- Food Ingredients & Additives

- Food Hydrocolloids Market

Food Hydrocolloids Market Size, Share, Growth, and Regional Forecast, 2026 - 2033

Food Hydrocolloids Market is segmented by Product Type (Gelatin, Pectin, Xanthan Gum, Carrageenan, Guar Gum, Gum Arabic, Others), Function (Thickener, Stabilizer, Emulsifier, Gelling, Coating, Others), End-user (Bakery & Confectionery, Meat & Poultry, Sauces & Dressings, Beverages, Dairy Products, Others), and Regional Analysis, 2026 - 2033

Food Hydrocolloids Market Share and Analysis

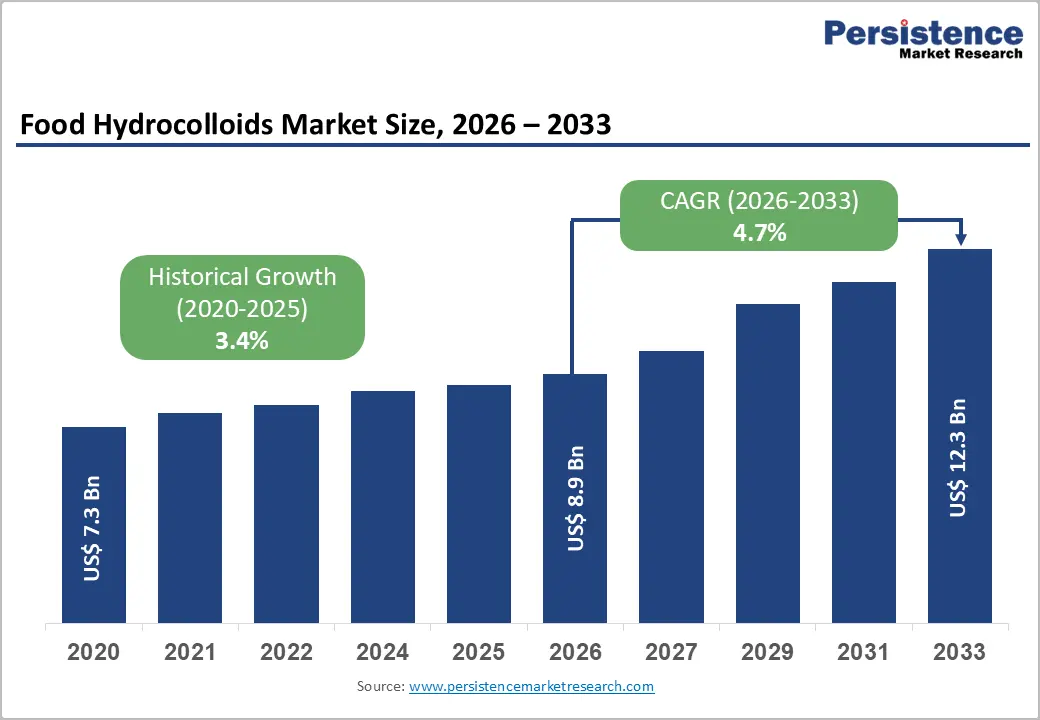

The global food hydrocolloids market size is expected to be valued at US$ 8.9 billion in 2026 and projected to reach US$ 12.3 billion by 2033, growing at a CAGR of 4.7% between 2026 and 2033. The global market is evolving into a high-impact functional ingredient space where texture engineering meets clean-label innovation. Once considered background stabilizers, hydrocolloids are now central to product reformulation strategies across plant-based, reduced-sugar, and fortified foods.

Demand is being reshaped by precision functionality, viscosity control, emulsification, and water-binding aligned with modern dietary expectations. At the same time, supply-side complexities and climate sensitivity are forcing companies to rethink sourcing and formulation strategies. With strong cross-industry relevance spanning bakery, dairy alternatives, beverages, and processed proteins, hydrocolloids are no longer commoditized inputs but strategic enablers of next-generation food design.

Key Industry Highlights:

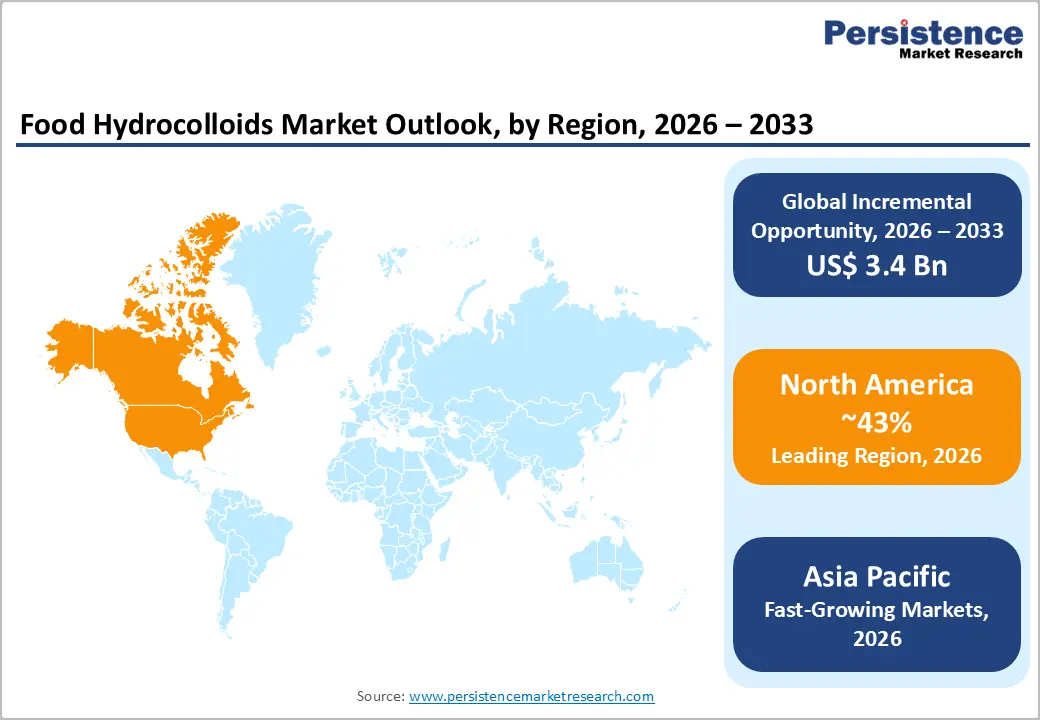

- Leading Region: North America, holding ~43% market share, driven by a mature food processing ecosystem, strong demand for functional and clean-label foods, and continuous innovation in low-sugar and fortified formulations

- Fastest-Growing Region: Asia Pacific, fueled by rapid urbanization, rising middle-class consumption, expansion of processed food sectors, and increasing shift toward plant-based and functional ingredients

- Fastest-Growing Product Type Segment: Carrageenan and plant-based hydrocolloids, driven by strong demand in dairy alternatives, protein stabilization, and clean-label reformulations

- Growth Indicators: Rising shift toward plant-based and clean-label ingredients is accelerating the adoption of natural hydrocolloids as multifunctional stabilizers, texturizers, and emulsifiers across diverse food applications

- Opportunities: Expansion into vegan meat and dairy alternatives, where advanced hydrocolloid blends enable replication of texture, mouthfeel, and structural integrity in next-generation products

- Consumer Trends: Increasing preference for label transparency, reduced additives, and functional benefits is pushing manufacturers to adopt high-purity, plant-derived hydrocolloids with tailored performance characteristics

- Key Developments: In March 2026, Guangrao Liuhe Chemical Co., Ltd. showcased its guar gum portfolio at the China International Food Additives and Ingredients Exhibition (FIC 2026), highlighting advancements in food ingredient innovation.

| Key Insights | Details |

|---|---|

|

Food Hydrocolloids Market Size (2026E) |

US$ 8.9 Bn |

|

Market Value Forecast (2033F) |

US$ 6.8 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

4.7% |

|

Historical Market Growth (CAGR 2020 to 2025) |

3.4% |

Market Dynamics

Driver - Rising shift toward plant-based and clean-label ingredients

The accelerating shift toward plant-based, clean-label, and transparently sourced ingredients drives the market growth. Increasing lifestyle-related health concerns, highlighted by organizations such as the Food and Agriculture Organization, are pushing consumers to favor natural functional additives over synthetic alternatives. Hydrocolloids such as pectin and guar gum are gaining traction as label-friendly stabilizers, thickeners, and emulsifiers across a wide range of food applications. Their plant-derived origin and compatibility with non-GMO and allergen-free formulations make them highly attractive in modern product development.

Beyond clean-label positioning, hydrocolloids are increasingly used to improve texture and stability in plant-based dairy, beverages, and reduced-fat foods. Companies like Cargill, Incorporated and Ingredion Incorporated are expanding botanical ingredient portfolios to meet this demand, supporting innovation in functional and health-oriented food categories.

Restraints - Raw material volatility and climate-linked supply disruptions

A major constraint in the global food hydrocolloids market is the high dependence on climate-sensitive raw materials and geographically concentrated supply chains. Key inputs such as gum arabic from the Sahel region and carrageenan derived from seaweed in Southeast Asia are highly vulnerable to droughts, flooding, and oceanic changes. Insights from organizations like the World Bank highlight how climate variability and trade disruptions can trigger supply shortages and sharp price fluctuations. This volatility creates procurement challenges and margin pressures for manufacturers.

Companies such as CP Kelco and Tate & Lyle must navigate inconsistent supply and pricing instability, often complicating long-term contracts. These uncertainties can push end-users toward alternative or synthetic ingredients, limiting consistent market expansion.

Opportunity - Rapid Expansion into the Vegan Meat and Dairy Alternative Sector

A significant opportunity in the global food hydrocolloids market lies in the rapid expansion of plant-based meat and dairy alternatives. Hydrocolloids play a critical role in replicating the texture, viscosity, and mouthfeel of animal-derived products, enabling manufacturers to achieve creaminess in plant-based milks and structural integrity in meat substitutes. As consumer demand for vegan and flexitarian diets accelerates, food producers are increasingly relying on advanced hydrocolloid systems to deliver sensory experiences comparable to conventional products.

Innovation is shifting toward customized blends of texturizers and gelling agents that enhance meltability, stretch, and stability in applications such as vegan cheese and plant-based proteins. Companies investing in high-purity, flavor-neutral hydrocolloids with optimized functionality are well-positioned to capture premium segments. This trend is further supported by growing R&D efforts to improve protein-hydrocolloid interactions, unlocking new formulation possibilities for next-generation alternative food products.

Category-wise Analysis

Source Insights

Gelatin and xanthan gum remain dominant segments in the global food hydrocolloids market, driven by their wide functionality and established industrial usage. Gelatin remains a cornerstone of confectionery due to its unique thermoreversible gelling and melt-in-the-mouth properties, though demand is gradually being influenced by the rise of plant-based alternatives. Xanthan gum is highly preferred for its excellent cold-water solubility, shear stability, and performance across a wide pH range, making it indispensable in sauces, dressings, and ready-to-eat formulations. Its ability to deliver consistent viscosity under processing stress strengthens its position in large-scale food manufacturing.

Meanwhile, carrageenan is experiencing strong adoption in dairy applications for its superior interaction with milk proteins, enhancing texture and suspension stability. Gum arabic remains critical in beverage systems, particularly for stabilizing flavor emulsions in carbonated drinks. Additionally, pectin and guar gum are gaining traction in clean-label and plant-based formulations, supporting broader product diversification.

End-user Insights

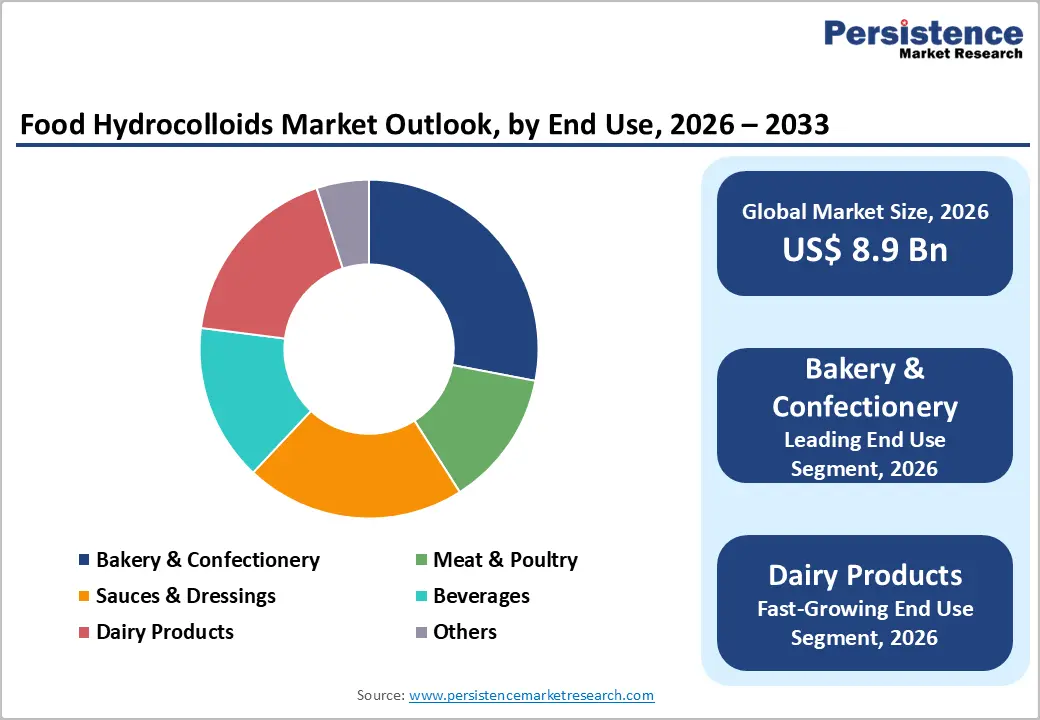

The bakery and confectionery segment remains the leading end-use category in the global food hydrocolloids market, accounting for nearly 29% share in 2025. Hydrocolloids play a crucial role in improving dough handling, controlling gluten structure, and preventing syneresis in fillings and toppings. They enhance moisture retention, extend shelf life, and deliver consistent texture in products such as cakes, pastries, and confectionery gels. Their functionality is particularly valuable in gluten-free and reduced-sugar formulations, where maintaining structure and softness is critical for product quality.

The dairy products segment is the fastest-growing, driven by rising demand for low-fat, lactose-free, and plant-based alternatives. Hydrocolloids provide creaminess, viscosity, and suspension stability in products like yogurt, flavored milk, and dairy substitutes. Meanwhile, the meat and poultry segment benefits from improved water-binding and yield enhancement, while the beverage sector increasingly uses hydrocolloids for pulp stabilization, mouthfeel enhancement, and fiber enrichment in functional drinks.

Region-wise Insights

North America Food Hydrocolloids Market Trends and Insights

North America is the leading region in the global market, holding a 43% market share in 2025. The region's leadership is underpinned by a highly mature food processing industry and a massive consumer base in the United States and Canada that prioritizes convenience and health-fortified foods. The presence of global market leaders like Ingredion and ADM ensures a constant pipeline of product innovation and high levels of investment in extraction technology.

Innovation in the North American market is currently focused on low-sugar and low-salt reformulations. There is a notable trend toward using hydrocolloids to compensate for the textural losses associated with sugar reduction. Furthermore, the region's strong focus on Sports & Clinical Nutrition has led to a surge in the use of specialized gums in protein-dense snacks. The high disposable income and the established habit of using functional ingredients maintain North America as the primary engine for global market value and high-end product launches throughout the forecast period.

Asia Pacific Food Hydrocolloids Market Trends and Insights

Asia Pacific is identified as the fastest-growing segment for the food hydrocolloids market through 2033. This rapid expansion is primarily driven by the burgeoning middle class in China, India, and ASEAN countries, who are increasingly adopting Western-style convenience diets. The rising awareness of heart health and the move away from traditional starch-heavy diets in urban centers have led to a surge in demand for functional hydrocolloids. China is a major global player, serving as a leading producer of Xanthan Gum and Carrageenan.

The region also benefits from significant manufacturing advantages and lower raw-material costs in Southeast Asia. In India, the government's focus on food processing infrastructure has encouraged local players to integrate functional additives into traditional dairy and snack formats. The rapid expansion of modern retail and the massive reach of e-commerce platforms have made processed foods containing hydrocolloids more accessible to a wider demographic. As Asian manufacturers look to replace synthetic ingredients with plant-based alternatives, the Asia Pacific region is poised to become the global hub for both consumption and value-added production.

Competitive Landscape

The global food hydrocolloids market features a moderately consolidated structure, with leading multinational players such as Cargill, Incorporated, DuPont, and Tate & Lyle exerting strong influence across the value chain. These companies leverage vertically integrated operations, spanning raw material sourcing to advanced ingredient processing and global distribution. Strategic initiatives are centered on geographic expansion, development of synergistic hydrocolloid blends, and acquisitions aimed at strengthening supply security and enhancing product portfolios.

At the same time, the market remains highly dynamic at the regional level, with specialized players targeting niche segments such as organic, clean-label, and pharmaceutical-grade hydrocolloids. Competitive differentiation is increasingly defined by viscosity precision, product purity, and adherence to global safety and sustainability certifications such as FSSC 22000, alongside the ability to deliver customized functional solutions.

Key Developments:

- In March 2026, Guangrao Liuhe Chemical Co., Ltd. showcased its core guar gum product portfolio at the China International Food Additives and Ingredients Exhibition 2026, held at the National Exhibition and Convention Center, highlighting its capabilities in food ingredient innovation.

- In December 2025, the Ministry of Marine Affairs and Fisheries announced plans to secure up to US$8 million in potential deals at the Food Ingredients Europe 2025, aiming to strengthen the global presence of Indonesia’s rapidly growing seaweed industry.

Companies Covered in Food Hydrocolloids Market

- Cargill, Incorporated

- DuPont

- Tate & Lyle PLC

- Ingredion

- ADM

- DSM-Firmenich

- Kerry Group PLC

- BASF SE

- Ashland Inc.

- Givaudan SA

- Jungbunzlauer Suisse AG

- Darling Ingredients Inc

- Others

Frequently Asked Questions

The global food hydrocolloids market is projected to be valued at US$ 8.9 Bn in 2026.

Rising shift toward plant-based and clean-label ingredients is a major driver of the global food hydrocolloids market.

The global Food Hydrocolloids market is poised to witness a CAGR of 4.7% between 2026 and 2033.

Rapid Expansion into the Vegan Meat and Dairy Alternative Sector is a significant opportunity in the food hydrocolloids market.