- Technology

- ID Card Printer Market

ID Card Printer Market Size, Share, and Growth Forecast 2026 - 2033

ID Card Printer Market by Product Type (Single-sided Card Printers, Double-sided Card Printers, High-performance Card Printers, Standard Card Printers), Technology (Retransfer, Direct-to-Card, Rewritable), End-Use Industry (Government & Public Sector, Healthcare, Banking & Financial Services, Corporate/Enterprise, Education, Transportation & Logistics, Retail & Hospitality, Defense & Security, Events & Entertainment), Distribution Channel, Regional Analysis, 2026 - 2033

ID Card Printer Market Size and Trend Analysis

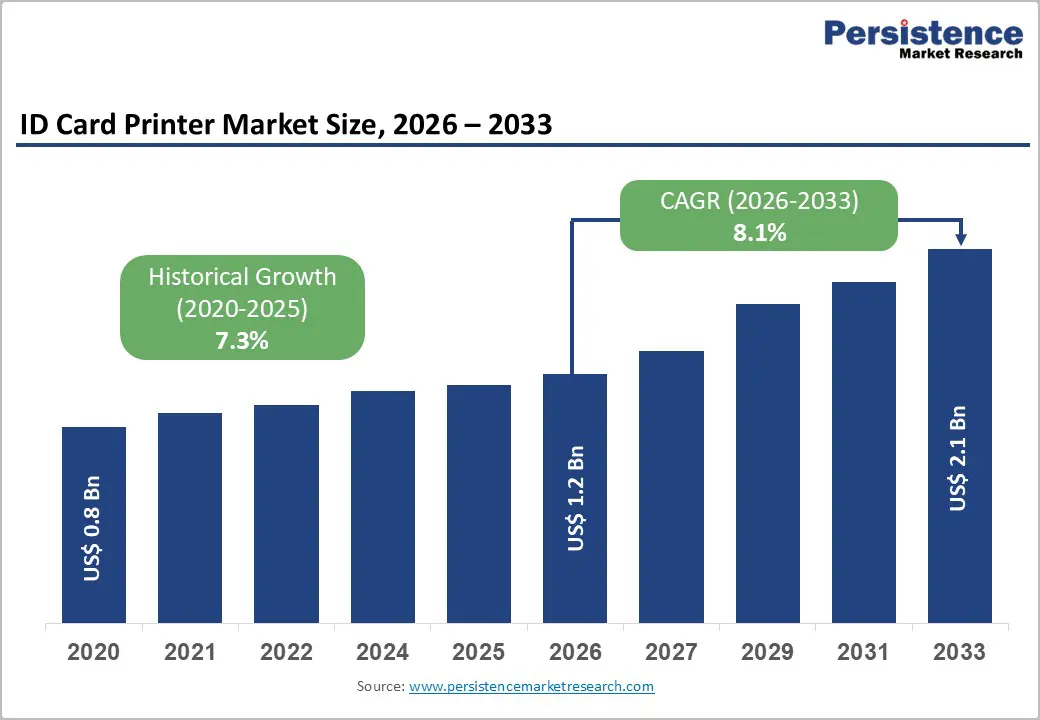

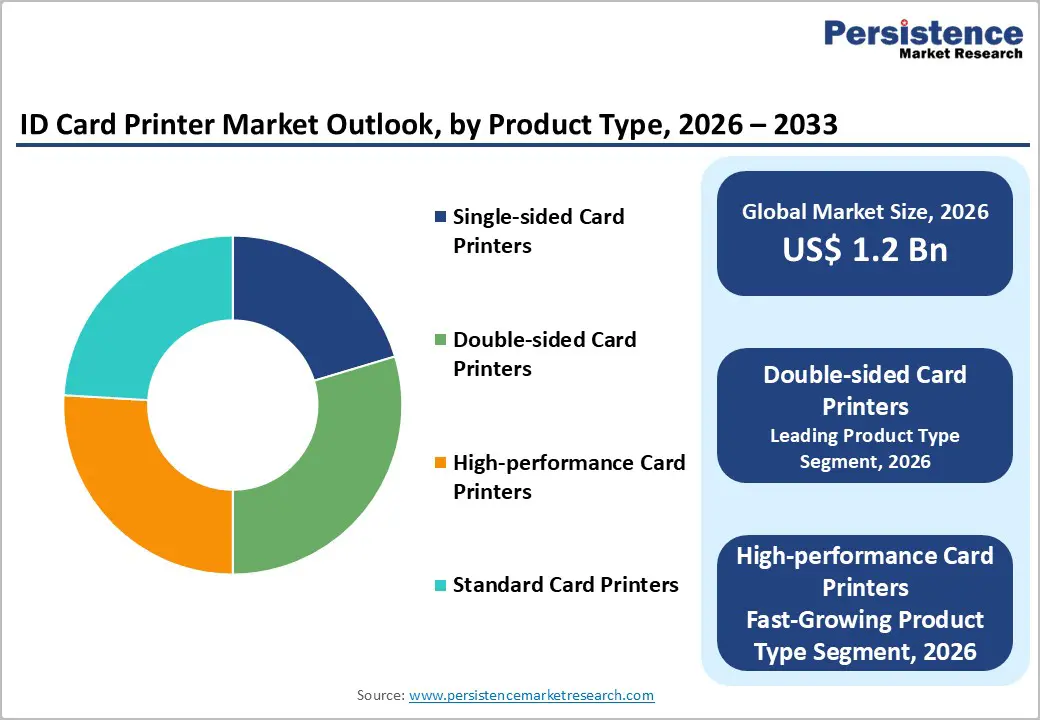

The global ID card printer market size is expected to be valued at US$ 1.2 billion in 2026 and projected to reach US$ 2.1 billion by 2033, growing at a CAGR of 8.1% between 2026 and 2033.

The rising demand for secure identification solutions across the government, corporate, healthcare, and education sectors is a major growth driver. Growing concerns about identity theft and strict regulatory mandates for employee and visitor credentials are accelerating adoption. Governments worldwide are strengthening access control standards, encouraging the deployment of advanced printing systems. Technological advancements, including enhanced print durability, smart card encoding, and biometric integration, are further supporting market expansion and operational efficiency.

Key Market Highlights

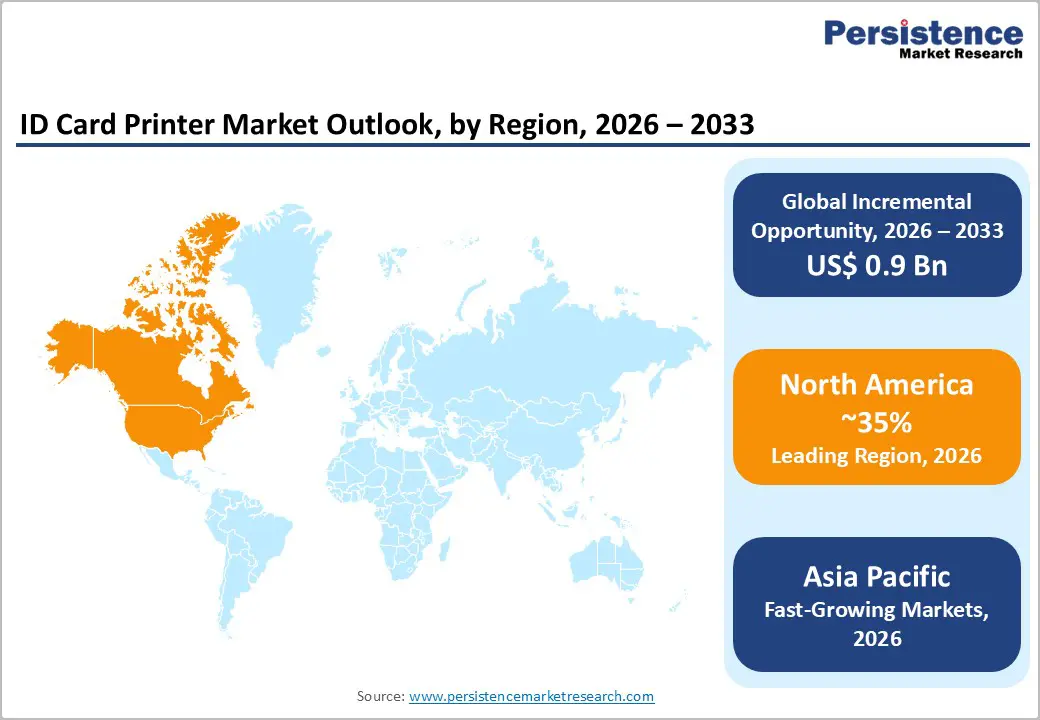

- Leading Region: North America dominates the ID Card Printer market with a 35% share in 2025, supported by strong regulatory frameworks such as REAL ID enforcement in the United States.

- Fastest-Growing Region: Asia-Pacific, with

- a 30% share in 2025, is the fastest-growing region, driven by large-scale identification programs across China, India, and ASEAN economies.

- Leading Product Category: Double-sided card printers account for 45% share in 2025, preferred for high-efficiency, dual-sided printing in enterprise and government applications.

- Leading Technology Segment: Direct-to-Card technology holds a 52% share in 2025, widely adopted for cost-effective and high-volume PVC card printing.

- Key Market Opportunity: The continued expansion of national ID initiatives and public-sector digitization programs globally sustains demand for secure, high-volume ID card printing solutions.

| Key Insights | Details |

|---|---|

|

ID Card Printer Size (2026E) |

US$ 1.2 billion |

|

Market Value Forecast (2033F) |

US$ 2.1 billion |

|

Projected Growth CAGR(2026-2033) |

8.1% |

|

Historical Market Growth (2020-2025) |

7.3% |

Market Dynamics

Drivers - Rising Incidence of Identity Fraud Driving Demand for Secure and Compliant Identification Solutions

The growing number of identity theft and fraud incidents is significantly increasing the demand for secure ID card printing solutions. With the FBI reporting over 1.1 million identity theft complaints in 2023, organizations are prioritizing tamper-resistant credentials embedded with holograms, microtext, and smart chips. Government agencies, financial institutions, and corporate enterprises rely on secure printers to reduce the risk of unauthorized access and strengthen identity verification systems.

Regulatory mandates and global standards such as ISO/IEC 14443 for contactless smart cards are compelling institutions to adopt compliant printing technologies. In-house card issuance helps organizations reduce breach risk, control sensitive data, and lower outsourcing costs. The expansion of hybrid and remote work models further drives demand for secure employee badges and controlled facility access worldwide.

Continuous Technological Advancements and Smart Integration Enhancing Printing Efficiency

Rapid technological innovations in ID card printing are accelerating market growth across industries. Retransfer printing technology, known for superior image clarity and edge-to-edge coverage on uneven card surfaces, is gaining strong adoption. Improvements in print durability, faster output speeds, and enhanced color accuracy are enabling organizations to produce high-quality, long-lasting credentials suited for demanding security environments.

Furthermore, integration with RFID, NFC, and smart connectivity solutions is transforming traditional ID cards into multifunctional access tools. Businesses are upgrading legacy systems to enable seamless encoding, personalization, and centralized card management. Smart, network-enabled printers improve operational efficiency and scalability, particularly in high-volume government, education, and enterprise security applications.

Restraints - High Upfront Investment and Ongoing Consumable Costs Limiting Adoption

The substantial initial investment required for advanced ID card printers remains a key barrier, particularly for small and medium-sized enterprises. High-performance models often exceed US$ 2,000 per unit, making procurement challenging for cost-sensitive organizations. Budget-constrained sectors such as education, retail, and small offices often delay adoption or opt for outsourced printing services to minimize capital expenditures.

Beyond acquisition costs, recurring expenses for ribbons, laminates, cleaning kits, and replacement parts significantly increase total ownership costs. Industry estimates suggest that maintenance and consumables can add 20–30% to annual operating expenses. These financial pressures limit widespread penetration in emerging and price-sensitive markets, slowing adoption despite long-term operational and security benefits.

Growing Adoption of Mobile and Cloud-Based Digital Identification Solutions

The rapid expansion of digital identity platforms and mobile credentials is reducing reliance on physical ID cards. Technology providers such as Apple and Google report billions of digital ID activations, signaling a structural shift toward smartphone-based authentication. Organizations are increasingly adopting app-based verification systems that eliminate the need for printed badges in certain access control environments.

Evolving security frameworks and guidelines promoting cloud-based identity verification are accelerating this transition. Corporate offices, coworking spaces, and tech-driven enterprises are integrating digital wallets and virtual credentials into access systems. As more institutions migrate to paperless and contactless identification models, demand for traditional hardware-based ID card printers faces gradual pressure.

Opportunity - Expanding National ID Programs and Rising Defense Modernization Initiatives

Large-scale government identification programs are creating strong growth opportunities for ID card printer manufacturers. Initiatives such as biometric-based national ID systems and digital citizen databases are increasing demand for secure, high-volume card-issuance infrastructure. With global agencies estimating that over one billion people will require updated identification by 2030, demand for durable, compliant printing solutions is expected to remain robust.

In parallel, rising defense modernization budgets are strengthening opportunities in military and homeland security applications. Armed forces require advanced printers for secure access badges, personnel IDs, and encrypted smart cards. Long-term public sector contracts and strict security compliance standards provide stable revenue streams for vendors offering high-security, tamper-resistant printing technologies.

Accelerating Digital Transformation Across Healthcare and Education Institutions

Ongoing digital transformation in the healthcare and education sectors is generating new avenues for ID card printer adoption. Hospitals increasingly deploy patient wristbands and secure staff credentials to improve identification accuracy and operational safety. Global health agencies report millions of new identification requirements annually, reinforcing the need for reliable, on-demand printing systems integrated with hospital information platforms.

Similarly, universities and schools are strengthening campus security through advanced ID solutions. Rising investments in campus access control technologies and smart infrastructure are encouraging the integration of printers with IoT-enabled tracking systems. Rewritable and eco-friendly card technologies further present opportunities for cost savings and sustainability-focused institutions seeking reusable credential solutions.

Category-wise Analysis

Product Type Insights

Double-sided card printers lead the product segment, accounting for 45% of the market share in 2025. Their dominance is driven by the ability to print on both sides of a card in a single pass, eliminating manual intervention and improving operational efficiency. These printers are widely adopted across enterprises, banking institutions, and government offices where high-volume, professional-grade badge production is essential. Faster throughput rates and enhanced personalization capabilities further strengthen their position in demanding environments.

High-performance card printers are emerging as the fastest-growing product category. Their ability to deliver superior image quality, edge-to-edge printing, and enhanced durability makes them increasingly preferred for high-security applications. The growing demand for premium credentials for government IDs, financial institutions, and access-controlled facilities is accelerating the adoption of this advanced printing technology.

Technology Insights

Direct-to-Card (DTC) technology holds a leading 52% market share in 2025, primarily due to its cost-effectiveness and faster printing speeds. The technology is widely used for PVC card printing and supports high-volume issuance with relatively lower consumable costs. Its operational simplicity and reliability make it the preferred choice for retail, educational, and corporate environments in which standardized identification cards are produced regularly.

Retransfer printing technology represents the fastest-growing segment within this category. Its ability to print high-resolution images on uneven or smart card surfaces enhances card durability and visual appeal. Increasing demand for secure, tamper-resistant credentials in banking, government, and defense sectors is driving rapid adoption of this premium printing solution.

Industry Insights

The Government and Public Sector accounted for 38% of the market share in 2025, maintaining its leadership position due to stringent identification regulations and national security mandates. Policies such as GDPR in Europe and the REAL ID Act in the United States require secure, standardized credentials. Bulk issuance of voter IDs, employee badges, and citizen identification cards ensures consistent procurement from public authorities worldwide.

The healthcare sector is emerging as the fastest-growing end-use industry. Hospitals and medical institutions increasingly deploy secure staff badges and patient identification systems to enhance safety and compliance. The growing emphasis on digital health records and real-time tracking solutions is encouraging the integration of ID card printers into broader hospital information systems.

Distribution Channel Insights

Direct sales dominate the distribution channel segment, accounting for 55% of the market in 2025. Original equipment manufacturers prefer this channel to deliver customized solutions, offer technical demonstrations, and provide after-sales support. This approach strengthens relationships with enterprises, defense, and government clients that require tailored configurations and long-term service agreements.

Online and third-party distribution channels are witnessing the fastest growth. Small and medium-sized enterprises increasingly prefer digital procurement platforms for convenience and competitive pricing. Expanding e-commerce presence and simplified purchasing processes are enabling manufacturers to reach new customer bases across emerging and decentralized markets.

Regional Insights

North America ID Card Printer Market Trends

North America holds a leading 35% share of the global ID card printer market in 2025, supported by strong regulatory enforcement and technological innovation. The United States remains the primary contributor, with REAL ID compliance requirements driving large-scale issuance of secure driver’s licenses and identification cards. Federal mandates and homeland security initiatives continue to stimulate procurement of advanced printing systems.

The region also benefits from established technology ecosystems and ongoing R&D in smart and hybrid printing solutions. Frameworks developed by national standards bodies promote secure card production, while federal and state-level contracts ensure consistent demand. High adoption across corporate, healthcare, and government sectors further strengthens regional leadership.

Europe ID Card Printer Market Trends

Europe is expected to expand steadily, with a projected CAGR of 7.2% over the forecast period. Regulatory harmonization initiatives, such as eIDAS 2.0, are encouraging the integration of digital and physical identification systems across member states. Countries, including Germany and the United Kingdom, are at the forefront of secure national ID rollouts and infrastructure modernization efforts.

Strict data protection laws and compliance standards are reinforcing demand for tamper-resistant and secure card printing technologies. Smart city initiatives across France, Spain, and other European nations are further driving adoption. Government-backed identification programs and public sector modernization projects continue to provide stable opportunities for market participants.

Asia Pacific ID Card Printer Market Trends

Asia-Pacific accounts for 30% of the global market in 2025 and is one of the most dynamic regions for growth. Large-scale population identification programs in countries such as China and India are generating substantial demand for high-volume, secure printing solutions. Expanding urbanization and government digitization initiatives are accelerating adoption across public and private sectors.

The region benefits from strong manufacturing capabilities and cost-efficient production ecosystems. National ID upgrades, biometric integration, and the expansion of access control systems across ASEAN economies further support demand. Growing investments in logistics, education infrastructure, and enterprise security solutions continue to strengthen the region’s position in the global market.

Competitive Landscape

The ID Card Printer market is moderately consolidated, characterized by a mix of established global manufacturers and regional participants competing across enterprise and institutional segments. Leading players focus heavily on research and development to enhance print durability, smart card encoding, and integration with NFC and RFID technologies. Strong software ecosystems, secure encoding capabilities, and end-to-end card issuance solutions serve as key competitive differentiators in high-security environments.

Market participants are increasingly adopting subscription-based consumable models and managed print services to build recurring revenue streams. Advancements such as AI-enabled personalization, cloud connectivity, and remote printer management are shaping competition, while mid-tier players compete on pricing flexibility and customized solutions.

Key Developments:

- In June 2025, HID Global launched Evolis Primacy 2.0 with enhanced retransfer technology designed for high-security applications. The upgraded model offers improved edge-to-edge print quality, advanced lamination options, and stronger encoding capabilities, making it suitable for government IDs, financial cards, and enterprise-level secure credential issuance programs worldwide.

- In March 2024, Zebra Technologies introduced the ZC300 series, featuring integrated RFID encoding to streamline card personalization and data-embedding processes. The solution enhances operational efficiency with faster processing, a simplified user interface, and flexible connectivity options tailored for corporate, retail, and education environments.

- In November 2023, NXP Semiconductors partnered with multiple printer manufacturers to support secure chip embedding within smart ID cards. The collaboration focuses on strengthening encryption standards, enabling advanced authentication protocols, and improving compatibility with contactless systems used in transportation, banking, and government identification programs.

Companies Covered in ID Card Printer Market

- Zebra Technologies Corporation

- Evolis

- HP Inc.

- Brady Corporation

- Quadient (Neopost SA)

- Matica Technologies AG

- ID Tech Solution Pvt Ltd.

- Entrust Corporation

- Unicard Technologies Pvt Ltd.

- Kanematsu USA (Nisca and Swiftcolour)

- CIM USA

- HID Global Corporation

- Valid USA

- NBS Technologies

- MagiCARD Ltd.

Frequently Asked Questions

The global ID card market is projected to reach US$ 1.2 billion in 2026, driven by strong demand across government and enterprise sectors.

Rising identity fraud cases and regulatory mandates such as REAL ID are accelerating adoption, particularly in the Government & Public Sector segment, which holds a 38% share in 2025.

North America leads the market with a 35% share in 2025, supported by stringent U.S. federal identification mandates and compliance requirements.

Expansion of national ID programs globally presents strong opportunities, especially in Asia Pacific.

Leading companies include Zebra Technologies Corporation, Evolis, HP Inc., Brady Corporation, and Quadient (Neopost SA).