- Aerospace & Defense

- Flight Data Recorder (FDR) Market

Flight Data Recorder (FDR) Market Size, Share, and Growth Forecast, 2026-2033

Flight Data Recorder (FDR) Market by Product Type (Cockpit Voice Recorder (CVR), Flight Data Recorder (FDR)), Aircraft Type (Wide Body, Narrow Body, Turboprop, General Aviation & Business Jets, Rotorcrafts), Application (Civil, Military), and Regional Forecast for 2026-2033

Flight Data Recorder (FDR) Market Share and Trends Analysis

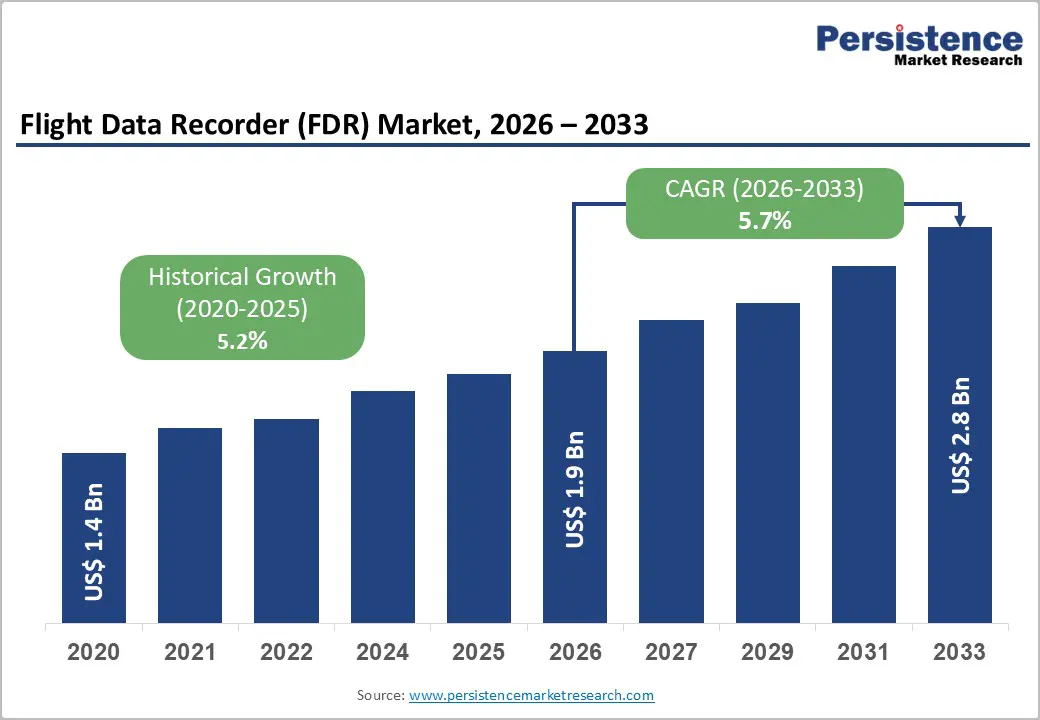

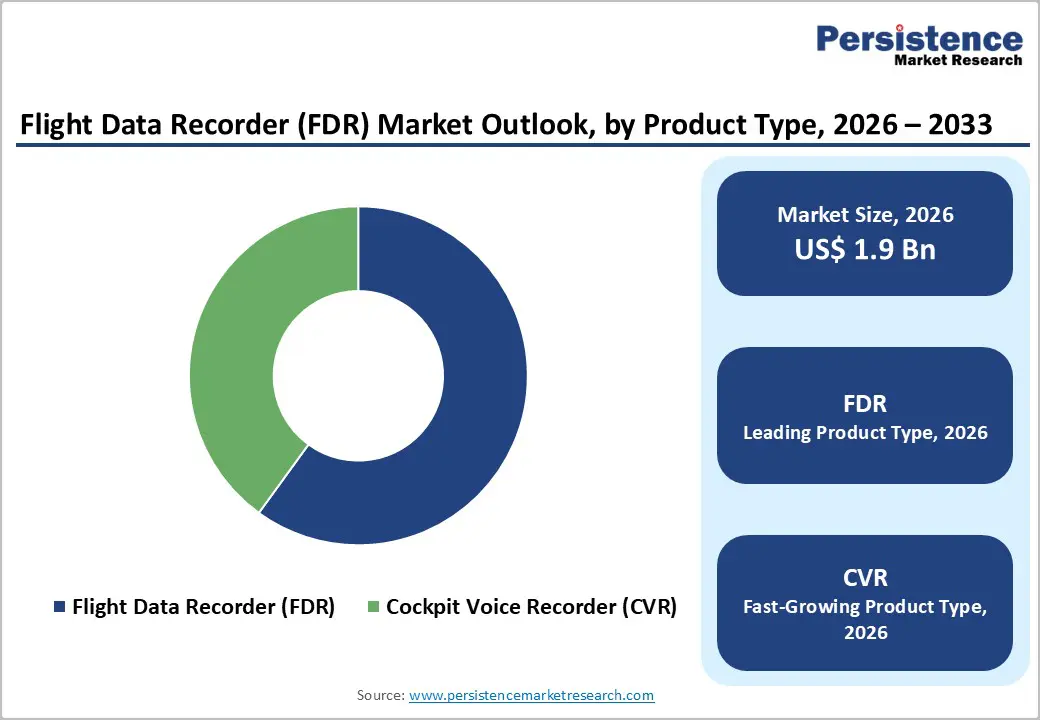

The global flight data recorder (FDR) market size is likely to be valued at US$ 1.9 billion in 2026, and is projected to reach US$ 2.8 billion by 2033, growing at a CAGR of 5.7% during the forecast period 2026-2033.

This steady growth is primarily driven by mandatory aviation safety regulations issued by international authorities such as the International Civil Aviation Organization (ICAO), the Federal Aviation Administration (FAA), and the European Union Aviation Safety Agency (EASA). These agencies have made flight data recorders an essential component for both civil and military aircraft, ensuring that all new and existing fleets are equipped with reliable recording technology. The growing global aircraft fleet and the ongoing replacement of outdated analog systems with advanced digital solid-state recorders are further accelerating market expansion.

The demand for flight data recorders is being reinforced by heightened investigative requirements following aviation incidents and accidents. Aviation authorities and operators are now prioritizing transparency in aircraft accident data, leading to greater adoption of flight data recorders for both retrofit and line-fit installations. This shift is not only improving safety standards but also enabling more accurate and comprehensive post-incident analysis. As a result, the market is experiencing sustained demand growth, with manufacturers focusing on innovation and compliance to meet evolving regulatory and operational needs.

Key Industry Highlights

- Product Type Outlook: Flight data recorders are expected to lead with 60% market share in 2026, supported by universal ICAO, FAA, and EASA mandates.

- Application Dynamics: Civil aviation is anticipated to dominate with 70% share in 2026, driven by mandatory global safety compliance, while military aviation is likely to grow fastest at about 6.1% CAGR through 2033 amid advancements in avionics

- Aircraft Type Trends: Narrow-body aircraft are projected to account for about 45% share in 2026, reflecting high utilization rates, whereas wide-body aircraft are set to grow the fastest at nearly 6% CAGR owing to long-haul fleet expansion drives.

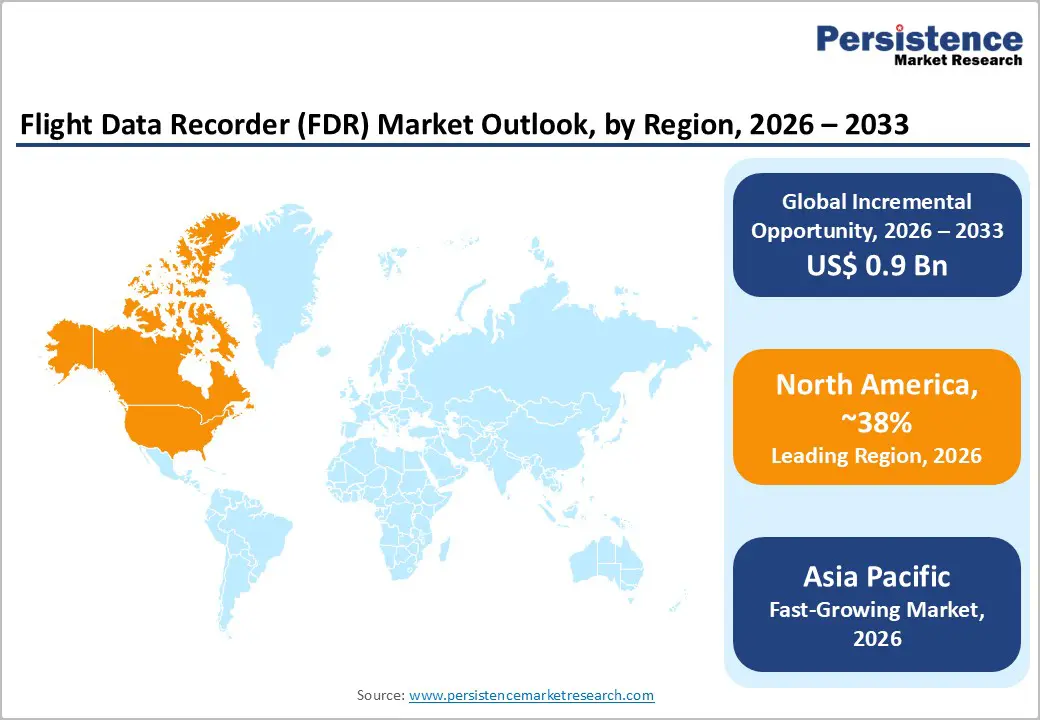

- Regional Performance: North America is forecast to command around 38% of the market in 2026, supported by a large installed aircraft base.

- Fastest-growing Market: Asia Pacific is projected to exhibit the highest 2026-2033 CAGR of 6.5%, fueled by rapid fleet expansion and regulatory alignment in China, India, and Southeast Asia.

- Regulatory & Technology Impact: Regulatory enforcement underpins the majority of recorder installations, ensuring structurally resilient demand across cycles, with technological upgrades fostering replacement demand.

| Key Insights | Details |

|---|---|

| Flight Data Recorder (FDR) Market Size (2026E) | US$ 1.9 Bn |

| Market Value Forecast (2033F) | US$ 2.8 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.7% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.2% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Fleet Expansion and Technology Upgrades in Aviation Safety Systems

The flight data recorder market growth is fundamentally driven by binding international aviation safety regulations enforced by the ICAO, FAA, and the EASA. ICAO Annex 6 mandates the installation of flight data and cockpit voice recorders on all turbine-powered aircraft above defined weight thresholds, making these systems a non-optional safety requirement. Regulatory updates introduced after high-profile aviation incidents have further expanded data retention duration, underwater locator beacon performance, and crash survivability standards. These requirements apply consistently across new aircraft deliveries and in-service fleets, establishing a structural, non-cyclical demand base that remains resilient to short-term aviation market fluctuations.

Alongside regulation, global fleet expansion and technology modernization continue to reinforce demand momentum. Narrow-body aircraft dominate new deliveries, particularly in high-growth aviation markets, directly driving line-fit installations of flight data and cockpit voice recorders. Simultaneously, aging fleets in mature regions are replacing legacy magnetic tape systems with solid-state digital recorders to meet updated compliance standards. Advancements in crash-protected memory, increased data storage capacity, and enhanced survivability under extreme conditions are accelerating upgrade cycles across civil and military aircraft, supporting sustained volume growth and improving average system value.

High Certification Burden and Dependence on Aircraft Production Cycles

The expansion of the FDR market for flight data recorders is being constrained by the stringent certification standards set by organizations such as the European Organisation for Civil Aviation Equipment (EUROCAE), the Radio Technical Commission for Aeronautics (RTCA), and various national aviation authorities. These bodies enforce rigorous performance and survivability requirements, which mandate that all recorders undergo extensive testing for impact shock, fire resistance, deep-sea pressure tolerance, and electromagnetic compatibility. The comprehensive nature of these evaluations significantly extends product development timelines and increases capital expenditure, making it difficult for new entrants to compete. Smaller avionics firms, in particular, face higher certification risks and limited access to testing infrastructure, resulting in high entry barriers. Consequently, competition remains moderate, and technological progress tends to be incremental rather than revolutionary.

Furthermore, the growth trajectory of the flight data recorder market is closely linked to the production cycles of major aircraft manufacturers. Fluctuations in production rates directly influence the demand for line-fit recorders, while delays in aircraft deliveries can disrupt installation schedules. Although aftermarket replacement and retrofit activities provide some demand stability, extended production adjustments still introduce revenue volatility. As a result, recorder manufacturers are highly sensitive to shifts in the broader aerospace supply chain, and their near-term revenue outlook depends largely on the planning and output of aircraft original equipment manufacturers (OEMs). This interdependence underscores the importance of monitoring aerospace industry trends to anticipate market opportunities and risks.

Aftermarket Retrofits, Defense Modernization, and Data-Driven Recorder Applications

Significant growth opportunities in the flight data recorder market arise from retrofit programs in emerging aviation markets and ongoing defense fleet modernization. Operators in Asia Pacific, Latin America, and Africa are progressively upgrading legacy aircraft to meet ICAO compliance standards, ensuring continued airworthiness for domestic and regional operations. Older aircraft often require the installation of certified flight data and cockpit voice recorders to maintain commercial eligibility. The civil aviation authorities are enforcing stricter compliance audits, which accelerates retrofit timelines and expands demand for aftermarket installations. These retrofits not only sustain recurring revenue streams for manufacturers but also reduce reliance on new aircraft deliveries, thereby providing market stability. Emerging market airlines are also recognizing the operational benefits of upgrading to solid-state recorders, which offer higher reliability and extended data retention.

Military modernization programs and data-driven applications are increasingly driving the flight data recorder market. Military rotorcraft and transport aircraft are integrating advanced recorders that align with NATO and national defense standards, thereby improving flight safety, training analysis, and mission debriefing. In civil aviation, flight data monitoring (FDM) and flight operations quality assurance (FOQA) programs enable airlines to analyze onboard data to monitor system health, detect abnormal trends, and identify component wear before failures. This allows a shift from reactive maintenance to predictive, condition-based maintenance, enhancing operational efficiency and reducing downtime. The approach also increases recorder value beyond compliance, optimizing fleet performance and maintenance costs. As hybrid recorder-analytics solutions gain traction, integrating operational insights with recorders further strengthens long-term growth prospects.

Category-wise Analysis

Product Type Insights

Flight data recorders are projected to account for roughly 60% of the FDR market value in 2026, driven by regulatory mandates for accident investigation and fleet safety. FDRs capture critical aircraft performance parameters and are installed across civil and military fleets under ICAO, FAA, and EASA requirements. Demand is reinforced by OEM line-fit orders and retrofits replacing legacy magnetic tape systems with modern solid-state recorders. Honeywell and Curtiss-Wright received certification for the HCR 25 FDR on Boeing 737, 767, and 777 platforms, showcasing next-generation technology. Advanced FDRs offer enhanced data retention, survivability, and compliance assurance. This certification underscores their market leadership and operational importance.

Cockpit voice recorders (CVRs) are poised to be the fastest-growing product segment, registering an estimated 6.3% CAGR through 2033, driven by heightened regulatory focus on human-factor analysis and audio data use in safety investigations. Modern CVRs offer higher channel counts and improved audio clarity, delivering richer operational insights. Manufacturers are developing extended-audio systems that comply with evolving global standards. Universal Avionics expanded its flight recorder readout services to support advanced CVRs, ensuring fleet maintenance and compliance. These innovations enhance safety monitoring and investigative capabilities. Growing regulatory focus and technological upgrades reinforce CVR market expansion.

Aircraft Type Insights

Narrow-body aircraft are projected to lead, capturing approximately 45% of the flight data recorder market revenue share in 2026, due to their prevalence in domestic and short-to-medium haul operations. Frequent flight cycles and large fleet scale drive steady replacement and retrofit demand. Service and maintenance enhancements improve operational reliability. For example, Lufthansa Technik and HENSOLDT introduced next-generation recorders for the Airbus A320 family, enabling on-wing data extraction without unit removal. This reduces maintenance workload and extends intervals. Compliance with stricter data retention mandates reinforces narrow-body dominance. These factors sustain stable market share for this segment.

Wide-body aircraft are projected to be the fastest-growing segment by aircraft type, posting an estimated 6% CAGR through 2033. Long-haul network expansion in Asia Pacific and the Middle East supports demand. Advanced onboard recorders with enhanced parametric capture and performance monitoring make adoption economically attractive. Retrofit and line-fit opportunities further expand penetration. Modern wide-body fleets encourage airlines to integrate advanced recorders for safety and operational insights. Retrofit and line-fit opportunities combine to expand market penetration for this segment, positioning wide-body aircraft as a key future growth driver.

Application Insights

Civil aviation is expected to remain the dominant application segment, accounting for around 70% of the FDR market's revenue share in 2026, driven by compliance requirements and the sheer scale of commercial fleets. Airlines rely on FDRs and CVRs for audits, insurance, and safety monitoring. Integration with FDM and FOQA programs improves predictive maintenance and operational performance. For example, Indian investigators successfully retrieved FDR and CVR data following an Air India Boeing 787 Dreamliner crash. This highlights the critical role of recorders in accident investigation and safety enhancement. Civil fleets continue to drive stable demand for advanced recorder systems.

Military aviation is projected to be the fastest-growing application segment, with an approximate 6.1% CAGR through 2033, driven by modernization programs and advanced flight safety analytics. Rotorcraft and transport aircraft increasingly use FDRs and CVRs compliant with NATO and U.S. defense standards. For example, Curtiss-Wright supplied encrypted recorders for Bell Textron’s MV-75 FLRAA program under the U.S. Army Future Vertical Lift initiative. These recorders enable crash survivability, encrypted data capture, and high-capacity storage. Analytics integration allows early anomaly detection and predictive maintenance, reducing downtime. Defense investments ensure recurring upgrades, positioning military aviation as a high-growth strategic segment.

Regional Insights

North America Flight Data Recorder (FDR) Market Trends

North America is expected to hold 38% of the flight data recorder market share in 2026, driven by a large commercial and military aircraft fleet and stringent regulatory enforcement. The United States anchors demand through the FAA, enforcing compliance audits and modernized recorder installation requirements. A mature maintenance, repair, & overhaul (MRO) ecosystem ensures rapid deployment and lifecycle support for both civil and defense fleets. High fleet utilization and defense aviation spending sustain aftermarket retrofit and upgrade programs. The FAA finalized enhanced flight recorder survivability standards for larger aircraft, encouraging adoption of next-generation devices. OEM partnerships strengthen the installed base, while retrofits provide recurring revenue. Regulation and infrastructure reinforce North America’s leadership position.

Suppliers benefit from long-term OEM and defense contracts, supported by the U.S. Department of Defense (DOD)’s modernization funding. The DOD’s 2025 proposed budget of US$ 850 billion, including US$ 311 billion for acquisition (procurement and RDT&E) and US$ 522 billion for operations and maintenance, allocates significant resources to avionics upgrades, including advanced flight recorders. Investment in digital analytics, predictive maintenance, and secure data systems enhances operational efficiency and recorder adoption. Civil operators also leverage FDM programs to improve fleet safety and reduce downtime. Retrofit compliance remains high, while technological innovation reinforces market differentiation.

Europe Flight Data Recorder (FDR) Market Trends

The Europe FDR market is supported by harmonized safety standards enforced by the EASA, ensuring consistent specifications, certification, and compliance timelines across member states. The key countries such as Germany, the U.K., and France anchor demand through large commercial fleets, major aviation hubs, and defense procurement programs. EASA updated crash survivability and underwater locator beacon standards, prompting airlines to initiate recorder retrofit programs ahead of enforcement deadlines. These regulations enhance fleet safety and ensure that recorders remain integral to both civil and military operations. Strong collaboration among airlines, regulators, and manufacturers sustains predictable adoption. OEMs continue to supply advanced recorder systems tailored to regional compliance requirements.

Aerospace research institutions and accident investigation agencies across Europe drive ongoing investment in recorder technology and operational analytics. Regional manufacturers offer integrated recorder and data processing solutions that meet evolving EASA requirements, strengthening adoption in civil and defense sectors. Defense modernization programs in France and Germany include upgraded flight data systems for rotary and transport aircraft, reinforcing military demand. Airlines increasingly incorporate recorder outputs into FOQA programs to optimize maintenance and operational safety. Coordinated compliance initiatives ensure standardization across fleets, reducing operational risk.

Asia Pacific Flight Data Recorder (FDR) Market Trends

Asia Pacific is projected to be the fastest-growing regional market for flight data recorders, expected to register a 6.5% CAGR between 2026 and 2033, driven by rapid fleet expansion in China, India, and ASEAN countries, which increases aircraft deliveries and retrofit programs. Carriers are modernizing operations and aligning with ICAO safety standards, mandating certified flight recorders on all turbine-powered aircraft. For example, India’s Directorate General of Civil Aviation (DGCA) now requires enhanced data retention for onboard recorders, prompting retrofit activity. Similarly, the Civil Aviation Administration of China (CAAC) updated recorder requirements to include extended data parameters and deeper event capture for commercial and general aviation aircraft. These regulations sustain aftermarket upgrades and fleet modernization. Airlines are adopting advanced recorder systems to enhance compliance and operational efficiency. Regulatory alignment and fleet growth drive sustained regional demand.

Manufacturing cost advantages and localized MRO expansion strengthen the regional aviation value chain. Local production partnerships reduce lead times and improve supply resilience, supporting both OEM and aftermarket demand. Domestic aircraft programs, including China’s narrow-body developments, further boost civil segment adoption. Defense modernization initiatives in China and India involve upgraded recorders for rotorcraft and transport aircraft, expanding military demand. Airlines integrate FDM and predictive maintenance analytics to optimize operations using recorder data. The policy support, fleet expansion, and technology adoption position Asia Pacific for high-growth, long-term opportunities across civil and defense aviation segments.

Competitive Landscape

The global flight data recorder market structure has achieved a moderate level of consolidation, with major industry leaders including Honeywell, Curtiss-Wright, L3Harris, and Universal Avionics collectively securing a significant portion of market revenue. These organizations have built extensive relationships with OEMs and airlines, which enable them to offer tailored solutions and maintain a competitive advantage. Their focus remains on developing advanced memory units, integrating hybrid recorder-analytics systems, and enhancing crash survivability features. Continuous investment in research and development ensures these companies sustain technological leadership, allowing them to respond effectively to evolving regulatory requirements and customer expectations.

Regional and niche players such as Teledyne Controls, Northrop Grumman, and Fokker Technologies are carving out market space by targeting specialized aircraft types and supporting retrofit programs for legacy fleets. Entry into this sector is hindered by high certification expenses and the complexity of system integration, but emerging trends such as predictive maintenance and cloud-enabled analytics are creating opportunities for software-centric participants. Strategic acquisitions and collaborative partnerships are accelerating market consolidation, while ongoing innovation in recorder technologies continues to differentiate product offerings. Defense modernization and civil aviation upgrades are expected to sustain demand over the long term, ensuring a dynamic and evolving competitive landscape.

Key Industry Developments

- In October 2025, HENSOLDT and Lufthansa Technik introduced SferiRec CVR and FDR systems with up to 45 hours of cockpit audio, 170 hours of datalink, and 1,600 hours of flight data. The recorders feature on-wing readout, enabling direct aircraft data extraction, reducing maintenance costs. Initial deployment targets the Airbus A320 family, exceeding FAA and EASA requirements. This launch enhances operational efficiency and fleet readiness.

- In October 2025, Acron Aviation partnered with Airbus to offer retrofit solutions using the SRVIVR25, a 25-hour CVR fully compliant with FAA and EASA regulations. SRVIVR25 simplifies compliance for existing narrow-body fleets and improves audio recording quality. Upgrades reduce aircraft downtime and strengthen aftermarket service opportunities.

- In July 2025, Air France-KLM, with Accenture and Google Cloud, launched a generative AI factory to scale AI capabilities across operations. The platform integrates flight data analytics for predictive maintenance and operational optimization. Tools like private AI assistants and retrieval-augmented generation (RAG) accelerate aircraft damage diagnosis by over 35%.

Companies Covered in Flight Data Recorder (FDR) Market

- L3Harris Technologies

- Honeywell Aerospace

- Curtiss-Wright Corporation

- Safran Electronics & Defense

- Leonardo S.p.A.

- GE Aerospace

- Elbit Systems

- Thales Group

- Universal Avionics

- ACR Electronics

- Teledyne Technologies

- Meggitt PLC

Frequently Asked Questions

The global flight data recorder (FDR) market is projected to reach US$ 1.9 billion in 2026.

Mandatory aviation safety regulations, global fleet expansion, and technological upgrades in crash-protected memory, analytics integration, and predictive maintenance are primary growth drivers.

The market is poised to witness a CAGR of 5.7% from 2026 to 2033.

Opportunities include retrofit programs in emerging aviation markets, military modernization initiatives, and integration of flight data with predictive maintenance and operational analytics.

Honeywell, Curtiss-Wright, L3Harris, Universal Avionics, Teledyne Controls, Northrop Grumman, Fokker Technologies are among the leading market companies.