- Food Ingredients & Additives

- Food Acidulants Market

Food Acidulants Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Food Acidulants Market by Ingredient Type (Acetic Acid, Fumaric Acid, Citric Acid, Phosphoric Acid, Lactic Acid, Malic Acid, Tartaric Acid), by Nature (Powder, Liquid), by Livestock/End-user (Bakery & Confectionery, Beverages, Dairy Food, Animal Nutrition, Others), and Regional Analysis, 2026-2033

Food Acidulants Market Share and Trends Analysis

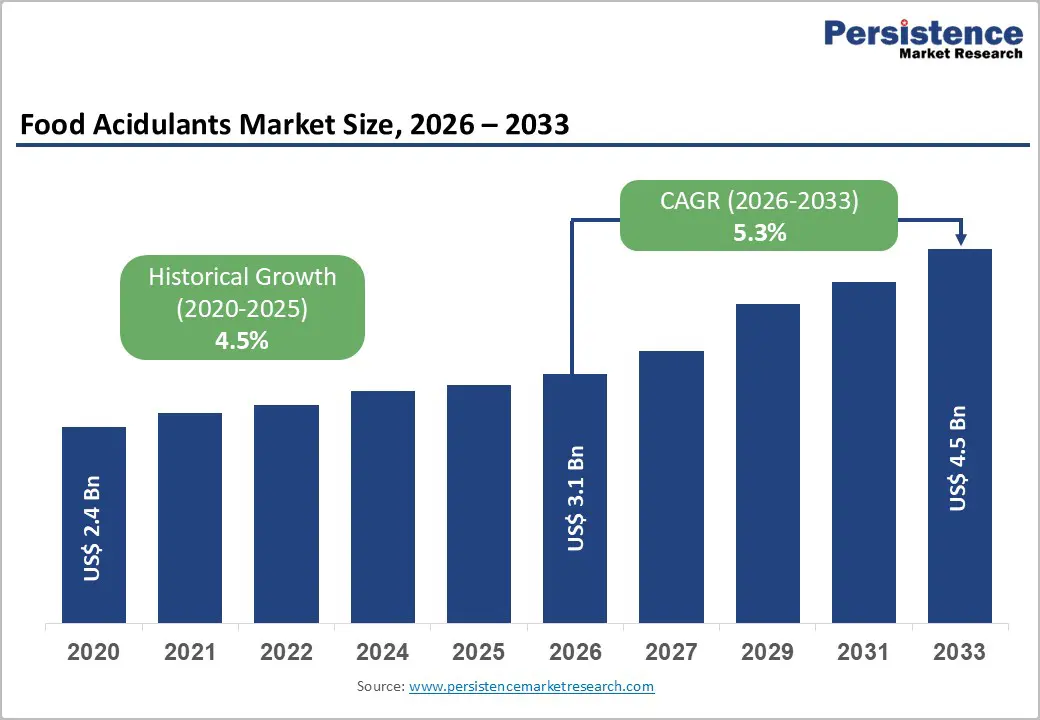

The global food acidulants market size is expected to be valued at US$ 3.1 billion in 2026 and projected to reach US$ 4.5 billion by 2033, growing at a CAGR of 5.3% between 2026 and 2033. The robust market expansion is primarily driven by the rise in global demand for processed and convenience foods, where acidulants serve as indispensable additives for flavor balancing and shelf-life extension. As urban populations rise and consumer lifestyles become increasingly hectic, the reliance on packaged goods that require high microbiological stability has surged. Furthermore, the burgeoning shift toward clean-label ingredients and the integration of specialized acidulants in animal nutrition to improve gut health have established a multi-sectoral demand base, ensuring a steady upward trajectory in market valuation throughout the forecast period.

Key Industry Highlights:

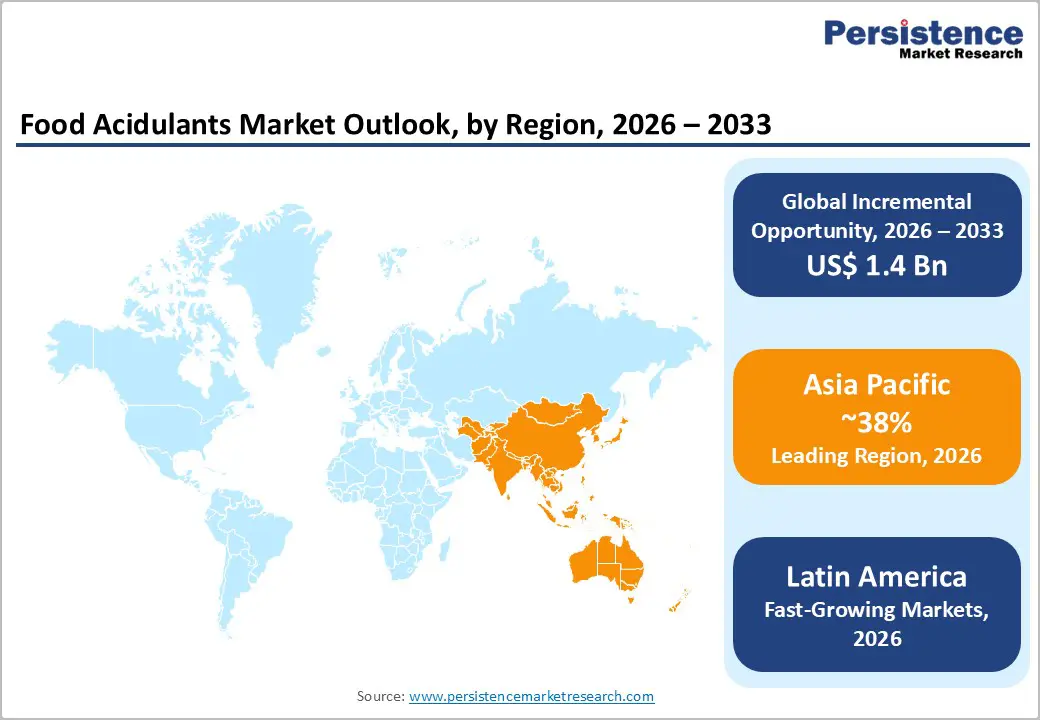

- Leading Region: Asia Pacific, accounting for around 38% market share in 2025, supported by large-scale food processing in China, India, and Japan, strong fermentation capacity, and proximity to key raw materials such as corn and cassava.

- Dominant Product Type Segment: Citric Acid, holding approximately 65% market share in 2025 due to its versatility, cost efficiency, mild taste profile, and wide acceptance across beverages, confectionery, and processed foods.

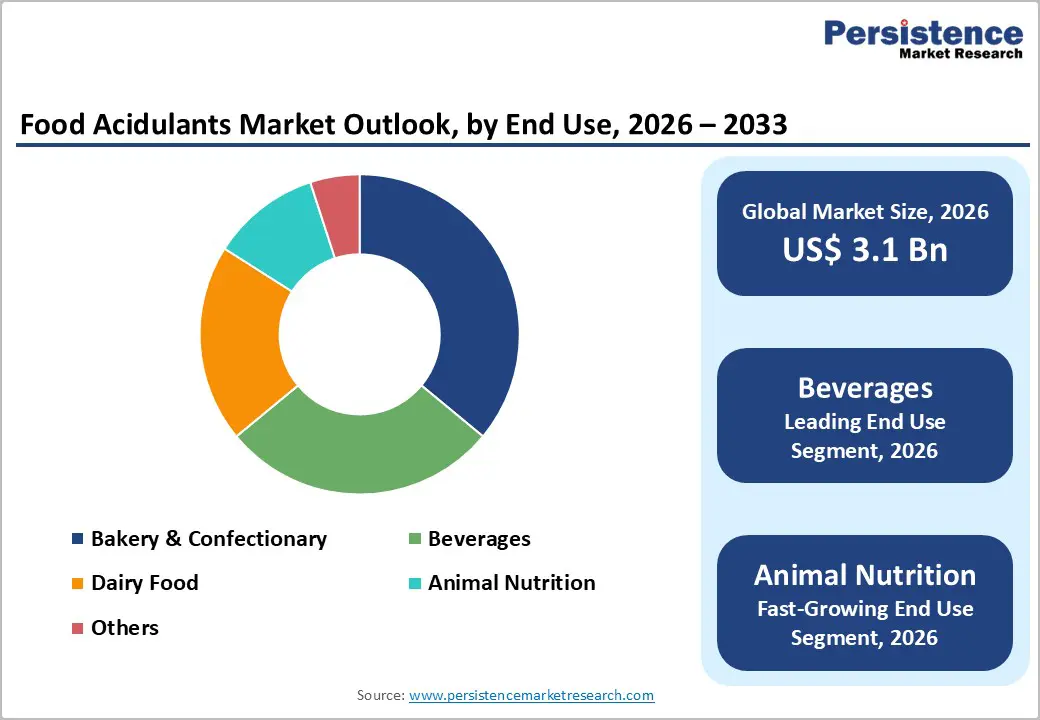

- Leading End-Use Segment: Beverages, capturing about 36% market share, fueled by high global intake of carbonated drinks, juices, energy drinks, and low-sugar functional beverages requiring precise pH control.

- Market Drivers: Rising consumption of processed and convenience foods is accelerating demand for acidulants that ensure microbial stability, extended shelf life, and consistent flavor profiles in industrial food production.

- Opportunities: Rapid expansion of plant-based and clean-label meat alternatives is creating demand for bio-derived acidulants that enhance flavor, texture, and safety while aligning with vegan and natural ingredient positioning.

- Key Developments: In December 2025, ICL Group agreed to acquire Bartek Ingredients to strengthen its malic and fumaric acid portfolio. In November 2025, Cairo 3A announced a US$150 million investment plan to expand food ingredient production capacity.

| Report Attribute | Details |

|---|---|

|

Global Food Acidulants Market Size (2026E) |

US$ 3.1 Bn |

|

Market Value Forecast (2033F) |

US$ 4.5 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

5.3% |

|

Historical Market Growth (CAGR 2020 to 2025) |

4.5% |

Market Dynamics

Driver – Rising Consumption of Processed and Convenience Foods

The primary driver for the food acidulants market is the structural shift in consumer dietary habits toward ready-to-eat and processed food products. In an era defined by rapid urbanization and time-constrained lifestyles, there is a massive reliance on packaged snacks, canned goods, and bottled beverages. Acidulants like Citric Acid and Malic Acid are critical in these products to manage pH levels, which prevents the growth of spoilage-causing microorganisms and ensures long-term safety. According to the Food and Agriculture Organization (FAO), the global processed food sector has seen continuous growth, directly correlating with the increased procurement of high-purity acidulants. These ingredients not only preserve quality but also provide the tangy sensory profiles that modern consumers demand, making them foundational to the industrial food processing supply chain.

Restraints – Volatility in Raw Material Prices and Supply Chain Disruptions

The food acidulants market faces significant resistance due to the fluctuating costs of raw materials used in fermentation and chemical synthesis. Major acidulants such as citric acid is primarily derived from substrates like maize or citrus fruits, which are highly susceptible to climatic changes and trade tensions. For example, recent supply chain bottlenecks and energy price hikes in major manufacturing hubs like China have led to unpredictable price surges for bulk acidulants. According to agricultural monitoring data, a 10% increase in industrial corn prices can disproportionately impact the profit margins of acidulant producers. This economic instability forces manufacturers to navigate a volatile pricing environment, which can deter long-term investment among smaller players.

Opportunity – Expansion of Plant-Based and Clean-Label Meat Alternatives

The meteoric rise of the plant-based meat industry presents a lucrative opportunity for the integration of specialized acidulants. Manufacturers of meat analogues require precise acidity control to replicate the flavor, color stability, and fibrous texture of animal proteins. Lactic Acid and Fumaric Acid are increasingly used to enhance the savory profile of mycelium and soy-based products while ensuring microbial safety. Recent developments, such as the USD 58 million funding for plant-based ventures in 2025, highlight the sector's growth potential. As companies like The Better Meat Co. and others scale their operations, the demand for bio-derived acidulants that align with vegan and clean-label standards is expected to generate significant revenue pockets for ingredient suppliers who can provide high-functionality organic acids.

Category-wise Analysis

By Product Type Insights

The citric acid segment remains the leading product type in the market, holding a dominant market share of approximately 65% as of 2025. The leadership of Citric Acid is justified by its unmatched versatility, low toxicity, and pleasantly sour taste, which makes it the preferred acidulant for nearly all food categories, from beverages to confectionery. Produced via the microbial fermentation of carbohydrates, it is favored for its chelating capabilities and its role as a natural preservative. According to research from Persistence Market Research, the segment benefits from its status as a "Generally Recognized as Safe" (GRAS) substance by the U.S. FDA. While other acids like Lactic Acid are growing rapidly in the meat and dairy sectors, the scale and cost-efficiency of Citric Acid production ensure it remains the cornerstone of the global food acidulants landscape.

By End-user Insights

The beverages segment is the leading end-use category, capturing a substantial 36% market share in 2025. This leadership is driven by the massive global consumption of carbonated soft drinks, fruit juices, and energy drinks, where acidulants are vital for flavor enhancement and pH regulation. Statistics indicate that the demand for low-sugar and functional beverages has surged by 14%, necessitating higher acidulant usage to balance flavor profiles. Conversely, the Animal Nutrition segment is identified as the fastest-growing category, with a projected high CAGR through 2032. The livestock industry is aggressively adopting acidulants to replace antibiotic growth promoters and improve the gastrointestinal health of poultry and swine. As global meat production intensifies, the procurement of acidulant blends for feed preservation and animal gut acidification represents a major emerging revenue stream.

Regional Insights

Asia Pacific Food Acidulants Market Trends and Insights

The Asia Pacific region held the leading position in the global market with a 38% share in 2025. This dominance is fueled by the massive food processing industries in China, India, and Japan, which cater to a burgeoning urban population with rising disposable incomes. China remains the world’s largest producer and exporter of Citric Acid, benefiting from a robust manufacturing infrastructure and lower production costs.

The region’s growth dynamics are also influenced by the "Healthy China 2030" initiative and similar policies that emphasize food safety and nutritional fortification. The expansion of the organized retail sector and the rapid growth of e-commerce in Southeast Asia have made packaged foods more accessible, further driving the demand for preservative acidulants. Manufacturing advantages in APAC, coupled with the proximity to major raw material sources such as cassava and corn, provide the region with a unique competitive edge in the global supply chain.

North America Food Acidulants Market Trends and Insights

North America remains a significant powerhouse in the market, characterized by a highly mature food and beverage sector and a robust innovation ecosystem. The United States leads the region, driven by high consumer demand for processed snacks and specialized sports drinks. A key trend in this region is the aggressive shift toward Clean-Label and non-GMO acidulants, as American consumers increasingly scrutinize ingredient labels.

The regulatory framework managed by the U.S. Food and Drug Administration (FDA) and the USDA ensures high standards of product safety and labeling transparency. Innovation in the U.S. is focused on "functionalization," where acidulants are used not just for taste but to deliver health benefits. Furthermore, the presence of major industry giants like Cargill, Incorporated and ADM facilitates rapid technological breakthroughs in fermentation technology. The region is also witnessing a surge in the use of organic acidulants in artisanal and craft beverages, reflecting a move toward premiumization and natural sourcing.

Latin America Food Acidulants Market Trends and Insights

Latin America Feed Binder Market is expected to grow at a CAGR of 7.7% as food acidulants gain strategic importance across beverage, dairy, and processed food manufacturing. Rising urban consumption, expanding cold-chain infrastructure, and greater emphasis on shelf-life stability are reshaping formulation strategies. In Brazil, beverage producers are increasing use of citric and lactic acid to balance sweetness and acidity in carbonated drinks, juices, and functional beverages. Local dairy processors are adopting fermentation-derived acidulants to improve texture, freshness perception, and clean-label positioning while managing tropical climate challenges.

Mexico shows accelerating demand for phosphoric and malic acid in bakery, confectionery, and sauces, driven by export-oriented processing. Across Chile, Colombia, and Peru, manufacturers favor powdered acidulants for cost control and storage efficiency. Regional suppliers are investing in localized blending, regulatory alignment, and sustainable sourcing to strengthen competitiveness regionally long-term.

Competitive Landscape

The global food acidulants market is characterized by a moderate degree of consolidation, where a handful of global agricultural and chemical conglomerates control a significant portion of the global supply of bulk organic acids. Companies like Cargill, ADM, and Corbion maintain their dominance through extensive vertical integration, controlling the supply chain from the procurement of raw grains to the manufacturing of finished ingredient solutions. These market leaders focus on a strategy of "specialization," moving beyond generic acids to provide high-performance, customized blends for specific industrial applications. Key differentiators employed by these leaders include the achievement of global sustainability certifications and robust R&D in fermentation yield optimization. Simultaneously, the market remains fragmented at the regional level, where numerous specialized producers in China and India compete on price and localized sourcing advantages.

Key Developments:

- In December 2025, ICL Group announced a definitive agreement to acquire Bartek Ingredients, a global leader in the production of malic and fumaric acids, aimed at expanding its portfolio in the specialty food ingredients sector.

- In November 2025, Cairo 3A unveiled a three-year investment plan valued at US$150 million aimed at expanding its industrial production capacity and enhancing Egypt’s self-sufficiency in key food ingredients.

- In July 2025, Petrobras considered setting up new acetic acid and monoethylene glycol (MEG) production plants at its Rio de Janeiro site as part of its 2025–2029 capital expenditure program valued at R$33 billion (US$6.08 billion).

- In November 2024, Jungbunzlauer partnered with the Technical University of Vienna (TU Wien) to support advanced research at the newly established Christian Doppler (CD) Laboratory, focusing on optimizing citric acid production through the refinement of high-performance fungal strains.

Companies Covered in Food Acidulants Market

- Cargill, Incorporated

- Tate & Lyle

- ADM

- Corbion N.V.

- BASF SE

- Jungbunzlauer Suisse AG

- Celanese Corporation

- FBC Industries, Inc.

- Parry Enterprises India Ltd.

- Corbion

- Others

Frequently Asked Questions

The global food acidulants market is expected to be valued at approximately US$ 3.1 billion in 2026, growing steadily at a CAGR of 5.3%.

The primary driver is the global shift toward processed and convenience foods, where acidulants are essential for maintaining flavor stability and extending shelf life through pH regulation.

The Asia Pacific region holds the leading market position with a 38% share in 2025, largely due to the massive scale of food processing in China and India.

Significant opportunities lie in the Plant-Based Meat sector and the integration of Microbial Fermentation technologies for sustainable, bio-based acidulant production.

The market is led by global giants including Cargill, Incorporated, ADM, Corbion N.V., Jungbunzlauer Suisse AG, and Tate & Lyle.