- Technology

- Solid State and Other Energy Efficient Lighting Market

Solid State and Other Energy Efficient Lighting Market Size, Trends, Share, and Growth Forecast 2026 - 2033

Solid State and Other Energy Efficient Lighting Market by Technology (Solid-state Lighting, Fluorescent Lighting, HID Lighting, Plasma, Induction Lighting), Installation Type (New, Retrofit), Application (General Lighting, Backlighting, Automotive Lighting, Medical Lighting, Other), and Regional Analysis for 2026 - 2033

Solid State and Other Energy Efficient Lighting Market Size and Trend Analysis

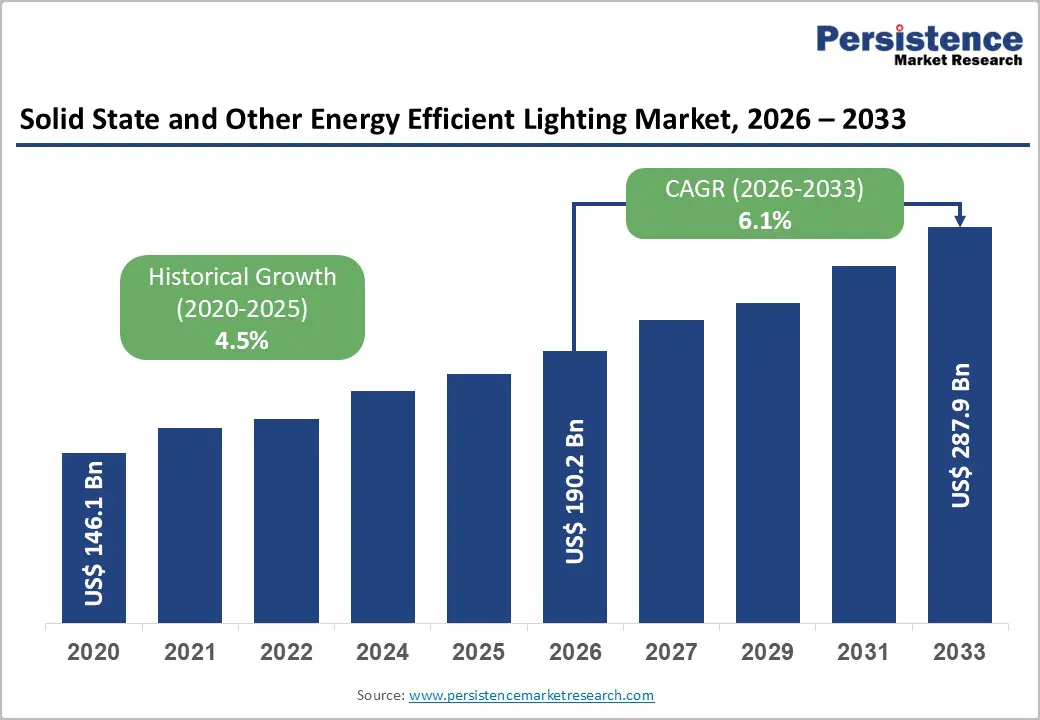

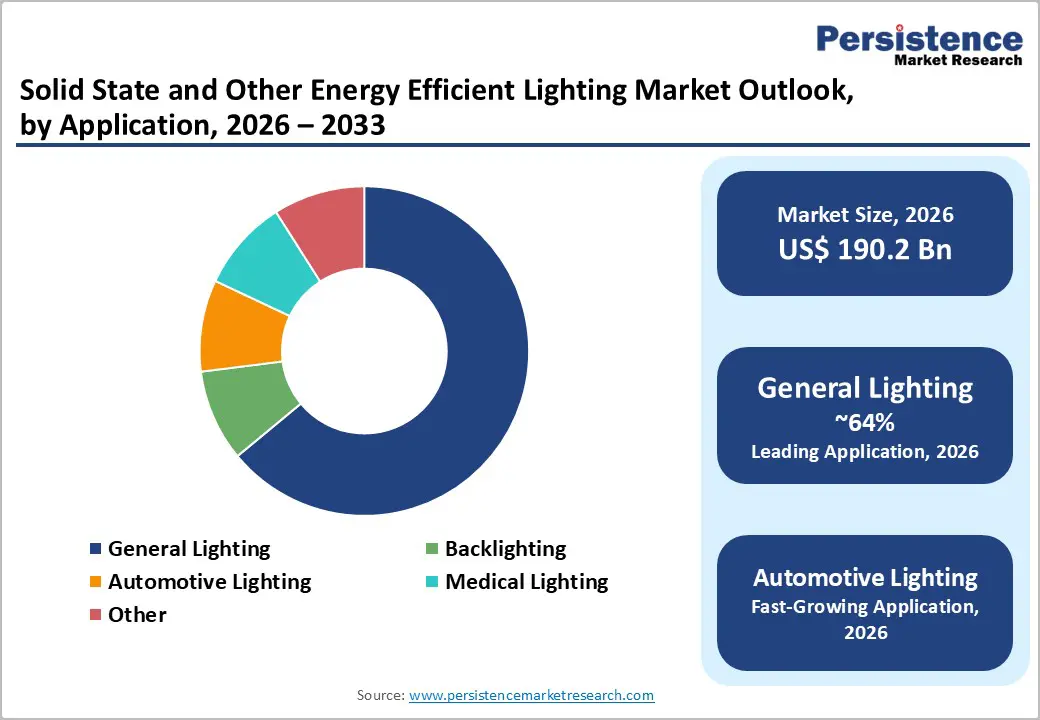

The global solid state and other energy efficient lighting market size is likely to be valued at US$ 190.2 billion in 2026 and is projected to reach US$ 287.9 billion by 2033, growing at a CAGR of 6.1% between 2026 and 2033.

Stringent global regulations phasing out inefficient lighting accelerate the adoption of energy-efficient alternatives like LEDs. Governments worldwide have implemented comprehensive bans on incandescent and fluorescent lighting, with the U.S. Department of Energy requiring light bulbs to produce at least 45 lumens per Watt from August 2023 and 147 countries committing to the complete phase-out of fluorescent lamps by 2027, creating mandatory demand for LED, OLED, and other solid-state alternatives. Advancements in efficacy beyond 220 lm/W further support cost reductions and widespread integration across sectors.

Key Industry Highlights:

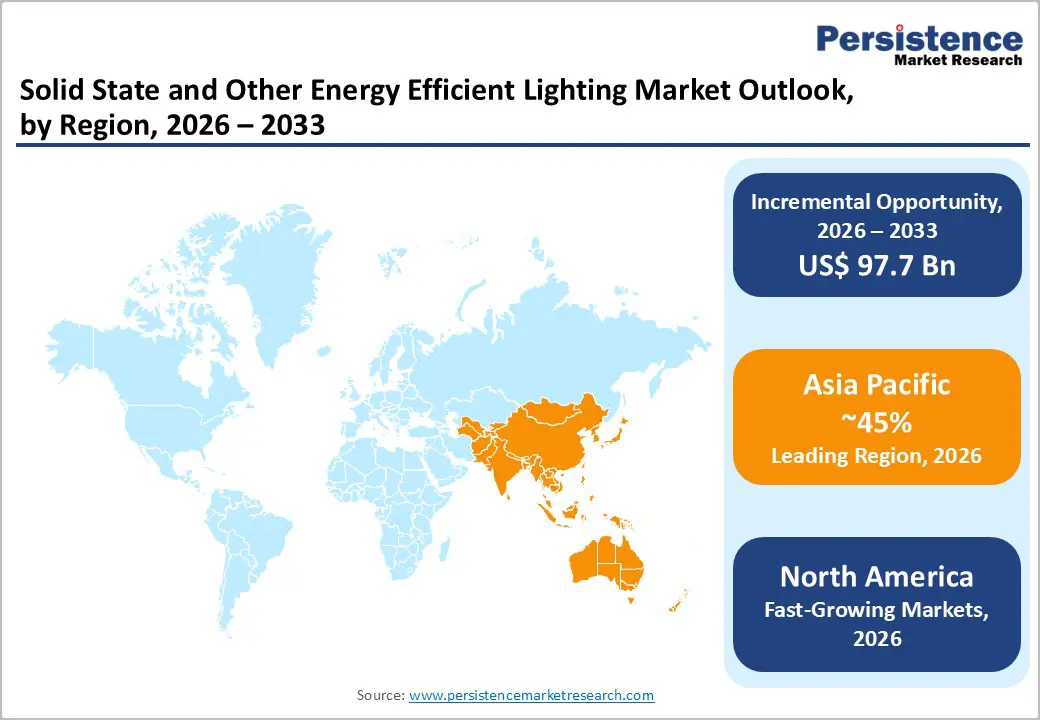

- Leading Region: Asia Pacific dominates the market, capturing approximately 45% of the global market, driven by rapid urbanization, industrial expansion, and government-backed smart city initiatives across China, India, Japan, and Southeast Asia.

- Fastest Growing Region: North America emerges as the fastest growing region, driven by an advanced regulatory framework, strong government incentives, and early adoption of digital lighting technologies.

- Leading Segment: Solid-State Lighting technology commands the largest market segment, representing 72% market share, driven by superior energy efficiency delivering 90% energy reduction, extended operational lifespans of 25,000-50,000 hours, and reduced maintenance requirements.

- Fastest Growing Segment: Retrofit Installation represents the fastest-growing installation category, projected to expand more rapidly than new construction demand, driven by accelerating replacement of legacy fluorescent, HID, and incandescent fixtures in existing infrastructure, supported by government incentive programs.

- Key Opportunities: Automotive Lighting and Smart Connected Systems represent exceptional growth opportunities as electric vehicle adoption accelerates and advanced driver assistance system penetration expands.

| Key Insights | Details |

|---|---|

| Solid State and Other Energy Efficient Lighting Market Size (2026E) | US$ 190.2 Bn |

| Market Value Forecast (2033F) | US$ 287.9 Bn |

| Projected Growth CAGR (2026 - 2033) | 6.1% |

| Historical Market Growth (2020 - 2025) | 4.5% |

Market Dynamics

Drivers - Regulatory Mandates for Energy Efficiency

Governments around the world are enforcing bans on incandescent and fluorescent lights, which is increasing the demand for solid-state lighting solutions. The European Union phased out most fluorescent lamps by 2023 under RoHS directives, which require a minimum energy class of B. This change is expected to save as much electricity annually as is consumed by Portugal. In the U.S., the Department of Energy (DOE) reported over 87 million LED installations by 2023, driven by energy efficiency mandates that aim to replace outdated lighting systems. Several states, including California, Colorado, Hawaii, Illinois, Maine, Minnesota, Oregon, Rhode Island, Vermont, and Washington, have implemented Clean Lighting Bills that phase out fluorescent lamps, with implementation timelines extending through 2027 and beyond.

These policies are projected to reduce energy consumption by up to 40% in general illumination, which, in turn, is fostering market growth through compliance incentives and utility rebates. An example of regulatory impact is seen in India’s Bureau of Energy Efficiency UJALA scheme, which has saved 5.3 billion kWh annually across 50 million households.

Superior Total Cost of Ownership and Energy Savings

Solid-state lighting provides high efficiency, operates without mercury, and boasts lifespans exceeding 50,000 hours, significantly reducing operational costs. The Department of Energy (DOE) predicts that by 2030, LED technology could save approximately 261 terawatt-hours (TWh) annually, representing a 40% reduction in projected site electricity consumption compared to a scenario without LED use. Energy codes, such as California's Title 24, ASHRAE 90.1 standards, and the International Energy Conservation Code (IECC), increasingly limit the maximum allowed watts per square foot. For instance, California has reduced the Lighting Power Allowance (LPA) from 0.65 to 0.6 watts per square foot, which creates a regulatory requirement to minimize energy use and achieve higher efficiency with solid-state alternatives.

The financial benefits of lower energy consumption, which can be up to 75% compared to fluorescent lighting, make this technology appealing to commercial adopters. By 2023, global urban street lighting achieved 56% LED coverage, according to the International Energy Agency (IEA), further supporting decarbonization efforts. These advantages encourage stakeholders to see positive returns, thereby accelerating both retrofit projects and new installations.

Restraints - High Initial Investment Costs

Despite recent cost reductions, LED fixtures remain 3 to 4 times more expensive than traditional lighting, creating significant barriers for small and medium-sized businesses and budget-constrained municipalities. While the LED market has become somewhat more accessible, the high upfront investment for full conversion often reaches thousands of dollars per facility.

The payback period from energy savings typically ranges from 3 to 7 years, which can deter organizations focused on immediate financial returns. Smaller enterprises and government entities often lack the capital for lighting upgrades, despite recognizing the long-term benefits, limiting demand in cost-sensitive markets and developing regions where purchasing power is considerably lower.

Technical Compatibility Issues with Legacy Infrastructure

Retrofitting existing buildings with solid-state lighting systems often faces technical incompatibilities with legacy electrical infrastructure. This includes older dimming controls, ballasts, and power management systems that were designed for fluorescent and High-Intensity Discharge (HID) lighting technologies. These compatibility issues require additional investments in upgrades to the supporting infrastructure, such as new drivers, control systems, and wiring modifications, which raise project costs.

Furthermore, variations in LED driver standards across the U.S., Europe, and Asia complicate international procurement and installation. Manufacturers must navigate diverse regulatory frameworks, including certifications like UL 8750, IEC 61347-2-13, and CCC.

Opportunity - Integration with Smart Lighting and IoT

IoT-enabled systems facilitate adaptive controls, occupancy sensing, and remote management, which are essential for the development of smart cities. Protocols like Zigbee and Wi-Fi integrate seamlessly with home ecosystems, resulting in energy savings of 30-50%. The combination of solid-state lighting with Internet of Things (IoT) technologies and smart building management systems presents significant growth opportunities for market participants. Leading manufacturers are actively innovating in this space. For example, in January 2024, Philips Lighting announced a new range of smart LED bulbs that feature enhanced connectivity. These bulbs integrate effortlessly with voice-activated assistants and mobile applications, allowing for dynamic lighting control, occupancy sensing, and predictive maintenance capabilities.

The LED and OLED lighting products and displays market is experiencing rapid growth, driven by connected lighting platforms. These platforms enable real-time energy monitoring, adaptive illumination based on natural light availability, and integration with security and HVAC systems, all working together to optimize overall building performance and enhance occupant comfort.

Growing Demand in Healthcare and Medical Lighting Applications

The Automotive Lighting Market is poised for substantial growth, driven by the rise of electric vehicles and the increasing adoption of advanced driver assistance systems. The sector is expected to expand from approximately $38.4 billion in 2025 to around $62.9 billion by 2032. Technologies like OLED and Micro-LED are gaining popularity in premium automotive applications due to their design flexibility, superior visibility, and energy efficiency. Additionally, adaptive driving beam (ADB) and matrix LED systems have seen an impressive increase of 215% between 2020 and 2023 in premium vehicle segments.

Furthermore, specialized applications such as medical imaging displays, surgical lighting systems, and backlighting modules for diagnostic equipment present high-margin opportunities. These applications leverage the need for precise illumination and the premium on regulatory compliance. The medical backlight module market is accelerating, fueled by the rising adoption of portable and handheld diagnostic devices, AI-driven surgical navigation systems, and telemedicine platforms, all of which require high-resolution and stable illumination. This trend is creating multiple adjacent market segments where advanced lighting solutions can command premium pricing, thereby ensuring sustained profitability.

Category-wise Analysis

Technology Insights

Solid-State Lighting (SSL) leads the technology segment, accounting for approximately 72% of total market revenue in 2025 and being the fastest-growing category throughout the forecast period. The prominence of solid-state technology is supported by its exceptional performance advantages, which include a 90% reduction in energy consumption compared to traditional incandescent and fluorescent sources. SSL also boasts operational lifespans of 25,000 to 50,000 hours, in contrast to just 1,000 hours for incandescent bulbs. Furthermore, it requires significantly less maintenance and offers a lower total cost of ownership.

LED technology, in particular, makes up the majority of solid-state lighting installations across residential, commercial, and industrial sectors. This widespread adoption is due to mature manufacturing processes, well-established supply chains, competitive pricing, and a diverse product portfolio that meets various voltage and color temperature needs. OLED and Micro-LED technologies are also rapidly gaining traction in specialized applications such as automotive lighting, architectural displays, and medical imaging. These technologies excel in design flexibility, superior color accuracy, and very high brightness, which justify their premium pricing and encourage ongoing development investments.

Installation Type Insights

Retrofit installation holds approximately 62% of the market share, highlighting the significant number of existing legacy lighting systems that need energy-efficient upgrades. Commercial building retrofits offer compelling returns on investment, with businesses reporting energy cost reductions of 35% to 40% and often recovering their investments within 18 months, as shown in various case studies. LED retrofit solutions consume up to 50% less energy than fluorescent lights and 80% less than incandescent bulbs, resulting in substantial savings on utility bills. Retail chains that adopt retrofit projects with motion sensors and daylight harvesting systems have observed a 35% decrease in energy costs, all while enhancing in-store ambiance.

Furthermore, the retrofit segment benefits from government incentive programs that provide rebates and financing support, especially for municipal facilities, warehouses, and parking structures. In these cases, lighting often constitutes a large part of operational expenses, and LED upgrades lead to immediate sustainability benefits and reduced carbon footprints.

Application Insights

General lighting applications dominate the market, accounting for approximately 64% of total revenue. This is largely due to widespread adoption in residential buildings, offices, educational institutions, and public infrastructure, all of which require consistent and efficient illumination. The versatility of general lighting systems allows them to meet diverse aesthetic, task-specific, and ambient lighting needs. Furthermore, the energy code mandates that progressively reducing maximum power allowances contribute to a sustained demand across various geographic regions and building types.

On the other side, backlighting for displays, automotive lighting for vehicles, advanced signaling systems, and medical lighting for diagnostic and surgical purposes represent high-growth, specialized segments. These areas justify premium pricing due to their demanding performance requirements, which drive innovation in technology. The rapid adoption of automotive lighting, especially in luxury vehicle segments that utilize adaptive driving beams, OLED ambient lighting, and interior display illumination, coupled with investments in the healthcare sector for advanced diagnostic equipment that requires precise illumination, creates numerous high-value market opportunities. This environment supports sustained pricing power and profit margin expansion.

Regional Insights

North America Solid State and Other Energy Efficient Lighting Market Trends

North America is projected to capture approximately 36.3% of the global share by 2025, driven by an advanced regulatory framework, strong government incentives, and early adoption of digital lighting technologies. The U.S. has implemented stringent federal efficiency standards, requiring a minimum of 45 lumens per watt starting in August 2023, with further restrictions on general service lamps set for July 2028. Several states, including California and Colorado, have also enacted legislation to phase out fluorescent and HID lamps by 2027, impacting over one-fifth of the U.S. population.

Furthermore, North America drives the global smart adaptive lighting retrofit market. This growth is driven by high retrofit rates in commercial and municipal sectors and the deployment of IoT-enabled adaptive lighting systems. Government incentives, utility rebates, and tax credits help lower retrofitting costs, while integration with smart city initiatives significantly boosts demand for connected lighting solutions across various properties.

Europe Solid State and Other Energy Efficient Lighting Market Trends

Europe is set to retain a significant market share, particularly due to the strong market presence in France, Germany, and the U.K. The EU's Ecodesign Directive is the most comprehensive regulatory framework globally, phasing out inefficient light sources and promoting the adoption of LED, OLED, and advanced solid-state technologies. Germany leads the European smart lighting retrofit market due to stringent energy regulations, government incentives, and advanced digital infrastructure. Major manufacturers like Osram drive innovation in automotive and general lighting for luxury vehicles and high-performance industrial applications.

Furthermore, Europe is rapidly adopting human-centric lighting systems in healthcare, education, and commercial sectors. This trend is fueled by a focus on occupant well-being and productivity, in line with sustainability goals from the EU Green Deal. Significant investments in smart city infrastructure and sustainable building modernization across the U.K., Germany, France, and other member states create ongoing demand for advanced lighting solutions that integrate digital controls and energy management capabilities.

Asia Pacific Solid State and Other Energy Efficient Lighting Market Trends

The Asia Pacific region is the dominant global market, representing about 45% market share, with rapid growth driven by urbanization, industrialization, and government initiatives in renewable energy and sustainability. China dominates the regional market due to extensive smart city projects and the expansion of residential construction for 449.7 million households. Government procurement programs are also boosting demand for energy-efficient lighting in various sectors.

India shows strong growth potential with a projected CAGR of 9.5%, supported by the USD 30 billion Smart Cities Mission for intelligent street lighting and production-linked incentive programs that lower manufacturing costs for local LED producers. The region benefits from established supply chains, ample semiconductor production, and competitive labor costs, allowing manufacturers to maintain healthy profit margins. Japan and South Korea lead in technological innovations, with Seoul Semiconductor becoming the top backlight LED display maker and companies exploring advanced quantum dot and semiconductor technologies for automotive and medical applications.

Competitive Landscape

The solid-state and energy-efficient lighting market has a moderately consolidated competitive structure with significant competition from both established multinational manufacturers and emerging regional players. Major multinational companies like Philips Signify, Osram Licht AG, General Electric, and Samsung Electronics dominate the market with extensive product portfolios and global distribution. Emerging competitors such as Seoul Semiconductor, Nichia, Toyoda Gosei, and Toshiba are driving innovation in specialized areas like automotive lighting and advanced OLED technologies. As regulations encourage a shift to solid-state lighting, opportunities emerge for manufacturers specializing in niche products tailored to human-centric applications and smart integration. Key differentiation strategies include smart lighting control platforms, enhanced thermal management solutions, specialized optical designs, and strategic acquisitions to consolidate supply chains and expand technology portfolios.

Key Developments:

- January 2025: Wolfspeed Inc. launched its Gen 4 Silicon Carbide MOSFET technology platform, delivering up to 80% fewer power losses for electric vehicles and a 40% reduction in thermal loads for AI data centers, significantly enhancing LED driver efficiency and performance in high-power lighting applications.

- June 2024: OSRAM launched a new generation of high-power LEDs with improved luminous efficacy, supporting sophisticated lighting controls designed to reduce energy consumption across commercial, industrial, and municipal applications while maintaining superior light quality and color rendering performance.

- January 2024: Philips Lighting announced a new range of smart LED bulbs with enhanced connectivity features, integrating seamlessly with voice-activated assistants and mobile applications to enable dynamic lighting control, occupancy sensing, and predictive maintenance capabilities for residential and commercial building automation.

Top Companies in Solid State and Other Energy Efficient Lighting Market

- Philips Lighting Holding (Netherlands) dominates the global market through Signify with an extensive portfolio of energy-efficient LED solutions spanning residential, commercial, and industrial applications. The company leverages expertise in connected lighting systems and smart home integration, competing for multi-year city contracts and delivering innovative lighting-as-a-service business models that reduce customer capital expenditures while ensuring predictable performance and maintenance.

- OSRAM Licht AG (Germany) maintains a significant market share through German engineering excellence and diversified technology platforms encompassing LED, OLED, and advanced lighting controls. The company focuses on professional lighting applications and automotive technologies, expanding into connected lighting and sustainable solutions while securing major municipal retrofit contracts across European metropolitan areas through proven reliability and technical performance.

- Samsung Electronics Co. Ltd. (South Korea) leverages semiconductor manufacturing capabilities and vertical integration to deliver cost-competitive LED components and finished lighting products for large-scale commercial projects. The company unveiled its latest LED lighting technology for commercial applications in September 2024, focusing on smart building integration and energy management systems that optimize operational efficiency while providing superior illumination quality and design flexibility.

Companies Covered in Solid State and Other Energy Efficient Lighting Market

- OSRAM Licht AG

- Royal Phillips Electronics

- Mitsubishi Electric Corporation

- Samsung Electronics Co. Ltd.

- Toshiba Corporation

- Seoul Semiconductor Co. Ltd.

- General Electric Company

- Wolfspeed Inc.

- Energy Focus Inc.

- Sharp Corporation

- Aixtron SE

- Applied Materials, Inc.

- Toyoda Gosei Co., Ltd.

Frequently Asked Questions

The solid state and other energy efficient lighting market is likely to be valued at US$ 190.2 Bn in 2026, reaching US$ 287.9 Bn by 2033 at 6.1% CAGR, driven by stringent government regulations mandating the phase-out of inefficient technologies and accelerating the adoption of energy-efficient solutions across residential, commercial, and industrial sectors worldwide.

The primary demand drivers include stringent government regulations, including the EU's Ecodesign Directive, U.S. Department of Energy efficiency standards, and fluorescent lamp phase-out commitments across 147 countries by 2027.

Solid-State Lighting technology dominates the market, commanding approximately 72% of total market revenue in 2025, driven by unparalleled performance advantages, including 90% energy reduction, operational lifespans of 25,000-50,000 hours, and minimal maintenance requirements.

Asia Pacific represents the largest global market, capturing approximately 45% of revenue, driven by rapid urbanization, industrial expansion, government-backed smart city initiatives across China, India, Japan, and Southeast Asia, supported by established manufacturing ecosystems providing competitive global pricing and exceptional scalability.

Automotive Lighting and Smart Connected Systems represent the most significant market opportunity, driven by electric vehicle proliferation, advanced driver assistance system adoption, OLED and Micro-LED technology integration supporting design innovation, and premium pricing power in luxury vehicle and safety-critical applications.

Royal Phillips Electronics (Signify N.V.), Osram Licht AG, Samsung Electronics Co. Ltd., General Electric Company, Seoul Semiconductor Co. Ltd., and Mitsubishi Electric Corporation represent the leading market players, leveraging extensive product portfolios, global distribution networks, and established customer relationships.