- Home Care & Utilities

- Residential Lighting Fixtures Market

Residential Lighting Fixtures Market Size, Share, and Growth Forecast, 2025 - 2032

Residential Lighting Fixtures Market By Product Type (Ceiling Fixtures, Pendant & Chandeliers), Light Source (LED/OLED, Incandescent), Distribution Channel, Application, and Regional Analysis for 2025 - 2032

Residential Lighting Fixtures Market Size and Trends Analysis

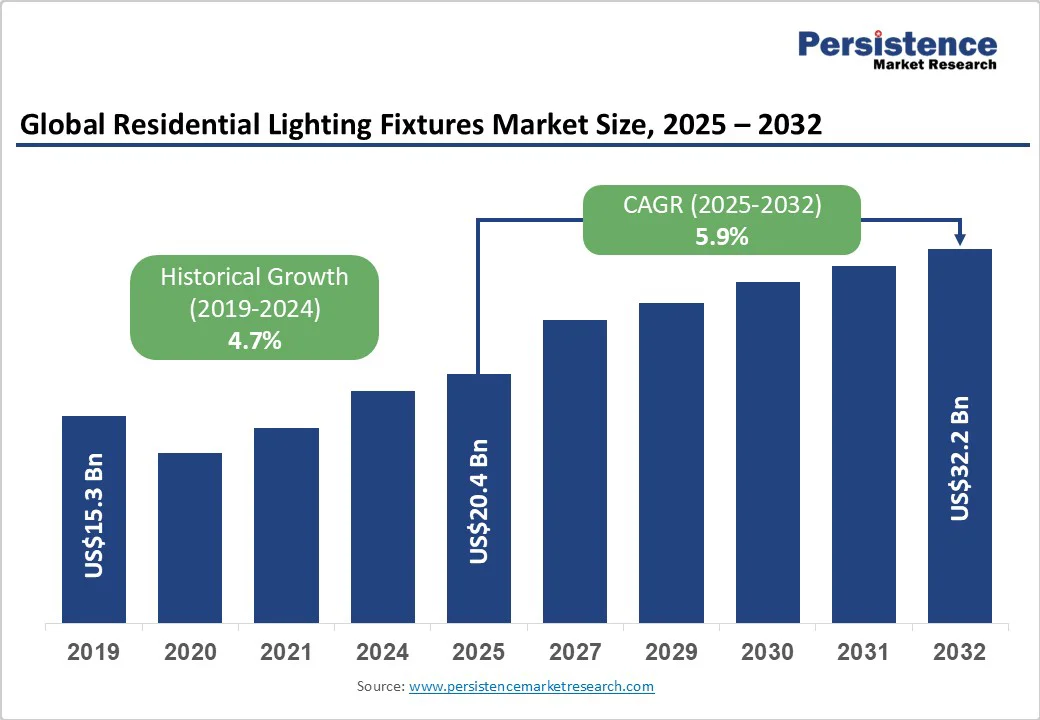

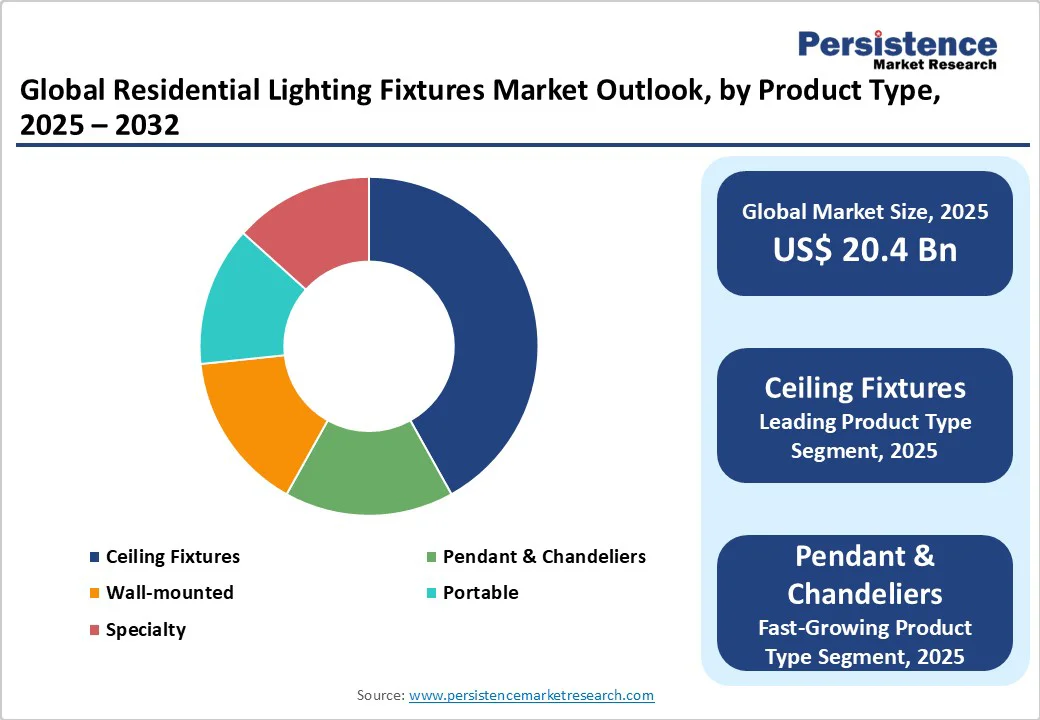

The global residential lighting fixtures market size was valued at US$20.4 Bn in 2025 and is projected to reach US$32.2 Bn by 2032, growing at a CAGR of 5.9% between 2025 and 2032, driven by the rapid adoption of LED replacements, growing integration of smart lighting technologies, increased residential construction and renovation activity in Asia Pacific and North America, and the rising demand for connected, human-centric lighting solutions.

Energy-efficiency regulations and incentive programs have shifted demand toward LED and integrated luminaires, while online retail channels provide consumers with broader product access and faster purchase cycles.

Key Industry Highlights

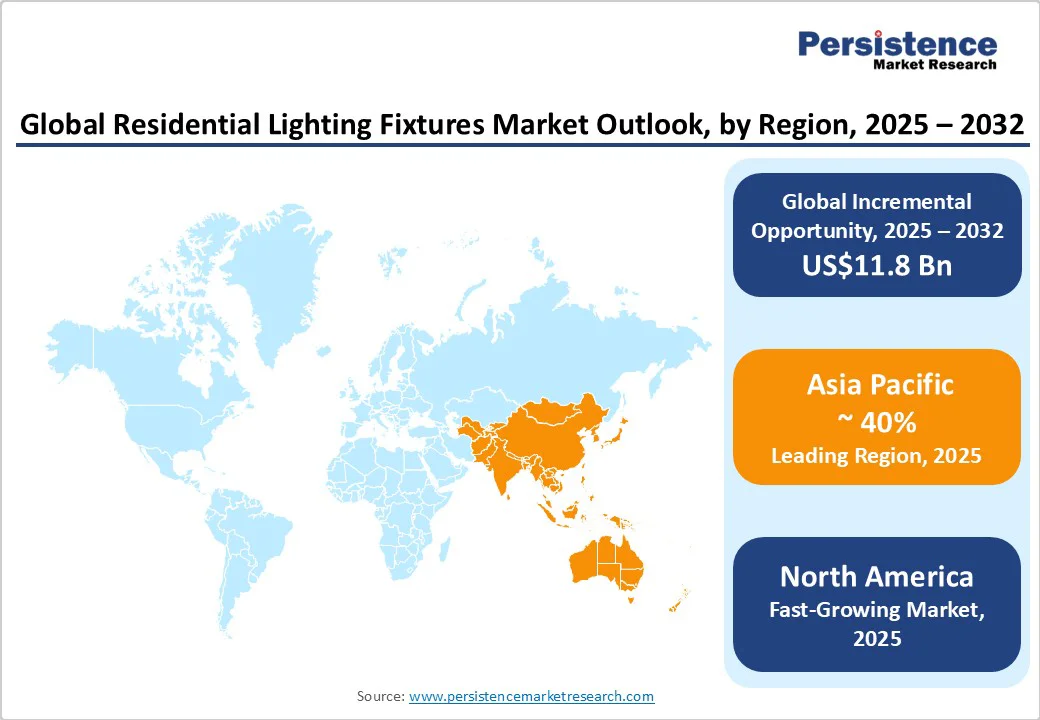

- Leading Region: Asia Pacific, with nearly 40% market share in 2025, driven by China’s manufacturing scale, domestic adoption, and rising middle-class consumption.

- Fastest-growing Region: North America, projected CAGR of 6.2% between 2025 and 2032, supported by smart-home adoption, energy-efficiency regulations, and renovation activity.

- Investment Plans: Companies are focusing on smart-home integrated systems, LED panel expansion, and IoT platform partnerships, with key investments exceeding US$500 Mn across major markets in 2024 - 2025.

- Dominant Product Type: Ceiling fixtures, accounting for approximately 44% of revenue, due to standardization in new construction and retrofit projects.

- Leading Light Source: LED & OLED, representing 50% of total market sales, supported by energy-efficiency regulations, government incentives, and growing consumer preference for long-lasting, low-energy solutions.

| Key Insights | Details |

|---|---|

| Market Size (2025E) | US$20.4 Bn |

| Market Value Forecast (2032F) | US$32.2 Bn |

| Projected Growth (CAGR 2025 to 2032) | 5.9% |

| Historical Market Growth (CAGR 2019 to 2024) | 4.7% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - LED Penetration and Regulatory Push

Global LED adoption continues to reshape the market, with LEDs representing approximately half of residential lighting sales in 2022. Policies in North America, Europe, and Asia target nearly 100% LED adoption in the mid-2020s. These regulations stimulate retrofit demand and drive higher ASPs for integrated luminaires. Incentives from governments and utilities, combined with rising energy-efficiency standards, support sustainable market growth while enabling manufacturers to invest in advanced, higher-margin product lines.

Smart and Human-Centric Lighting Adoption

The rise of smart homes and wellness-focused lighting has created demand for connected luminaires that integrate dimming, circadian rhythms, and voice-control compatibility. Smart and integrated fixtures are experiencing faster growth than traditional lamps, particularly in North America and Europe, where disposable income and technological infrastructure support premium adoption. Partnerships between lighting manufacturers and IoT/cloud platform providers accelerate product development and reduce time-to-market for feature-rich luminaires.

Residential Construction and Renovation Cycles

Increased housing starts, renovation spending, and urbanization in Asia Pacific and parts of Europe boost fixture installations per dwelling. Developers prefer integrated, energy-efficient fixtures to meet code requirements and market expectations, while renovations often prioritize decorative or smart upgrades. These macroeconomic and demographic trends drive predictable, high-volume demand, particularly for ceiling and recessed systems.

Barrier Analysis - Price Pressure from Imports and Commoditized Products

A significant portion of the market is highly price-sensitive, with low-cost imports exerting pressure on mid-market suppliers. Commodity fixtures often yield thin margins, compelling manufacturers to differentiate through smart features or premium design. Price competition limits revenue growth despite high unit volume, posing challenges for firms lacking brand equity or proprietary IP.

Supply Chain and Component Volatility

LED drivers, chips, and electronic controls face supply volatility and price fluctuations, which can affect fixture costs and delivery schedules. Manufacturers lacking diversified supplier networks or long-term agreements risk margin erosion and delayed shipments. Outsourced smart components and software services also increase post-sale support obligations, adding operational complexity.

Opportunity Analysis - Retrofit and Energy-Efficiency Programs

Government and utility-led retrofit initiatives for multifamily housing and public projects present sizable market potential. Bundled solutions including finance, certified installation, and performance guarantees can capture high-volume demand. These programs also open recurring revenue opportunities through monitoring, maintenance, and replacement services.

Smart Services and Subscription Models

Beyond hardware, subscription services such as energy monitoring, extended warranties, and software updates provide recurring revenue streams. Integrated lighting systems connected with home automation platforms allow cross-selling with HVAC, security, and wellness solutions. Companies standardizing on open protocols and secure update channels can accelerate adoption and increase customer lifetime value.

Category-wise Analysis

Product Type Insights

Ceiling fixtures, including recessed downlights, flush mounts, and integrated panel systems, dominate with a 44% share in the market. Their prevalence in new construction and renovation projects stems from standardized installation practices and performance reliability. For example, in the U.S., recessed LED downlights are specified in over 60% of new residential builds due to energy efficiency and compatibility with modern ceiling designs.

In Europe, integrated ceiling panels are widely adopted in multifamily housing projects to comply with eco-design regulations, providing consistent illumination while reducing energy consumption. Developers and contractors favor ceiling systems for their low maintenance requirements and long-term operational efficiency.

Decorative pendants, chandeliers, and smart ceiling-hanging luminaires are experiencing the fastest growth due to rising consumer demand for aesthetic differentiation and connected-home capabilities. For instance, products such as Philips Hue’s decorative smart pendants or IKEA’s TRÅDFRI smart pendant systems allow homeowners to adjust color temperature, brightness, and light schedules through apps or voice assistants.

Urban homeowners increasingly prioritize style and wellness, driving the adoption of features such as tunable white lighting for circadian alignment. Average selling prices for these premium products are higher, contributing to revenue growth even with lower volume compared to ceiling fixtures.

Light Source Insights

LED and OLED luminaires account for approximately 50% of residential lighting sales globally, a share that continues to rise due to superior energy efficiency, longer operational lifespan, and compliance with international energy regulations. LEDs have effectively replaced incandescent bulbs in most developed markets; for example, in Germany and the U.S., energy efficiency standards have phased out most incandescent lamps in residential settings.

OLED panels are gaining traction in premium applications due to their ultra-thin profiles, uniform light diffusion, and design flexibility, often used in high-end kitchens, living rooms, or offices within homes. LED adoption is supported by utility rebate programs and government incentives, encouraging rapid market penetration.

Integrated LED fixtures and OLED panels, which combine the light source and fixture into a single unit, are growing at the highest CAGR. These products offer energy savings of up to 50% compared to conventional LED lamps, reduce maintenance frequency, and provide slimmer, modern aesthetics that suit contemporary interior designs.

Examples include the Cree SmartCast integrated LED panels, which are increasingly used in multifamily housing projects, and LG OLED ceiling panels designed for high-end residential and luxury apartments. The growth of smart homes also accelerates demand for integrated luminaires compatible with platforms such as Google Home, Amazon Alexa, or Apple HomeKit, enabling automated lighting schedules and color-tunable options.

Distribution Channel Insights

Traditional offline channels, including specialty lighting stores, electrical wholesalers, and home improvement chains, remain the largest revenue contributors in most regions. These channels cater to a wide customer base ranging from homeowners to contractors and developers. For example, Home Depot and Lowe’s in the U.S., Leroy Merlin in France, and B&Q in the U.K. provide extensive ceiling fixture selections, LED panels, and decorative pendants.

Project-based procurement by developers and builders also dominates volume sales, where fixtures are often selected based on architectural specifications or brand reputation. This segment benefits from tactile product evaluation, expert advice, and bundled installation services, which are important for high-value or complex fixture types.

E-commerce and DTC channels are expanding rapidly due to convenience, wider product selection, and the ability to target niche consumer preferences. Platforms such as Amazon, Wayfair, and Flipkart enable brands, including Philips Hue, IKEA, and Syska, to reach a broader audience and offer product customization, subscription-based lighting controls, and remote support.

E-commerce facilitates quicker market entry for emerging brands, allowing them to offer unique designs, app-integrated smart features, and energy-efficient solutions without extensive physical retail investment. The digital channel also provides manufacturers with valuable consumer insights, helping to refine product offerings, improve after-sales services, and drive repeat purchases.

Regional Insights

North America Residential Lighting Fixtures Market Trends - Smart-Home Integration and Energy Efficiency Drive the U.S. Market Growth

North America is the fastest-growing market, primarily driven by the U.S., which is projected to generate nearly US$2.8 Bn in 2025. Growth is fueled by rising smart-home adoption, stringent energy-efficiency regulations, and increasing residential renovation and construction activity. State-level energy codes, such as California’s Title 24, encourage the installation of energy-efficient LED and smart fixtures in both new and existing homes.

Consumers are also showing strong preference for connected lighting solutions, including app-controlled and voice-enabled systems, which has led manufacturers such as Acuity Brands, Signify, and Eaton to focus on technology integration and smart-home compatibility.

Recent developments include Eaton’s launch of a connected lighting system in 2024, targeting urban residential projects in the U.S., and Acuity Brands’ 2025 partnership with a major IoT platform to enhance smart fixture interoperability. In Canada, government rebate programs for energy-efficient lighting have accelerated LED adoption in residential renovations, making it a significant growth contributor.

Europe Residential Lighting Fixtures Market Trends - Energy Efficiency and Smart Decorative Lighting Lead Premium Residential Markets

Europe represents a high-value market, with Germany, the U.K., and France leading adoption due to robust energy-efficiency standards and harmonized regulatory frameworks. Germany emphasizes contractor-led specifications and technical innovation, where integrated LED panels and smart ceiling luminaires are widely adopted in multifamily housing and premium residential projects. The U.K. and France are experiencing rising demand for decorative and smart lighting solutions, driven by urban renovations and premium residential developments.

European Union eco-design and energy-label requirements favor certified manufacturers, which benefits companies such as Zumtobel, OSRAM, and Signify. Notable developments include Zumtobel’s 2024 launch of tunable white LED panels with integrated IoT controls in Germany and OSRAM’s 2025 introduction of connected chandeliers in France, targeting high-end residential interiors. In Spain, the renovation segment is expanding due to government incentives for energy-efficient lighting in older housing, contributing to overall market growth.

Asia Pacific Residential Lighting Fixtures Market Trends - Largest Volume Market Fueled by Urbanization, LED Adoption, and Smart Technology

Asia Pacific is the largest volume market for residential lighting fixtures, led by China’s extensive manufacturing base and domestic demand. Rapid urbanization, rising middle-class income, and government initiatives for energy-efficient housing fuel market growth. In India, the push for LED adoption through programs such as the UJALA scheme has significantly increased residential LED penetration, particularly in urban and semi-urban areas. ASEAN countries, including Thailand and Indonesia, are experiencing similar growth trends driven by new housing projects and urban infrastructure development.

Japan leads in design and technological adoption, with advanced OLED panels and smart integrated fixtures gaining traction in luxury apartments. Key developments include Philips Hue’s 2024 expansion of smart residential lighting products in China and India, targeting premium urban segments, and Panasonic’s 2025 launch of integrated LED ceiling panels in Japan that combine energy efficiency with app-controlled lighting. Competitive intensity is high, with global brands focusing on premium and smart categories while local manufacturers compete on price, creating opportunities for retrofit projects, smart-home integration, and localized manufacturing.

Competitive Landscape

The global residential lighting fixtures market is moderately fragmented, with a few global leaders and numerous regional players. Leading firms such as Signify, Acuity Brands, OSRAM/LEDVANCE, Eaton, and Zumtobel dominate premium and spec-driven channels. Market concentration is higher in smart lighting, where intellectual property, platform integration, and service capabilities are differentiators.

Leading firms pursue product premiumization, platform-based offerings, and cost leadership. Key differentiators include integrated smart systems, developer partnerships, and multi-channel distribution.

Key Industry Developments

- In April 2025, Signify launched the Philips LightTheatre in India, a plug-and-play smart lighting system that synchronizes ambient lighting with on-screen content from movies, music, and games, enhancing home entertainment experiences.

- In January 2025, Philips Hue introduced an AI-powered lighting assistant, enabling users to create personalized lighting scenes based on various occasions, moods, or styles, with compatibility across all Philips Hue lights.

- In December 2024, IKEA updated its Home smart mobile app to include a dynamic lighting feature that automatically adjusts the color temperature and brightness of its smart lights throughout the day, promoting well-being.

Companies Covered in Residential Lighting Fixtures Market

- Signify (Philips Lighting)

- Acuity Brands

- OSRAM/LEDVANCE

- Zumtobel Group

- Eaton (Cooper Lighting Solutions)

- GE Lighting

- Hubbell Lighting

- Legrand

- Panasonic

- Samsung Electronics

- LG Electronics

- Havells

- Bajaj Electricals

- Syska

- Wipro Lighting

- Cree/Lumileds

- Schneider Electric

- Fagerhult Group

- Thorn Lighting

- Sharp Corporation

Frequently Asked Questions

The residential lighting fixtures market size is estimated at US$20.4 Bn in 2025.

The lighting fixtures market is projected to reach US$32.2 Bn by 2032.

Key trends include LED and OLED adoption, smart-home integration, decorative lighting demand, energy-efficiency regulations, and e-commerce expansion.

Ceiling fixtures lead the lighting fixtures market, accounting for approximately 44% of revenue, due to standardization in new construction and retrofit projects.

The residential lighting fixtures market is expected to grow at a CAGR of 5.9% from 2025 to 2032.

Major players in the residential lighting fixtures market include Signify (Philips Lighting), Acuity Brands, OSRAMLEDVANCE, Zumtobel Group, and Eaton (Cooper Lighting Solutions).