- Smart Packaging

- Booklet Label Market

Booklet Label Market Size, Share, and Growth Forecast, 2026 - 2033

Booklet Label Market by Material (Paper, Plastic, Others), Product Type (Fold-out Labels, Multi-page Labels, Leaflet Labels), Functionality (Regulatory/Instructional, Promotional, Security/Anti-Counterfeit), and Regional Analysis 2026 - 2033

Booklet Label Market Size and Trends Analysis

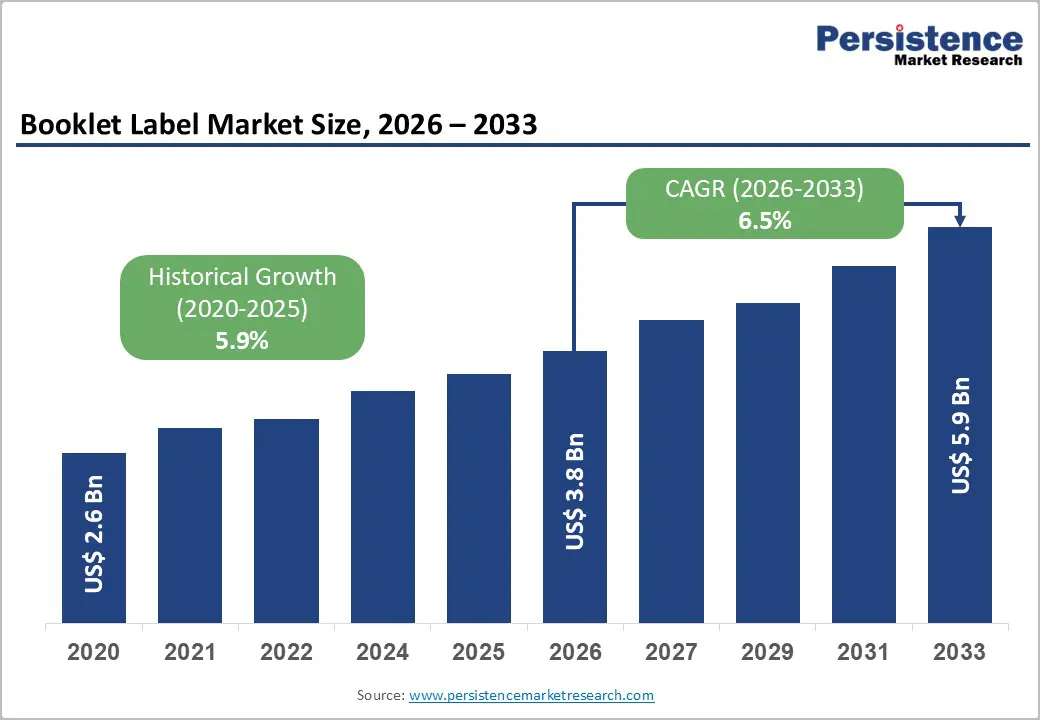

The global booklet label market size is likely to be valued at US$3.8 billion in 2026 and is expected to reach US$5.9 billion by 2033, growing at a CAGR of 6.5% during the forecast period from 2026 to 2033, driven by stricter pharmaceutical regulations requiring detailed instructional labels and a growing demand for security features to combat counterfeiting.

Increasing regulatory demands for comprehensive product information, especially in the pharmaceutical and agrochemical industries, are contributing to the market's expansion. Brand owners are also adopting multi-page label formats to include multilingual instructions and security features, all while preserving primary packaging dimensions. This shift helps reduce secondary packaging waste while ensuring compliance with global labeling standards.

Key Industry Highlights:

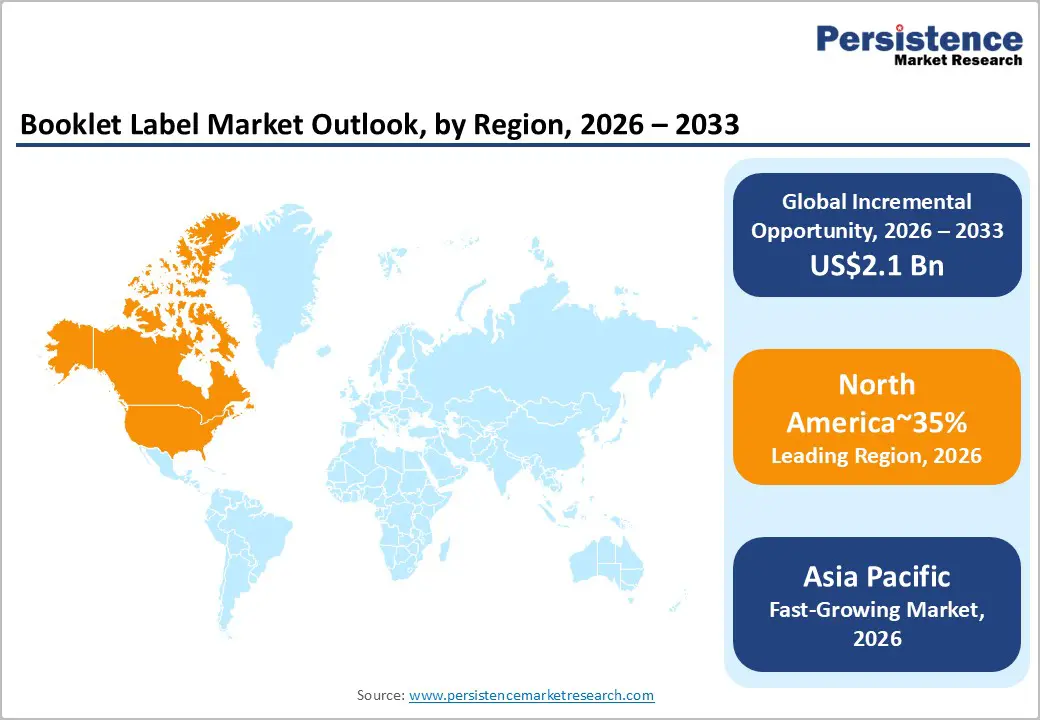

- Leading Region: North America is projected to lead due to deep pharmaceutical manufacturing intensity, accounting for approximately 35% share in 2026, advanced packaging automation, and established regulatory enforcement frameworks.

- Fastest-growing Region: Asia Pacific is anticipated to grow fastest due to rapid industrial expansion, regulatory modernization, and rising adoption across pharmaceuticals, chemicals, and premium consumer goods sectors.

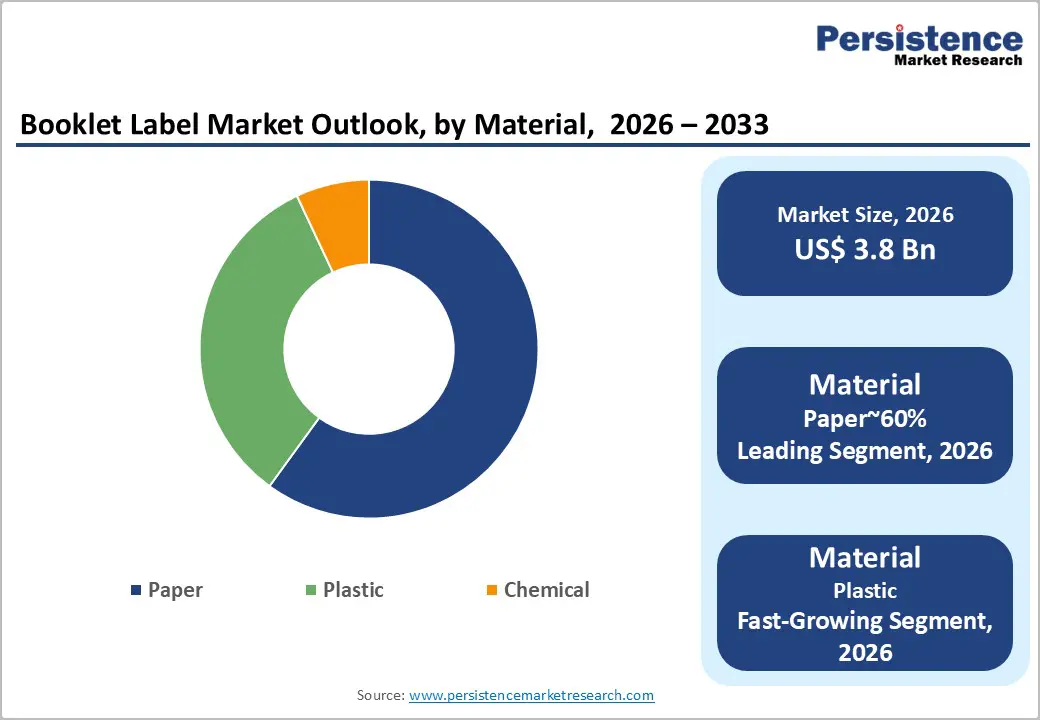

- Leading Material: The paper segment is anticipated to dominate accounting with approximately 60% share in 2026 through entrenched pharmaceutical adoption, high production throughput compatibility, print clarity, and suitability for high-value regulatory applications.

- Leading Functionality: Regulatory/Instructional is projected to dominate for compliance simplicity, cost optimization, and mandatory use across pharmaceuticals and chemicals, holding approximately 54% share in 2026.

| Key Insights | Details |

|---|---|

|

Booklet Label Market Size (2026E) |

US$3.8 Bn |

|

Market Value Forecast (2033F) |

US$5.9 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

6.5% |

|

Historical Market Growth (CAGR 2020 to 2025) |

5.9% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis – Globalized Manufacturing Footprints and Multilingual Packaging Standardization

The consolidation of multinational manufacturing hubs is intensifying cross-border distribution complexity within consumer goods value chains. Centralized production models increasingly serve linguistically diverse end markets from single origin facilities. This structural shift necessitates multilingual disclosure frameworks embedded directly within primary packaging configurations. Booklet labels enable simultaneous inclusion of multiple language instructions without expanding packaging footprints. Standardized multi-country packaging architectures reduce stock-keeping fragmentation and simplify global inventory rationalization. International trade facilitation bodies recognize harmonized labeling as a lever for lowering logistical coordination burdens. Consequently, multi-page labeling solutions are becoming integral to globally optimized packaging strategies.

The multilingual labeling reduces repackaging cycles and downstream localization costs. Unified packaging formats enhance demand forecasting accuracy across regionally diversified distribution networks. Regulatory heterogeneity across jurisdictions further reinforces the need for adaptable labeling in real estate. Booklet architectures accommodate jurisdiction-specific disclosures while preserving brand consistency across markets. This flexibility mitigates the obsolescence risk associated with regulatory amendments and language updates. Technology-enabled print workflows support scalable variable content integration within centralized production systems. The globalization and linguistic diversity embed expanded labeling formats as structural enablers of supply chain efficiency.

Serialization Mandates, and Clinical Trial Complexity in Pharmaceutical Labeling

Pharmaceutical labeling demand is structurally driven by expanding regulatory disclosure obligations across global markets. In the European Union, Directive 2001/83/EC mandates multilingual labeling across member states. This requirement compels manufacturers to consolidate extensive statutory content within constrained primary packaging formats. Expanded content labels enable multi-country stock-keeping units, reducing region-specific packaging fragmentation and inventory duplication. Authorities, including the U.S. Food and Drug Administration and the European Medicines Agency, require comprehensive disclosures spanning indications, dosage protocols, and contraindication frameworks. Recent revisions under the European Medicines Agency Blue Box guidance intensify visibility and user-interface expectations.

Parallel digitization of pharmaceutical supply networks reinforces demand through serialization and traceability obligations. The Drug Supply Chain Security Act mandates interoperable electronic tracing at the package level across the United States. Similarly, the Falsified Medicines Directive requires unit-level serialization and tamper-evident safeguards across European markets. Booklet labels accommodate two-dimensional data carriers alongside mandated statutory text without compromising readability standards. Expanded labels, therefore, function as adaptive compliance platforms across commercial and clinical pharmaceutical operations.

Barrier Analysis - Application Speed Constraints Across Automated Packaging Lines

The integration of booklet labels into automated packaging environments introduces mechanical and throughput limitations. Their multi-layered construction increases caliper thickness relative to conventional single-ply label formats. Elevated material bulk affects dispensing precision under high-speed rotary and inline labeling systems. Packaging lines calibrated for thin substrates frequently require hardware modification or recalibration. Misfeeds, edge lifting, and jamming risks intensify when applied at rapid operational velocities. These technical constraints reduce achievable line speeds and compromise overall equipment effectiveness. High-volume manufacturing segments experience disproportionate productivity impacts from reduced packaging throughput.

The slower line speeds translate into higher per-unit conversion costs. Capital expenditure may be required for reinforced applicators and upgraded motion-control systems. Validation cycles extend when mechanical adjustments intersect with regulated packaging environments. Operational downtime during retrofitting further erodes short-term production efficiency. Fast-moving consumer goods manufacturers prioritize velocity to protect margin structures and asset utilization. Any reduction in throughput directly affects cost absorption and inventory turnover dynamics.

Raw Material Price Volatility

Volatility in substrate and adhesive input markets constrains cost stability across booklet label manufacturing ecosystems. Paperboard, specialty films, laminates, and pressure-sensitive adhesives are closely linked to pulp, petrochemical, and energy markets. Fluctuating upstream commodity prices are transmitted directly into conversion costs and procurement budgeting cycles. Label converters operating under fixed supply agreements face margin compression when input escalation outpaces contractual repricing mechanisms. Short procurement visibility complicates inventory planning and disrupts production scheduling across print and finishing operations. Supply chain disruptions in pulp processing and polymer production amplify exposure to cyclical price swings. These structural cost uncertainties weaken pricing predictability within the broader packaging value chain.

Raw material instability alters competitive positioning between integrated and non-integrated converters. Large vertically aligned suppliers may partially hedge input risk through diversified sourcing strategies. Smaller converters remain disproportionately exposed to short-term procurement shocks and working capital strain. Buyers in regulated sectors resist frequent price revisions due to validation and compliance constraints. This misalignment between input volatility and customer repricing flexibility erodes operating margins. Technology upgrades and sustainability-grade materials further elevate baseline material intensity and capital burden. Consequently, raw material volatility functions as a persistent structural restraint on profitability and investment planning.

Opportunity Analysis – Smart Label Integration and Digital Traceability Enablement

The integration of near field communication and quick response technologies into booklet labels creates incremental value across regulated and consumer-facing markets. Growing consumer emphasis on product traceability and authenticity verification strengthens demand for digitally enabled labeling architectures. Smart labels enable real-time access to origin data, compliance documentation, and lifecycle transparency through connected platforms. This capability enhances post-sale engagement while supporting anti-counterfeit and parallel trade mitigation strategies. Regulatory scrutiny over supply chain visibility further reinforces adoption across pharmaceuticals, premium consumer goods, and specialized industrial products. Partnerships between label converters and technology solution providers accelerate embedded electronics and secure data encoding capabilities. As digital ecosystems mature, connected labeling becomes a structural extension of broader supply chain digitization frameworks.

Smart label integration reallocates demand toward chip embedding, secure printing, and data management infrastructure. Anti-counterfeit functionality enhances value capture within high-risk product categories exposed to diversion and imitation. Security-focused segments exhibit sustained growth as authentication becomes embedded within compliance architectures. Digital traceability also supports inventory analytics, recall management, and regulatory reporting automation. Upfront integration costs are offset by downstream efficiency gains and brand protection benefits. Interoperability with enterprise resource planning and serialization systems further elevates strategic importance. Consequently, smart booklet labels represent a convergence point between packaging, data intelligence, and compliance-driven innovation.

Convergence of Interactive Packaging and Smart Label Technologies

The convergence of physical labeling with embedded digital technologies is redefining functional packaging architectures. Integration of radio frequency identification, near field communication, and quick response interfaces transforms booklet labels into connected data nodes. These technologies enable secure product authentication, real-time inventory visibility, and dynamic consumer content delivery. Interactive labeling directly addresses rising expectations for transparency, traceability, and brand-level digital engagement. Advanced packaging frameworks increasingly align with enterprise digitization strategies across regulated and premium product categories. Embedded connectivity strengthens anti-diversion controls while enhancing lifecycle monitoring across distribution networks. This evolution positions booklet labels as interoperable components within broader intelligent packaging ecosystems.

Smart integration shifts value creation toward data infrastructure and secure encoding capabilities. Packaging suppliers expand competencies into electronics embedding, firmware integration, and cloud-linked data management. Retailers and brand owners leverage interactive features to refine demand analytics and post-purchase engagement. Authentication functionality mitigates counterfeiting exposure in high-value and compliance-sensitive markets. Inventory traceability improves recall responsiveness and regulatory audit readiness. The expanding smart packaging segment reflects structural investment in digitally enabled labeling platforms. Consequently, interactive booklet labels represent a scalable growth vector within advanced packaging markets.

Category-wise Analysis

Material Type Insights

The paper segment is anticipated to dominate, accounting for approximately 60% share in 2026, supported by entrenched adoption across pharmaceuticals and high-volume consumer goods. Its cost advantage relative to synthetic films reinforces default selection in margin-sensitive packaging programs. Superior ink absorption and fold memory support dense regulatory text without legibility failure. Alignment with recyclability mandates strengthens positioning within mono-material packaging architectures. Suppliers, including Avery Dennison, UPM Raflatac, and CCL Industries, expand certified and recycled paper portfolios. Innovations such as linerless constructions and wash-off adhesives improve logistics efficiency and end-of-life processing.

Plastic is projected to be the fastest-growing segment in the booklet label market, driven by performance requirements in moisture-intensive and chemically exposed environments. Polyethylene, polypropylene, and polyethylene terephthalate films ensure durability where paper substrates degrade. Cold-chain biologics, agrochemicals, and flexible personal care packaging accelerate the shift toward film-based constructions. Companies such as Schreiner MediPharm and UPM Raflatac advance recycled and bio-based film innovations. Clear multilayer films and squeeze-resistant laminates support premium aesthetics and structural resilience. Film substrates also enable secure embedding of connected authentication components. These attributes position plastic booklet labels as the market’s high-growth performance engine.

Functionality Insights

The regulatory/instructional segment is anticipated to dominate the market segment, accounting for approximately 54% share in 2026, anchored by mandatory disclosure requirements across pharmaceuticals, chemicals, and food sectors. Compliance with frameworks enforced by the U.S. Food and Drug Administration and the European Medicines Agency necessitates multi-page instructional formats on constrained packaging surfaces. Booklet labels address small-container limitations while preserving legibility and standardized hazard communication. Suppliers such as Schreiner MediPharm, CCL Industries, and Denny Bros embed resealable constructions and detachable components to support workflow continuity.

The security/anti-counterfeit segment is expected to be the fastest-growing segment, driven by escalating global losses from counterfeit trade and parallel market diversion. Brand owners increasingly integrate tamper-evident seals, serialized identifiers, and covert authentication layers within booklet constructions. Technology providers, including Avery Dennison, Securikett, and 3M, advance RFID, optical variable inks, and high-bond security adhesives. Embedded near-field communication and blockchain-linked identifiers elevate traceability across e-commerce and cross-border logistics channels. Anti-counterfeit functionality increasingly serves both public safety and revenue protection imperatives.

Regional Insights

North America Booklet Label Market Trends

North America is expected to remain the leading market, accounting for approximately 35% share in 2026, supported by deep pharmaceutical penetration and advanced packaging automation infrastructure. Regional dominance is anchored in strong healthcare manufacturing intensity and structured compliance frameworks that necessitate multi-page disclosure formats. High enterprise adoption of digital and flexographic printing platforms is expected to reinforce scale efficiencies and rapid version control across regulated product lines. Demand is anticipated to remain concentrated in pharmaceuticals, specialty chemicals, and high-transparency consumer goods, where expanded content labels function as compliance-critical components. Sustainability integration and smart tracking capabilities are positioned to shape procurement priorities, embedding RFID-enabled and recycled-content constructions within mainstream packaging workflows.

The U.S. is projected to anchor regional momentum by shaping technology standards, regulatory interpretation, and capital allocation across booklet label applications. Federal oversight frameworks governing drug labeling and environmental disclosures are expected to sustain structurally high documentation density per package. Leading converters such as Avery Dennison, CCL Industries, and 3M are positioned to expand smart labeling and durable adhesive platforms within pharmaceutical and industrial supply chains. Investment is likely to prioritize automation, cloud-linked print management, and serialization compatibility to support healthcare traceability mandates. As e-commerce logistics and biopharma scale continue to intensify, the U.S. is expected to preserve North America’s structural leadership in advanced booklet label deployment.

Asia Pacific Booklet Label Market Trends

Asia Pacific is projected to emerge as the fastest-growing region, while expanding its structural contribution through manufacturing scale and regulatory modernization. Regional acceleration is expected to be anchored in China and India, where pharmaceutical production, specialty chemicals, and export-oriented consumer goods continue to intensify labeling complexity. Governments across the region are anticipated to align domestic compliance frameworks with international documentation standards, thereby increasing multi-page and multilingual labeling requirements. Expanding middle-class consumption and premium packaging expectations are likely to reinforce demand for high-content disclosure formats across healthcare, cosmetics, and packaged food categories. Cost-efficient production ecosystems are expected to position the region as a global supply hub for booklet labels embedded within export packaging workflows.

India is anticipated to anchor high-volume expansion by integrating export-compliant booklet labels within generic pharmaceutical shipments targeting regulated Western markets. Regional and multinational players such as CCL Industries, Avery Dennison, Jindal Poly Films, and Cosmo Films are positioned to expand advanced film substrates, RFID-enabled constructions, and sustainable linerless technologies across Asia Pacific manufacturing clusters. As pharmaceutical exports, e-commerce logistics, and regulatory convergence accelerate, Asia Pacific is expected to solidify its fastest-growing trajectory within the global booklet label landscape.

Europe Booklet Label Market Trends

Europe is expected to remain a stable and mature market, supported by harmonized regulatory enforcement and diversified industrial end-use sectors. Regional demand is projected to remain structurally consistent due to mandatory multilingual labeling requirements under European Union classification and packaging directives. Germany is anticipated to function as the industrial anchor, with sustained utilization across chemical manufacturing, automotive supply chains, and agrochemical exports requiring high-density instructional formats. The U.K. and France are expected to reinforce stability through pharmaceutical serialization requirements and luxury cosmetics compliance documentation. The competitive landscape is projected to remain moderately fragmented, balancing multinational converters with specialized regional firms focused on compliance-driven customization and sustainability engineering.

Germany is expected to anchor regional continuity by integrating advanced digital print systems with high-durability label substrates for regulated chemical and agricultural exports. National manufacturers are projected to prioritize tear-resistant, weather-stable booklet constructions capable of accommodating over twenty language panels for single market distribution. Leading European label specialists such as Faubel are positioned to advance QR-enabled and compliance-centric booklet solutions supporting traceability and authentication objectives. As regulatory alignment and sustainability mandates deepen, Germany is expected to sustain Europe’s stable structural position in the advanced booklet label segment.

Competitive Landscape

The global booklet label market is moderately fragmented, with leadership concentrated among global converters such as CCL Industries, Avery Dennison, and 3M. These firms exert structural influence through vertically integrated material sourcing, advanced digital and flexographic print platforms, and embedded compliance expertise across pharmaceutical, chemical, and premium consumer goods sectors. Their technological footprint extends into RFID-enabled constructions, serialization-compatible substrates, and sustainable adhesive chemistries, shaping procurement specifications for multinational brand owners.

Competitive positioning reflects both horizontal scale advantages in global production networks and vertical specialization in regulated end-use segments requiring high documentation density. Regional players differentiate through niche capabilities such as tamper-evident engineering, multi-language booklet formats, and rapid version control for export-driven applications. Industry behavior is expected to remain characterized by selective mergers and acquisitions, capacity rationalization, and continued investment in automation and cloud-linked print management systems. Platform convergence toward integrated packaging ecosystems is likely to strengthen long-term supplier consolidation while preserving targeted specialization in high-compliance verticals.

Key Industry Developments:

- In February 2026, Avery Dennison expanded its NFC product line with Pragmatic Semiconductor’s flexible chips for digital product passports, enabling the mass production of low-cost, smart booklet labels that allow consumers to verify product authenticity via a simple smartphone tap.

- In January 2026, CCL Industries acquired ALT Technologies, strengthening its CCL Design division and enhancing its functional label portfolio for automotive and durable goods, offering advanced materials for booklet-style technical labels.

- In May 2025, Schreiner MediPharm launched a groundbreaking digital display label for clinical trial drugs, eliminating the need for manual re-labeling when protocol numbers or expiry dates change, significantly reducing time-to-market for new drugs.

Companies Covered in Booklet Label Market

- CCL Industries

- Multi-Color Corporation

- Avery Dennison

- All4Labels Global Packaging Group

- Schreiner Group

- Resource Label Group

- Denny Bros

- Faubel

- JH Bertrand

- Securikett

- Skanem

- Reflex Labels

- NSD International

- Edwards Label

- CS Labels

- JH Bertrand

Frequently Asked Questions

The global booklet label market is projected to be valued at US$3.8 billion in 2026 and is expected to reach US$5.9 billion by 2033, driven by stringent pharmaceutical labeling mandates, rising anti-counterfeit requirements, and expanding multilingual packaging needs across globalized supply chains.

Expanding regulatory disclosure obligations across the require extensive dosage instructions, contraindications, serialization codes, and multilingual content on compact packaging formats. Booklet labels provide scalable multi-page capacity without increasing primary pack dimensions, making them structurally integral to compliance-driven pharmaceutical and clinical trial packaging architectures.

The booklet label market is forecast to grow at a CAGR of 6.5% from 2026 to 2033, reflecting steady expansion across regulated industries and increasing integration of smart traceability technologies.

North America leads the market, accounting for approximately 35% share, supported by advanced pharmaceutical manufacturing, strict regulatory enforcement by federal agencies, and early adoption of digital printing, RFID-enabled labels, and automated packaging systems.

The booklet label market is moderately fragmented, with leading participants including CCL Industries, Multi-Color Corporation, Avery Dennison, Schreiner Group, and Denny Bros. Competition centers on regulatory expertise, digital printing scale, smart label integration, and vertically integrated material sourcing capabilities.