- Automotive Components & Materials

- Bicycle Light Market

Bicycle Light Market Size, Share, and Growth Forecast, 2026-2033

Bicycle Light Market by Product Type (Front Lights, Rear Lights, Helmet Lights, Others), Technology (LED, Halogen, Rechargeable, Motion Sensors, Others), Sales Channel (Online, Offline, Others), and Regional Analysis for 2026-2033

Bicycle Light Market Share and Trends Analysis

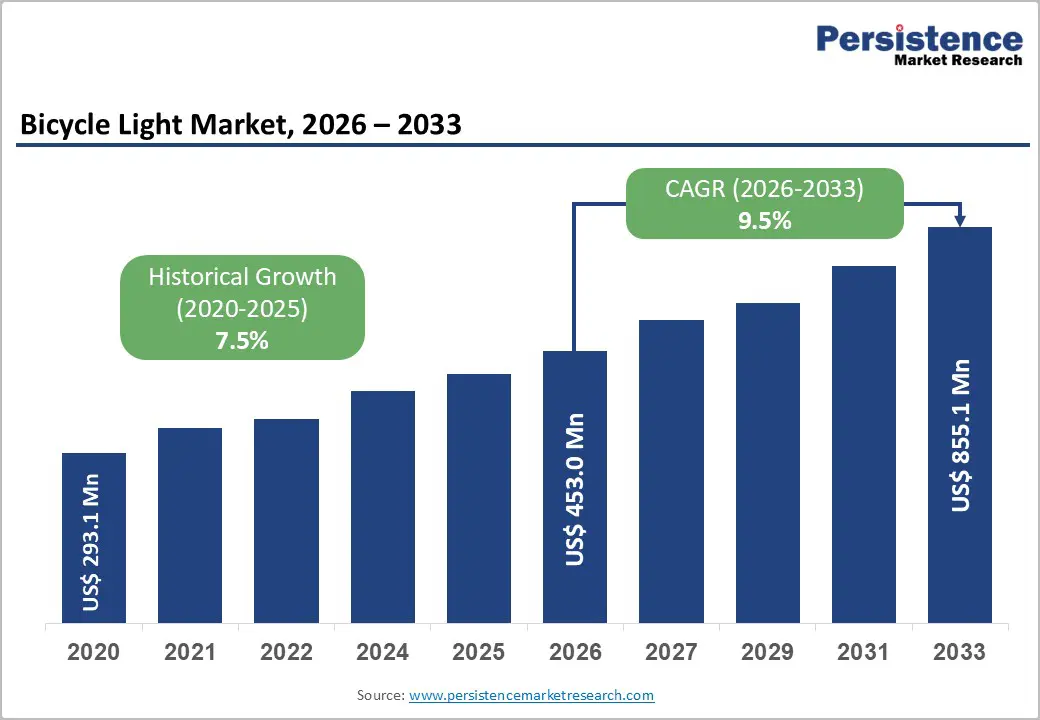

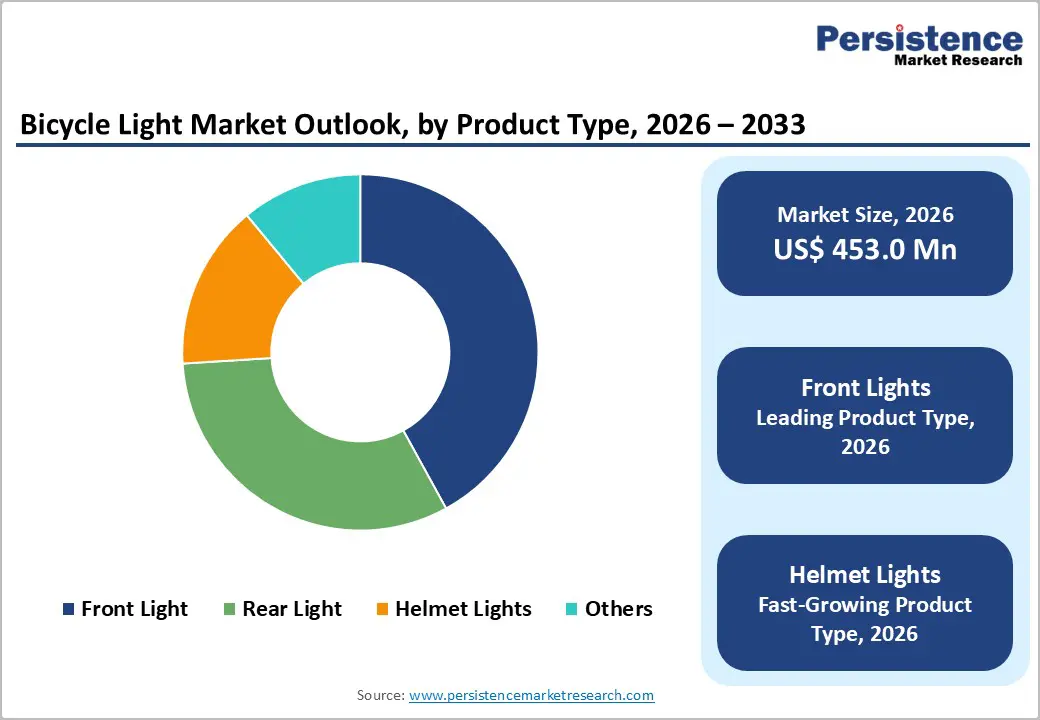

The global bicycle light market size is likely to be valued at US$ 453.0 million in 2026, and is projected to reach US$ 855.1 million by 2033, growing at a CAGR of 9.5% during the forecast period 2026–2033.

Widening cyclist safety awareness, particularly in densely populated cities where shared road use is intensifying, is primarily driving market growth. Governments are investing in dedicated cycling lanes and smart transport corridors, which is encouraging higher bicycle adoption. Regulatory mandates requiring functional front and rear lighting systems also reinforce baseline demand across commuter and recreational segments. Technological advancement is further strengthening product appeal. Manufacturers are introducing light-emitting diode (LED) systems with higher luminosity, improved battery efficiency, and multiple illumination modes to enhance visibility under varied riding conditions. The integration of rechargeable lithium-ion batteries, water-resistant casings, and sensor-based auto-activation features supports product differentiation. Expanding e-commerce platforms are improving market access and enabling direct-to-consumer distribution models.

Key Industry Highlights

- Dominant Product Types: Front lights are projected to lead with approximately 42% revenue share in 2026, while helmet lights are expected to be the fastest-growing at a CAGR of around 11.3% through 2033, driven by high urban cycling adoption.

- Leading Technologies: LED bicycle lights are anticipated to capture over 70% revenue share in 2026, while smart-integrated lights are forecasted to post a CAGR of about 12.1% during 2026–2033, reflecting rising demand for connected cycling solutions.

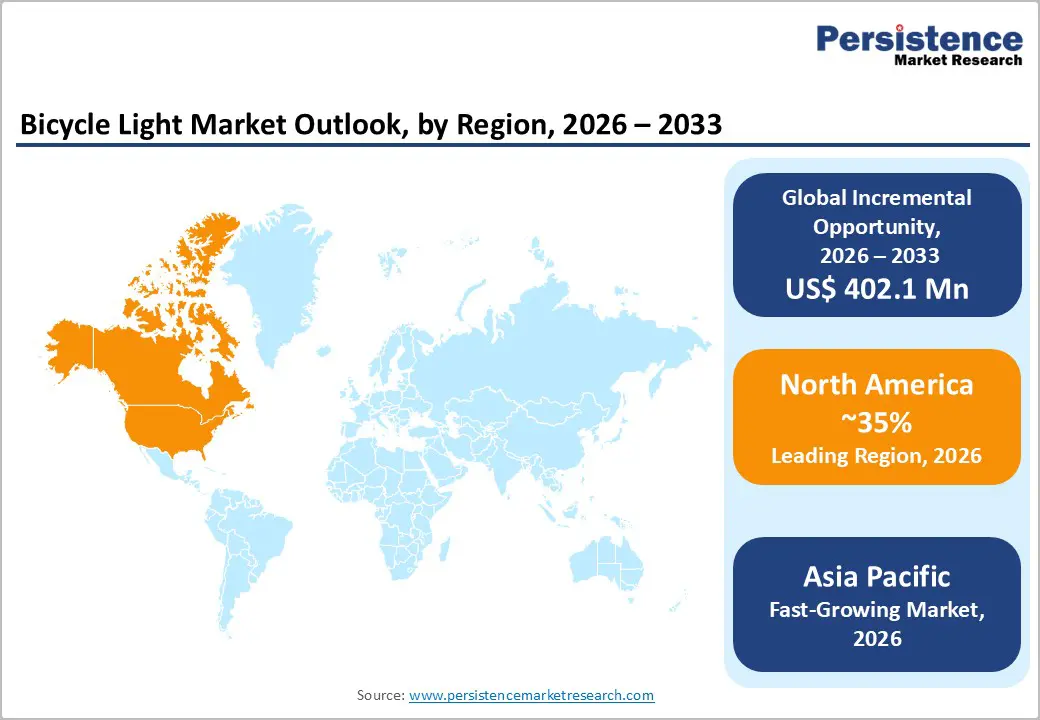

- Regional Leadership: North America is poised to lead the market, with an estimated 35% share in 2026, while Asia Pacific is projected to deliver a 10.5% CAGR over 2026-2033, driven by urban cycling infrastructure expansion.

- Competitive Environment: Market competition is defined by technological innovation, regional expansion, and strategic collaborations, including smart lighting development, and partnerships targeting emerging markets in Asia Pacific and Latin America.

- December 2025: Rivian unveiled an e-bike accessory ecosystem that includes a helmet with integrated brake-light technology, enhancing rider safety by improving visibility and signaling to other road users.

| Key Insights | Details |

|---|---|

| Bicycle Light Market Size (2026E) | US$ 453.0 Bn |

| Market Value Forecast (2033F) | US$ 855.1 Bn |

| Projected Growth (CAGR 2026 to 2033) | 9.5% |

| Historical Market Growth (CAGR 2020 to 2025) | 7.5% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Rising Safety Awareness & Regulatory Compliance

Increasing road accident rates involving cyclists, especially in urban and mixed-traffic environments, are driving demand for high-visibility bicycle lighting systems. Governments in Europe and North America have intensified enforcement of night-riding regulations, directly boosting sales of front, rear, and helmet lights. In the Netherlands, enforcement authorities issued 55% more fines to cyclists riding without lights between May and August 2025, signaling stronger compliance pressure. Such enforcement activities reinforce regulatory expectations and elevate rider safety behaviors. These measures are also influencing manufacturers to prioritize compliance-ready designs that meet evolving safety standards.

Consumer preference for safety accessories has grown alongside cycling for commuting, recreation, and fitness. California’s updated mandate now requires rear reflectors or lights to be visible at all times, not just in darkness, effectively widening the use case for reliable lighting systems. Heightened public awareness campaigns and stricter enforcement of visibility standards have become quantifiable contributors to volume growth, aligning regulatory action with increased consumer safety investment and solidifying structural demand for bicycle lights. The combined effect of legislation and awareness initiatives ensures sustained adoption among urban and suburban cyclists.

Technological Innovation in Lighting Systems

LED and smart lighting technologies continue to transform the bicycle light market by improving brightness, energy efficiency, and usability. LEDs offer lifespans exceeding 50,000 hours and support advanced features such as automatic brightness adjustment and motion sensing. Technology integration is further validated by safety-oriented infrastructure planning in key markets, which emphasizes smart lighting compatibility for commuter and performance cycling ecosystems. In addition, innovations in lightweight and modular designs are making high-performance systems more accessible to a broader consumer base.

Across the market, LED lights account for over 70% of total sales, while motion-sensor and app-connected lighting solutions are experiencing strong annual growth in adoption. Rechargeable battery systems are increasingly preferred over traditional battery types due to lower total cost of ownership and environmental benefits. These advances in lighting technology not only enhance product differentiation but also expand the total addressable market, encouraging both upgrades among existing cyclists and new product adoption among safety-conscious riders. Enhanced software integration with smartphones and cycling apps further strengthens market growth by offering convenience and improved safety monitoring.

High Cost of Premium Lighting Solutions

Advanced bicycle lights with smart features, high lumen outputs, and durable rechargeable systems carry significantly higher price points than basic models. This cost difference limits adoption among budget-conscious consumers, particularly in developing regions where price sensitivity is high. Entry-level riders often continue using basic halogen or battery-powered lights due to affordability constraints. Fluctuating raw material costs, including those for LED components and lithium-ion batteries, further exacerbate production volatility. These factors combine to restrict penetration of premium lighting solutions. Adoption in urban and suburban markets is slower than projected due to these financial barriers.

Recent regulatory and trade developments have amplified cost pressures. U.S. tariffs eliminated exemptions for low-value bicycle imports, raising landed costs for high-performance lighting systems. Similarly, the UK Trade Remedies Authority extended anti-dumping duties on bicycles and bicycle components, thereby increasing component prices. These measures elevate retail prices and dampen uptake among price-sensitive consumers. Consequently, high upfront costs continue to constrain conversion from low-end models. Manufacturers face challenges balancing affordability with advanced feature integration in this environment.

Counterfeit & Low-Quality Imports

The proliferation of low-cost, non-compliant bicycle lights undermines overall market value and erodes consumer confidence. Counterfeit products distort competitive pricing and challenge legitimate manufacturers, while substandard imports slow the adoption of premium, safety-compliant lighting solutions. In extreme cases, defective products may pose safety risks, undermining consumer trust and discouraging repeat purchases. Retailers and manufacturers face additional costs for warranty claims, returns, and customer support when counterfeit products circulate in the market.

Enforcement actions in past years highlight the ongoing problem. Chinese authorities seized over US$ 1.6 million in counterfeit bicycle goods, including unsafe lighting components. European cycling bodies also called for strengthened market surveillance on imported e-bikes and accessories to reduce safety risks. These developments confirm that counterfeit and low-quality imports remain a structural barrier, undermining consumer trust and adoption. Manufacturers and regulators must address both compliance and education to mitigate these risks effectively.

Opportunity Analysis- Smart & Connected Lighting Systems

Smart bicycle lights, featuring motion sensing, automatic brightness adjustment, and smartphone connectivity, represent a high-growth opportunity in the market. Tech-savvy riders and safety-focused commuters are increasingly willing to pay premiums for features that improve awareness and hazard responsiveness. The adoption of smart LED systems is 30% faster among early adopters than that of traditional lighting, highlighting strong potential for market expansion. Urban and performance cyclists alike are seeking lighting solutions that integrate seamlessly with other connected devices, increasing overall engagement with the product ecosystem.

The growing emphasis on cycling innovation is reflected in events such as the Taipei International Cycle Show 2025–2026, which showcased connected and smart lighting technologies as a central theme. Media coverage of pedal-integrated lighting products that can improve visibility by up to 1 km indicates rising consumer interest in advanced safety solutions. These developments validate the trend toward smart, integrated lighting systems and reinforce growth potential for manufacturers offering interoperable ecosystems and app-connected solutions. Investment in software integration and rider analytics further enhances recurring revenue opportunities.

Expansion in Emerging Markets

The emerging economies of Asia Pacific and Latin America offer substantial untapped potential as urban cycling infrastructure improves and disposable incomes rise. Countries such as India and China are experiencing a surge in bicycle use for commuting and recreation, thereby increasing demand for high-quality lighting solutions. The growing urban cyclist population, exceeding 40 million active riders worldwide, represents a significant addressable market for durable and reliable lighting systems. Affordable yet feature-rich solutions can help capture new riders while supporting safe urban mobility.

Government investments and policy initiatives are accelerating this growth. In India, the Pune Metropolitan Region Development Authority allocated INR 286 crore in 2025–26 to upgrade cycling infrastructure ahead of the 2026 international cycling event, improving urban cycling safety. The 2025 Ciclociudades Monitor initiative in Mexico and other Latin American cities also highlighted government commitment to active mobility. These real-world developments create a supportive environment for affordable yet high-quality lighting products, enhancing adoption and market penetration in emerging regions. Coordinated marketing and local partnerships can further maximize reach and revenue potential.

Category-wise Analysis

Product Type Insights

Front lights are expected to remain the dominant product type, accounting for approximately 42% of the bicycle light market revenue share in 2026, due to their essential role in illuminating rider paths and ensuring visibility to oncoming traffic. High-intensity front LED systems are now standard, especially for urban commuters and low-light conditions. Regulatory mandates in Europe and North America requiring night visibility further reinforce this segment’s market dominance. The Garmin Varia RearVue 820 launch in February 2026 highlights industry innovation; although primarily a rear system, its high lumen output and integrated safety tech reflect performance standards expected of front lights, signaling cross-product innovation and elevated safety expectations.

Helmet lights are projected to be the fastest-growing product type, with a CAGR of 11.3%, driven by urban riders, tech-savvy cyclists, and younger demographics seeking 360° visibility and supplementary safety features. Helmet-mounted lights complement front and rear systems, providing elevated visibility angles in traffic. Recent trends emphasize lightweight, rechargeable, and smart sensor-integrated helmets that pair with mobile apps and adaptive lighting. Increasing urban cycling participation and awareness of personal safety are fueling adoption, positioning helmet lights for sustained growth across both emerging and mature markets.

Technology Insights

LED technology is likely to continue its dominance in 2026, capturing over 70% of the bicycle light market share due to superior brightness, energy efficiency, and longevity compared with halogen or xenon systems. LEDs are standard across most front, rear, and auxiliary lighting solutions, including rechargeable variants, making them the baseline for both premium and mass-market products. Falling component costs and long operational life support innovation with adaptive brightness and smart connectivity features. Expert reviews in 2026 highlight the versatility and continued preference for LED lights, confirming their position as the leading technology across bicycle lighting segments.

Motion sensor technology is rapidly gaining adoption, particularly in adaptive lighting and automatic on/off functionality, with around 28% of new lighting models now including motion-based features. The segment is projected to grow at a CAGR of 12.1%, driven by declining sensor costs and rising demand for automation. The Wahoo Trackr Radar light, reviewed in 2026, exemplifies this trend, offering dual flashing LEDs, vehicle detection, and smart-sensor-enabled safety features. Such innovations reflect the increasing mainstream adoption of intelligent, responsive bicycle lighting solutions and the shift toward premium, high-tech systems.

Regional Insights

North America Bicycle Light Market Trends

North America is poised to remain the leading regional market, holding around 35% of the bicycle light market value, supported by widespread cycling safety regulations, high personal income levels, and expanding urban cyclist populations. In Canada’s Ontario province, cyclists are legally required to have a white front light and a red rear light or reflector when riding at night, driving foundational demand for compliant lighting systems across major cities. Community safety initiatives such as Ottawa’s “Cyclists, light up your ride” campaign distributed free bike lights and visibility gear while promoting safer riding practices, underscoring grassroots support for enhanced visibility and lighting adoption.

In the United States, recognition of cycling as a priority mode of active transport is growing: 460 U.S. communities were named “Bicycle Friendly” in early 2025 by the League of American Bicyclists, reflecting local policy and infrastructure improvements that encourage safer riding environments and increase the utility of safety accessories like lights. Such designations typically coincide with investments in bike lanes, shared-use paths, and educational programs that elevate the importance of lighting compliance, particularly for night and low-light conditions. Nationwide efforts, such as the Bipartisan BIKE Act introduced in late 2025, aim to expand youth bike safety education, reinforcing safe riding behaviors and the use of lighting from an early age.

Europe Bicycle Light Market Trends

Europe holds a significant share of the market for bicycle lights, owing to a well-entrenched and expanding cycling culture, urban mobility policies, and safety-oriented infrastructure initiatives. National and municipal governments continue to promote active transport as part of sustainable mobility agendas, reflected in public events such as Urban Mobility Days 2025, organized by the European Commission (EC), where policymakers and city authorities explored accelerating sustainable urban mobility, including cycling safety measures backed by transport departments and authorities across European Union (EU) member states.

Cycling infrastructure improvements and recognition campaigns continue to galvanize regional adoption. The Tour de France Cycle City label celebrated its fifth year with 189 cities recognized for concrete cycling promotion measures, including deployment of bike paths, safety education, and improved amenities, highlighting growing municipal commitment to cycling as daily transport and not just leisure. Urban planners are also testing reward-based cycling incentive programs such as Stockholm’s Bike2Green project, which increased cycling activity using gamification and voucher rewards, demonstrating how European cities are experimenting with behavior-based policies that elevate active mobility and, by extension, demand for visibility gear bicycle lights.

Asia Pacific Bicycle Light Market Trends

Is Asia Pacific likely to emerge as the fastest-growing regional market for bicycle lights, with a projected CAGR of approximately 10.5% during the 2026-2033 forecast period, driven by rapid urbanization, rising disposable income, and expanding active mobility infrastructure. Government actions such as China’s enforcement of mandatory safety standards for e-bikes, designed to improve manufacturing quality and crack down on unsafe products, reinforce demand for compliant visibility solutions including high-performance bicycle lights. Asia’s urban planning initiatives, including cycle lane expansions across South and Southeast Asian cities, support greater daily cycling and increase the demand for quality lighting solutions.

Regional recognition of cycling as an active transport mode is also rising. For example, Christchurch was ranked the most bicycle-friendly city in the Asia-Pacific region, reflecting broader trends toward safer, well-supported cycling environments that promote the uptake of visibility gear. In major economies such as China, India, and Japan, local manufacturing hubs and e-commerce penetration are expanding product availability, while governments encourage cycling as part of sustainable urban mobility strategies. These factors create fertile ground for growth in both entry-level and premium bicycle lighting segments across the region.

Competitive Landscape

The global bicycle light market structure is moderately consolidated, with leading players such as Garmin, Wahoo, Cateye, Lezyne, and Bontrager (Trek) commanding a significant portion of the revenue share. These established companies leverage strong brand recognition, extensive distribution networks, and expertise in smart lighting technology, including LED, motion sensors, and app-connected systems. They continuously invest in R&D to enhance brightness, energy efficiency, connectivity, and durability, ensuring competitive differentiation in both consumer and professional cycling segments.

On the other hand, regional and niche players such as Magicshine, Knog, and Lupine focus on specialized segments, including high-lumen off-road lighting, helmet-mounted systems, and affordable urban commuter solutions. Barriers such as regulatory compliance, high technological development costs, and brand loyalty limit new entrants, but digitalization and smart connectivity trends are enabling tech-focused startups to enter via app-integrated lighting and IoT-enabled safety solutions. Market consolidation is expected to increase gradually as leading global players acquire smaller innovators to expand geographically and technologically, while partnerships with software developers enhance smart lighting ecosystems and recurring aftermarket revenue.

Key Industry Developments

- In January 2026, Magene and iGPSPORT secured partnerships with UCI WorldTour teams for the 2026 season, with Magene supplying smart bike computers, radar tail lights, and training devices to the XDS Astana Team, and iGPSPORT equipping Groupama-FDJ with its navigation systems and radar lights.

- In January 2026, Lezyne strengthened its global distribution network by forming new partnerships with regional distributors in Spain, Portugal, South Africa, Colombia, Denmark, and Sweden, enhancing availability and service support for its LED bike lights and accessories.

- In November 2025, ams OSRAM introduced the new LEDSbike Compact Series, a line of high-performance bicycle LED lights designed to offer improved visibility, compact design, and energy efficiency for urban and outdoor cycling. These lights integrate advanced LED technology and optics to enhance brightness and durability while meeting rider safety requirements.

Companies Covered in Bicycle Light Market

- Cateye Co., Ltd.

- Knog Pty Ltd.

- Garmin Ltd.

- Lezyne Inc.

- Cygolite

- NiteRider

- Blackburn Design

- BBB Cycling

- Gaciron Technology

- Lord Benex International

- Princeton Tec

- Dinotte Lighting

Frequently Asked Questions

The global bicycle light market is projected to reach US$ 453.0 million in 2026.

Increasing safety awareness, regulatory mandates for night riding, and adoption of LED and smart lighting technologies are driving the market.

The market is poised to witness a CAGR of 9.5% from 2026 to 2033.

Emerging demand for smart and connected lighting systems and expansion in urban cycling markets in Asia Pacific and Latin America are key opportunities.

Garmin, Wahoo, Cateye, Lezyne, Bontrager, Magicshine, Knog, and Lupine are some of the key players in the market.