- Aerospace & Defense

- Aircraft Flight Control System Market

Aircraft Flight Control System Market Size, Share, and Growth Forecast, 2026 - 2033

Aircraft Flight Control System Market by Functional Role (Primary Flight Control Surfaces, Secondary Flight Control Surfaces), Component System (Control Surfaces, Actuators, Flight Control Surface Mechanism, Sensors, Cockpit Control, Others), Aircraft Type (Commercial Aircraft, Military Aircraft, Business Jets, Regional Aircraft, UAVs / Drones, Helicopters), and Regional Analysis for 2026 - 2033

Aircraft Flight Control System Market Share and Trends Analysis

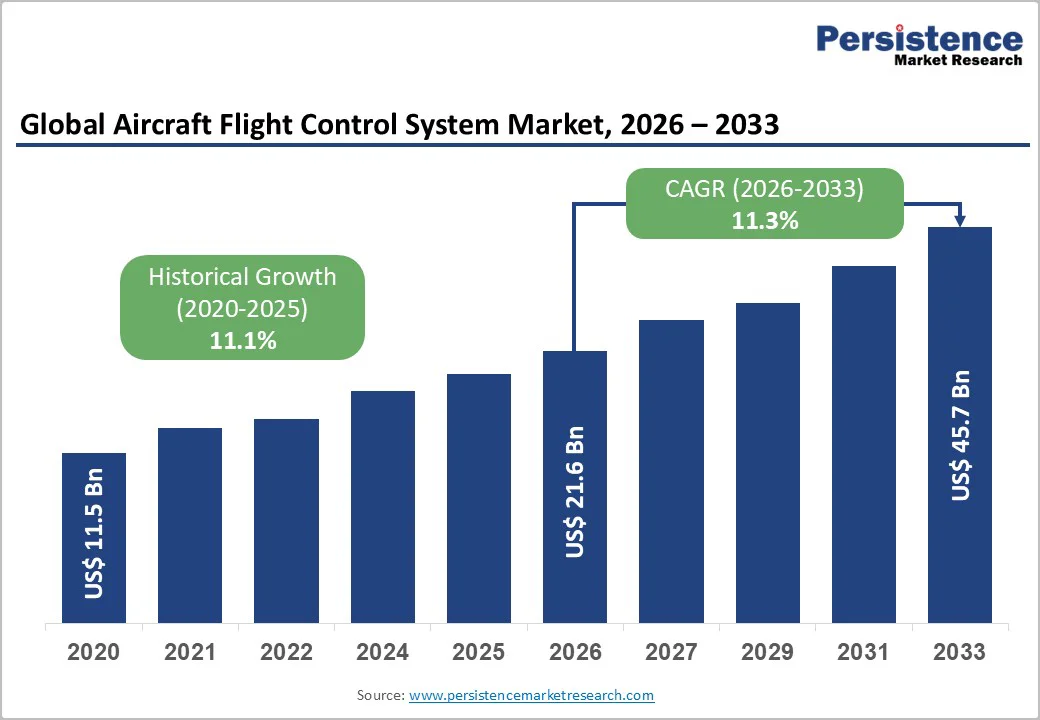

The global aircraft flight control system market size is likely to be valued at US$ 21.6 billion in 2026 and is estimated to reach US$ 45.7 billion by 2033, growing at a CAGR of 11.3% during the forecast period 2026 - 2033.

Increasing demand for air travel globally, technological advancements such as fly-by-wire and power-by-wire systems, and heightening need for safety and fuel efficiency in aviation are factors driving the expansion of the market. Innovation in sensors and actuators, along with growth in emerging economies such as the Asia Pacific, further propels market growth. Regulatory frameworks emphasizing safety and automation also support sustained expansion.

Key Industry Highlights

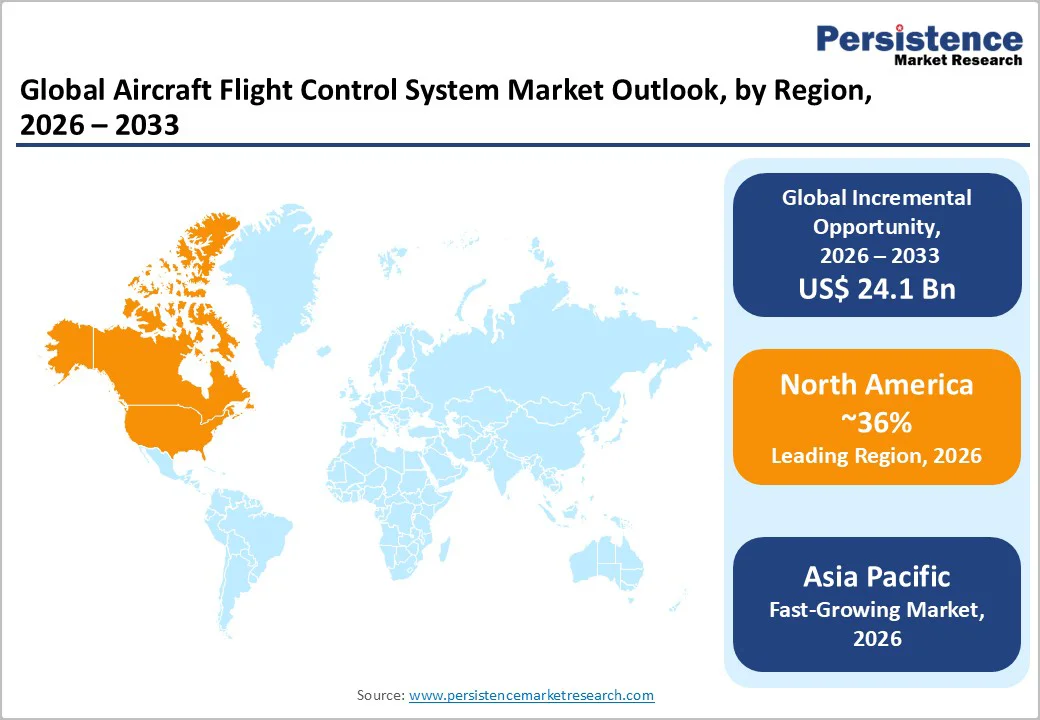

- Dominant Region: North America is projected to hold a 36% share in 2026, driven by a growing aircraft fleet in the U.S. and a robust supplier ecosystem.

- Fastest-growing Market: Asia Pacific is expected to be the fastest-growing market through 2033, owing to fleet modernization and indigenous aircraft production.

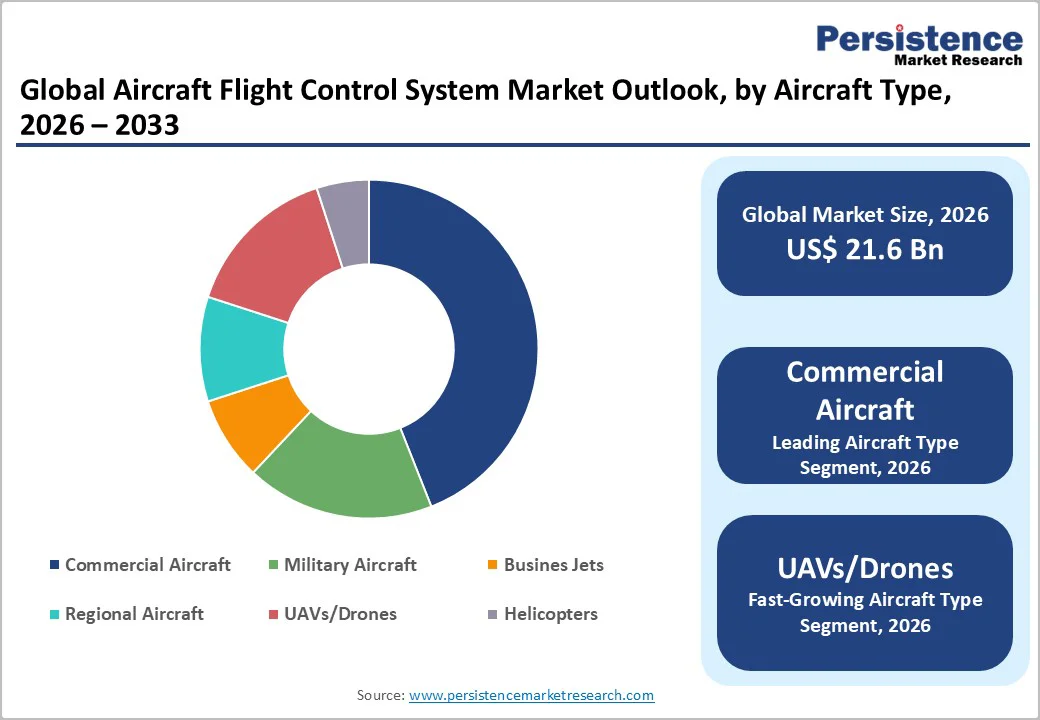

- Leading Aircraft Type: Commercial aircraft are projected to lead with a 44% share in 2026, driven by fleet expansion, aircraft replacement, and fuel-efficient model adoption.

- Fastest-growing Aircraft Type: UAVs and drones are likely to be the fastest-growing segment from 2026 to 2033, on account of expanding defense budgets and increase in the number of regulatory approvals.

- November 2025: Airbus announced an immediate software update for 6,000 A320 aircraft due to a vulnerability discovered after an incident involving data corruption in control systems due to solar radiation.

| Key Insights | Details |

|---|---|

| Aircraft Flight Control System Market Size (2026E) | US$ 21.6 Bn |

| Market Value Forecast (2033F) | US$ 45.7 Bn |

| Projected Growth (CAGR 2026 to 2033) | 11.3% |

| Historical Market Growth (CAGR 2020 to 2024) | 11.1% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Advancements in Flight Control Technologies

Modern flight control systems represent a competitive advantage in contemporary aviation, delivering measurable improvements across three critical dimensions. Enhanced precision capabilities reduce pilot workload substantially, while sophisticated flight envelope protection mechanisms strengthen safety performance across commercial aircraft, military platforms, and unmanned aerial vehicles (UAVs).

The architecture supporting these improvements centers on digital fly-by-wire systems (DFBW), intelligent actuators, and sensor fusion technologies that enable aircraft to respond with greater agility and reliability. Operators actively seek control solutions that expand handling capabilities and refine control logic, creating sustained demand for sophisticated next-generation systems that meet increasingly stringent performance benchmarks.

The acceleration toward autonomous and semi-autonomous flight operations introduces a second transformative dimension, as these capabilities fundamentally depend on advanced control algorithms and dependable real-time processing infrastructure.

The industry's transition to lightweight electromechanical actuators, coupled with embedded health-monitoring functionality and redundancy architectures, establishes longer equipment lifecycles and more predictable modernization schedules.

High Production and Maintenance Costs

High production and maintenance costs remain a central restraint due to the technical depth involved in developing flight-critical systems that must meet stringent certification standards. Engineering teams work with advanced composites, redundant architectures, precision sensors, and high-reliability actuators, each requiring specialized manufacturing environments and rigorous validation cycles.

Every component must align with strict safety, durability, and performance thresholds, raising expenditures tied to design, testing, certification, and quality assurance. This creates a capital-intensive environment that elevates entry barriers and extends development timelines.

Maintenance requirements further amplify the cost burden, as operators must support continuous inspection, calibration, and replacement schedules to sustain performance and airworthiness. Components experience mechanical stress, vibration loads, and environmental exposure, driving demand for high-value spare parts and technically skilled labor.

Airlines and defense operators face recurring lifecycle expenses, from software upgrades to actuator overhauls, which influence procurement decisions and slow broader fleet-level integration.

Increasing Demand for UAVs/Drones

Growing deployment of unmanned aerial platforms is creating a new design and technology cycle for advanced control architectures. Rising adoption of drones in defense missions, long-endurance surveillance and mapping, inspection, and cargo operations requires compact, lightweight, and highly resilient control solutions capable of managing rapid maneuvers, variable payloads, and autonomous navigation.

This expansion pushes manufacturers to integrate higher-precision actuators, adaptive control logic, and next-generation sensing frameworks tailored for unmanned operations.

High-volume production of commercial and industrial UAVs is accelerating demand for scalable, cost-efficient control modules that support automation, real-time decision capabilities, and mission reliability. Growing adoption of BVLOS (Beyond Visual Line of Sight) operations, automated fleet management, and AI-driven flight stabilization is stimulating long-term investment in advanced control technologies.

This shift is strengthening the pathway for innovation, creating space for suppliers to introduce miniaturized components, digital control architectures, and integrated flight management solutions suited for diverse UAV classes.

Category-wise Analysis

Functional Role Insights

Primary flight control surfaces hold the leading position with a projected 52% of the aircraft flight control system market revenue share in 2026, supported by their essential function in maintaining aircraft stability, attitude control, and overall flight performance.

Every commercial, military, business, regional, and unmanned platform relies on these surfaces for safe operations, creating consistent procurement cycles. Their mandatory integration, strict certification standards, and continuous demand in production and maintenance reinforce a strong and sustained leadership position.

Secondary flight control surfaces are set to represent the fastest-growing segment from 2026 to 2033, fueled by their rising integration in new-generation aircraft and expanding adoption in UAV platforms. Innovations in lightweight mechanisms, advanced actuation systems, and digital control capabilities are elevating efficiency and mission adaptability.

Growth is expected to accelerate by 2026 as manufacturers invest in upgraded configurations and air-framers prioritize improved lift management, energy optimization, and enhanced low-speed performance across diverse aircraft fleets.

Component System Insights

Actuators are poised to dominate the component system segment with a projected 37.8% share in 2026, reflecting their indispensable role in translating control commands into reliable control surface movements.

Original equipment manufacturers (OEMs) and maintenance, repair, & overhaul (MRO) providers prefer actuators for their robust mechanical design, high load tolerance, and regulatory-proven performance. Integrated redundancy, established supply chains, and predictable lifecycle replacement cycles continually sustain revenue stability and investment in the market

Sensors are expected to be the fastest-growing component segment between 2026 and 2033, owing to escalating system complexity and demand for precise situational awareness across platforms.

Downsizing, higher sampling rates, and fusion of inertial, optical, and air-data inputs enable autonomous functions and safe BVLOS operations. Suppliers reporting strong uptake anticipate accelerated sensor adoption by 2026, driving R&D spending, modular sensor suites, and integration with digital flight-control architectures.

Aircraft Type Insights

Commercial aircraft are predicted to hold the leading position with a market share of approximately 44% in 2026, driven by continuous fleet expansions, replacement of older aircraft, and the introduction of next-generation fuel-efficient models.

Airlines prioritize operational reliability, reduced maintenance costs, and compliance with environmental regulations, sustaining consistent demand. Established supply chains and long-term procurement cycles further reinforce their market dominance.

UAVs and drones are likely to be the fastest-growing segment during the 2026 - 2033 forecast period, fueled by increasing defense budgets and broader adoption across commercial applications such as surveillance, inspection, and logistics.

Technological advancements in autonomous navigation, lightweight materials, and flight control systems enhance operational efficiency and mission versatility. Strong growth prospects in 2026 are supported by expanding regulatory approvals and rising investment in unmanned solutions across military and commercial sectors.

Regional Insights

North America Aircraft Flight Control System Market Trends

North America is projected to hold an estimated 36% of the aircraft flight control system market share in 2026, rooted in the concentration of aerospace and defense manufacturing capabilities in the region. The deeply entrenched operations of global aircraft OEM giants such as Boeing, Lockheed Martin, and Northrop Grumman are ensuring a steady demand for advanced control systems across commercial, military, and unmanned platforms.

The Federal Aviation Administration (FAA) estimates that the U.S. commercial aircraft fleet alone numbered about 7,387 aircraft in 2024, with a forecast rise to 10,607 by 2045, highlighting the scale of operations supporting sustained demand.

A robust supplier ecosystem for actuators, sensors, and digital control units enables rapid integration of next-generation technologies, including fly-by-wire systems, adaptive control algorithms, and autonomous navigation modules

The dominance of North is further reinforced by high defense spending, enabling acquisition of sophisticated military aircraft and unmanned aerial platforms equipped with advanced control systems. Commercial aviation’s emphasis on fleet modernization and fuel-efficient aircraft enhances adoption rates.

Mature regulatory frameworks, streamlined certification processes, and access to high-precision component suppliers strengthen operational efficiency, ensuring North America remains a leading hub for the development, production, and deployment of advanced aircraft control solutions.

Europe Aircraft Flight Control System Market Trends

Europe maintains a strong position in the aircraft control space, driven by established aerospace hubs in countries such as France, Germany, and the United Kingdom.

Leading manufacturers such as Airbus, Rolls-Royce, and Leonardo ensure consistent demand for advanced control systems across commercial, military, and unmanned platforms. A mature supplier ecosystem supports integration of actuators, sensors, and digital control units, enabling adoption of fly-by-wire systems, adaptive algorithms, and autonomous navigation modules.

Regional prominence is reinforced by extensive research and development infrastructure, government-supported aerospace programs, and stringent regulatory frameworks through bodies such as the European Union Aviation Safety Agency (EASA).

Fleet modernization initiatives, including new fuel-efficient commercial aircraft and advanced military platforms, create steady procurement cycles. Europe’s focus on technological innovation, combined with a skilled workforce and high-precision component supply chains, ensures operational efficiency and positions the region as a key contributor to the development, production, and deployment of next-generation aircraft control solutions.

Asia Pacific Aircraft Flight Control System Market Trends

Asia Pacific is anticipated to be the fastest-growing regional market for aircraft flight control systems between 2026 and 2033, owing to the the rapid expansion of both commercial and defense aviation sectors.

Countries such as China, India, Japan, and South Korea are investing heavily in fleet modernization, indigenous aircraft production, and unmanned aerial platforms. Increasing air traffic demand and government-supported aerospace programs are fueling the procurement of advanced control systems, including digital actuators, sensors, and fly-by-wire technologies.

The growth trajectory is further accelerated by the adoption of newer aircraft models emphasizing fuel efficiency, automation, and safety. Emerging aerospace supply chains and investments in research and development enhance regional manufacturing capabilities, allowing local integration of adaptive control algorithms and autonomous navigation modules.

Expanding regulatory frameworks for civil and military aviation, along with rising defense budgets, reinforce long-term market potential. The strategic focus of market players in Asia Pacific on modern aviation infrastructure and technological adoption positions the region as a hub for future growth in aircraft control solutions.

Competitive Landscape

The global aircraft flight control system market structure is moderately consolidated, where a restricted group of established manufacturers commands substantial market positions across OEM and aftermarket service channels.

These market leaders distinguish themselves through continuous technological advancement, robust certification processes, and demonstrated system dependability, delivering consistent performance and safety outcomes across commercial aviation, military operations, and unmanned aerial platforms.

The competitive landscape reflects a clear bifurcation between specialized component suppliers and diversified aerospace enterprises, with focused suppliers commanding actuator, sensor, and cockpit control segments while integrated aerospace firms dominate complete system integration and delivery.

The competitive positioning of key players increasingly centers on electrification initiatives reduce reliance on hydraulic systems, digitalization enhances monitoring and diagnostics, and lightweight engineering minimizes aircraft weight while preserving structural integrity.

This strategic direction directly supports emerging aircraft architectures and next-generation platform requirements. Companies that excel across this domain are likely to position themselves as preferred partners for OEMs and fleet operators seeking modern control solutions.

Key Industry Developments

- In June 2025, Applied Aerospace secured a contract from De Havilland Canada to produce critical flight control surfaces such as ailerons, flaps, and elevators for the DHC-515 firefighting aircraft. The DHC-515, an advanced twin-engine amphibious platform, scoops over 6,000 liters of water in 12 seconds and builds on the CL-415 legacy with upgraded avionics and corrosion resistance.

- In June 2025, Collins Aerospace set up an expanded production line for electric thrust reverser actuation systems (elecTRAS) in the U.K. and France. ElecTRAS cuts aircraft weight by 15-20%, boosts fuel efficiency, simplifies maintenance by eliminating hydraulics, and powers over 600 Airbus A350s with 11 million flight hours. Future targets include A350 freighters and next-gen platforms via wing actuators and anti-icing electrification.

- In June 2025, Regal Rexnord Aerospace Solutions launched electro-mechanical actuator (EMA) subsystems for aerospace and defense, integrating motors, bearings, screws, and seals from its brands for high reliability in extreme conditions. These solutions accelerate the shift from hydraulics, simplify supply chains, cut weight, and target advanced air mobility and electric vertical takeoff and landing (eVTOL) platforms.

Companies Covered in Aircraft Flight Control System Market

- Honeywell International Inc.

- BAE Systems plc

- Safran S.A.

- Parker Hannifin Corporation

- Moog Inc.

- Collins Aerospace

- Liebherr-Aerospace

- Rolls-Royce Controls and Data Services

- Thales Group

- Curtiss-Wright Corporation

- Leonardo S.p.A.

- Mitsubishi Heavy Industries

- Embraer S.A.

- Hindustan Aeronautics Limited

Frequently Asked Questions

The global aircraft flight control system market is projected to reach US$ 21.6 billion in 2026.

Rising demand for advanced, reliable, and automated flight control solutions across commercial, military, and unmanned aircraft is driving the market.

The market is poised to witness a CAGR of 11.3% from 2026 to 2033.

Rapid adoption of UAVs and drones, fleet modernization, and integration of digital and autonomous flight technologies present key market opportunities.

Some of the key market players include Honeywell International Inc., BAE Systems plc, Safran S.A., Parker Hannifin Corporation, Moog Inc., and Collins Aerospace.