- Non-food Packaging

- Label Converting Equipment Market

Label Converting Equipment Market Size, Share, and Growth Forecast, 2026 - 2033

Label Converting Equipment Market by Application (Food & Beverages, Pharmaceutical, Personal Care, Industrial), Technology (Digital, Flexographic, Offset, Others), End-user (Label Manufacturers, Packaging Companies, Others), and Regional Analysis for 2026-2033

Label Converting Equipment Market Share and Trends Analysis

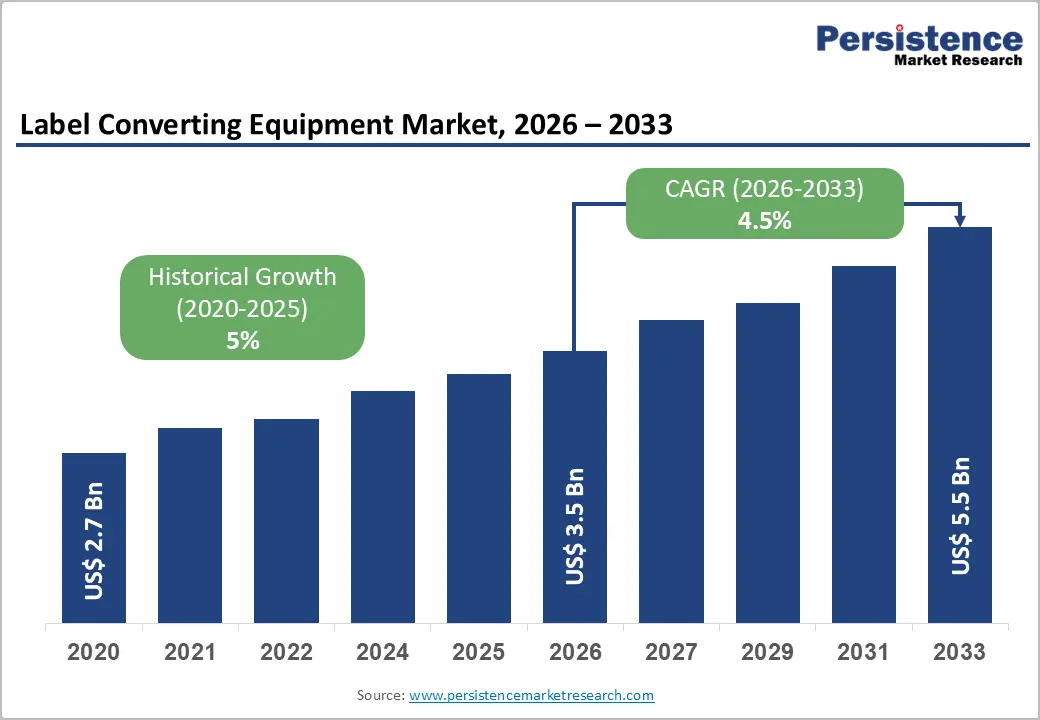

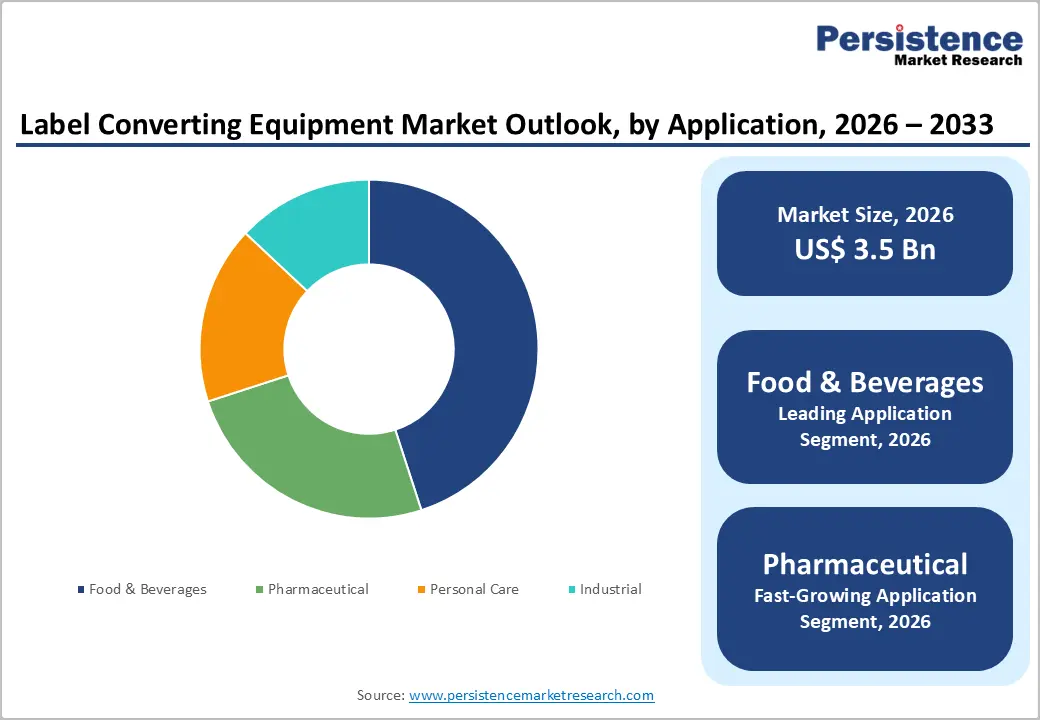

The global label converting equipment market size is likely to be valued at US$ 3.5 billion in 2026, and is projected to reach US$ 5.5 billion by 2033, growing at a CAGR of 4.5% during the forecast period 2026−2033.

The expansion of the market is primarily driven by the accelerating shift toward short-run, on-demand label production across the food & beverage, pharmaceuticals, and logistics sectors. Rapid adoption of digital printing technologies, particularly UV inkjet and laser-based systems, is enabling converters to reduce setup times and material waste, while meeting increasingly complex variable-data and regulatory labeling requirements. Simultaneously, heightened regulatory mandates for track-and-trace serialization in pharmaceutical packaging and sustainability-linked procurement by major consumer goods brands are compelling label manufacturers to upgrade production infrastructure.

Key Industry Highlights

- Technology Leadership: Flexographic is expected to capture approximately 48% revenue share in 2026, and digital technologies are likely to register the fastest growth over the 2026-2033 forecast period.

- Application Dynamics: Food & beverages are set to dominate with about 36% revenue share in 2026, while pharmaceutical is likely to be the fastest-growing segment through 2033.

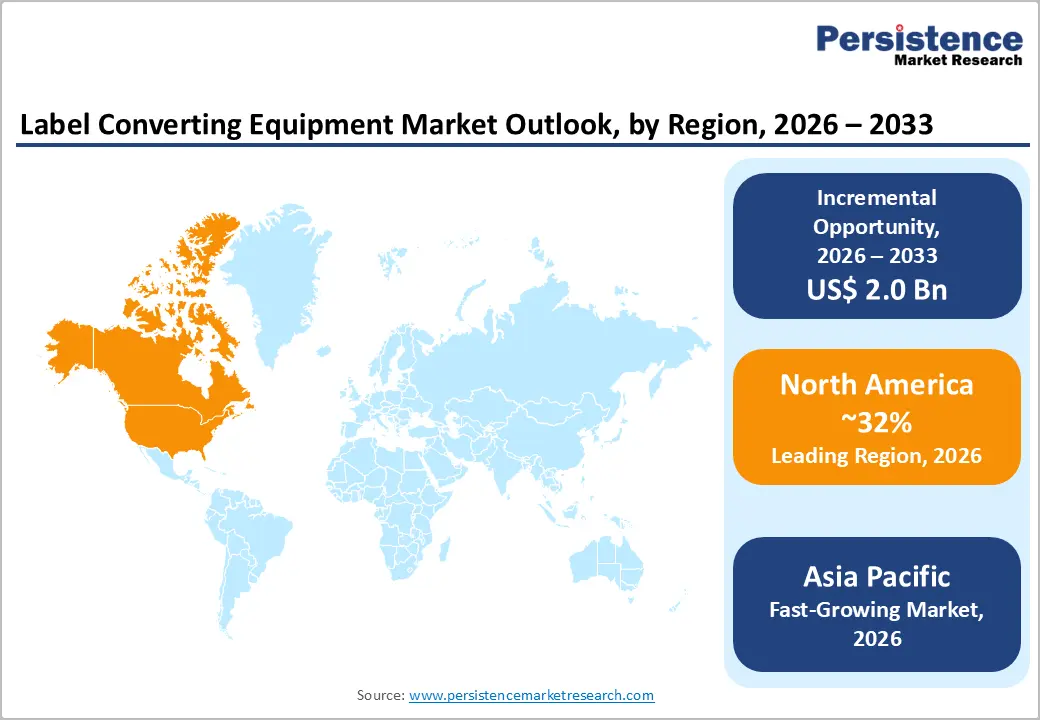

- Dominant Region: North America is anticipated to hold around 32% market share in 2026, owing to its advanced technological infrastructure and strong emphasis on innovation.

- Fastest-growing Market: The Asia Pacific market set to be the fastest-growing during 2026-2033, on account of rapid industrialization and urbanization in China and India.

| Report Attribute | Details |

|---|---|

|

Label Converting Equipment Market Size (2026E) |

US$ 3.5 Bn |

|

Market Value Forecast (2033F) |

US$ 5.5 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

4.5% |

|

Historical Market Growth (CAGR 2020 to 2025) |

5% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Rising Demand for Short-Run & On-Demand Label Production

Brands are prioritizing personalization strategies, seasonal marketing campaigns, and compliance with region-specific regulatory labeling standards, which is accelerating the proliferation of stock-keeping unit (SKU) variations across product portfolios. This expansion is reshaping the cost structure and operational dynamics of label production because shorter print runs are becoming more prevalent in developed markets. Industry bodies such as the Flexible Packaging Association (FPA) are indicating that short-run orders are now representing a substantial share of total label demand, particularly within fast-moving consumer goods (FMCG) segments where rapid product turnover is essential.

Digital label converting technologies are enabling manufacturers to reduce minimum order quantities, compress production lead times, and accelerate product launches, strengthening responsiveness to market trends.

Organizations such as the European Label Forum (ELF) are observing that digital press installations are expanding, reinforcing long-term investment in advanced converting infrastructure across global markets. Companies are benefiting from improved production flexibility, reduced material waste, and faster turnaround times, which collectively enhance operational efficiency and profitability. Equipment manufacturers are simultaneously innovating to incorporate automation, intelligent quality control systems, and modular configurations that improve scalability for converters of varying sizes.

Early adopters of digital converting solutions will have strengthened their ability to accommodate diverse customer requirements, respond to regulatory changes, and introduce new product variations without significant cost escalation.

Pharmaceutical Track-and-Trace Regulatory Mandates

Pharmaceutical manufacturers are investing heavily in high-precision label converting technologies to generate compliant variable data labels at industrial production volumes while meeting evolving regulatory expectations. Stringent serialization and traceability mandates are driving this transition, particularly under frameworks such as the U.S. Drug Supply Chain Security Act (DSCSA), the European Union (EU) Falsified Medicines Directive (FMD), and oversight requirements from the Central Drugs Standard Control Organisation (CDSCO) in India. These regulations are requiring unique product identification, track-and-trace capability, and secure authentication across supply chains, which is compelling companies to modernize labeling infrastructure. Label converters that are serving pharmaceutical clients are prioritizing ultra-precise print registration, microtext readability, and tamper-evident security features to reduce counterfeiting exposure and ensure patient safety.

Advanced finishing and converting lines are enabling pharmaceutical stakeholders to meet these complex requirements by integrating real-time inspection, automated verification, and digital data encoding capabilities within production workflows. Manufacturers are moving toward full interoperability with serialization ecosystems, which will have improved data accuracy, traceability reliability, and audit readiness across distribution channels. Demand is rising for next-generation machinery that supports high-speed variable printing, inline quality monitoring, and automated rejection of noncompliant units, which is enhancing production efficiency while minimizing recall risks.

Companies are also benefiting from reduced manual intervention, faster batch release cycles, and improved documentation accuracy through automation-driven compliance processes. Adoption of these technologies is allowing firms to future-proof operations against tightening global mandates and increasing scrutiny from regulatory authorities.

Supply Chain Volatility in Precision Components

Label converting equipment manufacturing relies critically on specialized components such as precision servo motors, ultraviolet (UV) curing systems, and high-resolution print heads, many of which are sourced from a concentrated supplier base located primarily in Germany, Japan, and the U.S. This geographic concentration is creating structural supply dependencies that are exposing equipment producers to disruption risks when global events affect semiconductor availability or industrial component production.

Recent supply chain shocks are demonstrating how shortages can significantly extend procurement lead times, which is delaying equipment delivery schedules and disrupting downstream production planning for label converters. In response, companies are actively implementing risk mitigation strategies that include supplier diversification, dual sourcing agreements, and the establishment of strategic inventories for critical subassemblies.

Supply chain volatility is also complicating capital investment decisions, particularly for mid-sized converters that are operating with constrained financial flexibility and limited risk tolerance. Businesses are showing caution in committing large capital expenditures when equipment delivery timelines remain uncertain, which is increasing demand for flexible financing structures such as leasing arrangements and performance-linked payment models.

Forward-looking manufacturers are designing modular equipment architectures that allow component substitution without extensive system redesign, thereby improving adaptability during supply disruptions. This engineering flexibility is reducing downtime risk and supporting long-term operational resilience. Enhanced visibility into global inventory flows and shipment status is also enabling faster decision-making and more accurate forecasting.

High Capital Expenditure and Total Cost of Ownership

Advanced digital label converting systems such as UV inkjet presses equipped with inline finishing modules are requiring significant capital expenditure, which is creating substantial entry barriers for small and mid-sized converters. Organizations are conducting rigorous total cost of ownership (TCO) assessments before committing investment as acquisition expenses are only one component of the financial burden. Digital platforms are often generating higher operating costs than conventional flexographic solutions, particularly when utilization rates remain below optimal thresholds.

Ongoing maintenance requirements, print head servicing, and consumable inputs such as inks and coatings are adding further financial pressure. Converters that are serving high-volume commodity label segments are encountering additional constraints since substrate compatibility limitations can restrict production flexibility across lower-cost materials.

Industry participants are actively exploring alternative financial and operational models to overcome investment constraints and accelerate modernization. Leasing programs, subscription-based equipment access, and pay-per-use structures are distributing capital commitments over extended periods, which is easing liquidity pressure and enabling earlier technology adoption. Shared production facilities and collaborative equipment hubs are emerging as practical solutions that allow smaller converters to utilize advanced systems without assuming full ownership risk.

Companies are simultaneously optimizing workflow design, scheduling efficiency, and job batching strategies to improve equipment utilization and maximize return on investment (ROI). Innovations in energy-efficient hardware architecture, automated calibration systems, and intuitive user interfaces are further reducing operational expenses and simplifying maintenance for internal technical teams.

Printing Technologies and the Increasing Demand for Customized Labels

End-use industries such as food and beverages, pharmaceuticals, and personal care are enhancing production capacity and product diversity, fueling the demand for efficient and adaptable labeling technologies. Brand owners are requiring equipment that can process multiple substrate types, manage intricate graphics, and support complex compliance requirements without compromising throughput. Label converting equipment manufacturers are responding by engineering application-specific machinery that incorporates high-speed processing, precision registration, and variable data printing capabilities to meet sector-specific operational needs. These technological enhancements are enabling converters to address challenges related to traceability, branding differentiation, and rapid product turnover across diverse markets.

The global transition toward environmentally responsible packaging is gaining momentum, as regulatory bodies and consumers are placing greater emphasis on recyclability and biodegradability.

Innovation strategies are also focusing on flexibility and scalability to help converters respond quickly to changing material specifications and market requirements. Equipment providers are differentiating through modular platforms that can accommodate new substrates, adhesive technologies, and finishing techniques without extensive system redesign. This adaptability is enabling rapid production adjustments for seasonal product launches, regional customization, and short-run promotional campaigns.

Investment in research and development (R&D) remains a central priority, with companies collaborating closely with material suppliers to evaluate emerging sustainable substrates during early development stages. These partnerships are ensuring compatibility between new materials and converting processes before commercial deployment, reducing operational risk for customers.

Increasing Adoption of Digitalization and Automation in Label Converting Equipment

Businesses are intensifying efforts to improve operational efficiency and reduce production costs within label converting environments, which is accelerating the integration of digitalization and automation across manufacturing workflows. Equipment manufacturers are responding by developing advanced machinery that incorporates Internet of Things (IoT) connectivity, real-time performance monitoring, and embedded data analytics capabilities to optimize production outcomes. These smart systems are enabling operators to track machine parameters continuously, identify performance deviations, and implement corrective actions with minimal delay.

Integrated sensor networks are detecting mechanical anomalies and process irregularities before they escalate into operational disruptions, while predictive maintenance algorithms are reducing unplanned downtime and extending equipment lifespan.

The deployment of connected equipment is also strengthening data-driven decision-making across production facilities by providing actionable visibility into workflow performance and resource utilization. Production teams are accessing centralized dashboards that highlight bottlenecks, waste patterns, and efficiency gaps, which supports continuous process refinement and quality optimization. Management personnel are generating performance reports that guide strategic planning, capacity allocation, and compliance monitoring, thereby reinforcing adherence to industry standards and regulatory requirements.

Equipment providers are enhancing customer value propositions through seamless integration with enterprise software ecosystems and cloud-based platforms that enable remote diagnostics, firmware updates, and system optimization.

Category-wise Analysis

Application Insights

Food and beverages are anticipated to lead with approximately 36% of the label converting equipment market revenue share in 2026 due to the indispensable role of labels in conveying product information and strengthening brand visibility at the point of sale. Regulatory frameworks are requiring comprehensive disclosure of nutritional values, ingredient composition, allergen warnings, and storage instructions, which is increasing the need for precise and compliant label production.

Advanced converting equipment is enabling manufacturers to generate high-resolution graphics and consistent print quality at scale while maintaining regulatory conformity. Rising global consumption of packaged foods, including convenience-oriented ready-to-eat products, is further accelerating label volume demand across retail channels.

The pharmaceutical sector is projected to register the fastest growth during the 2026-2033 forecast period since labeling functions as a critical component of patient safety, traceability, and regulatory compliance. Medicinal packaging is requiring exact information related to dosage instructions, contraindications, batch identification, and expiration timelines, which necessitates extremely accurate and reliable production processes. Advanced label converting equipment is ensuring these stringent performance standards through precise registration control, variable data printing, and automated inspection capabilities.

Regulatory authorities are continuously tightening pharmaceutical labeling requirements, increasing the demand for sophisticated machinery that can maintain compliance across multiple jurisdictions.

Technology Insights

Flexographic printing is set to dominate in 2026, capturing around 48% of the label covering equipment market share, aided by its operational efficiency, scalability, and compatibility with high-volume label production requirements. This technology is enabling converters to process a wide range of substrates and ink chemistries, which supports applications spanning food packaging, consumer goods, and industrial labeling. Manufacturers are favoring flexographic systems because they provide consistent output quality during extended production runs while maintaining cost efficiency. Continuous technological improvements in plate manufacturing, anilox roller design, and ink formulations are enhancing print resolution and color consistency while reducing material waste and setup time.

Digital printing is projected to register the fastest growth during the 2026 to 2033 forecast period because it is delivering superior customization capability, rapid job changeovers, and shorter production lead times compared with conventional processes. This technology is particularly valuable for short-run orders, variable data printing, and personalized packaging initiatives that are becoming increasingly prevalent across industries such as food and beverages, personal care, and pharmaceuticals.

Businesses are prioritizing agility to respond quickly to shifting consumer preferences, promotional campaigns, and regulatory updates, and digital systems are enabling this responsiveness through software-driven workflow integration.

Regional Insights

North America Label Converting Equipment Market Trends

North America is projected to account for approximately 32% of the label converting equipment market value in 2026, driven by advanced industrial infrastructure, strong technology adoption, and sustained investment in innovation. Companies across the region are prioritizing research and development initiatives to enhance machinery performance, automation capability, and production precision, which is reinforcing competitive leadership. A mature packaging ecosystem is generating consistent demand for modern converting solutions that improve throughput and operational efficiency.

Sustainability objectives are also shaping purchasing decisions, as manufacturers are increasingly adopting equipment designed to process recyclable substrates, reduce material waste, and optimize energy consumption.

Customization requirements and personalization trends are further accelerating market activity across industries such as food and beverages and personal care, where brands are seeking rapid product differentiation and shorter production cycles. Converters are requiring versatile equipment capable of handling short runs, variable designs, and frequent changeovers without compromising quality, which is increasing demand for digitally enabled platforms.

Manufacturers are investing heavily in automation technologies, inline finishing modules, and real-time monitoring systems to streamline workflows and maintain consistent output standards. Strategic collaborations between equipment producers and technology providers are strengthening innovation pipelines and enabling faster deployment of advanced solutions across production facilities.

Europe Label Converting Equipment Market Trends

The Europe market is expected to display robust growth through 2033, as companies across the region are prioritizing production quality, regulatory adherence, and technological precision, particularly within food and pharmaceutical applications. Stringent compliance standards are requiring machinery that delivers accurate print placement, consistent finishing performance, and reliable durability across high-volume operations. Sustainability considerations are significantly influencing purchasing preferences, as businesses are adopting converting solutions that support recyclable substrates, minimize resource consumption, and reduce environmental impact.

Innovations in packaging technology are further stimulating demand for equipment capable of processing water-based inks, lightweight materials, and compact production formats that improve operational efficiency without compromising performance.

The region’s mature packaging ecosystem is actively embracing digitalization and automation to enhance operational transparency and efficiency across converting facilities. Organizations are upgrading to interconnected production environments that incorporate real-time data monitoring, predictive maintenance tools, and process optimization software to reduce downtime and improve output consistency. Europe is strengthening its position as a global hub for sophisticated converting solutions through continuous technological refinement and engineering excellence.

Manufacturers are also pursuing strategic localization initiatives by establishing regional service centers and technical support networks that ensure rapid response times and customer proximity. Customized equipment configurations are addressing country-specific regulatory requirements and production preferences, which is facilitating smoother market adoption.

Asia Pacific Label Converting Equipment Market Trends

Asia Pacific is expected to emerge as the fastest-growing market for label converting equipment between 2026 and 2033, powered by the transformation of production ecosystems across China and India. Accelerating urbanization is increasing demand for packaged consumer goods within metropolitan areas, while a growing middle-income population is consistently seeking premium products with strong brand presentation. These structural shifts are creating immediate requirements for advanced labeling infrastructure that can support higher production volumes and improved quality standards.

Expanding manufacturing sectors across the region are driving investments in packaging capabilities, as companies are recognizing the importance of high-quality labels for brand differentiation and regulatory compliance.

The regional competitive environment is also intensifying as label converters are expanding operations and adopting advanced production technologies to maintain global competitiveness. Digital printing platforms are gaining adoption because they support short-run customization, variable data applications, and rapid product launches that are becoming increasingly common across consumer goods sectors. Automation technologies are streamlining workflows, reducing production lead times, and improving cost efficiency, which is critical for companies operating in price-sensitive markets.

Governments are promoting industrial development through infrastructure investments and policy initiatives that support manufacturing corridors, which is encouraging the establishment of new production facilities.

Competitive Landscape

The global label converting equipment market structure features moderate concentration. Spartanics, ASHE Converting Equipment, Daco Solutions, and Bobst Group control approximately 45% to 52% of total market share. These companies are strengthening competitive positioning by prioritizing continuous technological advancement, strategic partnerships, and mergers and acquisitions (M&A) that expand product portfolios and geographic reach. Competitive intensity is encouraging sustained investment in R&D to address rapidly evolving customer requirements across multiple end-use industries. This strategic emphasis is enabling companies to improve machine performance, automation integration, and application versatility, which supports broader adoption across diverse manufacturing environments.

Industry leaders are also differentiating through the development of advanced machinery that delivers superior efficiency, consistent accuracy, and scalable production capabilities to accommodate both high-volume and short-run applications. These technological improvements are allowing converters to optimize workflows, reduce material waste, and maintain quality standards across complex labeling formats. Companies are also leveraging reliable engineering performance and service support networks to strengthen customer relationships and reinforce long-term loyalty.

Key Industry Developments

- In February 2026, ABG International launched an integrated nonstop unwind system for label converting lines, enabling continuous production without material changeover interruptions to improve efficiency, reduce downtime, and increase throughput for converters handling high-volume jobs.

- In February 2026, Cartes installed the world's first Gemini production line equipped with a dual-bar Jet D-Screen digital embellishment unit at Rotocel-Space, an Italian converter specializing in premium labels for wine, olive oil, spirits, and personal care.

- In April 2025, Domino Printing Sciences unveiled its compact N410 LED digital label press at Labelexpo Europe 2025, designed as a cost-efficient entry platform for converters seeking to expand into digital printing with high-quality CMYK plus white output and energy-efficient UV LED curing technology.

Companies Covered in Label Converting Equipment Market

- Spartanics Ltd.

- ASHE Converting Equipment

- Daco Solutions Ltd

- SMAG Graphique

- Bobst Group SA

- Orthotec Label Machines

- A B Graphic International Ltd

- Prati SRL

- J&J Converting Machinery

- Sohn Manufacturing, Inc.

- Lemorau LDA

- Austik PTY Ltd.

Frequently Asked Questions

The global label converting equipment market is projected to reach US$ 3.5 billion in 2026.

The market is driven by rising demand for automation, regulatory compliance in pharma/food sectors, and e-commerce packaging.

The market is poised to witness a CAGR of 4.5% from 2026 to 2033.

Major opportunities lie in digital/hybrid systems for short-run customization, sustainable labeling solutions, and Asia Pacific manufacturing investments.

Spartanics Ltd., ASHE Converting Equipment, Daco Solutions Ltd and Bobst Group SA are some of the key players in the market.