- Technology

- Lighting as a Service Market

Lighting as a Service Market Size, Share and Growth Forecast, 2026 - 2033

Lighting as a Service Market by End-use Industry (Commercial, Industrial, Others), Application (Indoor, Outdoor), Business Model (Subscription-based, Energy Savings Performance Contracts (ESPC), Others), and Regional Analysis for 2026 - 2033

Lighting as a Service Market Share and Trends Analysis

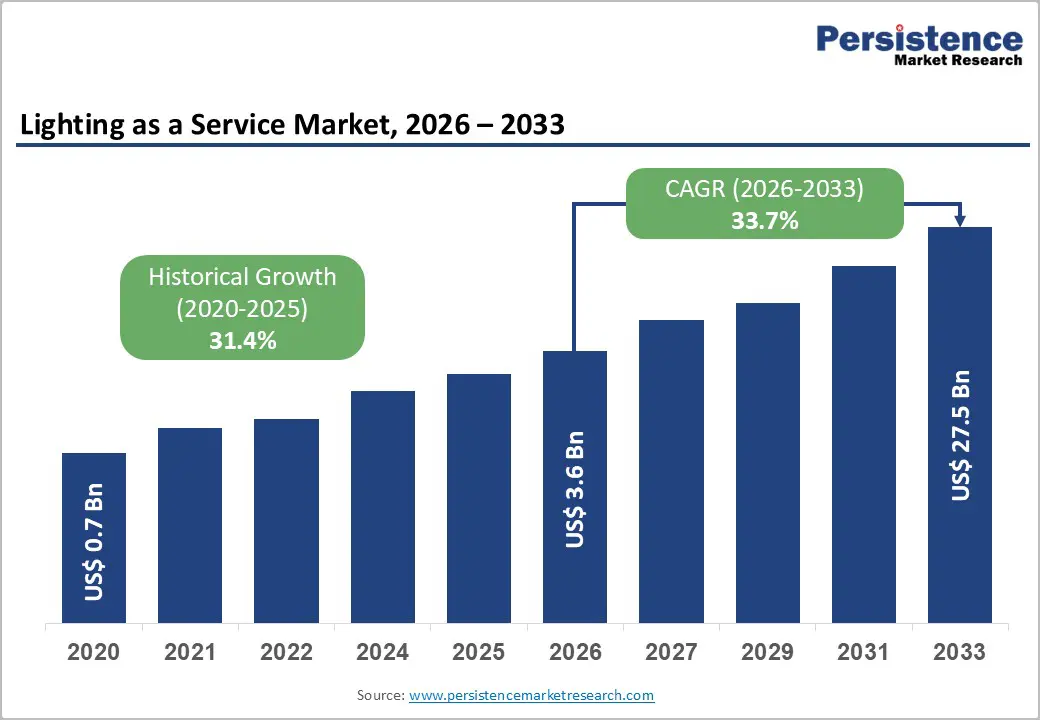

The global lighting as a service market size is likely to be valued at US$3.6 billion in 2026 and is projected to reach US$27.5 billion by 2033, growing at a CAGR of 33.7% during the forecast period 2026–2033, driven by rising demand for energy-efficient lighting solutions, accelerated adoption of smart lighting systems, and increasing emphasis on reducing operational expenditures across commercial and public infrastructure.

Growing regulatory pressure for carbon neutrality, particularly across developed economies, is further accelerating LaaS adoption. Organizations are shifting toward subscription-based infrastructure models to avoid high upfront capital investment while ensuring predictable energy savings and lifecycle management.

Key Industry Highlights:

- End-use Segment Dynamics: The commercial segment is set to command around 42% revenue share in 2026, while the municipal & public segment is likely to grow the fastest, driven by expansion of smart street lighting and rising focus on energy savings and lifecycle management in urban infrastructure.

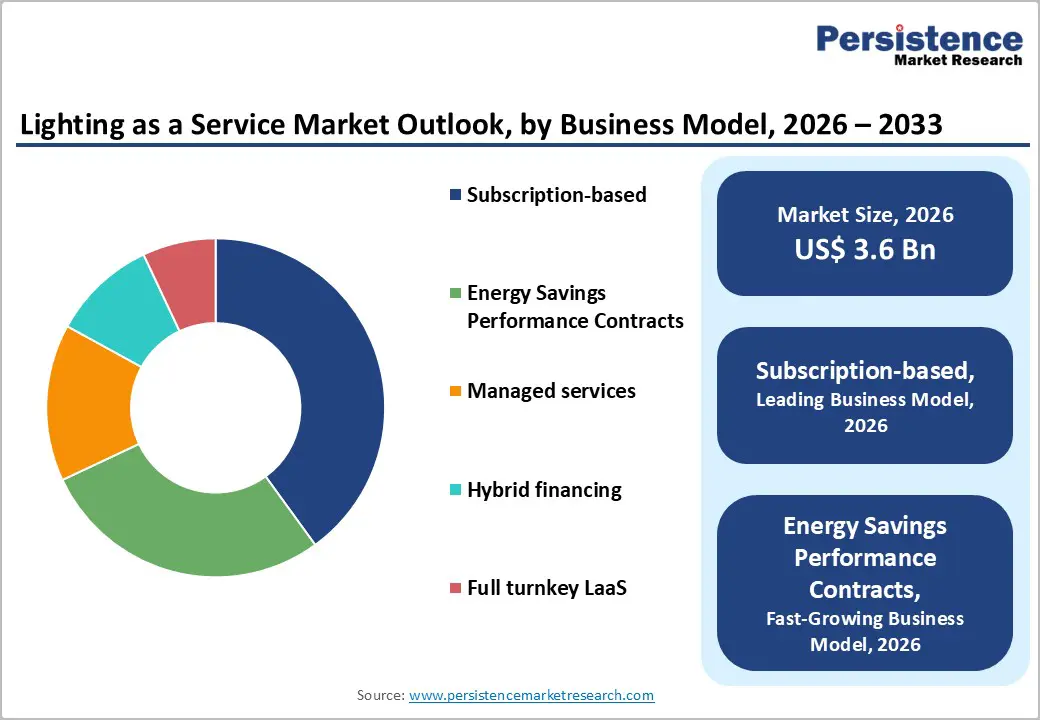

- Dominant Business Model: The subscription-based LaaS model is set to command around 40% revenue share in 2026, while Energy Savings Performance Contracts (ESPC) are likely to grow the fastest, supported by performance-linked payments and increasing adoption in public-sector efficiency programs.

- Application Dynamics: The indoor application segment is set to lead with around 58% market share in 2026, driven by deployment of smart lighting systems for energy optimization and productivity gains, while the outdoor application segment is likely to grow the fastest due to rising smart city and infrastructure lighting projects.

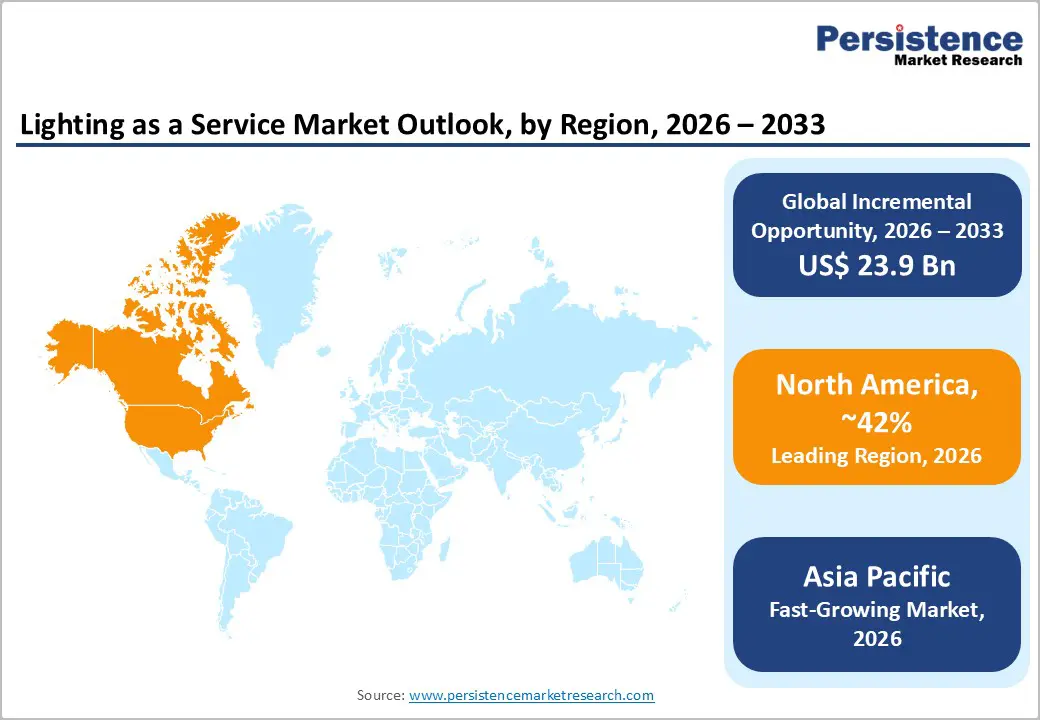

- Regional Leadership: North America is set to command around 42% market share in 2025, driven by strong adoption of smart building systems, while Asia-Pacific is likely to grow the fastest through 2033, supported by rapid urbanization and large-scale smart city investments across China, India, and Japan.

- Competitive Environment: The top players are set to collectively hold around 50% market share in 2026, while competition is intensifying through investments in IoT-enabled smart lighting ecosystems, cloud-based energy platforms, and long-term service expansion strategies.

DRO Analysis

Drivers - Rapid Transition toward Energy Efficiency and ESG Compliance

One of the strongest drivers of the Lighting as a Service Market is the global transition toward energy efficiency and ESG-driven infrastructure modernization. According to the International Energy Agency (IEA), lighting accounts for nearly 15–19% of global electricity consumption in commercial buildings. Governments in the EU, U.S. Department of Energy (DOE), and India’s Bureau of Energy Efficiency (BEE) are enforcing stricter efficiency standards and phasing out inefficient lighting systems such as halogen and fluorescent lamps.

This regulatory momentum is pushing enterprises toward LED-based smart lighting systems delivered via LaaS models, which reduce energy consumption by up to 50–70%. The shift is particularly strong in municipal and industrial sectors, where sustainability targets are tied to funding eligibility and compliance mandates. As a result, LaaS adoption is becoming a strategic lever for both cost reduction and carbon footprint optimization.

Restraints - High Dependency on Long-Term Contractual Commitments

A key restraint in the lighting as a service market is the reliance on long-term service contracts, typically ranging from 7–15 years. Many small and mid-sized enterprises hesitate to adopt LaaS due to concerns over contractual rigidity, vendor lock-in, and uncertain long-term savings realization. Additionally, the lack of standardized contractual frameworks across regions creates legal and financial complexity.

In developing economies, limited credit availability and inconsistent energy pricing structures further slow adoption. While LaaS reduces upfront capital expenditure, the perceived risk of long-term dependency on service providers remains a critical barrier, affecting nearly 25–30% of potential SME adoption pipelines globally.

Opportunity - Expansion of Smart City Infrastructure and Digital Lighting Ecosystems

The market is witnessing strong momentum driven by the rapid global expansion of smart city infrastructure and the increasing integration of digital lighting ecosystems. Governments are prioritizing intelligent urban transformation, with smart city investments projected to exceed US$1 trillion by the early 2030s, accelerating deployment of IoT-enabled street lighting, adaptive control systems, and centralized energy platforms. This shift is evident in large-scale initiatives such as India’s Smart Cities Mission and China’s urban modernization programs, where LaaS models are being adopted to enhance efficiency, reduce energy consumption, and improve lifecycle management of public infrastructure.

Within this landscape, the municipal & public lighting segment leads adoption with an estimated 38% share, driven by sustained government-led modernization and public-private partnerships, while smart street lighting systems represent the fastest-growing subsegment through 2033, fueled by smart highway corridors and city-wide retrofitting programs across developed and emerging economies.

A new high-value opportunity is emerging in indoor aesthetic and experiential lighting, where commercial spaces such as retail, hospitality, and premium offices are increasingly investing in design-driven smart lighting solutions to enhance ambience, customer engagement, and brand identity, significantly expanding LaaS penetration beyond utility-focused applications.

Category-wise Analysis

End-use Industry Insights

The commercial segment is estimated to lead with 42% share in 2026, driven by strong adoption of smart lighting systems across offices, retail, and corporate campuses to improve operational efficiency and reduce energy intensity. This is likely supported by ongoing corporate net-zero retrofit initiatives in large commercial real estate portfolios across North America and Europe, where lighting modernization is expected to remain a core decarbonization lever.

In contrast, the municipal & public segment is projected to be the fastest-growing at approximately 35%+ CAGR through 2033, supported by smart city programs and urban infrastructure modernization. This growth is likely to be reinforced by EU-aligned municipal lighting upgrade programs across European cities, where governments are expected to continue replacing conventional street lighting with IoT-enabled adaptive systems. The resulting impact is expected to improve public safety, reduce energy consumption, and enhance centralized urban lighting control efficiency.

Application Insights

The market is expected to be shaped by increasing demand for intelligent, experience-driven lighting environments. The indoor application segment is projected to dominate with 58% share in 2026, driven by widespread adoption across offices, healthcare, retail, and institutional buildings. This trend is likely supported by continued large-scale commercial building retrofit programs in global business districts and premium retail environments, where smart indoor lighting is being deployed to enhance productivity, user experience, and energy optimization.

The outdoor application segment is expected to be the fastest-growing through 2033, driven by smart infrastructure expansion and transport corridor modernization. Growth is likely supported by the planned deployment of adaptive street lighting systems across major Asian urban transit networks, where sensor-based lighting is being integrated to adjust brightness dynamically based on traffic and environmental conditions. This is expected to improve energy efficiency, reduce operational costs, and enable predictive maintenance of public infrastructure assets.

Business Model Insights

The subscription-based model is projected to lead with 40% share in 2026, driven by predictable payment structures, bundled maintenance, and elimination of upfront capital expenditure. Adoption is likely to remain strong across multi-site commercial portfolios, where enterprises are increasingly standardizing energy savings and lifecycle management frameworks to improve operational predictability.

Energy Savings Performance Contracts (ESPC) are expected to be the fastest-growing model at approximately 34% CAGR through 2033, driven by increasing preference for performance-linked financing structures. The growth is likely supported by municipal and institutional lighting retrofit programs in developed markets, where payments are tied to verified energy savings outcomes. This model is expected to enable large-scale infrastructure upgrades while reducing upfront fiscal pressure on public sector budgets.

Regional Analysis

North America Lighting as a Service Market Trends

North America is estimated to account for around 42% of the global lighting as a service market in 2026, supported by the deep penetration of smart building systems, strong efficiency regulations, and widespread deployment of connected lighting infrastructure across commercial and public assets. The region is steadily moving toward fully integrated building ecosystems, where lighting functions as part of broader digital energy and facility management networks. Increasing use of AI-led analytics and predictive maintenance is further improving operational efficiency across large property portfolios.

U.S. Lighting as a Service Market Trends

The U.S., estimated at 42% of the regional market in 2026, is expected to remain the primary demand center, supported by large-scale deployment of connected lighting across airports, healthcare networks, and corporate campuses. A notable trend is the modernization of major transport and logistics hubs with intelligent lighting systems designed to enhance visibility, reduce energy use, and improve asset monitoring in real time.

Canada Lighting as a Service Market Trends

Canada, estimated at 18% of the North American share by 2026, is steadily scaling adoption, backed by sustainability-led building policies and infrastructure modernization initiatives. Municipal upgrades are increasingly shifting toward subscription-based lighting models in transit corridors and public facilities, helping reduce upfront investment while improving long-term energy performance and maintenance efficiency.

Europe Lighting as a Service Market Trends

Europe is estimated to represent around 30–32% of the global market in 2026, driven by aggressive decarbonization targets, smart city expansion, and tightly aligned regulatory frameworks across member states. The region is increasingly replacing conventional lighting infrastructure with service-based, digitally connected systems aimed at long-term emissions reduction. Municipal modernization and commercial building retrofits remain the core demand drivers.

Germany Lighting as a Service Market Trends

Germany, estimated at 26% of the European market, continues to lead adoption, supported by industrial modernization and energy transition programs. Industrial zones and logistics corridors are increasingly deploying automated lighting systems with real-time energy monitoring, improving efficiency in high-load operational environments while reducing wastage.

U.K. Lighting as a Service Market Trends

The U.K. estimated at 17% of the regional share, is expanding adoption across urban redevelopment zones and commercial districts. Smart lighting is increasingly being integrated into city regeneration projects, where adaptive systems are improving energy efficiency while lowering long-term maintenance requirements for both public and private infrastructure.

Asia Pacific Lighting as a Service Market Trends

Asia Pacific is estimated to be the fastest-growing region, accounting for around 24% of the global lighting as a service market in 2026, driven by rapid urban expansion, infrastructure buildout, and accelerating smart city programs. The region is undergoing a structural shift toward connected urban ecosystems, where lighting is increasingly integrated with mobility systems, IoT networks, and centralized energy platforms. Cost-efficient deployment models and public-private partnerships are further accelerating adoption.

China Lighting as a Service Market Trends

China, estimated at 39% of the Asia Pacific market in 2026, remains the largest contributor, driven by large-scale smart infrastructure programs and continuous urban modernization. Cities are increasingly deploying AI-enabled adaptive lighting systems across commercial districts and industrial zones, improving energy control, operational visibility, and maintenance efficiency through centralized digital platforms.

India Lighting as a Service Market Trends

India, estimated at 22% of the regional share in 2026, is emerging as a high-growth market supported by rapid urbanization and infrastructure expansion. The adoption is increasing across urban development corridors and smart infrastructure zones, where municipalities are gradually shifting toward service-based lighting models to reduce capital pressure while improving energy efficiency and lifecycle performance.

Competitive Landscape

The global lighting as a service market is moderately consolidated, with leading players such as Signify, Siemens, Schneider Electric, Johnson Controls, and Eaton collectively accounting for a significant share of global revenues. These companies dominate through integrated smart lighting ecosystems and energy management platforms, combining hardware, software, and financing models. Their competitive strength is increasingly defined by the ability to deliver measurable energy savings and lifecycle efficiency outcomes under long-term service contracts.

Regional and niche players such as Acuity Brands, Zumtobel Group, and LEDVANCE are strengthening their positions through targeted offerings in commercial and municipal segments. Entry barriers remain high due to long contract cycles, system integration complexity, and performance-based delivery requirements. However, rising adoption of cloud-based lighting control and IoT-enabled platforms is enabling new collaboration models. The market is expected to gradually consolidate through acquisitions and strategic partnerships focused on expanding digital capabilities.

Key Industry Developments:

- In July 2025, Schneider Electric strengthened its digital energy and smart infrastructure leadership by acquiring the remaining 35% stake in SEIPL for €5.5 billion, gaining full ownership of its India operations. The move is expected to accelerate its IoT-enabled smart building and lighting ecosystem strategy, reinforcing India as a global hub for connected energy and automation solutions aligned with national digitalization programs.

- In January 2025, Acuity Brands expanded its Intelligent Spaces portfolio through the acquisition of QSC for approximately US$1.2 billion, enhancing its cloud-first building control ecosystem. The integration is expected to strengthen its data-driven smart building and lighting solutions, combining audio-visual, control, and spatial intelligence systems to enable more integrated, energy-efficient environments.

Companies Covered in Lighting as a Service Market

- Signify

- Siemens

- Schneider Electric

- Eaton

- Johnson Controls

- Honeywell International

- General Electric

- Acuity Brands

- Zumtobel Group

- Cree Lighting

- Osram Licht AG

- Hubbell Incorporated

- Lutron Electronics

- Virtual Extension

- ENGIE Solutions

Frequently Asked Questions

The global lighting as a service market is projected to reach US$3.6 billion in 2026.

The lighting as a service market grows due to rising demand for energy-efficient lighting solutions, ESG compliance, and cost-effective smart infrastructure upgrades.

The lighting as a service market is expected to grow at a 33.7% CAGR from 2026 to 2033.

Key opportunities include expansion of smart city infrastructure, IoT-enabled lighting systems, and subscription-based energy efficiency models.

Key players include Signify, Siemens, Schneider Electric, Johnson Controls, and Eaton.