- Pharmaceuticals

- Liquid Embolic Market

Liquid Embolic Market Size, Share, and Growth Forecast, 2026 - 2033

Liquid Embolic Market by Therapeutic Modality (NBCA, Onyx/EVAC, PVA), Application (AVMs, DAVFs, CCFs). Distribution Channel (Hospitals, ASCs, Neurointerventional Centers), and Regional Analysis for 2026 - 2033

Liquid Embolic Market Size and Trends Analysis

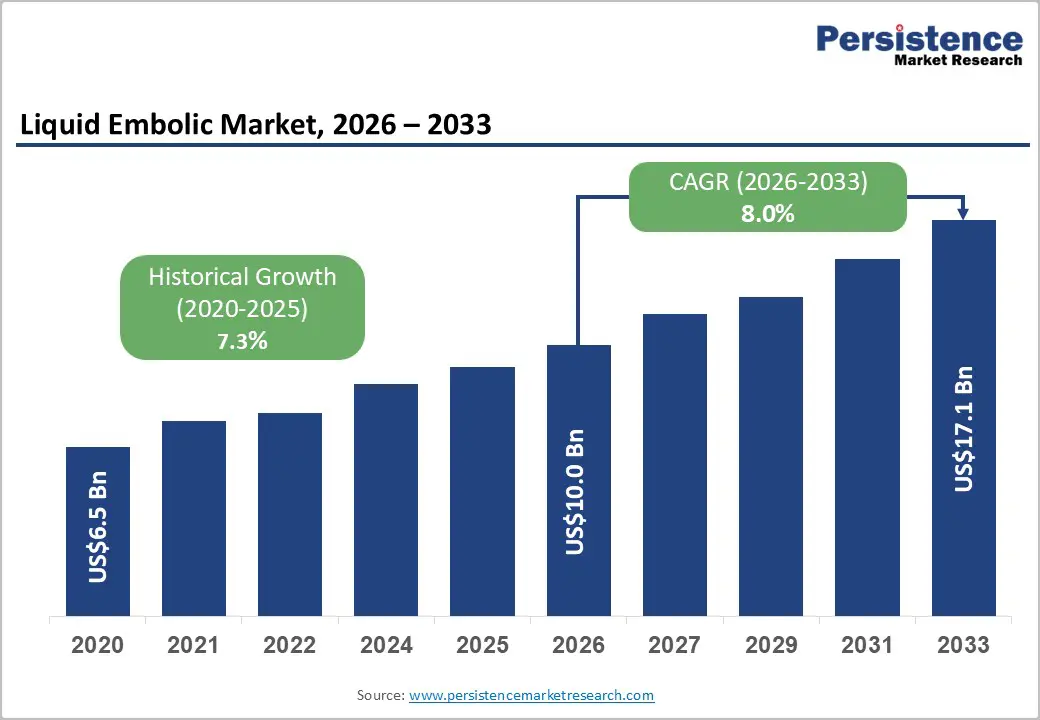

The global liquid embolic market size is likely to be valued at US$ 10.0 billion in 2026, and is expected to reach US$ 17.1 billion by 2033, growing at a CAGR of 8.0% during the forecast period from 2026 to 2033, driven by increasing global incidence of intracranial vascular anomalies, rapid technological advancement in embolic agent formulations, the proliferation of minimally invasive neurointerventional techniques, and improving access to specialized neurovascular centers in emerging markets.

Key Industry Highlights:

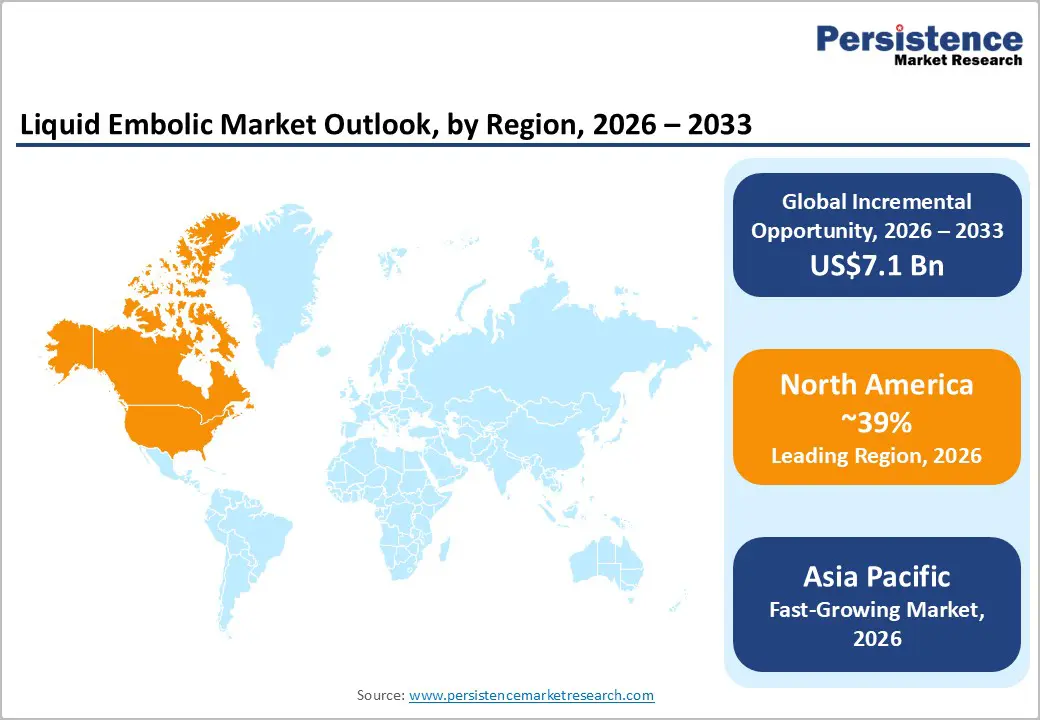

- Dominant Region: North America is projected to dominate the liquid embolic market with about 39% of revenue in 2026, driven by a high burden of cerebrovascular disorders, advanced neurointerventional infrastructure, and early adoption of innovative embolic technologies.

- Fastest-growing Region: Asia Pacific is expected to be the fastest-growing liquid embolic market, due to rising healthcare investments, improving hospital infrastructure, and increasing adoption of advanced neurointerventional procedures.

- Leading Product Type: Ethylene vinyl alcohol copolymer (EVAC/Onyx) is expected to dominate with an estimated 55% revenue share in 2026, due to its non-adhesive properties that enable precise and controlled embolization.

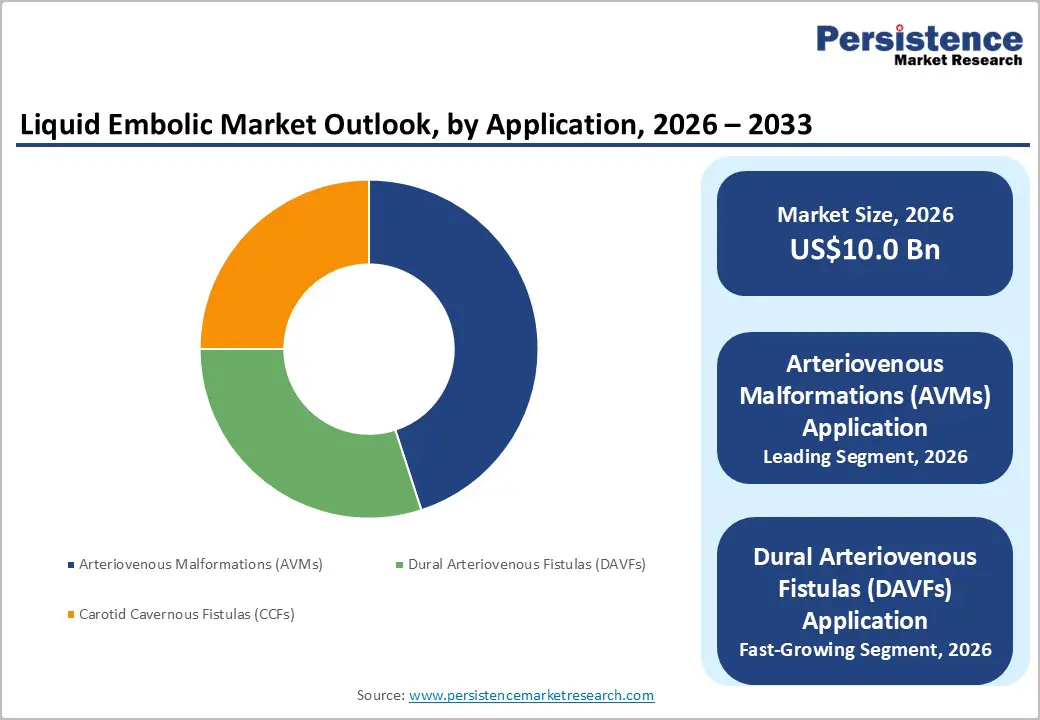

- Dominant End-use Industry: Arteriovenous malformations (AVMs) are expected to dominate the application segment with approximately 45% of market revenues, driven by their reliance on multimodal treatment involving embolization, microsurgery, and radiosurgery.

DRO Analysis

Driver - Technological Advancements in Embolic Agent Formulations

Continuous innovation in liquid embolic chemistries has substantially improved procedural outcomes, expanded clinical indications, and attracted interventionalists to adopt newer agents. Second- and third-generation EVAC formulations (Onyx HD-500 and Precipitating Hydrophobic Injectable Liquid/PHIL) offer enhanced viscosity profiles, enabling more precise penetration into nidus architecture and reducing the risk of non-target embolization. Manufacturers are investing in radiopaque formulations with improved fluoroscopic visibility, DMSO-free carriers to minimize endothelial toxicity, and bioresorbable variants for temporary occlusion.

The integration of 3D rotational angiography and cone-beam CT into neurointerventional suites has further amplified the value proposition of controllable liquid embolic agents, as real-time volumetric imaging allows operators to monitor filling dynamics precisely. Clinical outcomes data published in journals such as the Journal of NeuroInterventional Surgery and the American Journal of Neuroradiology consistently demonstrate complete angiographic obliteration rates of 75-95% with EVAC-based embolization for Grade I-III AVMs, reinforcing physician confidence and driving adoption.

Restraint - High Procedural Complexity and Training Requirements

Liquid embolic procedures represent some of the most technically demanding interventions in neurovascular medicine, requiring a high level of operator expertise, specialized training, and extensive procedural experience. Unlike mechanical devices or particulate embolics, liquid embolic agents must be delivered with exceptional precision through microcatheters positioned within complex and often fragile cerebrovascular networks.

Physicians must possess a detailed understanding of cerebral vascular anatomy, blood flow dynamics, lesion architecture, and the unique properties of each embolic material to ensure safe and effective treatment. Even minor deviations in catheter placement or embolic delivery can have severe consequences. Unintended reflux of the embolic agent into normal cerebral vessels may result in the occlusion of critical arteries supplying functional brain regions responsible for movement, speech, vision, or cognition.

Opportunity - Expanding Applications in Peripheral and Oncological Embolization

Expanding applications in peripheral and oncological embolization are creating significant growth opportunities across the interventional radiology landscape. Peripheral embolization is increasingly used to manage conditions such as peripheral arterial bleeding, vascular malformations, uterine fibroids, benign prostatic hyperplasia, and traumatic injuries. These minimally invasive procedures offer targeted treatment, reduced hospitalization, faster recovery, and lower complication rates compared to traditional surgery, driving wider clinical adoption.

In oncology, embolization techniques including transarterial chemoembolization (TACE), radioembolization, and bland embolization are gaining prominence for treating liver cancer and metastatic tumors. These procedures enable localized delivery of therapeutic agents while preserving healthy tissue, improving treatment outcomes, and patient quality of life. Growing cancer prevalence worldwide, combined with increasing demand for minimally invasive therapies, is accelerating procedure volumes.

Category-wise Analysis

Therapeutic Modality Insights

Ethylene vinyl alcohol copolymer (EVAC/Onyx) is forecast to dominate the therapeutic modality, holding an estimated 55% revenue share in 2026. Its superiority stems from a non-adhesive mechanism that allows controlled, cohesive filling of vascular nidi without premature polymerization at the catheter tip. Onyx™ Liquid Embolic System by Medtronic is an EVOH/EVAC-based non-adhesive liquid embolic agent used to treat brain arteriovenous malformations (AVMs), dural arteriovenous fistulas, hypervascular tumors, and peripheral vascular lesions.

N-Butyl cyanoacrylate (NBCA) is likely to represent the fastest-growing modality. Cost advantages over EVAC, reduced DMSO-related tissue toxicity concerns, and newer glue dilution techniques enabling more predictable polymerization profiles are driving renewed clinical interest. TRUFILL® n-BCA is an N-Butyl Cyanoacrylate (NBCA)-based liquid embolic agent used for the embolization of arteriovenous malformations (AVMs) and other vascular lesions.

Application Insights

Arteriovenous malformations (AVMs) are estimated to dominate the application segment, representing approximately 45% of market revenue in 2026. AVMs are complex, high-flow vascular lesions for which multimodal treatment combining embolization, microsurgery, and radiosurgery is the standard of care. Onyx™ Liquid Embolic System from Medtronic, which is specifically indicated for the presurgical embolization of brain arteriovenous malformations (AVMs).

Dural arteriovenous fistulas (DAVFs) represent the fastest-growing application. Improved neuroimaging protocols have significantly increased DAVF detection rates; a condition historically underdiagnosed now accounts for 10-15% of all intracranial vascular malformations identified in major neurovascular registries. SQUID™ Liquid Embolic System, manufactured by Balt Group. SQUID™ is an EVOH-based liquid embolic agent widely used for the endovascular treatment of dural arteriovenous fistulas (DAVFs) and other neurovascular malformations.

Distribution Channel Insights

Hospitals are expected to dominate the distribution channel, retaining approximately 62% of global market revenue in 2026. Major academic medical centers and tertiary-care hospitals house the hybrid angiographic suites, neurovascular ICUs, and multidisciplinary teams required for complex liquid embolic procedures. The Cleveland Clinic Cerebrovascular Center exemplifies the hospital-dominated end-user segment, combining hybrid neurointerventional operating suites, dedicated Neuro ICU facilities, and multidisciplinary neurovascular teams to support complex liquid embolic procedures for AVMs, DAVFs, and other cerebrovascular disorders.

Ambulatory surgical centers (ASCs) represent the fastest-growing distribution channel. Driven by payer pressure to migrate low-complexity embolization cases out of inpatient hospital settings, ASCs equipped with biplane fluoroscopy are increasingly performing elective embolization for small-volume AVMs, CCFs, and peripheral applications. RIVEA, a specialized vascular and interventional radiology center in India, exemplifies the ASC/outpatient trend by offering same-day embolization procedures for uterine fibroids, varicoceles, and benign prostatic hyperplasia, reducing reliance on traditional inpatient hospital care.

Regional Insights

North America Liquid Embolic Market Trends

North America is projected to dominate the market growth, estimated at approximately 39% of global revenues in 2026. The market is driven by the high prevalence of cerebrovascular disorders such as arteriovenous malformations (AVMs), dural arteriovenous fistulas (DAVFs), and aneurysms, which drive strong procedural demand. The region benefits from advanced neurointerventional infrastructure, widespread availability of specialized stroke and neurovascular centers, and early adoption of innovative embolic technologies.

U.S. Liquid Embolic Market Insights

The U.S. accounts for the overwhelming majority, driven by one of the highest per-capita rates of cerebrovascular imaging and intervention globally. Over 5,533 Joint Commission-certified Comprehensive Stroke Centers operate across the U.S., providing the institutional backbone for liquid embolic procedures.

Canada Liquid Embolic Market Insights

The Canada market, while smaller in absolute terms, benefits from Canada Health Act universal coverage and government-funded neurovascular equipment programmes that have equipped leading centres in Ontario, Quebec, and British Columbia with state-of-the-art biplane angiography suites.

Europe Liquid Embolic Market Trends

Europe represents a significant liquid embolic market due to its well-established healthcare systems, growing adoption of minimally invasive neurovascular procedures, and strong presence of specialized interventional radiology centers. The region benefits from increasing diagnosis of cerebrovascular disorders through advanced imaging technologies.

Germany Liquid Embolic Market Trends

Germany is anticipated to dominate the market in Europe, due to its advanced healthcare infrastructure, high concentration of specialized neurovascular and interventional radiology centers, and strong adoption of minimally invasive treatment techniques. The country benefits from substantial healthcare spending and access to cutting-edge embolization technologies.

U.K. Liquid Embolic Market Trends

The U.K. market is growing steadily, due to increasing adoption of minimally invasive neurovascular and endovascular procedures across major NHS and private healthcare centers. Strong access to advanced diagnostic imaging and specialized interventional radiology services supports early diagnosis and treatment of vascular abnormalities.

Asia Pacific Liquid Embolic Market Trends

Asia Pacific is likely to be the fastest-growing market, driven by rising healthcare investments, expanding access to advanced neurointerventional procedures, and improving hospital infrastructure across emerging economies. The region is witnessing an increasing diagnosis of cerebrovascular disorders as awareness and availability of advanced imaging technologies grow.

China Liquid Embolic Market Trends

China is a major growth market for liquid embolic agents due to the rapid expansion of tertiary hospitals, increasing availability of neurointerventional services, and significant healthcare infrastructure investments. The rising incidence of cerebrovascular diseases and greater use of advanced diagnostic imaging are driving procedure volumes.

India Liquid Embolic Market Trends

India's market is expanding rapidly, due to increasing prevalence of cerebrovascular disorders, growing awareness of minimally invasive treatments, and rising demand for advanced neurointerventional procedures. The country is witnessing significant investments in tertiary-care hospitals, cath labs, and interventional radiology infrastructure.

Competitive Landscape

The global liquid embolic market is moderately consolidated, with a select group of multinational medtech corporations and specialized neurovascular device companies commanding significant market influence. Stryker Corporation and Medtronic plc collectively account for approximately 35-40% of the global market, leveraging their broad endovascular portfolios, established hospital relationships, and global distribution infrastructure.

Johnson & Johnson (Cerenovus), Penumbra, Inc., Terumo Corporation, B. Braun Melsungen AG, and Asahi Intecc Co., Ltd. round out the competitive field. Cerenovus brings the PHIL (Precipitating Hydrophobic Injectable Liquid) platform, a DMSO-compatible, non-adhesive embolic with iodine-based radiopacity as a differentiated entry.

Key Industry Developments:

- In January 2026, Instylla initiated the commercial launch of its Embrace™ Hydrogel Embolic System after Dr. Ripal Gandhi performed the first commercial procedure using the device. The milestone followed FDA premarket approval in 2025 and marked the clinical introduction of the first liquid embolic specifically approved for hypervascular tumor embolization. The company highlighted Embrace™ HES's ability to achieve deep tumor-vessel penetration and sustained vessel occlusion, supporting more precise embolization procedures for cancer patients.

- In March 2024, CERENOVUS, a Johnson & Johnson MedTech company, launched the TRUFILL™ n-BCA Liquid Embolic System Procedural Set, expanding its hemorrhagic stroke treatment portfolio. The company introduced two preconfigured sterile sets that included the accessories required for preparation and delivery, helping clinicians streamline procedural setup and improve workflow efficiency.

Companies Covered in Liquid Embolic Market

- Asahi Intecc Co., Ltd.

- B. Braun Melsungen AG

- Penumbra, Inc.

- Terumo Corporation

- Stryker

- Johnson & Johnson

- Medtronic

Frequently Asked Questions

The global liquid embolic market is projected to reach US$10.0 billion in 2026.

The rising prevalence of cerebrovascular disorders, arteriovenous malformations (AVMs), aneurysms, and hypervascular tumors is driving demand for liquid embolization procedures.

The liquid embolic market is poised to witness a CAGR of 8.0% from 2026 to 2033.

Expanding applications in peripheral embolization and oncology interventions present significant growth opportunities for liquid embolic agents.

Key players include Stryker, Medtronic, Johnson & Johnson (Cerenovus), Penumbra Inc., Terumo Corporation, B. Braun Melsungen AG, Asahi Intecc Co., Ltd., Stryker, and Medtronic.