- LED & Lighting (Optoelectronics)

- Lighting Controllers Market

Lighting Controllers Market Size, Trends, Share, and Growth Forecast, 2025 - 2032

Lighting Controllers Market by Product Type (LED Drivers and Ballasts, Sensors, Switches, Dimmers, Transmitters and Receivers, and Others (Timers and Photosensors), by Connectivity Type (Wired and Wireless), by Application (Residential, Industrial, and Commercial), and Regional Analysis for 2025 - 2032

Lighting Controllers Market Size and Trends Analysis

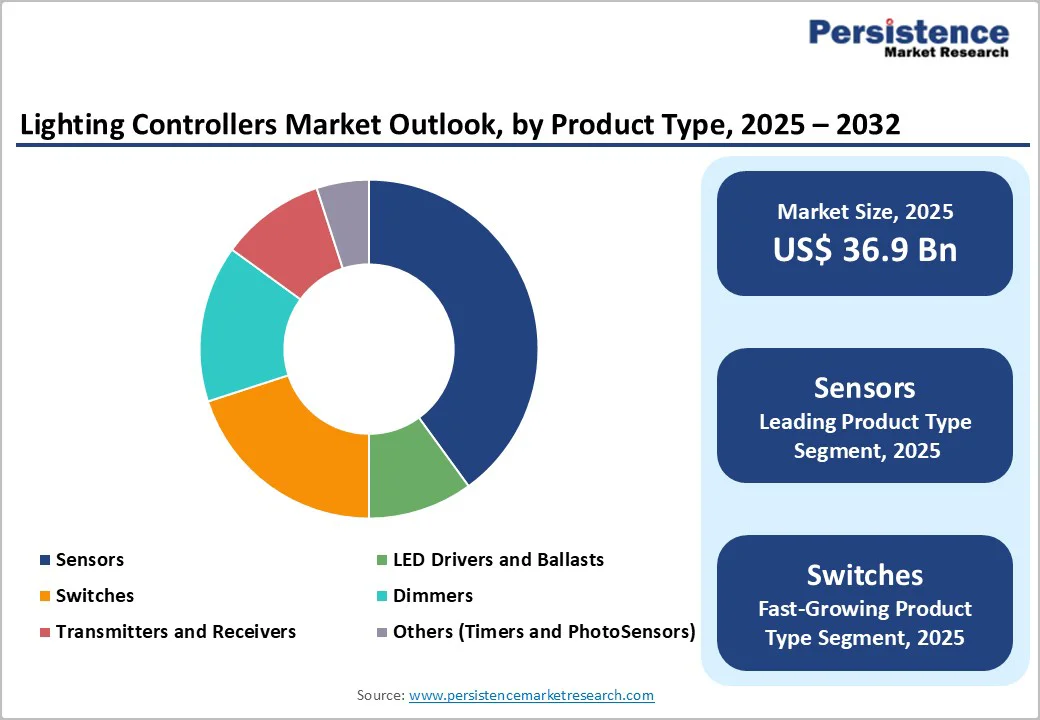

The global lighting controllers market size is valued at US$ 36.9 billion in 2025 and is projected to reach US$ 108.7 billion, growing at a CAGR of 16.7% between 2025 and 2032.

This exceptional expansion reflects accelerating smart building adoption, with lighting accounting for 30% of commercial building energy consumption, IoT integration enabling cloud-based control platforms managing millions of connected luminaires, and regulatory mandates driving 40% energy reduction through occupancy sensors and daylight harvesting systems.

Key Industry Highlights:

- Product Segments: Sensors dominate with 31.2% market share, driven by widespread use in occupancy detection, daylight harvesting, and ambient light monitoring for automated lighting control. Smart switches are the fastest-growing segment, expanding at a 20% CAGR, supported by rising adoption of Wi-Fi and smart switches enabling voice control via Alexa/Google Assistant and remote operation through smartphone apps.

- Connectivity Segments: Wired lighting control systems lead with 64% share, supported by established electrical infrastructure, high reliability, and strong adoption in commercial buildings. Wireless systems represent the fastest-growing segment at 18% CAGR, enabled by Bluetooth Mesh, Zigbee, and Thread protocols that reduce installation costs by 40% and accelerate retrofit deployment in existing buildings.

- Application Segments: Residential applications dominate with 35.5% market share, driven by rapid smart home adoption and integration with connected ecosystems. The commercial segment is the fastest-growing at 17% CAGR, propelled by smart lighting controls achieving 30% energy savings and delivering 2-4-year payback periods in offices, retail, and industrial facilities.

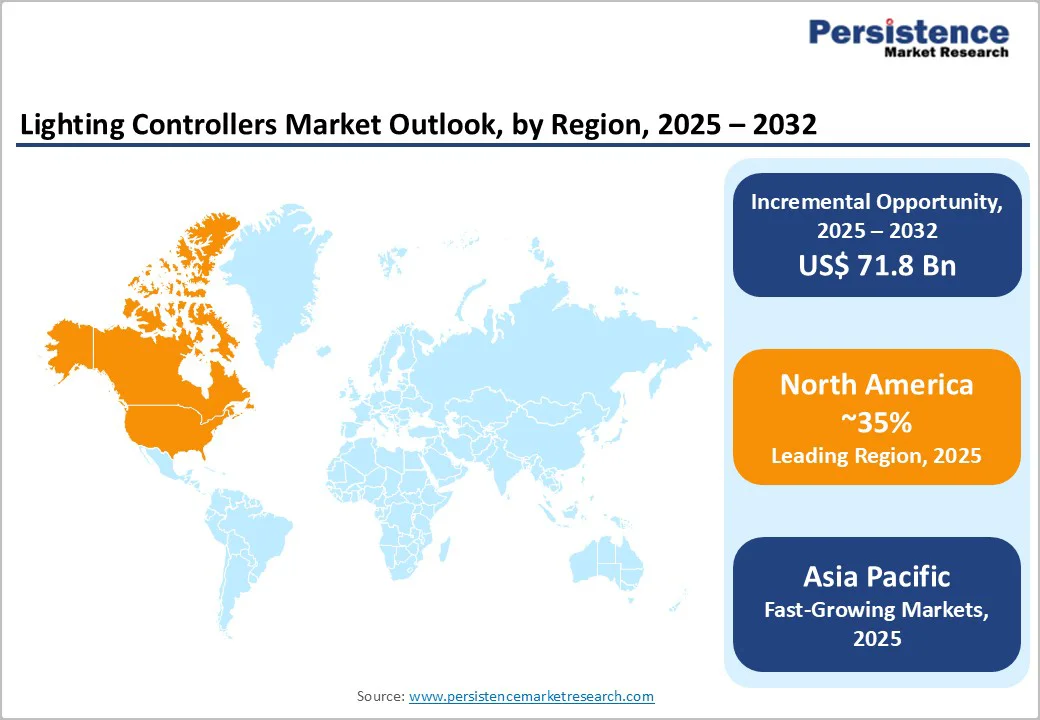

- Regional Dynamics: North America leads with 35% global share and a 15.2% CAGR, supported by DOE lighting mandates, utility rebate programs, and high adoption of connected lighting controls. Asia Pacific is the fastest-growing region with 19.5% CAGR, with China contributing 42% of regional demand and India expanding at a 26% CAGR through smart city and infrastructure modernization initiatives.

- Strategic Market Developments: Signify leads with 14% market share, driven by its Interact IoT lighting platform. Legrand, Acuity Brands, and Lutron maintain strong competitive positioning through integrated control ecosystems. The global retrofit lighting market represents a US$45 billion opportunity, while smart-city lighting initiatives add US$22 billion potential by 2032, powered by municipal LED conversions and IoT-enabled infrastructure upgrades.

| Key Insights | Details |

|---|---|

| Lighting Controllers Market Size (2025E) | US$ 36.9 Bn |

| Market Value Forecast (2032F) | US$ 108.7 Bn |

| Projected Growth (CAGR 2025 to 2032) | 16.7% |

| Historical Market Growth (CAGR 2019 to 2024) | 15.8% |

Market Dynamics

Drivers - Energy Efficiency Mandates and Cost Reduction Imperatives

Global building energy consumption regulations mandating 30% lighting energy reduction through intelligent controls drive comprehensive deployment of automated dimming, occupancy sensors, and daylight harvesting systems, achieving documented 30% energy savings.

Commercial buildings where lighting represents 30% of total energy consumption demonstrate substantial cost reduction opportunities, with integrated lighting control systems enabling 10-30% energy savings through dimming capabilities, 25% through occupancy sensors automatically switching off unoccupied spaces, and 240% through daylight harvesting adjusting artificial lighting based on available natural illumination.

Historic England retrofit case study demonstrates 54% annual energy reduction (4,211 kWh to 1,941 kWh) through daylight harvesting and LED integration, achieving 930 kg CO2 reduction validates the business case for lighting control investment.

U.S. Department of Energy regulations requiring commercial building energy performance disclosure and European Union Energy Performance of Buildings Directive mandating near-zero energy new construction by 2030 create regulatory compliance drivers supporting lighting control adoption.

Smart Building Integration and Building Management System (BMS) Convergence

Commercial building automation evolution toward integrated platforms combining HVAC, lighting, security, and access control systems creates architectural requirements for intelligent lighting controls interfacing with centralized building management infrastructure, optimizing overall facility operations.

Lighting control integration with HVAC systems enabling coordinated operation where unoccupied zones trigger simultaneous lighting shutdown and HVAC setback achieves 15-25% additional energy savings versus independent system operation.

Occupancy data from lighting sensors providing valuable input for HVAC optimization, space utilization analytics, and facility planning creates data value beyond lighting control justifying system investment through multi-system benefits.

Smart city initiatives representing 42.8% of intelligent lighting controls create public infrastructure IoT backbone, with connected streetlights serving as network nodes supporting traffic management, environmental monitoring, public Wi-Fi, and emergency response applications beyond illumination.

Restraints - High Initial Investment and Complex Installation Requirements

Comprehensive lighting control system deployment commanding $8-25 per square foot for commercial applications including hardware, installation labor, commissioning, and system integration creates substantial upfront investment barrier constraining adoption particularly among small-to-medium enterprises.

Wired lighting control systems requiring structured cabling, zone controllers, and centralized management platforms involve extensive installation labor representing 50-70% of total system cost, with retrofit applications facing additional complexity navigating existing building infrastructure and coordinating with ongoing operations.

Commissioning complexity requires trained technicians configuring sensor parameters, establishing zone relationships, programming scenes, and validating system performance extends project timelines 3-6 weeks and adds $2,000-10,000 professional service costs depending on system scale.

Integration challenges combining lighting controls with legacy building management systems, HVAC controllers, and security platforms require middleware solutions and custom programming elevating project complexity and cost 25-40% beyond standalone lighting control deployment.

Interoperability Challenges and Protocol Fragmentation

Lighting control industry fragmentation across competing wireless protocols (Bluetooth Mesh, Zigbee, Thread, EnOcean, KNX) and proprietary manufacturer systems creates interoperability barriers limiting design flexibility and elevating switching costs.

Vendor lock-in concerns where lighting control system selection constrains future fixture procurement to compatible manufacturers deter investment, with retrofit or expansion projects often requiring complete system replacement when switching vendors versus incremental additions.

Standards development lag behind technology advancement creates specification uncertainty, with emerging protocols lacking proven track record and established ecosystem deterring risk-averse commercial building owners from early adoption.

Cybersecurity vulnerabilities in wireless lighting systems create network access points potentially exploitable for unauthorized building access or data exfiltration, requiring comprehensive security architecture including network segmentation, encryption, and access controls elevating system complexity.

Market Opportunities

Retrofit Market and Existing Building Modernization

Global installed commercial building stock exceeding 200 billion square feet represents massive retrofit opportunity, with lighting control penetration below 15% in existing buildings creating addressable market of $120-180 billion for wireless retrofit solutions.

Wireless lighting control systems eliminating rewiring requirements enable economically viable retrofit deployment with payback periods of 2-4 years through energy savings, compared to 5-8 years for traditional wired systems where installation labor dominates costs.

Government retrofit incentive programs including U.S. utility rebates covering 30-50% of lighting control costs, EU green building grants, and India's Energy Conservation Building Code enforcement create financial incentives accelerating adoption.

Aging lighting infrastructure with 40% commercial lighting exceeding 15-year service life creates natural replacement cycles, with LED retrofit projects providing optimal timing for concurrent lighting control deployment achieving synergistic benefits.

Smart City Infrastructure and Municipal Lighting Modernization

Global smart city investment exceeding $150 billion annually with intelligent street lighting serving as foundational infrastructure creates substantial public sector opportunity, with connected luminaires enabling city-wide IoT network supporting multiple municipal services.

LED streetlight conversion programs across major cities including Los Angeles (215,000 lights), New York (250,000+), and London (50,000+) provide deployment opportunity for integrated lighting controls achieving 50% energy savings beyond LED conversion alone through dimming and adaptive scheduling.

Streetlight pole utilization for smart city sensors including traffic monitoring, air quality measurement, gunshot detection, and public Wi-Fi access points justifies lighting control system investment through multi-application infrastructure sharing.

Adaptive street lighting systems adjusting brightness based on traffic density, pedestrian presence, and time-of-night optimize safety while minimizing energy consumption and light pollution, with demonstration projects achieving 40-50% additional savings beyond static dimming schedules.

Category-wise Analysis

Product Type Insights

Sensors command 31.2% market share due to their critical role in occupancy detection, daylight measurement, and ambient light monitoring, enabling automated lighting systems that deliver significant energy savings.

PIR sensors activate lighting based on heat and motion, while photocell sensors support daylight harvesting by dimming or switching lights off when natural light is sufficient. Dual-technology sensors combining PIR and ultrasonic detection ensure accuracy in low-motion environments such as offices and classrooms.

Switches are the fastest-growing segment at about 18% CAGR, driven by rising adoption of smart switches offering wireless control, app-based operation, and voice integration with Alexa or Google Assistant. Smart dimmers and battery-free wireless switches support easy retrofits, flexible layouts, and premium user convenience.

Connectivity Type Insights

Wired systems command 64% market share due to their strong installed base in commercial buildings, superior reliability, and compliance with stringent safety and performance standards. Established protocols such as DALI enable individually addressable dimming across up to 64 devices, while 0-10V analog dimming remains widely used for cost-effective, simple control architectures. Their proven performance in mission-critical environments continues to support long-term adoption.

Wireless systems are the fastest-growing segment at about 18% CAGR, driven by 50% installation cost savings, easy retrofitting, and seamless IoT integration. Bluetooth Mesh and Zigbee support large, self-healing networks with 65,000+ nodes, while Thread provides IPv6-native connectivity. Smartphone configuration, cloud control, and flexible deployment accelerate wireless lighting controller adoption.

Application Insights

Residential applications command 35.5% market share, driven by the vast number of households, strong smart-home adoption, and consumer preference for easy DIY installations. High penetration of smart switches, dimmers, and voice-controlled devices (35-40% in many markets) supports steady growth, while wireless retrofit solutions that require no rewiring make smart lighting accessible to non-technical users.

Commercial applications are the fastest-growing segment at roughly 17% CAGR, propelled by energy-saving mandates, sustainability targets, and improved occupant comfort. Offices achieve 30% lighting energy reduction using occupancy sensors, daylight harvesting, and automated dimming, offering 2-4 year payback periods. Retail environments benefit from dynamic lighting scenes that enhance product visibility, customer engagement, and overall store ambiance while reducing energy costs.

Regional Market Insights

North America Lighting Controllers Market Trends

North America generates approximately US$12.9 billion market value in 2025 representing 35% global market share growing at 15.2% CAGR through 2032, driven by established commercial building stock, stringent energy codes, and technology adoption leadership.

The United States dominates regional market with 82% North American share through Department of Energy efficiency mandates, utility rebate programs incentivizing lighting control adoption, and smart building technology development.

California Title 24 energy code requiring lighting controls in all new commercial construction and major renovations creates regulatory compliance driver supporting market growth. Canadian market contributing 9% regional share through provincial energy efficiency programs and green building certification adoption.

Europe Lighting Controllers Market Trends

Europe represents US$9.2 billion market in 2025, capturing 25% global market share growing at 16.8% CAGR through 2032, characterized by strict energy efficiency regulations, sustainability leadership, and comprehensive building automation deployment. Germany leads European market with 28% regional share through energy efficiency mandate leadership, KNX protocol development, and industrial building automation expertise.

European Union Energy Performance of Buildings Directive mandating near-zero energy construction and major renovation energy upgrades creates regulatory framework supporting lighting control adoption. United Kingdom, France, and Nordic markets demonstrating growth through smart city initiatives, LED streetlight conversion programs, and commercial building energy disclosure requirements.

Asia Pacific Lighting Controllers Market Trends

Asia Pacific represents fastest-growing region at approximately 19.5% CAGR through 2032, with estimated market value reaching US$46 billion by 2032 comprising 30% global market share by 2032, driven by urbanization, smart city development, and manufacturing capacity advantages.

China dominates Asia Pacific with 42-48% regional share through government smart city initiatives, LED manufacturing leadership, and commercial building construction boom supporting lighting control infrastructure deployment.

India emerging as high-growth market at 22-26% CAGR through Smart Cities Mission targeting 100 cities, growing commercial real estate sector, and government energy efficiency programs including Energy Conservation Building Code enforcement.

Japan and South Korea contributing 16% combined regional share through technology leadership, advanced building automation deployment, and earthquake-resilient infrastructure requirements. Southeast Asia represents 12% regional growth through ASEAN economic development, urbanization acceleration, and green building adoption.

Competitive Landscape

The lighting controllers market exhibits moderate-to-high fragmentation with leading players commanding approximately 40% combined market share, while specialized regional suppliers, lighting fixture manufacturers, and control system integrators capture remaining segments.

Signify (Philips Lighting) emerges as market leader with estimated 14% market share through comprehensive Interact platform, global distribution network, and integrated lighting/control systems. Legrand maintains competitive positioning with 10% market share through building automation expertise, DALI protocol leadership, and North American market strength.

Key Industry Developments

- In April 2024, CISCO and Toronto-based Morgan Solar announced a pilot project to enhance collaboration and meeting spaces with solar power. The startup promotes the development of intelligent solutions that aim to reduce greenhouse gas emissions from traditional energy production technologies and provide companies with new paths to sustainable development.

- In December 2023, General Electric Company invested around USD 1,907 million and USD 1,786 million in 2023 and 2022, respectively. The company's investment drives the development of cutting-edge technologies, such as advanced sensors, wireless controls, and AI-driven systems.

Companies Covered in Lighting Controllers Market

- Hubbell

- GE Lighting, LLC

- OSRAM Light AG

- Philips Lighting Holding B.V

- Acuity Brands Lighting, Inc.

- Eaton Corporation

- Schneider Electric S.E

- Honeywell International

- Lutron Electronics

- Cree, Inc

- Other Market Players

Frequently Asked Questions

The Lighting Controllers market is estimated to be valued at US$ 36.9 Bn in 2025.

The key demand driver for the Lighting Controllers market is the global push for energy efficiency and regulatory compliance, which is accelerating the adoption of smart, automated lighting systems across residential, commercial, and industrial spaces.

In 2025, the North America region will dominate the market with an exceeding 35% revenue share in the global Lighting Controllers market.

Among the Product Types, Sensors hold the highest preference, capturing beyond 31.2% of the market revenue share in 2025, surpassing other Product Types.

The key players in the Lighting Controllers market are Hubbell, GE Lighting, LLC, OSRAM Light AG, and Philips Lighting Holding B.V.