- Automotive Components & Materials

- Light Vehicle (LV) Cabin AC Filters Market

Light Vehicle (LV) Cabin AC Filters Market Size, Share, and Growth Forecast 2026 - 2033

Light Vehicle (LV) Cabin AC Filters by Filter Type (Particulate Filters, HEPA Filters, Activated Carbon Filters, Electrostatic Filters, Nano-fiber / Advanced Composite Filters, Specialty Filters), by Vehicle Type (Passenger Cars, Hatchbacks, Sedans, SUVs & Crossovers, Luxury Cars, Light Commercial Vehicles), Sales Channel (OEM, Aftermarket), End-user (Individual Vehicle Owners, Commercial Fleets, OEM / Fleet Operators), by Regional Analysis, 2026-2033

Light Vehicle (LV) Cabin AC Filters Market Size and Trend Analysis

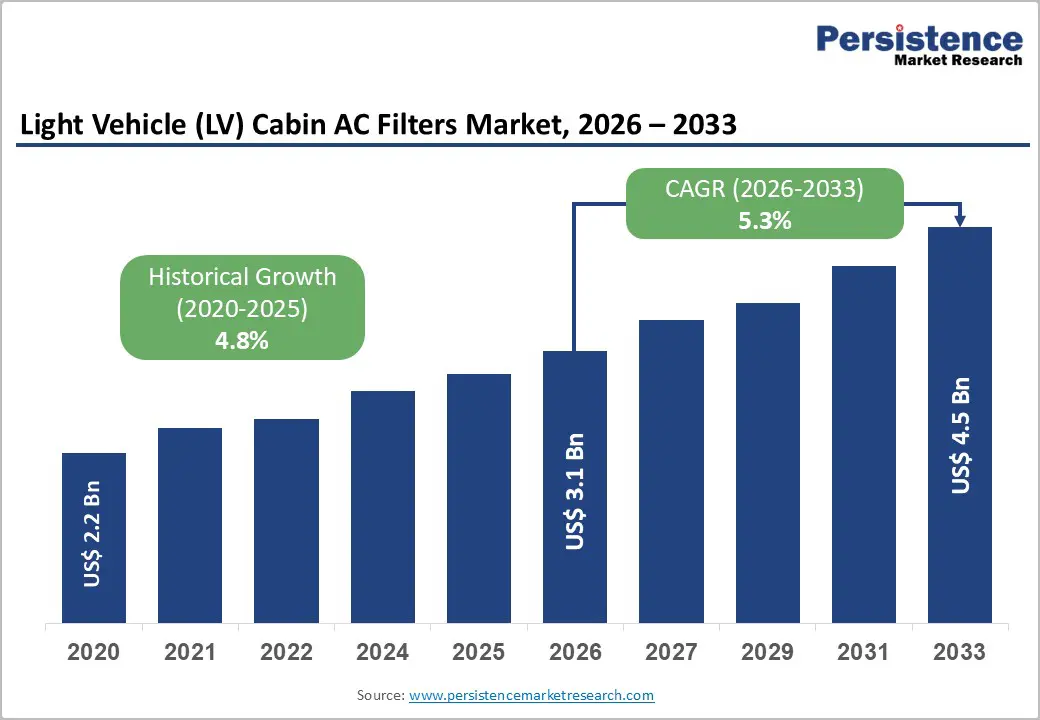

The global Light Vehicle (LV) Cabin AC Filters market size is likely to be valued at US$ 3.1 billion in 2026 and is expected to reach US$ 4.5 billion by 2033, growing at a CAGR of 5.3% during the forecast period from 2026 to 2033.

Key Industry Highlights:

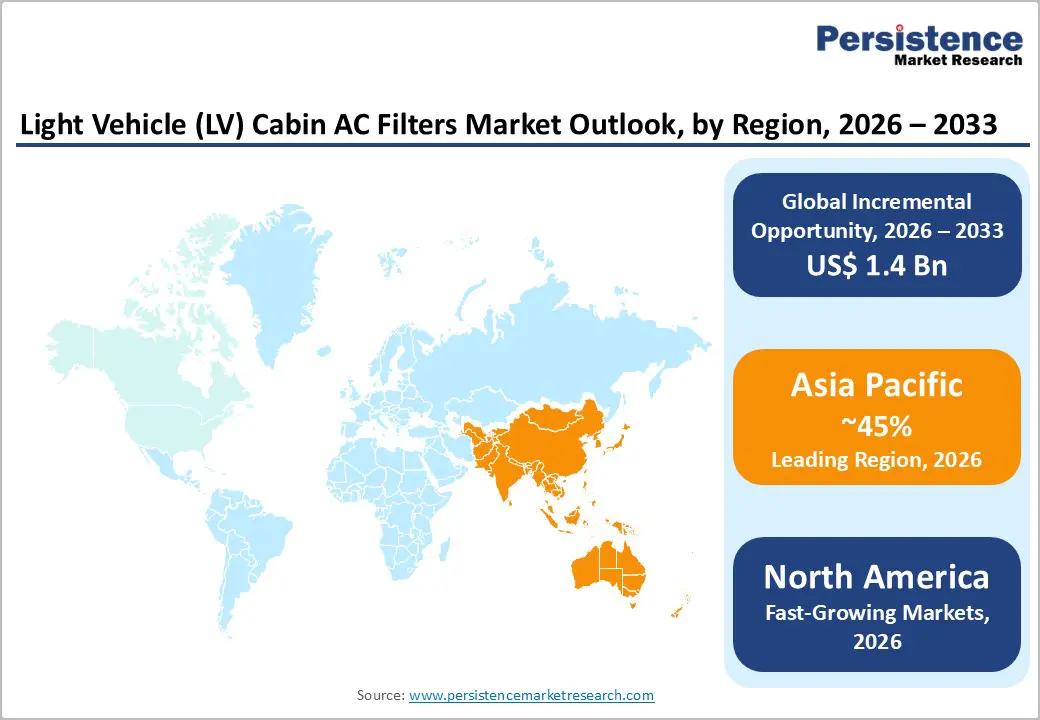

- Leading Region: Asia Pacific commands approximately 45% global light vehicle cabin AC filter market share with 6.29% CAGR, driven by China's exceptional vehicle production volume exceeding 28 million units annually and India's extraordinary 16.8% CAGR growth supported by rapid urbanization and rising health consciousness.

- Fastest growing Region: North America maintains a strong, established market position supported by stringent EPA and California regulatory requirements, high consumer health consciousness, and widespread SUV production driving demand for advanced cabin filtration systems across diverse vehicle segments.

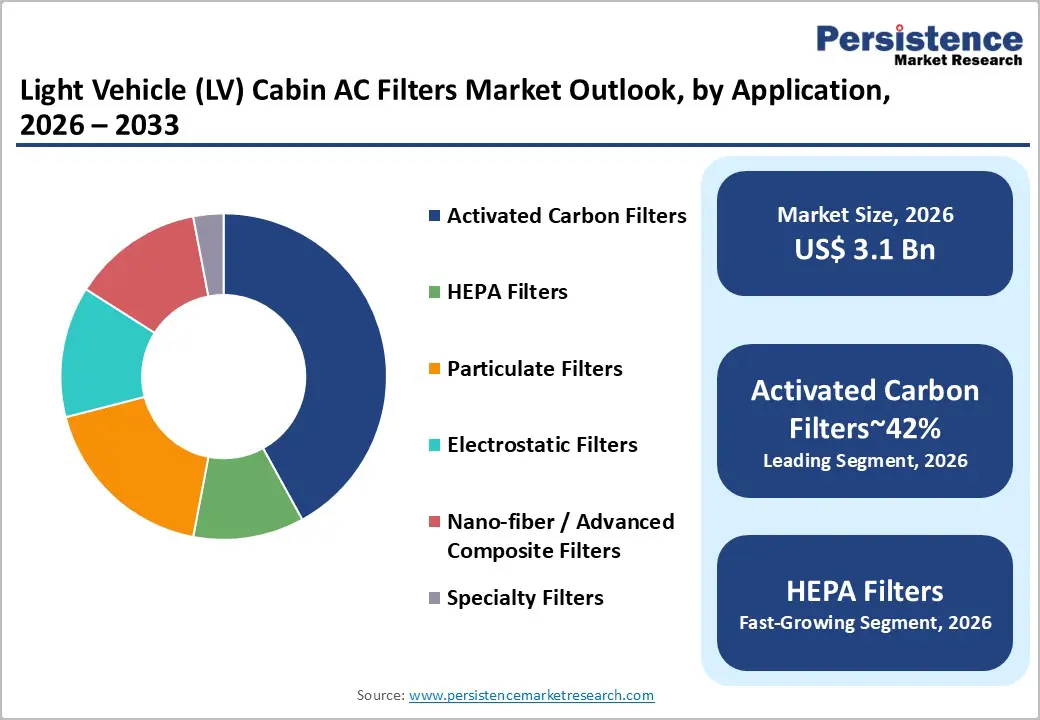

- Leading Segment: Activated carbon filters command approximately 42% market share, driven by superior capabilities removing 95% of harmful gases, odors, and volatile organic compounds from cabin air, making them particularly valuable in urban environments with chronic air pollution.

- Fastest Growing Segment: HEPA filter segment experiences fastest growth at 7.2% CAGR, enabled by Tesla's premium positioning and post-COVID health consciousness, with systems capturing particles as small as 0.3 microns with 99.97% effectiveness supporting premium vehicle adoption.

- Key Opportunity: OEM channels command 65% market share supported by mandatory regulatory compliance and manufacturer quality control, while aftermarket channels expand rapidly at 6%+ CAGR driven by consumer awareness, e-commerce accessibility, and recurring replacement demand cycles.

| Key Insights | Details |

|---|---|

| Light Vehicle (LV) Cabin AC Filters Market Size (2026E) | US$ 3.1 Billion |

| Market Value Forecast (2033F) | US$ 4.5 Billion |

| Projected Growth CAGR (2026-2033) | 5.3% |

| Historical Market Growth (2020-2025) | 4.8% |

Market Dynamics

Drivers - Accelerating Electric Vehicle Adoption with Premium Cabin Air Quality Features

The rapid adoption of electric vehicles (EVs) is significantly increasing demand for advanced cabin air filtration systems, as automakers use air quality features to differentiate premium models. Leading manufacturers are focusing on occupant health and comfort by integrating high-performance filtration technologies. Tesla’s “Bioweapon Defense Mode,” equipped with HEPA filtration in Model Y and Model X, has demonstrated strong consumer appeal by rapidly reducing extremely high particulate matter levels to near zero within minutes.

EV manufacturers are increasingly adopting multi-layer filtration systems that combine barrier layers, electrostatic attraction, activated carbon, and HEPA media to remove dust, pollen, bacteria, and harmful gases. Electric vehicle architectures offer greater design flexibility, allowing installation of larger and more efficient filters compared to traditional internal combustion vehicles. Premium EV pricing enables manufacturers to include advanced filtration as standard features, strengthening brand differentiation and positioning vehicles around wellness, safety, and superior cabin comfort.

Regulatory Mandates and Government Emission Standards Driving Advanced Filtration Integration

Government regulations across major automotive markets are increasingly mandating advanced cabin air filtration systems to support environmental goals and protect occupant health. Regulatory frameworks are shifting from focusing solely on tailpipe emissions to addressing in-cabin air quality. The European Union’s Euro 7 standards, expected to be implemented by 2025, require improved cabin air monitoring and filtration in new vehicles.

China’s National VI emission standards, fully enforced since 2021, include specific guidelines for managing in-vehicle air quality, contributing to significant reductions in particulate emissions. In North America, programs such as California’s Advanced Clean Cars initiative and ongoing amendments by the U.S. Environmental Protection Agency continue to tighten emission and air quality requirements. These policies indirectly drive the adoption of advanced cabin filters. Regulatory compliance creates consistent, long-term demand for high-quality filtration systems, ensuring stable market growth regardless of broader economic cycles.

Restraints -Fragmented Consumer Awareness and Limited Understanding of Filter Replacement Requirements

Limited consumer awareness regarding cabin air filter functionality and replacement schedules remains a key barrier to market growth, particularly in emerging regions. Many vehicle owners are unaware that cabin air filters typically require replacement every 12,000–15,000 miles or within 12–18 months to maintain effectiveness. As a result, filters are often under-replaced, reducing their ability to protect occupants from pollutants over the vehicle’s lifespan.

The absence of standardized labeling and performance ratings across aftermarket products creates confusion among consumers when choosing between basic particulate filters, activated carbon filters, and advanced HEPA systems. Differences in filtration performance are not always clearly communicated. Educational initiatives by vehicle service centers, OEMs, and filter manufacturers remain limited in several markets. This lack of awareness restricts wider adoption and prevents the market from fully capturing health-conscious but uninformed consumer segments.

High Cost of Advanced Filtration Technologies and Installation Complexity

The relatively high cost of advanced cabin air filtration systems presents a significant challenge, particularly for price-sensitive consumers and budget vehicle segments. Premium filtration solutions, such as HEPA filters and advanced activated carbon composites, are typically priced 30–50% higher than standard particulate filters. This price gap limits adoption, especially in entry-level vehicles.

HEPA filters often require specialized housings and professional installation, increasing complexity for aftermarket retrofits. These requirements raise total ownership costs and discourage widespread replacement outside OEM installations. Ongoing maintenance further adds to expenses, as advanced filters require regular replacement to maintain performance. For commercial fleet operators and individual owners alike, recurring replacement costs can impact long-term affordability. While the performance benefits are clear, cost considerations continue to restrict adoption across mass-market vehicles and emerging economies where affordability remains a primary purchasing factor.

Opportunity - Washable and Reusable Filter Technology Expansion across Commercial Fleet Operators

Washable and reusable cabin air filters present a strong growth opportunity, particularly among commercial fleet operators seeking cost efficiency and sustainability. These filters reduce long-term replacement expenses while maintaining effective air filtration performance. In January 2024, K&N Engineering, Inc. introduced washable cabin air filters for light commercial vehicles, offering service life exceeding 50,000 miles with consistent filtration efficiency. Fleet operators increasingly prioritize driver health and comfort to improve productivity, safety, and employee retention. Durable filtration solutions align well with these objectives.

Reusable filters also support environmental sustainability by reducing waste and dependence on disposable products, helping fleets meet corporate sustainability and ESG targets. As operating costs and environmental accountability become more important, fleet managers are showing increased willingness to invest in premium, reusable filtration technologies. This shift supports long-term market expansion while encouraging innovation in durable and environmentally responsible cabin air filtration solutions.

Sensor-Integrated Smart Filtration Systems and Real-Time Air Quality Monitoring

Smart cabin air filtration systems equipped with sensors and real-time air quality monitoring represent a rapidly emerging market opportunity. These systems provide transparency by continuously measuring particulate matter, volatile organic compounds, and odor levels inside the vehicle. Integrated sensors can notify drivers when filters require replacement and automatically adjust airflow to maintain optimal cabin conditions. This reduces reliance on manual maintenance schedules and improves overall system efficiency.

Smart filtration systems also enable data collection related to driving environments and pollution exposure, supporting predictive maintenance and enhanced vehicle health management. Smartphone connectivity and in-vehicle displays further improve user experience by providing real-time insights into air quality. Automakers adopting sensor-based filtration systems strengthen their positioning as technology leaders focused on occupant wellness. This opportunity is especially strong in premium vehicle segments, where consumers are more willing to pay for advanced, health-focused technology features.

Category-wise Analysis

Filter Type Insights

Activated carbon filters currently hold approximately 42% of the market, driven by their superior ability to remove odors, volatile organic compounds, and harmful gases that basic particulate filters cannot effectively address. These filters are particularly valuable in urban environments where air pollution levels remain consistently high. According to industry sources, activated carbon filters can eliminate up to 95% of hazardous gases and odors, making them a preferred choice among consumers seeking improved cabin comfort.

HEPA filters represent the fastest-growing segment, expanding at a CAGR of 7.2%, supported by rising health awareness, premium vehicle adoption, and stricter regulations. HEPA technology captures 99.97% of particles as small as 0.3 microns, offering significantly higher protection than conventional filters. Electrostatic filters remain a niche segment, appealing to environmentally conscious consumers due to their washable and reusable design, which supports long-term cost savings.

Vehicle Type Insights

Passenger cars account for approximately 40% of total market share, supported by high global production volumes and growing consumer interest in comfort and health-oriented vehicle features. Demand for advanced cabin air filtration is steadily increasing across passenger vehicles, particularly in urban markets. SUVs and crossovers are the fastest-growing segment, benefiting from consumer preference for larger vehicles with premium interior features, including enhanced filtration systems as standard equipment.

Mid-sized passenger cars dominated the market in 2024 due to their broad affordability and availability across regions. Light commercial vehicles are experiencing strong growth driven by the expansion of e-commerce and last-mile delivery services. Fleet operators are increasingly focused on improving driver comfort and health to enhance productivity and retention. This trend is driving greater adoption of high-quality cabin air filters in commercial vehicle fleets, supporting sustained growth across multiple vehicle categories.

Sales Channel Insights

OEM channels dominate the market with approximately 65% share, as automakers prioritize factory-installed cabin air filtration systems to ensure consistent quality, system compatibility, and warranty compliance. Growth in this segment is supported by increasing vehicle production volumes and regulatory requirements mandating enhanced cabin air quality management. As a result, manufacturers are integrating advanced filtration systems as standard features across more vehicle models.

The aftermarket segment holds approximately 38% share and continues to grow steadily. Increased consumer awareness of health benefits and replacement requirements is driving aftermarket demand. The expansion of e-commerce platforms and digital automotive marketplaces has improved access to replacement filters, making purchasing more convenient. Professional service centers and quick-service chains are actively promoting cabin filter replacement as part of routine vehicle maintenance, supporting recurring demand and stable revenue growth within the aftermarket channel.

End-user Insights

Individual vehicle owners represent the largest end-user segment, driven by increasing awareness of the health risks associated with prolonged exposure to polluted cabin air. Consumers are placing greater emphasis on comfort, wellness, and protection from airborne contaminants, supporting demand for higher-quality filtration solutions. Commercial fleet operators are emerging as an important growth segment, as companies prioritize driver well-being to improve retention, productivity, and overall operational efficiency.

Fleet managers increasingly view cabin air filtration as a strategic investment rather than a maintenance expense. OEMs and fleet operators are integrating filtration systems into broader vehicle specifications and fleet management strategies, aligning purchasing decisions with regulatory compliance and brand positioning. As awareness grows across both private and commercial users, demand for reliable and high-performance cabin air filtration systems is expected to remain strong across diverse vehicle ownership models.

Regional Insights

North America Light Vehicle (LV) Cabin AC Filters Market Trends

North America holds a significant share of the global cabin air filter market, supported by a well-developed automotive industry, strict air quality regulations, and high consumer health awareness. The United States is experiencing strong growth driven by increasing SUV production and rising demand for premium cabin comfort features. Regulatory initiatives such as California’s Advanced Clean Cars Program and updates to the Clean Air Act continue to push automakers toward advanced filtration integration.

Canada’s market growth is influenced by extreme climate conditions and seasonal air quality challenges, including wildfire-related smoke exposure. These factors increase demand for activated carbon filters capable of removing fine particles and chemical pollutants. North American consumers show a strong willingness to invest in premium filtration solutions, supporting HEPA filter adoption in higher-end vehicles. Innovation and wellness-focused marketing remain key drivers shaping regional market expansion.

Europe Light Vehicle (LV) Cabin AC Filters Market Trends

Europe’s cabin air filter market is driven by strong emphasis on environmental sustainability, regulatory compliance, and occupant health. Automotive manufacturers across the region increasingly focus on recyclable materials and biodegradable filter components to align with circular economy goals. Countries such as Germany, the United Kingdom, France, and Spain play a major role due to their established automotive manufacturing bases and strong presence in premium vehicle segments.

Demand for advanced HEPA and activated carbon filters remains high, supported by consumer expectations for superior cabin comfort. The upcoming Euro 7 regulations will require mandatory cabin air quality monitoring and enhanced filtration across all new vehicles, driving uniform adoption throughout the region. European automakers actively collaborate with filter suppliers to develop customized solutions addressing regional pollution challenges. Strong consumer focus on sustainability and health supports premium pricing and continued innovation in filtration technologies.

Asia Pacific Light Vehicle (LV) Cabin AC Filters Market Trends

Asia Pacific dominates the global cabin air filter market with approximately 45% market share and growth exceeding 6.29% CAGR. Rapid vehicle production expansion, rising vehicle ownership, and severe urban air pollution are key drivers. China leads the region with over 28 million vehicle sales in 2024, creating substantial demand for reliable cabin filtration systems. The country’s National VI emission standards mandate cabin air quality management, supporting widespread adoption of advanced filters.

India is experiencing exceptional growth, with the cabin air filter segment expanding at a CAGR of 16.8%, driven by rising incomes and increasing awareness of pollution-related health risks. Japan remains a leader in filtration innovation, focusing on advanced materials and premium applications. Southeast Asia’s rapid urbanization and worsening air quality further boost demand for effective cabin air filtration across developing automotive markets.

Competitive Landscape

The global light vehicle cabin AC filter market is moderately consolidated, with leadership concentrated among the major global manufacturers. Companies such as Robert Bosch GmbH, MAHLE GmbH, Mann+Hummel GmbH, Denso Corporation, and Sogefi SpA collectively account for approximately 40% of global market share. Their dominance is supported by strong OEM relationships, broad product portfolios, and established brand credibility. Additional players, including Valeo SA, Donaldson Company, Inc., Freudenberg & Co. KG, and K&N Engineering, Inc., contribute another 25% through specialized technologies and regional strengths.

Competitive differentiation focuses on HEPA filtration performance, advanced activated carbon formulations, nanofiber materials, and washable filter innovations. Leading manufacturers continue to invest heavily in research and development to improve filtration efficiency, sustainability, and system integration, ensuring ongoing innovation and competitive advantage in a growing global market.

Key Developments:

- In January 2024, K&N Engineering, Inc. launched washable cabin air filters for light commercial vehicles, offering over 50,000 miles of service life. The solution reduces replacement costs, minimizes waste, and supports fleet sustainability and long-term operational efficiency.

- In January 2024, Robert Bosch GmbH and MAHLE GmbH expanded ISO 29463-3 certified HEPA cabin filters with 99.97% efficiency at 0.3 microns, strengthening premium OEM offerings and supporting growing demand for high-performance aftermarket air quality upgrades.

- In December 2023, Freudenberg & Co. KG introduced biodegradable cabin air filter media using sustainable materials without compromising filtration efficiency, aligning with OEM sustainability goals and increasing consumer demand for environmentally responsible automotive components.

Companies Covered in Light Vehicle (LV) Cabin AC Filters Market

- Robert Bosch GmbH

- MAHLE GmbH

- Denso Corporation

- Sogefi SpA

- Valeo SA

- Donaldson Company, Inc.

- ACDelco

- Mann+Hummel GmbH

- K&N Engineering, Inc.

- Hengst SE & Co. KG

- ALCO Filters Ltd.

- EuroGIELLE S.r.l.

- Airmatic Filterbau GmbH

Frequently Asked Questions

The global light vehicle cabin AC filter market is projected to reach US$ 4.5 billion by 2033, growing at a 5.3% CAGR from 2026.

Demand is driven by EV premium positioning, rising health and air quality awareness, and strict global regulatory mandates requiring advanced cabin filtration.

Activated carbon filters lead with about 42% market share, while HEPA filters are the fastest-growing segment due to superior filtration efficiency.

Asia Pacific leads the global market, driven by high vehicle production in China, rapid growth in India, and severe urban air pollution.

Major opportunities include washable and reusable filters for fleets and sensor-based smart filtration systems offering real-time air quality monitoring.