- Aerospace & Defense

- Flight Simulator Market

Flight Simulator Market Size, Share, and Growth Forecast 2026 - 2033

Flight Simulator Market by Product Type (Full Flight Simulator, Flight Training Device, Full Mission Simulator, Fixed-Based Simulator), by Solution (Hardware Products, Software, Services), by Method (Live, Virtual, Synthetic), by Platform (Commercial, Military, UAV), by End User (Airlines, Military & Defense Organizations, Flight Training Academies, OEMs, Research Institutions), and Regional Analysis, 2026 - 2033

Flight Simulator Market Size and Trend Analysis

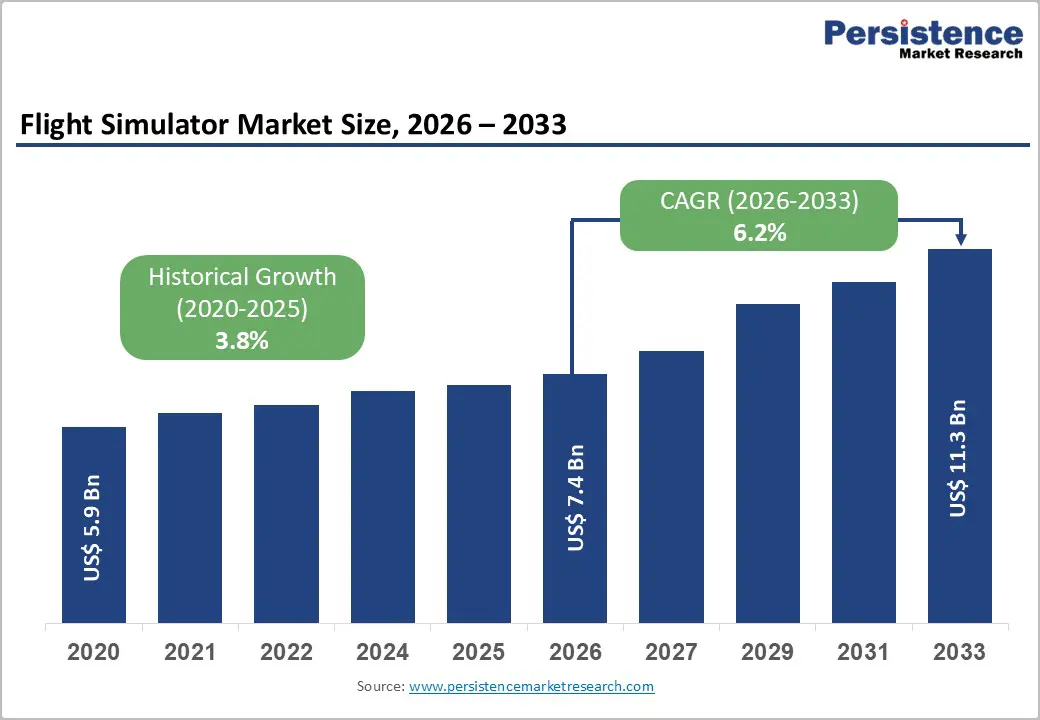

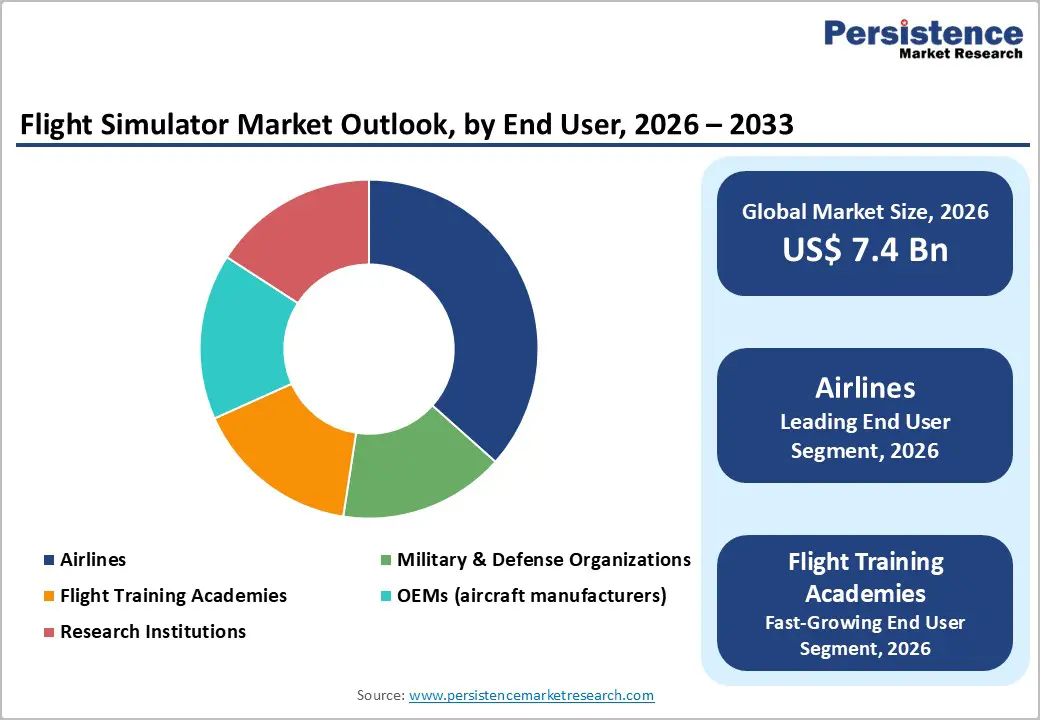

The global flight simulator market size is expected to be valued at US$ 7.4 billion in 2026 and projected to reach US$ 11.3 billion by 2033, growing at a CAGR of 6.2% between 2026 and 2033.

Rising global air traffic, a critical shortage of qualified pilots, and intensifying military modernization programs are collectively driving sustained demand for advanced flight simulation solutions. The International Air Transport Association (IATA) projects that the aviation industry will need over 600,000 new pilots by 2040, making simulation-based training a regulatory and operational imperative. Simultaneously, defense agencies worldwide are increasing procurement of high-fidelity simulators to reduce the cost and risk of live flight training, further anchoring the market's long-term growth trajectory.

Key Industry Highlights:

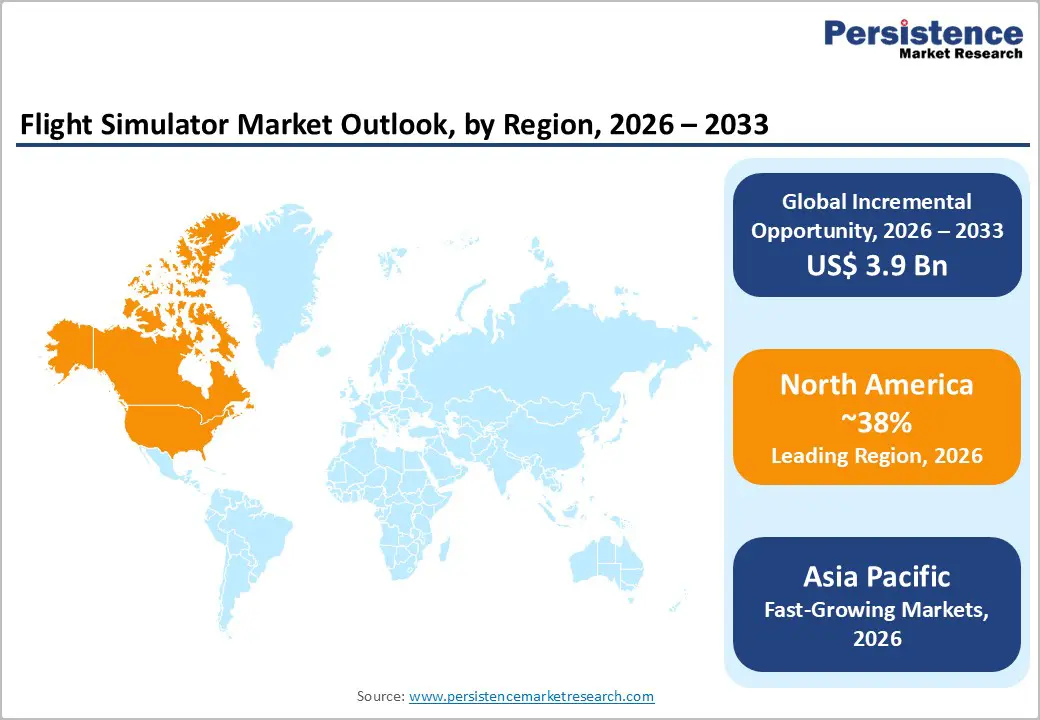

- Leading Region: North America leads the global flight simulator market with approximately 38% revenue share in 2025, anchored by the world's largest defense simulation budget and a dense network of FAA Part 142-certified commercial training centers.

- Fastest Growing Region: Asia Pacific is the fastest growing regional market at a projected CAGR of 8.1% through 2033, driven by China's CAAC mandates, India's aviation infrastructure expansion, and Southeast Asia's rapid low-cost carrier fleet growth.

- Dominant Platform: The Military platform segment commands approximately 46% of global market share in 2025, sustained by non-discretionary sovereign defense budgets and the cost-efficiency imperative of simulation over live flight training for fifth-generation aircraft programs.

- Fastest Growing Platform: UAV platform simulation is the fastest growing segment at approximately 9.6% CAGR through 2033, driven by emerging regulatory frameworks for drone BVLOS operations and the rapid expansion of military and commercial UAV fleets globally.

- Key Opportunity: The AI-driven simulation-as-a-service model represents the most actionable near-term opportunity, converting the market from CapEx to OpEx and expanding total addressable demand by bringing simulation within reach of smaller regional carriers and academies.

Market Dynamics

Drivers - Global Pilot Shortage and Mandatory Regulatory Training Requirements

Aviation stakeholders, including airlines, training academies, and regulatory bodies, must recognize that the escalating global pilot deficit is structurally hardwiring simulator demand into the industry's workforce development pipeline. The Federal Aviation Administration (FAA) and European Union Aviation Safety Agency (EASA) mandate minimum flight simulation hours for pilot certification and recurrent training, making Full Flight Simulator (FFS) usage non-discretionary.

Boeing's Pilot & Technician Outlook 2023-2042 estimates a need for 602,000 new commercial pilots globally over the next two decades, with Asia Pacific accounting for nearly 40% of this demand. This structural talent gap is converting simulator procurement from a capital expenditure choice into a compliance-driven necessity, reinforcing long-term order pipelines for manufacturers and training organizations alike.

Defense Modernization and Reduced Cost-Per-Flight-Hour Economics

Defense ministries globally are pivoting to simulation as the primary medium for tactical and combat training, driven by compelling economics and operational imperatives that cannot be met through live sorties alone. The U.S. Department of Defense (DoD) has repeatedly cited simulation as a cornerstone of its "Train as You Fight" doctrine, with the U.S. Army reporting that full-mission simulation reduces per-flight-hour training costs by as much as 90% compared to actual aircraft operations. The NATO alliance's collective defense spending target of 2% of GDP for member states, with many countries now exceeding this threshold, is channeling significant procurement budgets toward synthetic training environments.

The ongoing development of next-generation combat aircraft, including the F-35 Lightning II and Eurofighter Typhoon programs, embeds dedicated simulation ecosystems into program-of-record requirements, ensuring multi-year revenue visibility for market participants.

Restraints - High Capital Cost and Long Procurement Cycles for Full Flight Simulators

The prohibitive upfront capital cost of Level D Full Flight Simulators, the highest regulatory certification tier, suppresses market entry and constrains demand particularly among smaller regional carriers and training academies in emerging economies. A single Level D FFS can cost between US$ 10 million and US$ 18 million, with annual maintenance contracts adding 10-15% of asset value per year. Regulatory recertification requirements, typically mandated every 12 months under FAA Advisory Circular 120-40C and comparable EASA standards, add further recurring cost burdens.

For new entrants in markets such as Southeast Asia and Sub-Saharan Africa, this cost architecture creates a structural financing barrier, limiting market penetration and forcing many operators to rely on shared or leased simulator access rather than outright ownership.

Cybersecurity Vulnerabilities in Networked and Cloud-Connected Simulation Platforms

As simulation platforms increasingly integrate networked environments, cloud-based data analytics, and real-time software updates, they introduce expanding attack surfaces that defense and commercial operators must treat as mission-critical risks. The U.S. Cybersecurity and Infrastructure Security Agency (CISA) has classified aviation training infrastructure as a critical sector, and any breach in a military simulation network could compromise operational tactics or classified aircraft performance data.

Vendors unable to demonstrate robust cybersecurity compliance, particularly to frameworks such as CMMC (Cybersecurity Maturity Model Certification) for U.S. defense contracts, face disqualification from high-value government procurement processes. This regulatory and reputational risk dynamic is adding non-trivial cost and complexity to product development roadmaps, effectively slowing innovation cycles and increasing the barriers to winning sovereign defense contracts.

Market Opportunities

Rapid Expansion of UAV and Advanced Air Mobility (AAM) Simulation Platforms

The emergence of unmanned aerial vehicles and advanced air mobility as mainstream operational and commercial platforms presents a high-growth adjacency that established flight simulation vendors are uniquely positioned to capture, provided they act before a new generation of born-digital competitors defines the category. The Federal Aviation Administration issued its UAV Integration Pilot Program framework, and the agency's UAV Beyond Visual Line of Sight (BVLOS) regulatory pathway is creating certification requirements that implicitly demand simulation-based operator validation. The global commercial drone market is projected to carry cargo and passengers at scale by the late 2020s, with companies like Joby Aviation, Archer Aviation, and Wisk Aero actively developing dedicated simulator programs for their electric vertical take-off and landing (eVTOL) platforms.

Simulation vendors who develop modular, reconfigurable platforms compatible with next-generation aircraft architectures will capture early-mover advantage in a segment where training infrastructure is still nascent and standards are actively being written by regulators.

AI-Driven Adaptive Training Systems and Cloud-Based Simulation-as-a-Service

The convergence of artificial intelligence, cloud computing, and data analytics is enabling a structural shift from hardware-intensive simulation facilities to scalable, software-defined training ecosystems, and market participants who lead this transition will redefine competitive positioning across the value chain. AI-enabled adaptive training platforms can dynamically adjust scenario difficulty, identify individual trainee skill gaps in real time, and generate personalized training curricula, capabilities that are increasingly demanded by airlines facing compressed training timelines and budget pressures.

The EASA and ICAO are actively developing competency-based training frameworks that favor data-driven performance assessment over fixed hour requirements, directly incentivizing adoption of AI-powered simulators. Companies such as CAE Inc. have already launched cloud-based training platforms, CAE's CAE Rise™ platform exemplifies this shift, while startups are offering simulation-as-a-service (SaaS) models that dramatically lower the barrier to entry for smaller operators. This transition from CapEx to OpEx models is expanding the total addressable market by bringing simulation within reach of operators previously priced out of traditional hardware-centric procurement.

Category-wise Insights

Product Type Analysis

Full Flight Simulators (FFS) command approximately 42% of the flight simulator market by product type, a position sustained by their status as the only simulation category qualifying for zero-flight-time type rating certifications under FAA and EASA frameworks. This regulatory exclusivity makes FFS procurement a non-negotiable investment for major commercial airlines and military operators seeking to meet mandated training hour requirements. The segment's dominance is structurally durable as no lower-cost alternative replicates the motion, visual, and systems fidelity required for Level C and Level D qualification.

Flight Training Devices (FTDs), meanwhile, are the fastest growing type segment with an estimated CAGR of 7.8% through 2033, driven by their lower cost and the expanding pool of regional carriers and academies in Asia Pacific and Latin America seeking regulatory compliance at accessible price points.

Solution Analysis

Software solutions lead the flight simulator market by solution category, accounting for approximately 44% of total segment revenue in 2025, and the underlying drivers are structural rather than cyclical. The increasing complexity of simulation scenarios, encompassing multi-failure environments, adverse weather modeling, and synthetic threat generation for military applications, demands continuous software updates and AI integration that hardware alone cannot deliver. Vendors increasingly generate high-margin recurring revenue through software licensing and subscription models, making this segment the most attractive from a margin and growth perspective.

Services represent the fastest growing solution segment with a projected CAGR of 7.1% through 2033, reflecting rising demand for maintenance-as-a-service contracts, instructor-operated station upgrades, and cloud-based analytics subscriptions from operators seeking to reduce in-house technical staffing.

Method Analysis

The Virtual method segment accounts for approximately 48% of the market by training method in 2025, establishing clear leadership in simulation methodology. Virtual simulation's dominance reflects the broad utility of immersive, computer-generated environments that replicate real-world cockpit conditions without the infrastructure requirements of full-motion platforms. The adoption of virtual reality (VR) headsets, with manufacturers including Meta and Varjo introducing aviation-grade head-mounted displays, is expanding virtual simulation's addressable applications.

The Synthetic training method is the fastest growing segment at approximately 8.3% CAGR through 2033, driven by defense forces' growing investment in constructive simulation environments and large-force exercises that cannot be practically replicated in live or virtual-only environments.

Platform Analysis

The Military platform segment holds the leading position with approximately 46% market share in 2025, underpinned by the scale and non-discretionary nature of sovereign defense training budgets. Governments in the United States, United Kingdom, France, and India are investing heavily in simulation-based combat readiness programs to manage costs associated with fifth-generation fighter aircraft and helicopter fleet training. UAV platforms represent the fastest growing segment at an estimated CAGR of 9.6% through 2033, as civilian and military drone operators globally transition from ad hoc to structured, regulation-mandated simulation training programs.

End User Analysis

Airlines represent the dominant end-user segment at approximately 36% market share in 2025, driven by both regulatory compulsion and the volume scale of commercial aviation operations globally. IATA data confirms that commercial airlines collectively conduct tens of millions of flight hours annually, each associated with mandated initial, recurrent, and check training simulation requirements. The depth and predictability of airline procurement cycles, typically tied to multi-year fleet expansion plans, make this segment a stable revenue base for leading vendors.

Flight Training Academies are the fastest growing end-user category with a projected CAGR of 8.0% through 2033, as global aviation education investment accelerates particularly across Asia Pacific, Middle East, and Africa regions to address the long-term pilot supply deficit.

Regional Insights

North America Flight Simulator Market Trends and Insights

North America dominates the global flight simulator market with approximately 38% revenue share in 2025, anchored by the world's largest defense simulation procurement budget and a mature commercial aviation training infrastructure. The U.S. Department of Defense remains the single largest institutional customer for high-fidelity military simulation globally, while the dense concentration of commercial carriers and FAA-designated Part 142 training centers sustains consistent civilian demand.

Canada's robust aerospace manufacturing base, anchored by CAE Inc. in Montreal, further strengthens the region's supply-side capabilities. Looking ahead, the North American market is poised to accelerate adoption of cloud-integrated and AI-enhanced simulation ecosystems as operators modernize legacy training infrastructure.

U.S. Flight Simulator Market Size

The United States accounts for approximately 88% of North America's flight simulator market, reflecting its unmatched scale in both defense spending and commercial aviation training activity. The U.S. Air Force's Advanced Training Systems (ATS) program and the U.S. Navy's Naval Aviation Training Next (NATN) initiative collectively represent multi-billion-dollar modernization commitments through the early 2030s. With the FAA's projected airspace capacity expansion and growing airline demand, the U.S. market trajectory remains strongly upward through the forecast period.

Europe Flight Simulator Market Trends and Insights

Europe represents approximately 26% of global flight simulator revenues in 2025, shaped by a dual demand structure of civilian regulatory compliance and NATO-aligned military modernization. EASA's competency-based training and assessment (CBTA) framework is accelerating simulator adoption across European carriers and training organizations by shifting certification toward data-verified skill outcomes rather than fixed flight hours.

The region's commitment to the European Defence Fund (EDF) and bilateral defense cooperation programs is channeling new investment into joint simulation infrastructure across member states. Europe's trajectory points toward consolidation of regional training center networks and increased cross-border simulator utilization agreements.

Germany Flight Simulator Market Size

Germany holds approximately 18% of the European flight simulator market, supported by the Bundeswehr's active modernization of rotary and fixed-wing training programs and Lufthansa Aviation Training's world-class commercial simulation facility in Munich. Germany's status as a NATO frontline member and its expanding Eurofighter Typhoon fleet commitment sustains strong military procurement. Continued investment in next-generation aerospace platforms ensures Germany's position as Europe's leading simulation market will hold through 2033.

U.K. Flight Simulator Market Size

The United Kingdom accounts for roughly 16% of European flight simulator market revenue, driven by the Royal Air Force's Project Appropriation MFTS (Military Flying Training System) and British Airways' and EasyJet's ongoing simulator fleet investments. The UK's post-Brexit regulatory divergence from EASA has prompted domestic investment in CAA-compliant training infrastructure, creating near-term procurement opportunities. London Heathrow's position as one of Europe's busiest hubs sustains recurrent demand for commercial simulation capacity.

France Flight Simulator Market Size

France represents approximately 15% of the European market, underpinned by Thales Group's domestic production capabilities and the French Air and Space Force's (Armée de l'Air et de l'Espace) active Rafale fleet expansion. Air France Industries KLM Engineering & Maintenance operates one of Europe's largest commercial simulator maintenance ecosystems, sustaining strong aftermarket services demand. France's deepened defense industrial collaboration through the Future Combat Air System (FCAS) program signals growing simulation investment through the early 2030s.

Asia Pacific Flight Simulator Market Trends and Insights

Asia Pacific is the fastest growing regional market, projected to expand at a CAGR of approximately 8.1% between 2026 and 2033, fueled by aviation sector expansion across China, India, and Southeast Asia. China's Civil Aviation Administration of China (CAAC) has implemented stringent simulator training mandates, while COMAC's C919 commercial aircraft program is catalyzing domestic simulator ecosystem development. India's DGCA-mandated training requirements and Southeast Asia's rapidly expanding low-cost carrier networks are converting structural pilot demand into near-term simulator procurement.

Companies targeting this geography must align with local joint-venture requirements and rapidly evolving national aviation authority certification frameworks to capitalize on this accelerating growth.

India Flight Simulator Market Size

India represents approximately 18% of the Asia Pacific flight simulator market, with demand driven by the Directorate General of Civil Aviation (DGCA) mandates and India's ambitious target of operating 220 airports under the UDAN regional connectivity scheme by 2025. The Indian Air Force's Tejas MK-2 and MMRCA modernization programs are adding significant military simulation procurement volume. India's flight simulator market is on a steep growth trajectory that will likely elevate its regional share materially through the forecast period.

Japan Flight Simulator Market Size

Japan accounts for approximately 14% of the Asia Pacific market, anchored by Japan Airlines (JAL) and All Nippon Airways (ANA), which collectively operate among Asia's most comprehensive corporate simulation training fleets. The Japan Air Self-Defense Force (JASDF) is progressively expanding its simulation infrastructure in alignment with F-35A integration into its combat fleet. Japan's aging pilot workforce and strict aviation authority training protocols will sustain consistent demand growth through 2033.

Southeast Asia Flight Simulator Market Size

Southeast Asia collectively represents approximately 16% of the Asia Pacific flight simulator market, with the region's low-cost carrier proliferation, led by AirAsia, Lion Air Group, and VietJet Air, driving accelerating simulator procurement to meet ICAO and local DGCA training requirements. Singapore, through the Civil Aviation Authority of Singapore (CAAS), operates the region's most advanced regulatory framework, positioning it as the simulation hub for ASEAN carriers. The region is expected to see the fastest intra-Asia Pacific growth as fleet expansion continues at double-digit rates.

Competitive Landscape

The global flight simulator market is moderately consolidated, with CAE Inc., FlightSafety International, and L3Harris Technologies collectively commanding the highest revenue shares in both civil and defense simulation. Scale remains the primary competitive differentiator in the Full Flight Simulator segment, where long-term airline contracts, regulatory certification expertise, and global maintenance networks create formidable barriers to entry. However, the software and services layer is increasingly contested by both specialist technology firms and Tier 1 defense contractors pursuing vertical integration strategies.

Thales Group and Lockheed Martin have deepened their simulation capabilities through organic R&D and targeted acquisitions, while newer entrants are leveraging AI and game-engine technologies, notably Unreal Engine, to challenge the incumbents on visual fidelity and per-unit economics. The dominant strategic themes shaping competitive positioning include platform agnosticism, cloud interoperability, and the pivot from hardware-only sales toward lifecycle training partnerships.

Key Developments

- November 2025: Boeing launched its Virtual Airplane Procedures Trainer, a cloud-based pilot training platform powered by Microsoft Azure and Microsoft Flight Simulator, enabling immersive, customizable, and device-agnostic training to improve pilot readiness and reduce reliance on traditional simulators.

- June 2025: Next Level Racing partnered with Microsoft Flight Simulator to launch a purpose-built flight simulator cockpit featuring an ergonomic seat, modular design, and universal hardware compatibility, enhancing realism and long-duration comfort for immersive pilot training experiences.

- March 2025: MOZA Racing unveiled a new lineup of next-generation sim racing and flight simulation hardware, integrating automotive technologies to enhance realism, precision, and performance, aiming to bridge the gap between virtual simulation and real-world driving and flying experiences.

Flight Simulator Market - Key Insights & Details

| Key Insights | Details |

|---|---|

| Historical Market Value (2020) | US$ 5.9 Billion |

| Current Market Value (2026) | US$ 7.4 Billion |

| Projected Market Value (2033) | US$ 11.3 Billion |

| CAGR (2026 - 2033) | 6.2% |

| Leading Region | North America, 38% market share (2025) |

| Dominant Product Type | Full Flight Simulator, 42% market share (2025) |

| Top-Ranking Solution Type | Software, 44% market share (2025) |

| Incremental Opportunity (2026 - 2033) | US$ 3.9 Billion |

Companies Covered in Flight Simulator Market

- CAE, Inc.

- FlightSafety International Inc.

- L3Harris Technologies

- The Boeing Company

- Lockheed Martin Corporation

- Thales Group

- TRU Simulation + Training Inc.

- Raytheon Technologies Corporation

- HAVELSAN

- Aero Simulation Inc.

- Textron Aviation Inc.

- Elbit Systems Ltd.

- Indra Sistemas S.A.

- Frasca International Inc.

- Rockwell Collins (Collins Aerospace)

Frequently Asked Questions

The market is expected to reach US$ 7.4 billion in 2026.

Demand is driven by the global pilot shortage, defense modernization, and regulatory training mandates.

North America leads due to strong defense spending, advanced training infrastructure, and regulatory frameworks.

The key opportunity lies in AI-driven training systems and simulation-as-a-service models.

Key players include CAE Inc., FlightSafety International, L3Harris Technologies, The Boeing Company, Lockheed Martin Corporation, Thales Group, TRU Simulation + Training Inc., Raytheon Technologies Corporation, HAVELSAN, Aero Simulation Inc., Elbit Systems, and Indra Sistemas.