- LED & Lighting (Optoelectronics)

- LED & OLED Lighting Products and Displays Market

LED & OLED Lighting Products and Displays Market Size, Share, and Growth Forecast, 2026 - 2033

LED & OLED Lighting Products and Displays Market by Technology (LED, MiniLED, MicroLED, OLED, Flexible OLED), Product Type (Lighting (Bulbs, Fixtures, Panels), Displays (Mobile, TV, Monitor, Automotive, Digital Signage), Application (Residential, Commercial, Industrial, Automotive, Consumer Electronics), and Regional Analysis for 2026 - 2033

LED & OLED Lighting Products and Displays Market Share and Trends Analysis

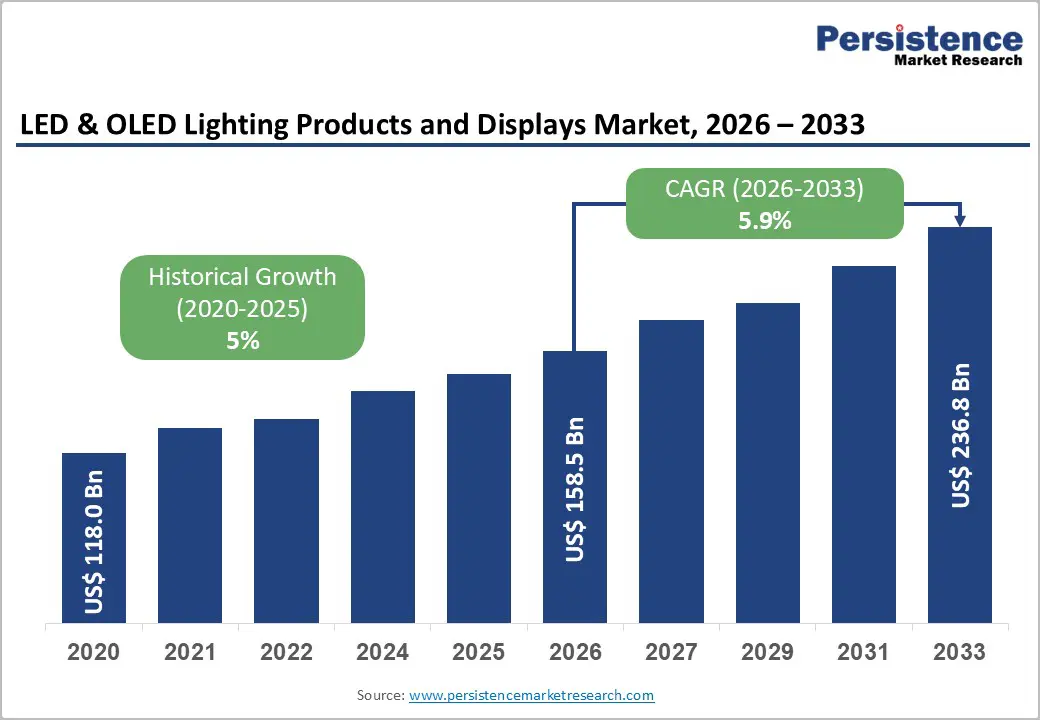

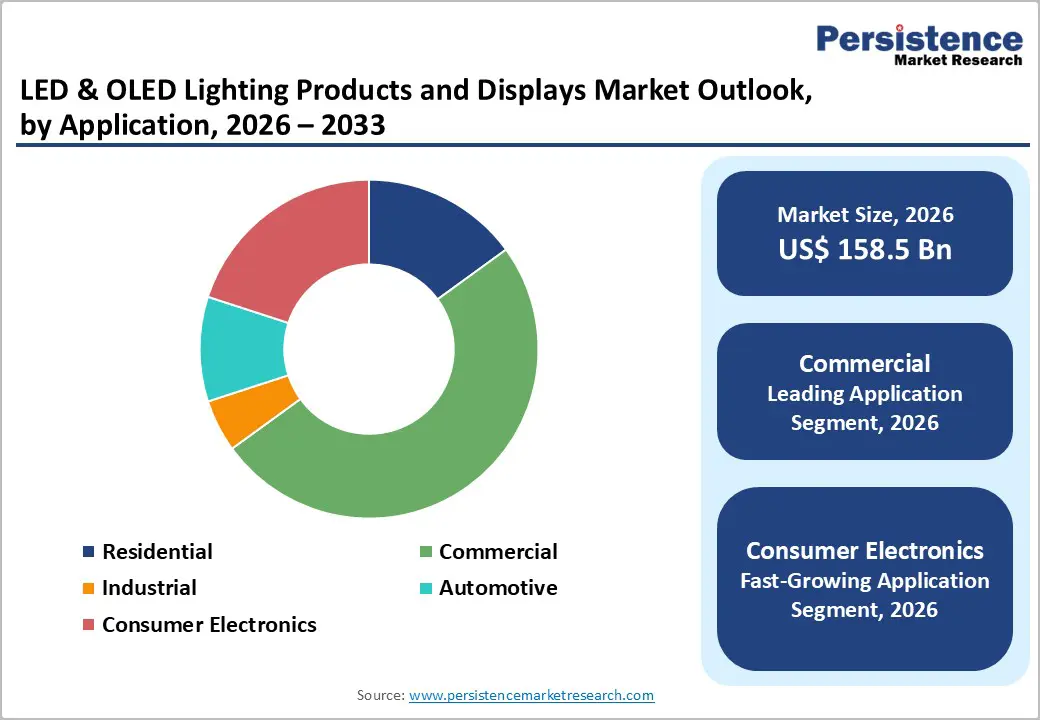

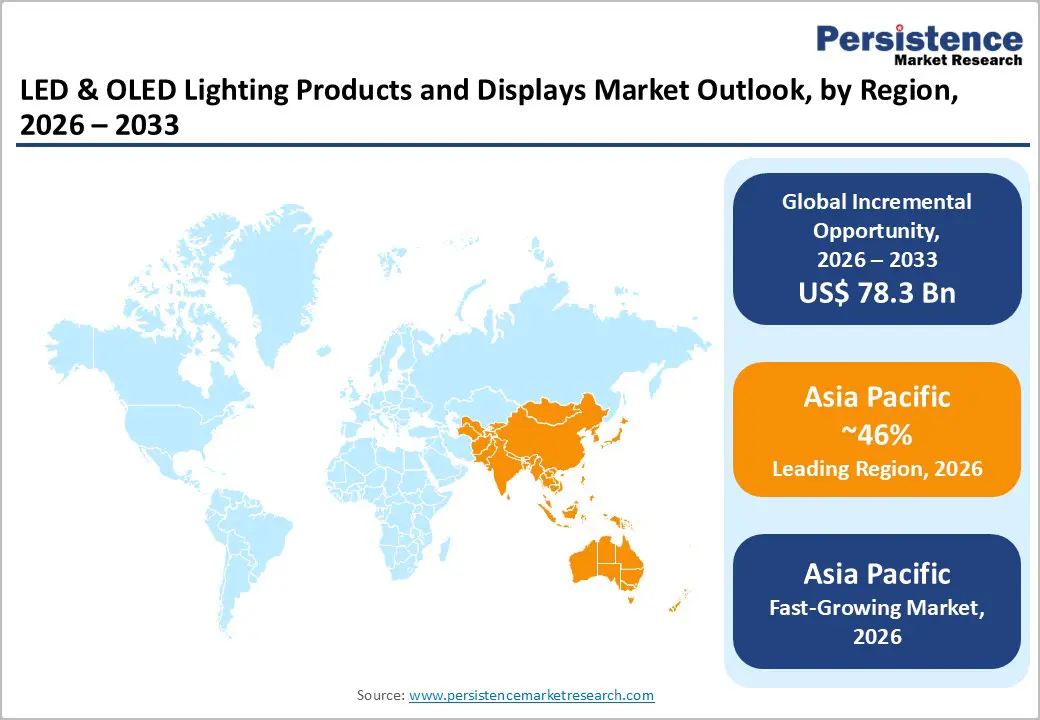

The global LED & OLED lighting products and displays market size is likely to be valued at US$ 158.5 billion in 2026, and is projected to reach US$ 236.8 billion by 2033, growing at a CAGR of 5.9% during the forecast period of 2026–2033.

The market continues to expand steadily, supported by strong structural demand drivers rather than short-term cyclical spikes. Growth is underpinned by tightening global energy-efficiency regulations, government-led LED transition initiatives, and the accelerated replacement of conventional lighting systems with smart, connected alternatives. In displays, increasing OLED penetration in premium smartphones, televisions, and automotive infotainment systems is strengthening value growth. Commercialization of MiniLED and MicroLED technologies is further enhancing performance standards in brightness, energy efficiency, and form factor flexibility. Meanwhile, sustained capital investments in Asia-Pacific manufacturing hubs and global decarbonization commitments are reinforcing long-term supply stability and demand visibility across lighting and display applications worldwide.

Key Industry Highlights

- Dominant Technology: LED technology is set to command approximately 63% of revenue share in 2026, while MicroLED is likely to grow the fastest through 2033, driven by next-generation form factor innovation.

- Leading Product Type: Lighting products are projected to hold nearly 57% of total revenue in 2026, while advanced display solutions are expected to record the highest 2026-2033 CAGR, supported by performance upgrades across consumer and commercial screens.

- Dominant Application: Commercial applications are anticipated to account for around 50% of revenue share in 2026, while consumer electronics applications are forecast to grow the fastest at about 11% CAGR through 2033, reflecting vehicle digitalization and premium device penetration.

- Regional Leadership: Asia Pacific is poised to dominate with an estimated 46% share in 2026 and register an 8.5% CAGR through 2033, led by manufacturing scale and semiconductor ecosystem depth.

- February 2026: Samsung unveiled its next-generation QD-OLED Penta Tandem display technology featuring a five-layer organic light-emitting structure that significantly boosts brightness, efficiency, and lifespan.

| Key Insights | Details |

|---|---|

| LED & OLED Lighting Products and Displays Market Size (2026E) | US$ 158.5 Bn |

| Market Value Forecast (2033F) | US$ 236.8 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.9% |

| Historical Market Growth (CAGR 2020 to 2025) | 5% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Regulatory-Led Energy Transition and Smart Infrastructure Modernization

Energy efficiency policies remain the strongest structural driver. According to the International Energy Agency (IEA), lighting accounts for approximately 15% of global electricity consumption. The transition to LED lighting reduces energy usage by up to 75% compared to incandescent lamps, significantly lowering operating costs for households, businesses, and municipalities. The U.S. Department of Energy (DOE) finalized updated efficiency standards in 2023–2024, mandating higher lumens-per-watt thresholds, effectively phasing out inefficient bulbs by 2025. The European Union’s Ecodesign Directive and India’s UJALA program have collectively accelerated LED penetration beyond 50% in many markets. This regulatory push creates structured replacement demand cycles, strengthens compliance-driven procurement, and stabilizes long-term revenue visibility for lighting manufacturers and component suppliers.

Industry developments from past years further reinforce this transition. At the 30th Guangzhou International Lighting Exhibition (GILE 2025), leading manufacturers introduced high-efficiency, smart-enabled LED systems targeted at urban infrastructure and industrial applications, signaling continued product innovation aligned with regulatory goals. These solutions emphasized integrated sensors, adaptive dimming, and connected control systems designed to optimize municipal energy consumption. In the automotive segment, Marelli unveiled next-generation OLED-TFT rear lighting systems at Auto Shanghai 2025, reflecting how vehicle electrification is accelerating demand for advanced, energy-efficient lighting technologies. As electric vehicles prioritize reduced power draw and design differentiation, advanced LED and OLED lighting becomes a strategic component. Together, these developments demonstrate that policy mandates are translating directly into commercialization, technology upgrades, and sustained capital deployment across lighting ecosystems.

Expansion of Consumer Electronics and Advanced Display Technologies

Global smartphone shipments remain above 1.1 billion units annually, as per 2024 industry data, with OLED panels increasingly dominant in premium and mid-range segments. OLED technology now accounts for over 50% of smartphone display revenues globally due to superior contrast ratios, deeper blacks, and thin form factors that enable sleeker device designs. Consumers continue to prioritize high-resolution, energy-efficient displays across smartphones, tablets, and televisions, driving continuous panel upgrades. MiniLED backlighting adoption in premium TVs and monitors is expanding rapidly, improving brightness, color accuracy, and local dimming performance. These technological advancements are increasing the average selling price of advanced display panels and enhancing profitability across the value chain.

At the TCL CSOT Display Tech-Ecosystem Conference (DTC 2025), the company showcased advancements in OLED and MicroLED production aimed at scaling large-format and automotive display applications. The event highlighted progress in yield improvement and panel efficiency, indicating readiness for broader commercialization. Coverage by The Verge in its 2026 TV industry outlook emphasized how major global brands are accelerating MiniLED and OLED deployments across flagship television models to meet premium consumer demand. Manufacturers are also investing in larger screen sizes and higher refresh rates to capture gaming and home entertainment markets. These developments confirm that next-generation display technologies are moving from innovation cycles into sustained commercial expansion, reinforcing long-term revenue growth in the displays segment.

Raw Material and Semiconductor Supply Volatility

LED and OLED production relies on semiconductor wafers, rare earth phosphors, and driver integrated circuits (ICs). Supply chain disruptions in 2024–2025, particularly related to geopolitical tensions affecting semiconductor exports, increased component costs by 8–12% in certain markets. Manufacturers face margin compression due to fluctuating gallium and indium prices. Smaller players remain vulnerable to inventory risks, which may slow expansion plans and affect short-term capital expenditure cycles. Volatility in upstream material sourcing also complicates long-term procurement contracts and pricing stability. As a result, cost predictability remains a key operational challenge across the value chain.

Recent industry developments underscore ongoing supply constraints. Semiconductor Manufacturing International Corp (SMIC) has announced major wafer capacity expansion but warned that rising depreciation costs and equipment timing mismatches are squeezing margins, highlighting persistent supply complexity in key components. Additionally, Qualcomm and Arm publicly reported that global memory chip shortages, particularly DRAM and related components, are significant enough to impact smartphone and consumer electronics production through 2027, illustrating structural allocation pressures. Lead times for automotive-grade memory and other semiconductors are lengthening, forcing manufacturers to hold larger inventories and negotiate complex contracts, which introduces further procurement risk and cost uncertainty.

High Capital Costs of OLED and MicroLED Manufacturing

OLED and MicroLED fabrication require advanced deposition and encapsulation processes with significant yield challenges. Capital expenditure for new display fabs can exceed US$ 5–10 billion per facility (company disclosures from major panel manufacturers). High upfront investments and lower yield rates limit rapid scalability, especially for MicroLED. This structural barrier slows price parity with LCD alternatives and may delay broader adoption in cost-sensitive segments. Complex mass-transfer processes and precision manufacturing requirements further elevate operational risk. Consequently, only a limited number of global players possess the financial capacity to scale next-generation display production.

The display industry itself is undergoing a structural change that reinforces this restraint. Major players in South Korea have shifted away from traditional LCD manufacturing to focus on OLED and next-generation displays, which concentrates investment needs and raises barriers to entry for smaller firms. At the same time, high fixed costs and capital intensity remain fundamental hurdles: the need to finance multi-billion-dollar fabrication plants with advanced production lines persists despite strong end-market demand. Lower production yields for advanced displays further increase per-unit cost, meaning price parity with incumbent alternatives is delayed, and cost-sensitive customers remain cautious. These economic realities continue to restrict the rapid expansion of OLED and MicroLED manufacturing capacity globally.

MicroLED Commercialization and Premium Display Expansion

MicroLED offers superior brightness and lifespan compared to OLED. As pilot production lines expand in 2025, premium TV and AR/VR device manufacturers are evaluating integration. The premium TV segment (above US$ 2,000 price range) represents a multi-billion-dollar annual revenue opportunity. As yields improve, MicroLED could capture 5–8% of high-end display revenues by 2030, creating incremental value for semiconductor-integrated lighting companies. Early commercial momentum is visible as leading brands prepare consumer products that leverage tiny, independently controlled LEDs for unparalleled contrast and energy efficiency. These developments signal a shift from laboratory breakthroughs to real market introductions for next-generation screens.

In addition to consumer TVs, MicroLED adoption potential extends into automotive displays, immersive wearables, and mixed-reality headsets. For example, Samsung has confirmed plans to debut a 115-inch MicroLED TV at CES 2026, showcasing premium large-format applications and reinforcing industry confidence in the technology’s future. These high-profile product showcases, combined with ongoing technical progress in mass transfer and full-color integration, suggest that MicroLED could begin to narrow the cost gap with incumbent technologies over the coming years. Commercial successes in premium segments will strengthen value capture for component makers and display original equipment manufacturers (OEMs) alike, widening the opportunity horizon beyond niche B2B to broader consumer adoption.

Smart Lighting Expansion and Emerging Market Penetration

Human-centric lighting solutions that adjust color temperature based on circadian rhythms are gaining traction in commercial offices and healthcare facilities. Smart lighting systems are increasingly integrating IoT-enabled LED panels, enabling remote monitoring, automation, and energy optimization. In 2025, municipalities including Delhi and Ahmedabad have moved forward with citywide smart LED streetlight upgrades, integrating real-time monitoring, centralized control systems, and automated fault detection to improve efficiency and safety. These deployments create recurring service revenue opportunities for infrastructure providers and technology partners, extending value beyond initial hardware sales into long-term managed services.

At the same time, LED adoption in parts of Africa, South Asia, and Latin America remains below developed market averages, representing substantial untapped demand. Government electrification programs and falling LED prices are creating new procurement cycles for public and private lighting projects. Smart lighting integration is becoming a core component of broader urban digital transformation efforts, with IoT-enabled poles increasingly supporting connectivity, environmental sensing, and public safety functions. This trend positions LED infrastructure as a foundation for future smart city deployments, where recurring operational services, data analytics, and connectivity platforms will drive ongoing investment and revenue growth across emerging and established markets alike.

Category-wise Analysis

Technology Insights

LED is expected to remain the leading technology segment, commanding around 63% of the LED & OLED lighting products and displays market revenue share in 2026. Its sustained dominance is anchored in cost efficiency, long operational life, and compliance with tightening global energy-efficiency mandates. Government procurement programs, residential retrofits, and commercial lighting modernization reinforce high LED adoption. Urban infrastructure projects continue to specify LED luminaires for lower operational costs and predictable maintenance cycles. Integration with smart control systems adds value beyond basic illumination. As energy codes become stricter, LEDs maintain their central role in both retrofit and new-build projects globally.

MicroLEDs are poised to be the fastest-growing display technologies, projected to expand at approximately 15% CAGR through 2033. Momentum in 2025–2026 reflects meaningful industry support: AUO Mobility Solutions is showcasing advanced MicroLED displays at CES 2026, including transparent and interactive modules tailored for automotive and premium spaces, signaling commercial readiness for next-generation applications. Display innovators such as Tianma unveiled multiple breakthrough display technologies at TIC 2025, expanding capabilities across AR/VR and automotive panels, underscoring broader ecosystem evolution. These developments indicate that high-performance displays are transitioning from prototype phases into scalable solutions, feeding accelerated adoption in premium electronic and mobility sectors.

Application Insights

Commercial applications are anticipated to lead by capturing roughly 50% of the LED & OLED lighting products and displays market share in 2026. Steady replacement cycles in homes and ongoing commercial retrofits sustain recurring demand for traditional and smart LED lighting. Urban development and infrastructure modernization continue to prioritize upgraded lighting, with smarter controls and energy reporting features becoming standard specifications. Industrial facilities and logistics hubs are also increasingly adopting adaptive LED solutions for energy savings and compliance with environmental standards. Integration with building automation platforms is further enhancing application value. This broad base of demand anchors stable revenue and mitigates short-term volatility.

Consumer electronics are likely to represent the fastest-growing application segment, expanding at an estimated 11% CAGR during the 2026-2033 forecast period. In the automotive space, next-generation lighting systems are gaining traction; for example, LG Innotek won the CES 2026 Innovation Award for its ultra-thin automotive lighting module, emphasizing energy-efficient, advanced vehicle illumination and V2X communication capabilities. Automotive OLED and pixel-based solutions such as dynamic rear lamps and ground projection systems exhibited at Auto Shanghai 2025 illustrate rising design and safety integration demand. On the consumer electronics side, TV and wearable makers are pushing richer display technologies, with the 2026 TV industry landscape seeing diverse adoption of advanced LED/OLED formats. These trends together are driving value-intensive growth in displays and integrated lighting systems across mobility and connected consumer devices.

Regional Insights

North America LED & OLED Lighting Products and Displays Market Trends

North America is a major contributor to global market revenue, supported by strong regulatory enforcement and sustained infrastructure upgrades. In 2025, the U.S. DOE announced additional funding rounds under its Building Technologies Office to accelerate high-efficiency solid-state lighting adoption across federal facilities. Commercial retrofit programs spanning offices, warehouses, and logistics hubs continue to stimulate demand for advanced LED luminaires. The rapid scaling of U.S.-based electric vehicle (EV) production is strengthening demand for adaptive LED headlamps and fully digital cockpit displays. Semiconductor reshoring initiatives are improving component supply stability and reducing import dependency. Innovation hubs in California and Texas remain active in advancing MicroLED and AR/VR display prototypes. Increased defense and aerospace display applications are further supporting high-performance OLED development across specialized segments.

The region is projected to grow steadily through 2033, reflecting stable, policy-backed demand. In early 2026, Reuters reported expanded OLED investment commitments by U.S.-based display technology firms targeting defense and immersive display applications, reinforcing high-value segment growth. Federal smart-city grants are accelerating intelligent streetlight deployments integrated with traffic management and public safety systems. Corporate sustainability mandates across commercial real estate portfolios are pushing large-scale lighting efficiency upgrades. Venture funding into spatial computing hardware in 2025 continues to support next-generation display demand. Semiconductor fabrication incentives are strengthening domestic manufacturing ecosystems and supply chain resilience.

Europe LED & OLED Lighting Products and Displays Market Trends

Europe remains a significant contributor to global demand, fueled by sustainability regulations and automotive leadership. In 2025, the European Commission (EC) advanced implementation measures under the Green Deal Industrial Plan, reinforcing stricter energy-efficiency benchmarks for lighting systems across member states. Public infrastructure modernization projects across Germany and France are replacing legacy sodium-vapor lamps with smart LED networks. Germany’s strong automotive OEM ecosystem continues to drive advanced lighting modules and OLED rear-display integration. European Union (EU)-wide regulatory harmonization reduces compliance complexity for manufacturers operating across multiple countries. Sustainable construction mandates are accelerating smart lighting integration in commercial buildings. Investment in energy-efficient renovation of older and historical buildings is further contributing to fixture upgrades.

The region is expected to expand steadily through 2033, supported by electrification and building decarbonization initiatives. In 2026, BBC and Financial Times coverage highlighted increased investment by European automotive suppliers into next-generation digital lighting systems for EV platforms, reinforcing high-value display integration trends. Municipalities across Spain and the Nordic countries expanded sensor-integrated street-lighting systems in 2025 to enhance energy monitoring and urban analytics. Circular economy regulations are encouraging longer-lasting, high-efficiency LED fixture adoption. Automotive digital cockpit innovation continues to increase OLED penetration in premium vehicle segments. Strong alignment with carbon neutrality targets ensures long-term procurement stability. Europe’s combination of regulatory clarity and automotive innovation sustains predictable and structured market growth.

Asia Pacific LED & OLED Lighting Products and Displays Market Trends

Asia Pacific is poised to dominate with approximately 46% of the LED & OLED lighting products and displays market value in 2026, supported by manufacturing scale and domestic consumption growth. In 2025, China’s Ministry of Industry and Information Technology (MIIT) reiterated policy support for advanced semiconductor and display manufacturing, reinforcing regional OLED and MicroLED capacity expansion. South Korean manufacturers announced additional OLED production line upgrades in 2025, widely covered by Reuters, aimed at automotive and large-format display applications. Japan continues investing in next-generation display materials and encapsulation technologies. India’s infrastructure modernization programs are accelerating public LED streetlight tenders. ASEAN urbanization further strengthens lighting replacement cycles. Export-oriented production continues to reinforce the region’s dominance in global supply chains.

Asia Pacific is also the fastest-growing region at 8.5% CAGR through 2033, driven by rising middle-class electronics demand and EV expansion. In 2026, leading Asian panel manufacturers confirmed increased capital allocation toward MicroLED pilot lines, signaling commercialization momentum in premium TVs and AR devices. Large-scale smart-city initiatives across India and Southeast Asia are integrating connected LED systems with traffic and surveillance networks. Regional supply chain integration enhances cost competitiveness and export capacity. Expanding domestic EV production across China, Japan, and Korea is accelerating adoption of OLED and adaptive LED modules. Increasing government incentives for advanced manufacturing are further supporting capacity expansion. The region remains the primary engine of global volume, innovation, and long-term industry growth.

Competitive Landscape

The global LED & OLED lighting products and displays market structure is moderately consolidated, with major players including Signify, ams-OSRAM, Samsung Electronics, LG Display, Panasonic, and Nichia holding a significant revenue share. These companies benefit from vertically integrated operations, strong patent portfolios, and deep OEM partnerships across automotive and consumer electronics sectors. Continuous R&D investment supports advancements in high-efficiency LEDs, flexible OLED panels, and MicroLED commercialization. Large-scale manufacturing capabilities, particularly in Asia, strengthen cost leadership and supply reliability. Strategic focus remains on performance optimization, smart integration, and premium display innovation.

Regional and specialized players such as BOE Technology, TCL CSOT, AUO, Seoul Semiconductor, and Everlight Electronics compete through niche expertise and capacity expansion. High capital requirements and complex semiconductor processes create substantial entry barriers. Automotive-grade quality standards further limit new participant penetration. However, IoT-enabled smart lighting platforms are enabling software-driven firms to enter via partnerships. Ongoing consolidation and strategic collaborations continue to shape competitive intensity and technological evolution.

Key Industry Developments

- In January 2026, LG Electronics won over 139 awards at CES, including multiple “Best of Innovation” honors for its OLED evo W6 and G6 TVs, recognized for ultra-slim design, AI-powered processors, and reflection-free display technology. The company’s AI-driven CLOiD home robot also received the “Best Robot” distinction, reinforcing LG’s leadership in premium OLED displays and smart home integration.

- In December 2025, HARMAN announced a definitive agreement to acquire ZF Group’s ADAS division for €1.5 billion, with closure expected in H2 2026. The deal integrates ZF’s radar, camera, and compute technologies with HARMAN’s digital cockpit systems, strengthening its position in software-defined vehicles and advanced automotive display ecosystems.

- In October 2025, TCL CSOT finalized its ¥ 11.088 billion acquisition of LG Display’s 8.5-generation LCD panel plant and module factory in Guangzhou. This move marks LG Display’s strategic exit from large-size LCD manufacturing in China while strengthening TCL’s global LCD market share, contributing to increased consolidation among leading Chinese panel makers.

Companies Covered in LED & OLED Lighting Products and Displays Market

- Signify N.V.

- Samsung Electronics Co., Ltd.

- LG Display Co., Ltd.

- OSRAM GmbH

- Panasonic Holdings Corporation

- Sony Group Corporation

- Nichia Corporation

- Cree LED

- Acuity Brands, Inc.

- Zumtobel Group AG

- BOE Technology Group

- TCL Technology

- Sharp Corporation

- Seoul Semiconductor

Frequently Asked Questions

The global LED & OLED lighting products and displays market is projected to reach US$ 158.5 billion in 2026.

Growth is driven by energy-efficiency regulations, rising OLED display adoption, automotive digitalization, and smart lighting integration.

The market is poised to witness a CAGR of 5.9% from 2026 to 2033.

Key opportunities include MicroLED commercialization, EV-integrated displays, and smart infrastructure lighting projects.

Major players include Signify, ams-OSRAM, Samsung Electronics, LG Display, Nichia, BOE Technology, and TCL CSOT.