Specialty & Fine Chemicals

- Liquid Masterbatches Market

Liquid Masterbatches Market Size, Trends, Share, and Growth Forecast 2026 - 2033

Liquid Masterbatches Market by Product Type (White, Black, Color, Additive and Fillers), Resin Type (Polyethylene, Polypropylene, Polyvinyl Chloride, Polyethylene Terephthalate and Others), End-user (Packaging, Building & Construction, Consumer Good, Automotive, Agriculture and Others), and Regional Analysis from 2026 to 2033

Liquid Masterbatches Market Share and Trends Analysis

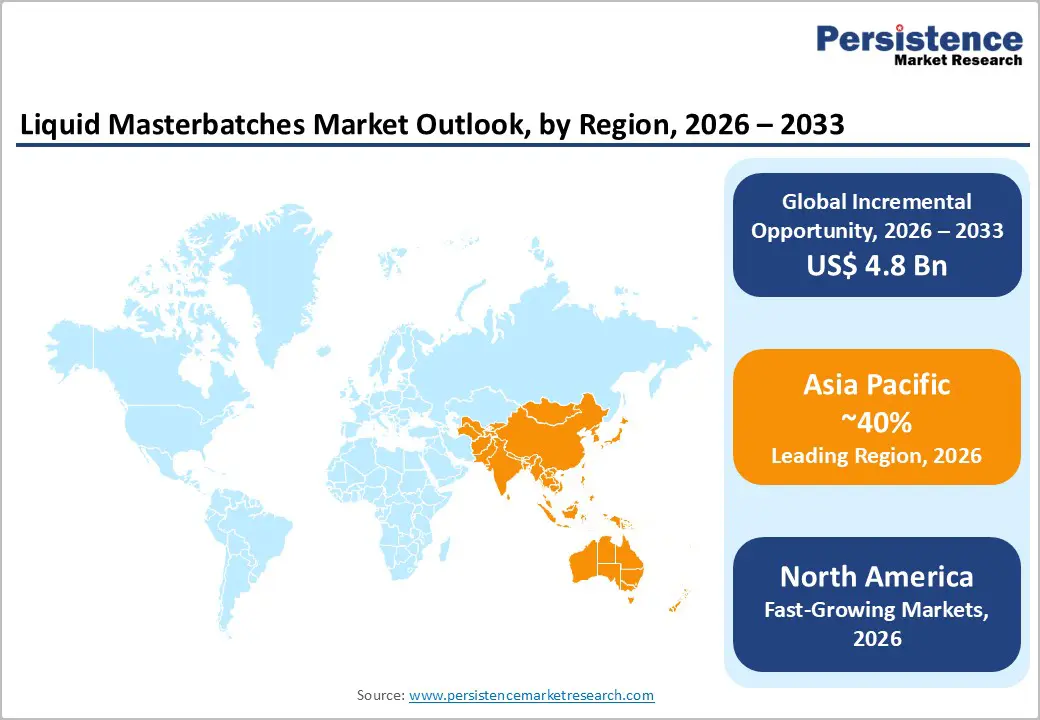

The global liquid masterbatches market size is likely to be valued at US$ 11.0 billion in 2026 and is projected to reach US$ 15.8 billion by 2033, growing at a CAGR of 5.4% between 2026 and 2033.

This market expansion is fundamentally driven by accelerating demand for premium plastic products across the packaging and construction sectors, with manufacturers increasingly adopting advanced color masterbatches, additive masterbatches, and functional pigment solutions to enhance operational efficiency and product performance.

Key Market Highlights:

- Leading Region: Asia Pacific dominates the global market with 40% share driven by China's 105 million tons annual plastic production, India's 7% annual growth rate, and Vietnam, Thailand, and Indonesia's manufacturing expansion supporting exceptional regional demand expansion through 2033.

- Fastest-Growing Region: Fastest growing region North America and Europe advancing at an accelerating CAGR with North America emphasizing sustainable packaging and automotive electrification, Europe pursuing circular economy compliance and biodegradable formulation development, driving specialized masterbatch adoption.

- Dominant Product Segment: Additive masterbatches account for 48% of the market, driven by antimicrobial, flame-retardant, UV-protection, and electrical-conductivity enhancement capabilities that support premium pricing and customer productivity optimization.

- Fastest-Growing Region: Polyethylene carrier systems are the fastest-growing material, with a 42% market share and expanding adoption across flexible packaging, injection molding, and blow molding applications, supporting the expansion of commodity and specialty plastic production.

- Opportunity: Sustainable packaging and circular economy initiatives represent a major market opportunity, driven by biodegradable masterbatch, post-consumer recycled (PCR) compatibility, and the development of closed-loop recycling systems, creating high-growth market segments that are expanding at 8% annually.

| Key Insights | Details |

|---|---|

| Liquid Masterbatches Market Size (2026A) | US$ 11.0 Bn |

| Projected Year Value (2033F) | US$ 15.8 Bn |

| Value CAGR (2026 - 2033) | 5.4% |

| Historical Market Growth Rate (CAGR 2019 to 2023) | 4.2% |

Market Dynamics

Drivers - Rising Demand for Premium Plastic Products and Enhanced Visual Appeal Across Packaging and Consumer Goods Industries

The packaging and consumer goods sectors are critical market drivers, collectively accounting for substantial consumption of liquid masterbatch, driven by increasing manufacturing sophistication and aesthetic requirements. Global plastic packaging production continues expanding with approximately 141 million tons of plastic packaging manufactured annually worldwide, according to the Waste and Resources Action Program, creating exceptional demand for vibrant color masterbatches and functional additives.

Consumer brands increasingly prioritize visual differentiation and product shelf appeal, compelling packaging manufacturers to adopt advanced liquid color masterbatches enabling precise color matching and consistent visual properties. Flexible packaging applications in the food and beverage industries represent particularly strong demand segments, with manufacturers requiring masterbatches providing UV stability, opacity, and heat resistance properties essential for product protection and brand visibility.

Advanced Additive Technology Development and Functional Property Enhancement Driving Market Adoption

Technological advances in functional additive development are a transformative market driver, with manufacturers increasingly deploying sophisticated antimicrobial masterbatches, flame-retardant additives, and UV-protection compounds, thereby enhancing polymer performance and product durability. Functional liquid masterbatches demonstrate the capacity for delivering multiple performance properties simultaneously, including electrical conductivity, thermal stability, and mechanical property enhancement, establishing specialized demand segments commanding premium pricing justification.

Construction industry adoption accelerates with an increasing emphasis on green building materials and energy-efficient plastic components, creating demand for masterbatches that improve material durability and environmental performance. Industries including automotive, electronics, and healthcare increasingly specify masterbatches meeting advanced performance requirements including heat resistance at temperatures exceeding 250 degrees Celsius and specialized mechanical property optimization.

Restraints - Volatile Raw Material Pricing and Supply Chain Disruption Constraining Manufacturing Economics

Liquid masterbatch manufacturing fundamentally depends on critical raw materials, including pigments, stabilizers, and polymer carriers, and commodity price volatility creates substantial margin compression for manufacturers. Petroleum-based feedstock prices fluctuate substantially in response to geopolitical dynamics and energy market conditions, with polymer resin prices exhibiting volatility exceeding 40% during periods of supply constraint. Pigment procurement similarly encounters volatility driven by mining production capacity and geopolitical considerations, particularly affecting the supply of specialized pigments, including specialty iron oxides and organic pigments from concentrated suppliers.

Manufacturing cost escalations directly cascade through industry value chains, constraining profitability, particularly for commodity-focused product segments. Supply chain disruptions stemming from logistics challenges, port congestion, and international shipping constraints periodically restrict raw material availability, thereby limiting production capacity and extending customer delivery timelines, potentially undermining market share positions for manufacturers facing prolonged material-sourcing constraints.

Intense Competitive Pricing Pressure and Environmental Regulation Complexity Reducing Profitability Opportunities

The liquid masterbatch market exhibits highly competitive dynamics, with established global manufacturers competing aggressively on price, while emerging regional suppliers from China and India offer cost-competitive alternatives. Original equipment manufacturers (OEMs) and industrial distributors continuously negotiate price concessions, leveraging purchasing power and specification flexibility, constraining pricing leverage for suppliers. Regulatory compliance complexity, including European Union REACH regulations, FDA standards in the United States, and emerging biodegradability certifications, creates substantial research and development investment requirements, limiting innovation resources for smaller competitors. Market consolidation trends, including strategic acquisitions among competitors, create competitive pressures forcing smaller players toward niche specialization or exit scenarios.

Opportunities - Accelerating Electric Vehicle Manufacturing and Lightweight Polymer Component Production Establishing Exceptional Growth Opportunities

Electric vehicle manufacturing expansion presents a substantial growth opportunity for liquid masterbatch demand, as automotive manufacturers implement lightweighting strategies and advanced polymer utilization in battery housings, thermal management systems, and structural components. Global electric vehicle sales reached 18.78 million units in 2024, resulting in substantial consumption of specialized masterbatch for components requiring thermal stability, electrical conductivity, and UV protection.

Battery enclosure manufacturing requires precision black masterbatches and conductive additives that enable efficient thermal management and electrical performance optimization, thereby establishing specialized, high-value demand segments. Lightweight plastic components for automotive bodies and interior systems create demand for masterbatches, enhancing mechanical strength while reducing material density, thereby supporting fuel-efficiency improvements and emission-reduction objectives.

Sustainability Initiatives and Circular Economy Model Implementation Creating High-Growth Market Segments

Environmental regulations and corporate sustainability commitments create significant market opportunities for liquid masterbatch manufacturers pursuing sustainable formulation development and integration into the circular economy. European Union plastic waste reduction directives and United States packaging sustainability regulations compelling manufacturers toward biodegradable masterbatch adoption and recycled content compatibility, establishing specialized demand segments expanding at 7-10% annually. Post-consumer recycled (PCR) plastic processing requires specialized masterbatches to ensure color consistency and performance stability across multiple processing cycles, thereby establishing recurring revenue opportunities through customer partnerships.

Circular economy initiatives, including closed-loop recycling systems and material recovery optimization, create demand for masterbatches engineered for processing thermoplastic elastomers, advanced polymers, and composite materials in diverse applications. Green building initiatives in the construction sector drive demand for masterbatches, improving plastic product sustainability credentials and environmental product declarations (EPDs), establishing differentiated market positioning for manufacturers emphasizing ecological responsibility.

Category-wise Analysis

Product Type Insights

Additive masterbatches command a clear market lead, with approximately 48% market share, reflecting exceptional versatility and performance-enhancing capabilities across diverse industrial applications and processing environments. Additive masterbatch consumption is accelerating, driven by expanding functionality requirements, including antimicrobial properties, flame retardancy, UV protection, and electrical conductivity enhancements, which justify premium pricing and support customer productivity optimization.

Color masterbatches capture approximately 35% of the market, demonstrating sustained adoption across packaging, automotive, and consumer goods applications that require vibrant coloration, color consistency, and aesthetic differentiation to support brand recognition and market positioning. White masterbatches and filler masterbatches collectively represent 17% market share, with white masterbatches demonstrating consistent demand driven by applications requiring opacity and brightness enhancement in films, injection-molded components, and agricultural applications.

Resin Type Analysis

Polyethylene (PE) carrier resin systems hold a clear market lead, commanding approximately 42% of the market and reflecting exceptional versatility, cost-effectiveness, and compatibility across diverse polymer applications and processing methods. Polyethylene masterbatches are widely used in film extrusion, injection molding, blow molding, and thermoforming, supporting commodity and specialty plastic production across industries.

Polypropylene (PP) masterbatches account for approximately 38% of the market, reflecting accelerating adoption driven by superior mechanical properties, temperature resistance, and expanding use in automotive components, packaging applications, and consumer goods manufacturing. Polyvinyl Chloride (PVC) masterbatches represent approximately 12% market share, maintaining consistent demand in construction materials, electrical insulation, and rigid plastic applications where flame retardancy and thermal stability requirements necessitate specialized formulation development.

End-user Insights

The packaging industry dominates end-user segments, commanding approximately 52% of liquid masterbatch consumption, driven by exceptional production volume, aesthetic requirements, and expanding sustainability mandates governing plastic packaging specifications. Packaging applications for food and beverage containers, pharmaceutical packaging, and consumer products require sustained procurement of liquid masterbatch to meet diverse color requirements and functional specifications. The building and construction industry accounts for approximately 21% of the market, despite lower production volumes relative to packaging, reflecting increasing plastic use in pipe manufacturing, weathering systems, and structural applications that require color consistency and durability.

Regional Insights

North America Liquid Masterbatches Market Trends

North America represents approximately 26% of global liquid masterbatch market, characterized by advanced manufacturing infrastructure, stringent quality standards, and established packaging industry foundations supporting sustained market demand. United States packaging industry leadership driven by consumer goods, food and beverage, and pharmaceutical sectors establishes substantial liquid masterbatch consumption, with manufacturers increasingly adopting sustainable masterbatch formulations supporting environmental regulatory compliance and corporate sustainability commitments.

A regulatory framework emphasizing FDA compliance for food-contact applications and EPA environmental standards establishes stringent quality requirements, compelling manufacturers to adopt premium masterbatch. Automotive manufacturing expansion in Mexico and the United States, supporting lightweighting initiatives, drives specialized demand for black masterbatches and conductive additives in battery housing and component applications.

Europe Liquid Masterbatches Market Trends

Europe maintains approximately 22% global market share underpinned by strict environmental regulations, advanced manufacturing specialization, and strong emphasis on sustainable plastic solutions. European Union REACH regulations and Single-Use Plastics Directive implementation are compelling manufacturers toward biodegradable masterbatch adoption and recycled content integration, establishing significant market transformation drivers supporting specialty masterbatch demand.

German manufacturing excellence and Swiss chemical industry leadership establish regional technology differentiation, supporting advanced coating systems and specialized additive development, creating premium market positioning. Northern European countries emphasizing circular economy principles and environmental stewardship drive demand for masterbatches engineered for closed-loop recycling and material recovery optimization, establishing differentiation opportunities for manufacturers emphasizing sustainability positioning and environmental responsibility commitment.

Asia Pacific Liquid Masterbatches Market Trends

Asia Pacific commands a dominant global position, accounting for approximately 40% of worldwide liquid masterbatch demand, driven by significant manufacturing expansion, rising adoption of CNC machining, and robust government infrastructure investments. China maintains clear regional leadership as the world's largest plastic converter with exceptional liquid masterbatch consumption spanning packaging, construction, automotive, and electronics manufacturing sectors.

Chinese plastic production exceeding 105 million tons annually drives significant masterbatch consumption, with manufacturers increasingly adopting advanced coatings and specialized geometries to optimize quality. India's manufacturing expansion, demonstrating 7-8% annual growth in masterbatch consumption driven by packaging export acceleration and emerging automotive capabilities, establishes exceptional growth opportunities.

Competitive Landscape

The liquid masterbatches market exhibits significant consolidation among global manufacturers including Clariant AG (Switzerland), Ampacet Corporation (United States), PolyOne (United States), Cabot Corporation (United States), and Tosaf (Israel) collectively commanding dominant market positions through comprehensive product portfolios, established customer relationships, and continuous innovation emphasis.

Mid-market competitors including PLASTIKA KRITIS S.A. (Greece), Plastiblends (India), Penn Color Inc. (United States), and Hubron International (Canada) pursue differentiation through specialized product development, regional market focus, and customer service excellence. Emerging regional manufacturers from China and India establish cost-competitive market positioning through domestic material sourcing and labor efficiency advantages, capturing price-sensitive market segments while established manufacturers pursue premium positioning emphasizing technology differentiation and reliability assurance.

Recent Strategic Developments and Market Trends

- In March 2025, Ampacet Corporation Launches Bio-Based Additive Masterbatch Line Supporting Circular Economy Objectives Ampacet Corporation introduced innovative bio-based additive masterbatch formulations engineered for post-consumer recycled (PCR) plastics supporting manufacturers pursuing circular economy objectives and environmental sustainability commitments.

- In October 2024, Clariant AG Expands Production Capacity in the Asia Pacific Region. Clariant AG announced substantial capacity expansion in Asian manufacturing facilities, targeting emerging market demand growth and supporting regional customer requirements for specialized color and additive masterbatch solutions.

Companies Covered in Liquid Masterbatches Market

- Clariant

- Ampacet Corporation

- Schulman, Inc.

- PolyOne

- Cabot Corporation

- PLASTIKA KRITIS S.A.

- Plastiblends

- Hubron International

- Tosaf

- Penn Color Inc.

- Other Market Players

Frequently Asked Questions

The global liquid masterbatches market was valued at US$ 11.0 billion in 2026 and is projected to reach US$ 15.8 billion by 2033, representing a 5.4% CAGR expansion through the forecast period.

Primary growth drivers include accelerating plastic packaging production with 141 million tons manufactured annually worldwide supporting exceptional liquid masterbatch consumption, and advanced polymer adoption across automotive electrification supporting battery housing and thermal management component manufacturing.

Additive masterbatches dominate with approximately 48% market share expansion driven by versatile functionality including antimicrobial properties, flame retardancy, UV protection, and electrical conductivity enhancements supporting diverse industrial applications.

Asia Pacific maintains dominant position with approximately 40% global market share driven by China's manufacturing leadership with 105 million tons annual plastic production and India's expanding capabilities demonstrating 7% annual growth rate.

Market leaders include Clariant AG, Ampacet Corporation, and Cabot Corporation establishing stronghold positions in carbon black and conductive masterbatch applications. Mid-market competitors including PolyOne, PLASTIKA KRITIS S.A., Tosaf, and Hubron International.