- Display Technologies

- Light Field Technology Market

Light Field Technology Market Size, Share, and Growth Forecast, 2025 - 2032

Light Field Technology Market By Component (Hardware, Software, Services), Application (Media, Entertainment, Content Creation, Others), and Regional Analysis for 2025 - 2032

Light Field Technology Market Size and Trends Analysis

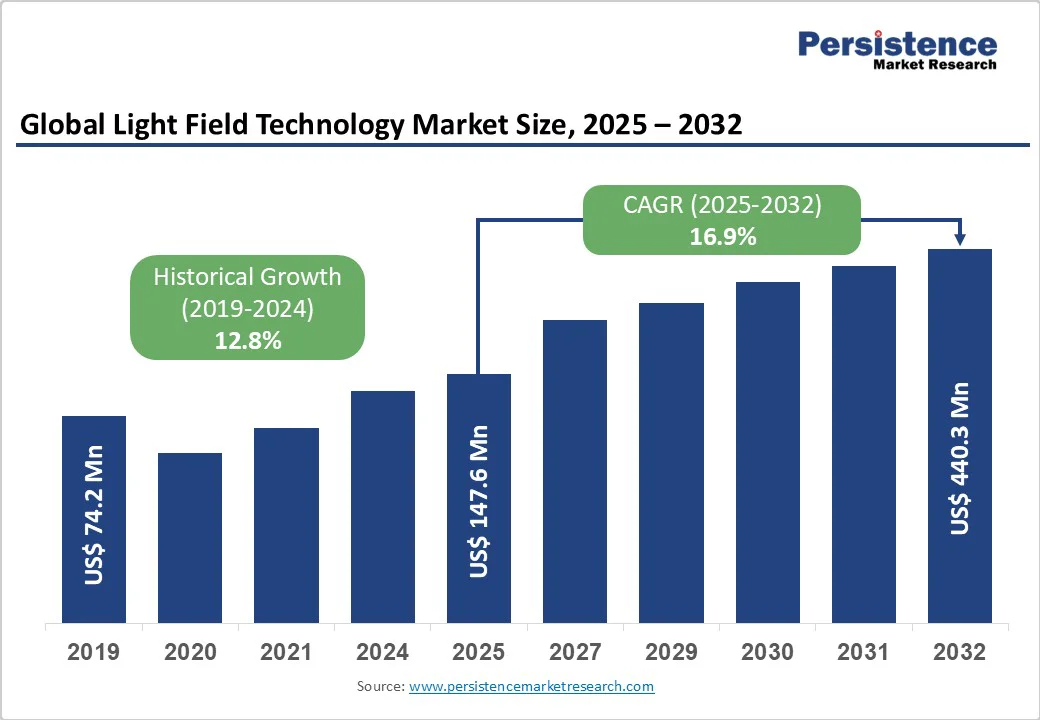

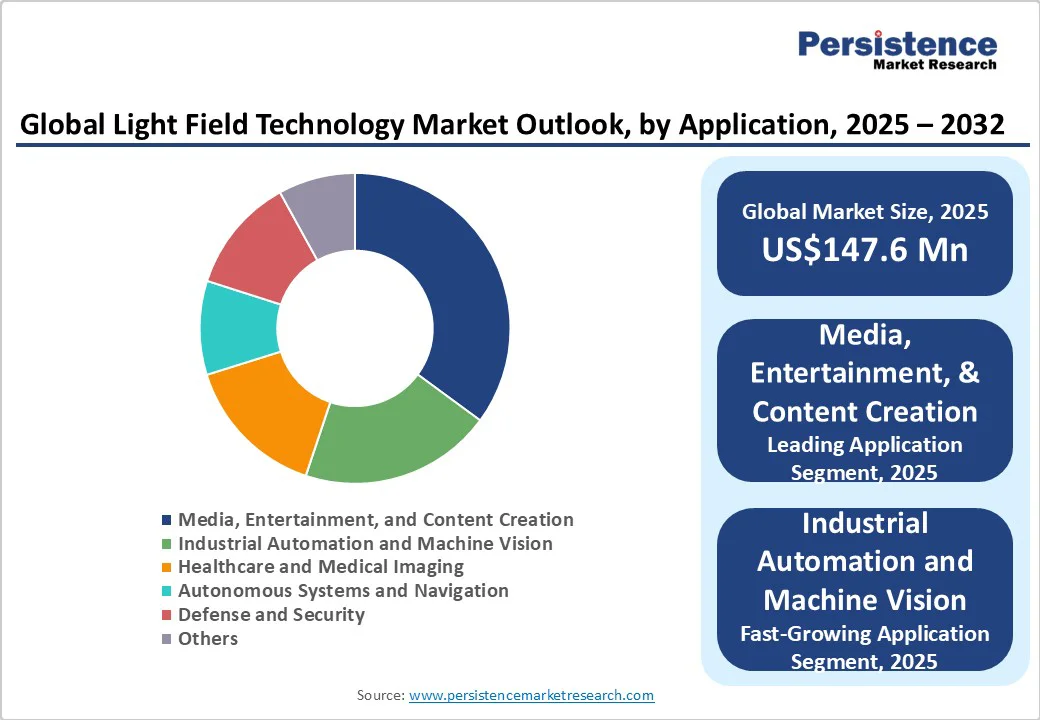

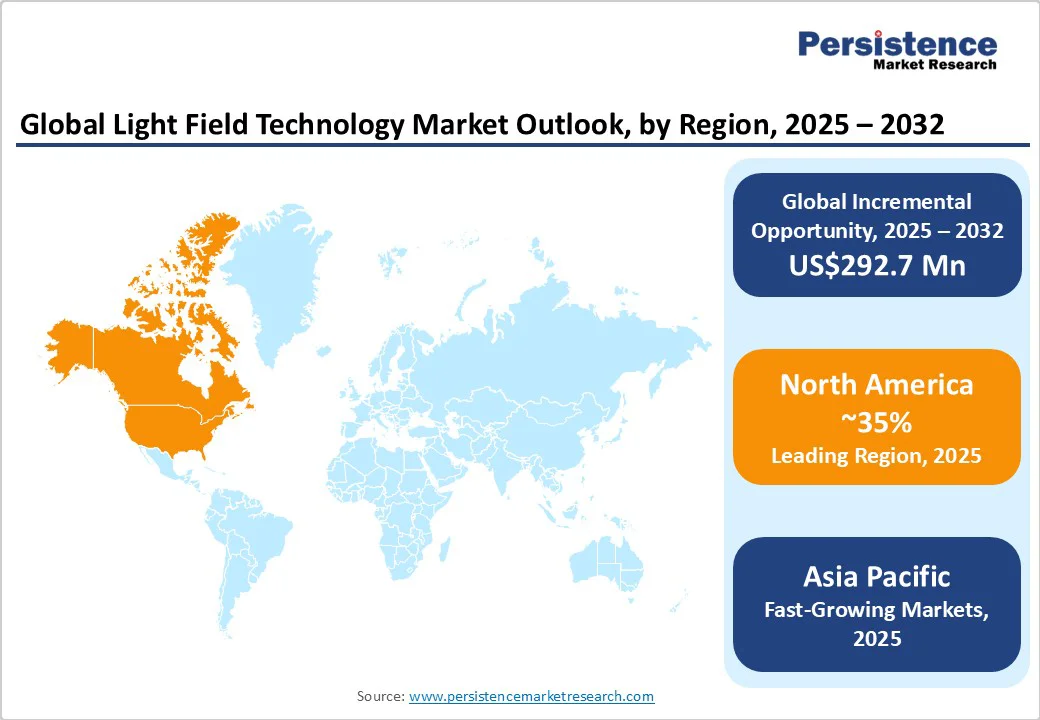

The global light field technology market size is likely to be valued at US$147.6 Mn in 2025. It is expected to reach US$440.3 Mn by 2032, growing at a CAGR of 16.9% during the forecast period from 2025 to 2032, driven by demand for precise spatial visualization, while the entertainment sector drives demand for more engaging, lifelike content. A shift toward miniaturized, cost-effective solutions is making these technologies more accessible. As they evolve, they are set to transform user experiences and improve operational efficiencies across multiple domains.

Key Industry Highlights:

- Leading Component: Hardware is projected to dominate with an over 62.7% share in 2025, due to its role in capturing multi-dimensional light data and enabling immersive experiences. Meanwhile, software adoption is growing for real-time rendering, AI-driven enhancements, and system integration.

- Leading Application: The media, entertainment, and content creation segment is anticipated to account for a 35.1% share in 2025, driven by demand for holographic visuals, virtual sets, volumetric video, AR/VR, gaming, and virtual production.

- Leading Region: North America is likely to hold over 34.6% share in 2025, driven by defense modernization, the growth of autonomous vehicles, and the integration of miniaturized, high-performance imaging technologies.

- Fastest growing Region: Asia Pacific is the fastest-growing market, driven by the rapid adoption of advanced imaging in consumer electronics & government initiatives supporting tech innovation.

- Key Opportunity: AI-driven healthcare imaging and integration with autonomous systems enable precise diagnostics, real-time visualization, and high-accuracy navigation in vehicles, drones, and delivery robots.

| Key Insights | Details |

|---|---|

|

Light Field Technology Market Size (2025E) |

US$147.6 Mn |

|

Market Value Forecast (2032F) |

US$440.3 Mn |

|

Projected Growth (CAGR 2025 to 2032) |

16.9% |

|

Historical Market Growth (CAGR 2019 to 2024) |

12.8% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Advancements in Hardware Miniaturization and Processing Power to Spur Growth

Progress in semiconductors and computational imaging is accelerating the adoption of light field technology. Global semiconductor sales reached US$630.5 Bn in 2024 (SIA), enabling compact, high-performance chips for advanced imaging. Miniaturized light field cameras are being embedded into smartphones, AR/VR headsets, and drones, while edge computing reduces latency for real-time rendering. With the Consumer Technology Association projecting U.S. consumer tech retail revenues at US$512 Bn in 2024, hardware integration is shifting light field systems from niche enterprise tools to scalable consumer applications, supported by economies of scale.

Regulatory Push for Defense and Security Modernization to Accelerate Technology Adoption

Defense agencies are heavily investing in next-generation imaging and navigation systems, with the European Defence Agency (EDA, 2024) reporting a 20% rise in defense R&D funding. It enhances real-time 3D situational awareness, supporting soldiers and autonomous systems in faster battlefield decision-making. Its depth-sensing capabilities also enhance navigation accuracy in GPS-denied environments, which is crucial for defense and aerospace missions.

Regulatory mandates for interoperability, standardization, and advanced AR/VR-based command systems are accelerating adoption, compelling defense contractors to integrate light field technology into modernization programs.

Data Processing Complexity and Latency Issues Hinder Market Growth

Capturing and rendering light field images is highly computationally intensive, with IEEE (2024) reporting that rendering times can be up to four times longer than those of conventional 3D imaging, thereby limiting their use in real-time automation and navigation applications. The massive multidimensional datasets generate significant storage, bandwidth, and transmission burdens, slowing adoption across industries.

Latency in rendering degrades user experience in immersive applications such as AR/VR. These challenges, coupled with high infrastructure costs, make large-scale deployment technologically demanding and prohibitive for industries with limited IT capabilities.

Supply Chain Disruptions and Component Shortages to Act as a Restraint

The production of light field cameras and sensors depends on high-precision optics, specialized semiconductors, and advanced computational modules sourced from a limited global supplier base. Ongoing semiconductor shortages, which pushed global chip lead times beyond 20 weeks in 2024, have particularly constrained access to high-performance processors required for real-time light field imaging.

Geopolitical tensions and trade restrictions further disrupt logistics, compounding procurement delays and raising costs. These supply chain vulnerabilities hinder large-scale production, delay deployments in defense, healthcare, and AR/VR, and make it difficult for companies to balance product quality, demand fulfillment, and competitive pricing, restraining market growth.

AI-Driven Light Field Imaging Unlocks New Opportunities in Precision Diagnostics

Light field imaging, when combined with AI, enables higher accuracy in diagnostics, real-time visualization, anomaly detection, and personalized treatment planning across various medical specialties, including radiology, ophthalmology, oncology, and surgery. AI enhances image reconstruction by reducing noise and improving resolution, making light field data clinically viable. Adoption is accelerating, supported by regulatory momentum such as the U.S. FDA expanding pathways for AI-driven imaging.

According to the Medscape & HIMSS AI Adoption Report 2024, 86% of health systems already use AI, with 60% believing it can detect patterns beyond human capability, underscoring commercialization opportunities for next-gen diagnostic platforms.

Integration with Autonomous Systems and Smart Mobility Fuels Technology Adoption

Convergence with autonomous systems and smart mobility is driving the adoption of light field technology by enabling high-accuracy 3D perception for obstacle detection and navigation in vehicles, drones, and delivery robots. Light field-based AR/VR interfaces enhance driver assistance, infotainment, and immersive navigation, while AI integration accelerates object recognition and situational awareness in complex traffic.

This technology also supports vehicle-to-infrastructure (V2I) communication through detailed spatial mapping, aligning with the goals of smart city mobility. For instance, a study by the U.K. government projects that 40% of new cars could have automated driving capabilities by 2035, underscoring strong market potential.

Category-wise Analysis

Component Insights

Based on component, the market is divided into hardware, software, and services. Among these, hardware is expected to account for more than 62.7% share in 2025 due to its critical role in capturing and rendering multi-dimensional light data. Users demand accurate depth perception, realistic spatial representation, and smooth real-time interaction, which can only be achieved through advanced hardware. The growing need for immersive and multi-dimensional experiences further drives investment in robust hardware solutions.

Software is expected to grow at a significant rate due to the increasing demand for advanced computational tools that efficiently process and render complex 3D light field data. Industries require precise depth mapping, real-time rendering, and AI-driven enhancements, which rely heavily on specialized software solutions. The need for seamless integration with autonomous systems, cloud computing, and analytics platforms is driving rapid adoption of light field software.

Application Insights

In terms of application, the market is segmented into media, entertainment, and content creation; industrial automation and machine vision; healthcare and medical imaging; autonomous systems and navigation; defense and security; and others. Media, entertainment, and content creation are expected to account for more than 35.1% share in 2025, due to growing demand for immersive and interactive 3D experiences.

Studios and creators require light field displays to produce holographic visuals, virtual sets, and volumetric video content without the need for headsets. This technology meets the industry’s need for realistic depth, multi-angle viewing, and high-fidelity rendering, enabling more engaging storytelling and innovative content formats. The rise of AR/VR, gaming, and virtual production drives further adoption in this sector.

Industrial automation and machine vision are expected to grow at the fastest rate due to the increasing demand for precise, high-speed inspection and quality control in manufacturing. It enables 3D depth perception, accurate defect detection, and dimensional measurements without contact, addressing the need for faster, error-free production. The rising adoption of smart factories and Industry 4.0 initiatives is prompting manufacturers to implement advanced vision systems that enhance efficiency, minimize waste, and ensure product consistency.

Regional Insights

North America Light Field Technology Market Trends

North America is expected to account for a share of more than 34.6% in 2025, driven by defense modernization, rapid adoption of autonomous vehicles and drones, and investments in biomedical imaging and government-backed research in advanced optics. Educational institutions in the U.S. and Canada are leveraging light field displays for immersive learning, such as medical schools simulating surgeries.

The gaming and esports sector is expanding, with companies utilizing light field technology for interactive 3D graphics and lifelike environments, supported by strong consumer demand, as evidenced by Pennsylvania’s gaming revenue reaching $6.14 billion in 2024, a 7.72% increase from 2023. Healthcare applications also benefit from high-resolution volumetric imaging for diagnostic purposes and surgical planning.

Asia Pacific Light Field Technology Market Trends

The Asia Pacific is the fastest-growing market, driven by the expansion of digital infrastructure in China, India, Japan, and ASEAN countries, alongside rapid urbanization and growth in digital entertainment and industrial automation. China leads in hardware manufacturing, particularly in AR/VR devices. At the same time, Japan focuses on healthcare imaging, supported by its 2024 Vision for the Medical Device Industry and AI guidelines that encourage the adoption of medical-grade 3D imaging.

India’s Digital India initiative boosts content creation and technology adoption. Favorable cost structures, high consumer electronics penetration, and policy support, such as China’s MIIT reporting 2024 digital industry revenue of ≈35 Tn yuan (US$4.9 Tn) (+3.5% YoY) and 2025 emphasis on embodied AI and sensing technologies, strengthen APAC’s competitive edge in advanced imaging and perception systems.

Europe Light Field Technology Market Trends

Europe’s push through the EU Digital Strategy and multi-year R&D programmes (Horizon, GenAI4EU, Digital Europe) is driving demand for advanced imaging, computational sensing, and trustworthy AI, with funding windows for imaging/AI integration in 2024–2025. In Germany, demand is fueled by the automotive and industrial sectors, with ~2.8 million new passenger car registrations in 2024, according to the Federal Motor Transport Authority, and national high-tech programs supporting sensor and quantum/microelectronics R&D.

France’s rising defense budgets for 2024–2025 are modernizing surveillance, autonomous systems, and battlefield situational awareness, creating strong public-sector demand for volumetric and depth-rich imaging, with spillover into civil sectors such as security, robotics, and inspection.

Competitive Landscape

The global light field technology market is fragmented, with numerous manufacturers competing on innovation, performance, and application-specific solutions. Companies are focusing on product differentiation by developing high-resolution, low-latency light field cameras and imaging systems tailored for automotive, healthcare, and gaming sectors. Forming partnerships and collaborations with AI and AR/VR technology providers helps enhance end-to-end solutions.

Key Industry Developments

- In April 2025, Looking Glass introduced a 27-inch immersive light-field display, enabling 3D visuals without headsets and allowing multiple users to share the experience. This new model sits between the company’s previous 16- and 32-inch professional displays and complements its larger 65-inch version.

- In March 2025, ZEISS launched Lightfield 4D, a new microscopy technology integrated into the LSM 910 and LSM 990 systems, enabling high-speed volumetric imaging of living organisms. The technology overcame limitations of traditional Z-stack imaging by capturing entire 3D datasets instantly, enhancing spatiotemporal accuracy for research in neuroscience, cancer, developmental biology, & plant sciences.

- In March 2024, Scientists at the Tokyo Institute of Technology introduced an innovative mixed light field technique, combining ray-controlled ambient lighting with projection mapping (PM). This innovative technology utilized a novel kaleidoscope array to achieve ray-controlled lighting and a binary search algorithm for removing ambient lighting from PM targets.

Companies Covered in Light Field Technology Market

- Japan Display, Inc.

- Toshiba Corporation

- Wooptix S.L.

- Quidient

- Sony Corporation

- Raytrix GmbH

- K-Lens GmbH

- Fathom Optics Inc.

- Avegant Corp.

- CREAL SA

Frequently Asked Questions

The light field technology market is projected to be valued at US$147.6 Mn in 2025.

The growing need for immersive 3D experiences, realistic depth perception, and multi-angle viewing is a key driver of the light field technology market.

The light field technology market is poised to witness a CAGR of 16.9% from 2025 to 2032.

Continuous advancements in computational imaging and AI-driven rendering are enabling more cost-effective and high-quality solutions, creating strong growth opportunities.

Japan Display, Inc., Toshiba Corporation, Wooptix S.L., Quidient, Sony Corporation, and Raytrix GmbH are among the leading key players.