- Inks, Coatings, Adhesives & Sealants (ICAS)

- Wet Glue Labeling Machine Market

Wet Glue Labeling Machine Market Size, Share, and Growth Forecast, 2026 - 2033

Wet Glue Labeling Machine Market by Glue Type (Water-Based Adhesive, Hot-Melt Adhesive), End-User (Food & Beverages, Pharmaceutical, Cosmetics, Household), Material (Paper, Plastic, Metallized Film), and Regional Analysis for 2026-2033

Wet Glue Labeling Machine Market Share and Trends Analysis

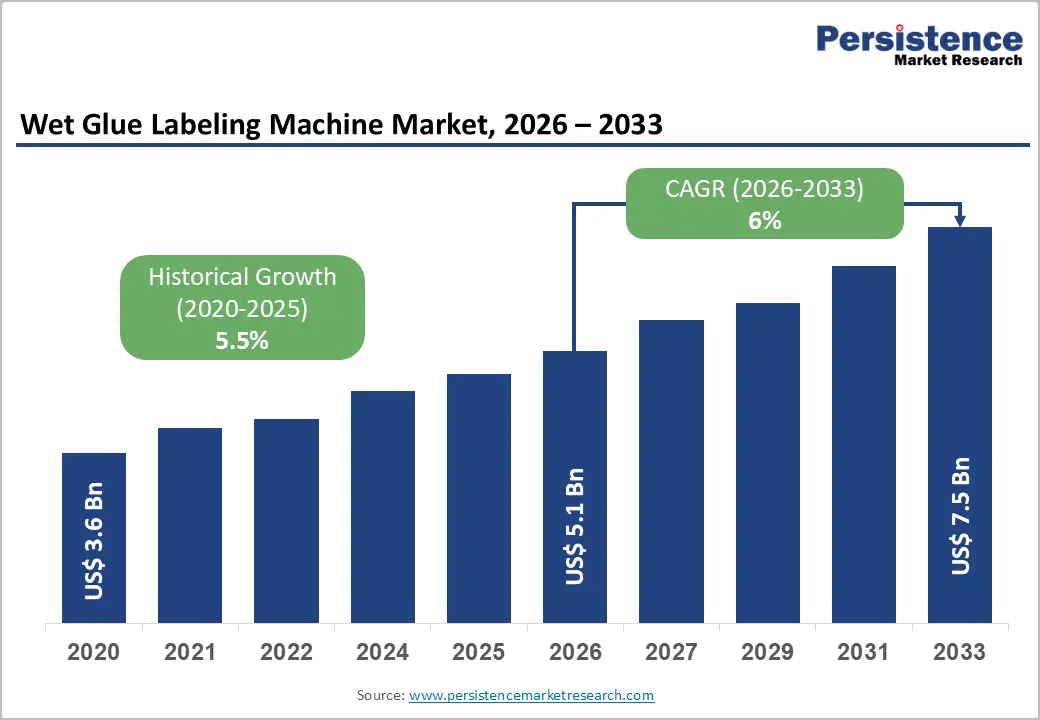

The global wet glue labeling machine market size is likely to be valued at US$ 5.1 billion in 2026, and is projected to reach US$ 7.5 billion by 2033, growing at a CAGR of 6.0% during the forecast period 2026−2033. This robust trajectory is supported by accelerating demand from the food & beverage, pharmaceutical, and personal care industries, all of which rely on high-speed, precision labeling solutions to comply with stringent product traceability regulations. Wet glue labeling, also known as cold glue labeling, remains the preferred technology for glass bottles, returnable containers, and premium product packaging, where label adhesion quality and aesthetic finish are paramount. The compatibility of the technology with paper, metalized foil, and specialty label substrates gives it a durable, competitive position relative to pressure-sensitive and heat-shrink alternatives.

Key Industry Highlights

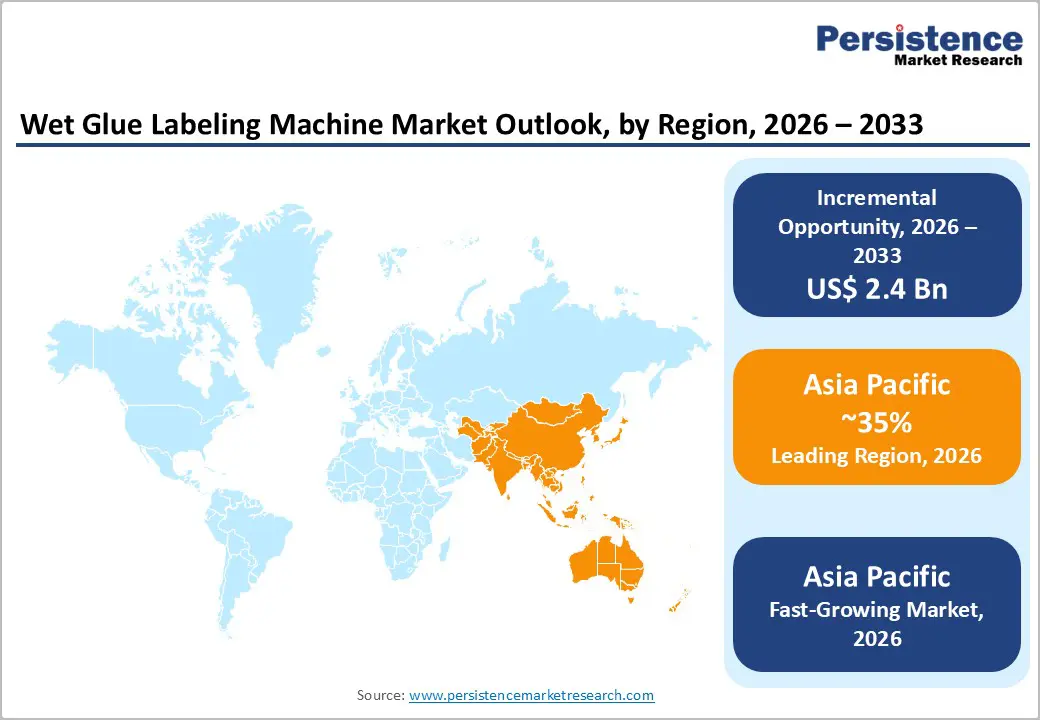

- Dominant Region & Fastest-growing Market: Asia Pacific is likely to dominate and emerge as the fastest-growing market through 2033, holding about 35% market share, driven by large-scale food & beverage manufacturing investments.

- Leading & Fastest-growing Glue Type: Water-based adhesive is likely to lead with approximately 65% revenue share, while hot-melt adhesives are set to grow the fastest during the 2026-2033 forecast period.

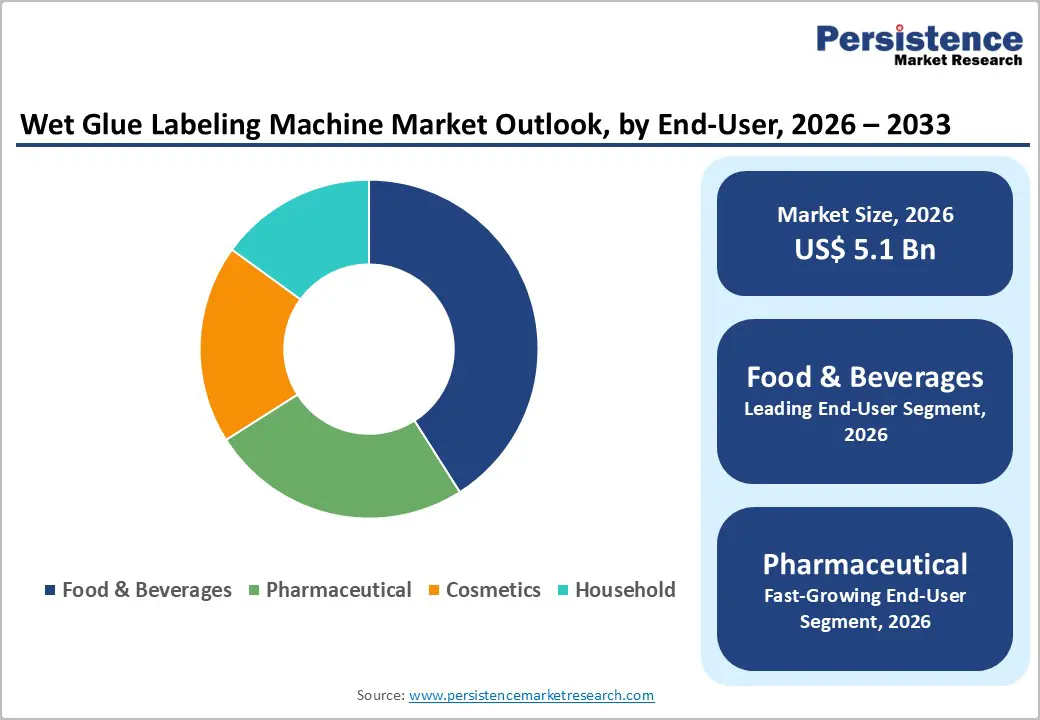

- Leading & Fastest-growing End-User: Food & beverages are poised to capture around 41% revenue share in 2026; pharmaceuticals are expected to be the fastest-growing segment through 2033.

- Market Opportunities: Premium spirits, wines, and craft beers are strengthening the demand for wet glue labeling machines, as brands use high-quality paper and foil labels to signal prestige and authenticity.

| Key Insights | Details |

|---|---|

| Wet Glue Labeling Machine Market Size (2026E) | US$ 5.1 Bn |

| Market Value Forecast (2033F) | US$ 7.5 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.5% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Surging Demand from the Food & Beverage Industry

The food and beverage sector is generating the strongest demand for wet glue labeling machines and is maintaining the largest installation base worldwide. Manufacturers are relying on these systems to sustain high-speed production while ensuring accurate label positioning on bottles and rigid containers. Segments such as premium spirits, wine, and craft beer are continuing to adopt glass packaging because it supports durable bonding with wet adhesive applications. This preference is strengthening the business case for wet glue technologies in both established and emerging markets. Companies are simultaneously upgrading production infrastructure to accommodate rising consumption volumes and product diversification by investing in automation, predictive maintenance, and line integration.

Regulatory oversight is intensifying and is accelerating capital allocation toward advanced labeling capabilities. The U.S. Food and Drug Administration (FDA) enforces compliance under the 21 Code of Federal Regulations (CFR) Part 101, while the Food Safety and Standards Authority of India (FSSAI) implements comparable labeling and disclosure frameworks. These mandates are requiring manufacturers to enhance traceability, accuracy, and readability across product information panels. Each regulatory update is increasing the need for adaptable machinery that supports format changes without disrupting productivity. This progression is strengthening production ecosystems across major economies and is preparing the sector for sustained scalability.

Industry 4.0 Integration and Smart Factory Adoption

Smart factory programs are accelerating investments in advanced manufacturing technologies, and companies are integrating IoT sensors into wet glue labeling machines to enhance visibility across production environments. Machine learning models are identifying defects in real time, while remote diagnostics capabilities are reducing response intervals during equipment disruptions. Manufacturers are targeting improvements in overall equipment effectiveness (OEE) by increasing availability, performance, and quality simultaneously. The transition toward intelligent automation is supporting uninterrupted production continuity in highly competitive markets. Servo-driven configurations are leading modernization efforts as they are enabling instant label position adjustments during operation.

Adoption momentum is rising across industrial economies such as Germany, Japan, and the United States, where labor shortages are encouraging enterprises to implement fully automated solutions. Advanced technology variants are commanding higher acquisition costs than conventional cam-driven alternatives, yet the pricing differential is reflecting measurable gains in reliability, consistency, and throughput efficiency. Equipment manufacturers are expanding revenue opportunities through innovation-driven differentiation, and they are aligning portfolios with Industry 4.0 transformation strategies. End users are gaining operational flexibility to manage diverse packaging formats without compromising speed or accuracy, elevating labeling from a functional necessity to a strategic capability.

Competition from Pressure-Sensitive and Sleeve Labeling Technologies

Pressure-sensitive labeling systems, also referred to as self-adhesive platforms, are dominating the global equipment landscape because they deliver strong versatility across substrates such as plastics and metals. Production teams are switching configurations rapidly between batches, which is supporting shorter changeover intervals and higher line utilization. These technologies are integrating efficiently with digital printing solutions to enable customized graphics and variable data requirements. Wet glue equipment is encountering limitations in flexible packaging applications because non-porous surfaces are reducing adhesive bonding strength during placement. At the same time, shrink-sleeve formats are gaining traction for beverages and personal care products since they provide full wraparound coverage and seamless visual presentation.

Polyethylene terephthalate (PET) bottles are increasingly incorporating label-free or minimal-label finishes to achieve a premium appearance, and consumers are responding positively to this streamlined aesthetic in retail channels. Competing labeling technologies are therefore reducing demand potential for wet glue systems within certain packaging categories. Producers are facing strategic pressure to innovate or concentrate on specialized domains such as glass containers, where wet adhesive applications continue to deliver performance and cost advantages at scale. Industry participants need to refine product offerings before future investment cycles to counter competitive intensity and maintain long-term market relevance.

Machine Set up and Labelling Changeovers

High capital requirements are constraining the uptake of wet glue labeling machines, particularly among cost-sensitive manufacturers. Organizations are incurring substantial expenditures during installation and commissioning because projects require equipment foundations, utility integration, and specialized technical expertise. These financial commitments are creating entry barriers for small and medium enterprises (SMEs), which are often postponing modernization or continuing with manual labeling approaches to preserve liquidity. Operational inefficiencies are also emerging during product transitions, as operators are experiencing extended changeover durations when container dimensions or label specifications vary. Companies that are conducting detailed total cost of ownership (TCO) assessments are recognizing that inefficient transitions can offset the productivity benefits of automation if not addressed strategically.

Sustainability considerations are introducing additional operational complexity, as product diversification is placing pressure on adhesive formulation stability and supply continuity. Raw material shortages are forcing repeated system adjustments, while trial runs and alignment errors are generating excess waste that affects both cost structures and environmental performance indicators. In response, manufacturers are adopting modular architectures and quick-release mechanisms to accelerate format transitions and reduce downtime exposure. Smaller enterprises are exploring leasing arrangements, contract manufacturing partnerships, and shared production facilities to avoid heavy upfront investments while maintaining market participation. Equipment providers are simultaneously developing versatile platforms capable of handling multiple packaging formats, which is improving scalability prospects.

Premiumization of Alcoholic Beverages and Spirits

Premium spirits, wines, and craft beers are generating strong demand for wet glue labeling machines, owing to brands emphasizing packaging quality to communicate authenticity and heritage. Producers are selecting high-grade paper and metallic foil labels that are bonding securely with glass bottles, which remain the dominant container format in upscale beverage categories. Buyers are associating refined finishes with superior product standards, which is encouraging distillers and brewers to invest in dependable equipment that maintains uniformity across production batches. Label integrity during transportation and storage is remaining a critical performance requirement, and consistent application quality is reinforcing brand loyalty in highly competitive retail environments.

The U.S. is also supporting market expansion through a dynamic craft brewery ecosystem, where independent producers are experimenting with distinctive packaging concepts that require accurate labeling execution. Glass packaging formats are aligning well with wet glue technologies for artisanal beverage positioning, which is encouraging companies to modernize production lines to accommodate decorative foils and textured substrates. Automation integration is enabling faster throughput across diverse product runs while maintaining aesthetic precision, thereby improving operational scalability ahead of anticipated demand increases. Strategic capital deployment across high-growth regions is therefore creating sustained revenue opportunities for equipment suppliers while reinforcing long-term market expansion prospects.

Sustainability-Driven Label Substrate Innovation

Regulatory frameworks are pushing companies toward recyclable packaging formats, and policy timelines are accelerating technology transitions across labeling operations. For example, the European Union (EU) Packaging and Packaging Waste Regulation (PPWR) is scheduled to take effect in 2030, while multiple states in the U.S. are implementing extended producer responsibility (EPR) legislation that assigns lifecycle accountability to producers. These requirements are compelling organizations to adopt environmentally compatible materials for both labels and containers. Wet glue systems are aligning effectively with this transition since water-based adhesives decompose efficiently during recycling processes and support glass recovery streams without contamination risks. Manufacturers are therefore gaining compliance advantages compared with alternative labeling approaches while also responding to consumer expectations for sustainable packaging practices in retail environments.

Material innovation is further reinforcing adoption momentum, as recycled-content metallic foils and bio-based adhesive formulations are integrating smoothly into modern wet glue configurations and are improving environmental performance metrics. Producers are offering retrofit kits that enable existing production lines to accommodate sustainable inputs without requiring complete equipment replacement, while original equipment manufacturers (OEMs) are embedding these capabilities into new-generation platforms. Suppliers are securing contracts in tightly regulated regions such as Europe and North America by positioning wet glue labeling as a future-ready solution under evolving compliance standards.

Category-wise Analysis

Glue Type Insights

Water-based adhesives are projected to account for approximately 65% of the wet glue labeling machine market revenue share in 2026. Food and pharmaceutical production facilities are favoring these systems because they provide lower odor emissions, simplified handling, and faster cleanup during sanitation procedures. Precision application components such as roller and palette mechanisms are delivering accurate metering and uniform adhesive films, which are supporting consistent label adhesion across container surfaces. Quick-release assemblies are enabling frequent washdown cycles without extended downtime, an important requirement for hygiene-sensitive environments. These operational refinements are preserving visual quality across multiple packaging formats while ensuring compliance with stringent cleanliness standards.

Hot-melt adhesive technologies are expected to register the fastest growth through 2033, as they deliver performance advantages in high-speed wraparound and neck labeling applications. These configurations are providing rapid initial tack strength that secures glossy labels with minimal dwell time, which is improving line efficiency for demanding production schedules. Manufacturing plants are relying on closed-melt delivery systems to maintain consistent adhesive properties, as these setups are stabilizing temperature control and incorporating anti-char safeguards that preserve material quality during extended operation. Automated refill melters are reducing manual intervention and minimizing downtime associated with replenishment tasks, enhancing workplace safety and cleanliness by limiting spills.

End-User Insights

Food and beverages are anticipated to capture roughly 41% of the revenue share in 2026, driven by stringent hygiene expectations and high production intensity. Food processors are prioritizing sanitary machine architecture, tool-less changeover mechanisms, and washdown-compatible components to support frequent product transitions in dynamic manufacturing environments. Integrated inspection technologies such as vision verification, date coding confirmation, and automated rejection units are strengthening regulatory compliance while reducing rework rates. Beverage production facilities require stable high-speed performance on glass and PET containers, even when surfaces are wet or exposed to condensation. Quick-change star wheels and stored recipe parameters are enabling efficient transitions between container sizes and production volumes, which is improving operational continuity.

Pharmaceuticals are slated to register the highest 2026-2033 CAGR, fueled by a strong demand from manufacturers for validated processes and integrated serialization capabilities to meet evolving regulatory mandates. These systems are ensuring compliance with traceability frameworks by incorporating error-prevention features that reduce the risk of mislabeling during critical production cycles. Labeling platforms are handling folded inserts efficiently while providing visible tamper-evident indicators that enhance patient safety. Material compatibility is receiving strong emphasis to prevent adverse interactions with sensitive substrates, while enhanced cleanability is minimizing cross-contamination risks between product batches. These capabilities are enabling pharmaceutical companies to maintain consistent quality assurance across the supply chain while meeting stringent compliance expectations.

Regional Insights

Asia Pacific Wet Glue Labeling Machine Market Trends

Asia Pacific is forecast to remain both the largest and fastest-growing market in 2026, securing nearly 35% of the wet glue labeling machines market share. Rapid industrialization across manufacturing hubs is sustaining demand for advanced production equipment, while an expanding middle-class population is increasing consumption of packaged products such as beverages and processed foods. Significant capital deployment in the food and beverage sector is accelerating modernization of labeling infrastructure to improve throughput and quality consistency. China is leading regional adoption due to its large-scale beer production capacity and expanding pharmaceutical manufacturing base that serves both domestic demand and export markets. India is emerging as the fastest-growing national market, supported by Production Linked Incentive (PLI) programs that are encouraging local manufacturing expansion and technology upgrades.

Japan and South Korea are emphasizing high-precision equipment to support premium cosmetics and personal care packaging, where visual accuracy and material compatibility are critical differentiators. Market growth in the ASEAN bloc is gaining momentum as foreign direct investment (FDI) inflows are strengthening regional manufacturing ecosystems. Competitive production costs are attracting global fast-moving consumer goods (FMCG) companies to establish or expand operations in these emerging economies, which is increasing demand for adaptable labeling technologies. Equipment suppliers are customizing machines to address varied regulatory frameworks, packaging formats, and operational requirements across countries, thereby improving market penetration and customer retention.

Europe Wet Glue Labeling Machine Market Trends

Europe is poised to become the second-largest regional market for wet glue labeling machines, supported by a strong concentration of premium beverage and specialty food production. Producers of wine, spirits, and artisanal food products are relying extensively on these systems to achieve precise label placement on glass containers, which remain the preferred packaging format in high-value segments. The EU is home to advanced industrial capabilities through well-established supply networks and engineering expertise. Germany is leading regional demand due to its large beer production volumes and diversified chemical sector, while also hosting major OEMs such as Krones AG and KHS GmbH that are driving technological innovation. France and Spain are benefiting from extensive wine production industries that are aligning closely with wet adhesive applications, and the U.K. is strengthening pharmaceutical and specialty food labeling capacity following post-Brexit supply chain adjustments.

Domestic capital investment is aligning with national industrial strategies that are encouraging localized manufacturing growth and modernization. The EU PPWR mandates recyclable labeling and adhesive solutions by 2030, which is accelerating equipment upgrades and adhesive reformulation initiatives across production facilities. Companies are pursuing retrofit programs to achieve sustainability objectives without disrupting existing operations, while technology providers are developing compatible solutions that integrate efficiently into installed production lines. Europe is therefore maintaining its role as a mature yet progressively evolving market leader with stable demand supported by policy-driven innovation.

North America Wet Glue Labeling Machine Market Trends

North America is expected to occupy a prominent position in the market for wet glue labeling machines through 2033, powered by the large spirits, craft beverage, and pharmaceutical production sectors of the U.S. Beverage manufacturers are requiring reliable labeling performance to support diverse bottle designs and frequent product variations, while pharmaceutical facilities are depending on highly accurate systems to meet stringent compliance requirements. A well-established healthcare regulatory environment is reinforcing expectations for equipment reliability and traceability. Breweries and distilleries are prioritizing adaptable machines that enable rapid adjustments across production runs. The U.S. FDA Drug Supply Chain Security Act (DSCSA) serialization requirements are accelerating modernization efforts in pharmaceutical labeling infrastructure to ensure end-to-end product traceability across distribution networks.

Organizations are investing in compliant labeling technologies to meet regulatory deadlines while strengthening supply chain transparency and product authentication capabilities. Innovation clusters in states such as Ohio, Pennsylvania, and California are supporting technological advancement, where OEMs are developing servo-driven platforms and IoT-enabled monitoring solutions to enhance operational intelligence. Environmental policies are also shaping equipment decisions, as the Environmental Protection Agency (EPA) guidelines and state-level EPR regulations are influencing material selection and packaging sustainability strategies. These regulatory and technological dynamics are shortening equipment replacement cycles across manufacturing facilities, which is creating recurring revenue opportunities for suppliers.

Competitive Landscape

The global wet glue labeling machine market is exhibiting moderate consolidation, with major participants such as Krones, KHS, Barry-Wehmiller, Sidel Group, and HERMA GmbH capturing nearly half of the total market share. Competitive dynamics are intensifying as manufacturers are prioritizing advanced engineering capabilities to differentiate performance and reliability. Established companies are maintaining leadership through customized system configurations, high operational efficiency, and collaborative business strategies that strengthen long-term customer relationships. Continuous investment in research and development is enabling these firms to introduce innovative solutions that address evolving production requirements across multiple industries. Strategic alliances and technology partnerships are supporting market expansion while reinforcing brand credibility in regulated sectors that demand consistent labeling accuracy and throughput stability.

Large corporations are retaining dominant positions due to robust technological expertise, integrated service offerings, and direct sales networks that improve customer engagement and after-sales support. Mid-sized manufacturers are expanding geographically to capture emerging opportunities, while specialized entrants are focusing on niche applications to achieve competitive differentiation through targeted innovation. Advancements in automation, digital connectivity, and energy-efficient machine architecture are defining competitive advantage, particularly as customers are seeking flexible platforms that accommodate diverse packaging formats.

Key Industry Developments

- In September 2025, HEUFT unveiled its fully modular HEUFT TORNADO II switch labelling machine at drinktec 2025, enabling rapid plug-and-play station changes, automated format adjustments, and hybrid labeling combinations such as wet glue, self-adhesive, and wrap-around at speeds up to 60,000 bottles per hour.

- In August 2025, SCREEN unveiled the Truepress LABEL 520AQ, a proof-of-concept water-based inkjet digital label press designed for high-speed production at up to 100 m/min on 520mm media width. It delivers 1200 x 1200 dpi offset-quality output with low-odor Truepress SC+ inks, precise registration via EQUIOS workflow, and versatility for paper, films, and specialty labels.

- In July 2025, at Labelexpo Europe 2025, Gallus, a subsidiary of HEIDELBERG, unveiled the all-digital Gallus Alpha and the high-performance hybrid Gallus Five, built on the Gallus Labelmaster platform. These innovations address label producers' demands for greater speed, flexibility, and quality amid shorter runs and tighter margins.

Companies Covered in Wet Glue Labeling Machine Market

- Krones AG

- KHS GmbH

- Barry-Wehmiller Companies

- Sidel Group

- HERMA GmbH

- Marchesini Group

- Accutek Packaging

- Neri S.r.l.

- P.E. Labellers S.p.A.

- IC Filling Systems

- Shanghai Jiuyuan

- Quadrel Labeling Systems

- Brothers Pharmamach India

- Fuji Seal International

- Pro Mach Inc.

Frequently Asked Questions

The global wet glue labeling machine market is projected to reach US$ 5.1 billion in 2026.

The market is driven by the automated packaging demand in food/beverage, regulatory compliance, and IoT advancements to boost efficiency.

The market is poised to witness a CAGR of 5.5% from 2026 to 2033.

Eco-friendly adhesives, expansion into Asia Pacific, and smart tech integration for premium segments are unlocking high-value market opportunities.

Krones AG, KHS GmbH, Barry-Wehmiller Companies, Sidel Group, and HERMA GmbH are some of the key players in the market.