- HVAC

- High Power Industrial Burner Market

High Power Industrial Burner Market Size, Share, and Growth Forecast for 2025 - 2032

High Power Industrial Burner Market by Product (Regenerative Burners, High Velocity Burners, Impulse Burners, Radiant Burner, Customized (Burner Boilers), Flat Flame Burners, Oxygen Burners, Sinter Burners, Low & Ultra-low NOx Burners and Flameless Burners), Burner Design (Mono-block, Duo-block), Fuel Type, Rated Power (1 to 5 MW, 5 to 10 MW, 10 to 20 MW, 20 to 50 MW, 50 to 100 MW), End-user, and Regional Analysis from 2025 - 2032

Global High Power Industrial Burner Market Size and Share Analysis

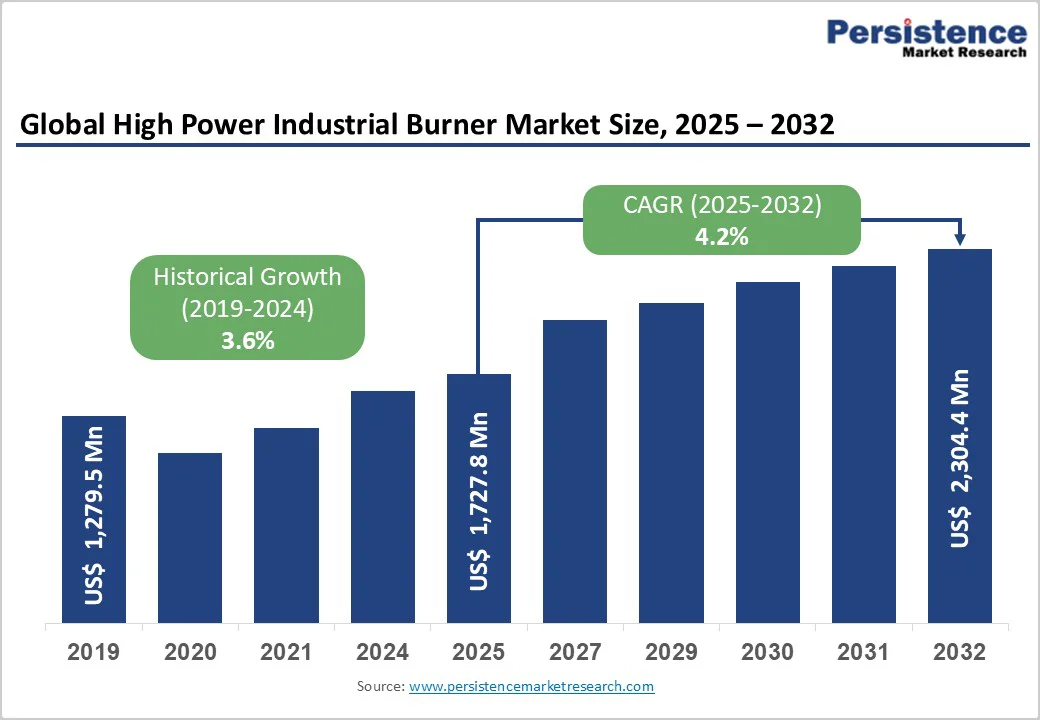

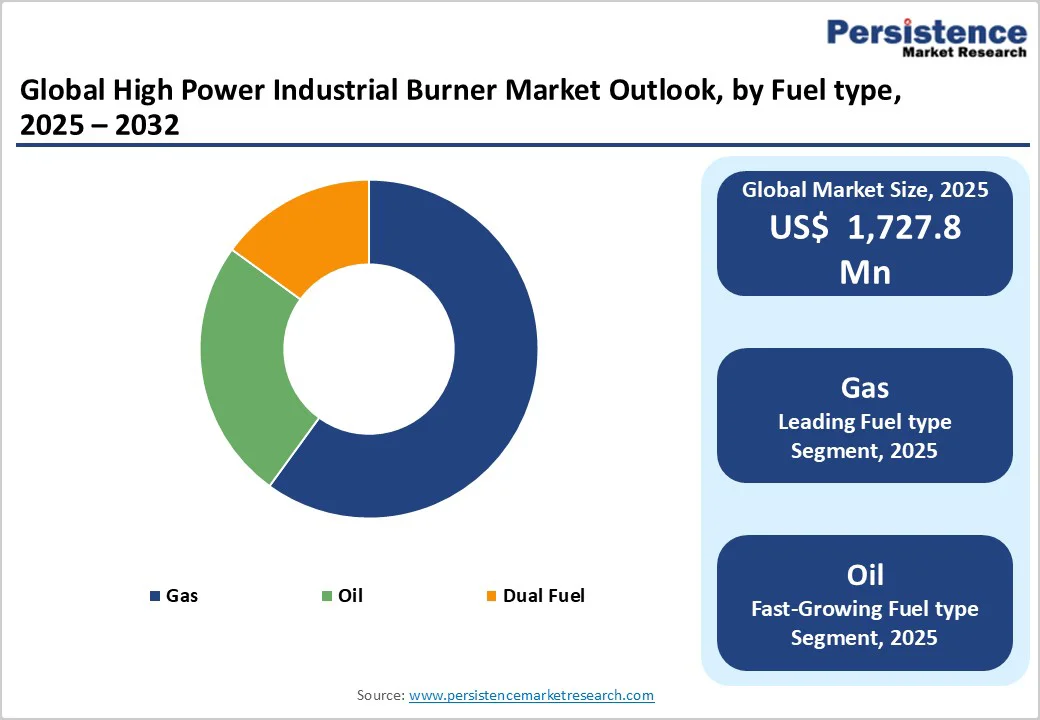

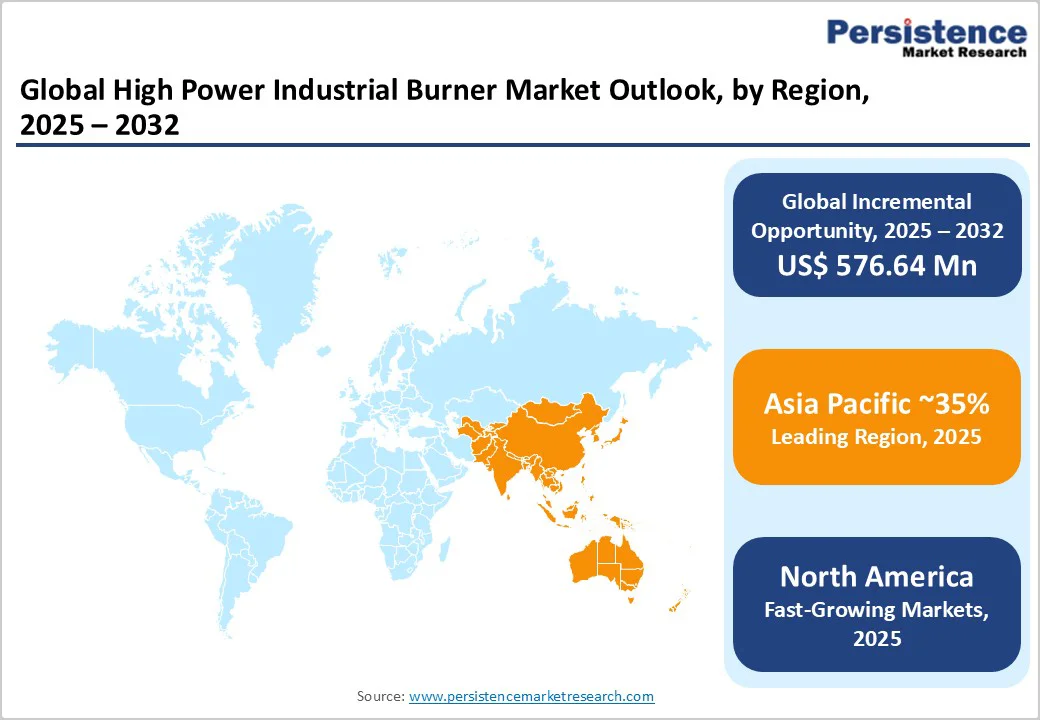

The global high power industrial burner market size is likely to value US$1.727 billion in 2025 and is projected to reach US$2.304 billion, growing at a CAGR of 4.2% between 2025 and 2032.

The market's expansion is fundamentally driven by rapid industrialization in emerging economies, particularly in the Asia Pacific, coupled with the global transition toward energy-efficient and low-emission burner technologies.

Key Highlights of the Market

- Leading Fuel Type: The gas burner segment dominates the market with a 52.7% share (USD 940 million) in 2025, driven by its high thermal efficiency, lower emissions, and cost-effectiveness compared to oil-based systems. The dual-fuel burner segment emerges as the fastest-growing category, offering flexible fuel-switching capabilities that enable operational continuity and cost optimization amid fluctuating fuel prices and supply uncertainties.

- Application Leadership: High-temperature industrial processes account for a 59.9% share of the market in 2025, supported by strong demand from metal forging, glass, and ceramics manufacturing. The boiler segment remains the largest individual application, driven by its critical role in steam generation for power plants, process industries, and large-scale manufacturing operations.

- Regional Dominance: Asia Pacific leads the global market with a commanding 33.4% share in 2025, reflecting rapid industrialization and infrastructure investment across petrochemical, metallurgy, and manufacturing sectors. China, representing 57.2% of the East Asian market, continues to expand at a 5.6% CAGR, supported by large-scale capacity additions and modernization of process industries.

- End-User Landscape: The Oil & Gas sector holds the largest revenue share at 60%, driven by the need for high-efficiency combustion systems to support reliable electricity and heat production.

- Technological Advancement: The market is transforming through the adoption of smart burners with IoT-enabled control systems, delivering up to 15% fuel efficiency improvements and predictive maintenance capabilities. Additionally, ultra-low NOx burner technologies, achieving sub-2.5 ppm emission levels, are gaining traction in highly regulated markets, creating competitive differentiation through advanced environmental compliance and energy performance.

| Key Insights | Details |

|---|---|

|

High Power Industrial Burner Market Size (2025E) |

US$1.727 billion |

|

Projected Market Value (2032F) |

US$ 2,304.4 Mn |

|

Global Market Growth Rate (CAGR 2025 to 2032) |

4.2% |

|

Historical Market Growth Rate (CAGR 2019 to 2023) |

3.6% |

Market Dynamics

Driver - Power Generation Infrastructure Expansion and Industrial Energy Demand

The global industrial burner market is experiencing significant growth fueled by increasing electricity consumption across industrial and residential sectors, with BRICS nations alone generating 8.5% more power in 2021 compared to 2019. Expanding power generation capacity requires substantial investments in boiler and combustion systems that utilize high-power industrial burners. Emerging markets such as India and China are prioritizing infrastructure development, with electricity consumption in China increasing by 9.7%, India by 4.8%, Russia by 6.4%, and Brazil by 9.5% in 2022. This infrastructure modernization directly translates to increased demand for advanced burner technologies capable of handling diverse fuel types and meeting stringent performance requirements.

Energy Efficiency and Environmental Compliance Regulatory Pressures

Stringent government regulations promoting energy efficiency and emissions reduction are compelling industries to adopt advanced burner technologies, particularly low-NOx systems that minimize environmental impact. The U.S. Energy Information Administration reports that total energy consumption accounts for a significant share of energy demand, driving the adoption of efficient solutions.

European Union regulations and similar policies in Asian countries establish strict environmental standards that favor manufacturers producing compliant burner systems. Low-nitrogen oxides (NOx) and ultra-low NOx burners are experiencing accelerating adoption, with technologies achieving emissions below 2.5 ppm gaining market traction. Companies implementing smart combustion control systems report fuel efficiency improvements of up to 15%, providing compelling economic incentives for industrial operators to upgrade existing installations.

Restraints - Trade Tensions and Supply Chain Disruption Risks

Tariffs on high-efficiency burner components, such as combustion sensors and flame control units, often imported from Germany and Switzerland, are eroding manufacturers' cost competitiveness, potentially reducing market growth forecasts by 0.3% annually. Trade restrictions between major economies create procurement challenges and increase operational costs. Supply chain fragmentation resulting from geopolitical tensions affects the availability of specialized components and increases lead times for burner system delivery. These structural constraints limit market expansion, particularly for manufacturers dependent on global supply networks.

High Capital Requirements and Technical Complexity Barriers

Advanced burner technologies require substantial capital investments for automation, IoT integration, and digital control systems, limiting adoption among small and medium-sized industrial operators. The complexity of modern combustion systems demands specialized engineering expertise and skilled labor, creating barriers to system installation and maintenance. Training requirements for operating sophisticated burner equipment with real-time monitoring capabilities add operational costs. Additionally, concerns about equipment obsolescence create financial risks for manufacturers investing in next-generation technologies.

Opportunities - Smart Burner Technology Integration and Industry 4.0 Adoption

Smart burners incorporating IoT and AI technologies enable real-time monitoring, predictive maintenance, and optimized fuel consumption, creating opportunities for premium-priced solutions with enhanced value propositions. Integration with Industry 4.0 ecosystems allows automated burner adjustment based on operating conditions and fuel quality variations. Remote diagnostics and performance analytics generate recurring revenue opportunities through subscription-based monitoring services. Manufacturers developing self-adjusting combustion systems and AI-driven optimization platforms are differentiating from competitors and capturing growing market segments seeking advanced operational efficiency.

Alternative and Renewable Fuel Infrastructure Development

The transition toward biogas, hydrogen, and other renewable fuels is creating substantial opportunities for burner manufacturers developing multi-fuel capable systems. European and North American policies promoting decarbonization create demand for hydrogen-compatible burners, with strategic partnerships like Fives Group and Lhyfe (July 2024) targeting industrial decarbonization applications. Emerging markets implementing cleaner fuel transitions are driving adoption of dual-fuel and biogas-compatible burners, expanding addressable market opportunities.

Category-wise Analysis

Burner Design

“Owing to their design features duo block high power industrial burners are in demand from End-users”

Based on burner design, the duo block high power industrial burners are anticipated to hold the largest market share owing to their applications in high-temperature combustion systems. The segment is anticipated to hold more than US$ 500 Mn of absolute dollar opportunity by 2032. Duo block burners occupy less space and operate with low noise, hence they are highly preferred for boiler & steam generation applications.

Fuel Type

“Gas based high power industrial burners are highly preferred among the end-users”

Based on fuel type, gas burners are estimated to account for the largest share of the high-power industrial burner market. Gas as fuel emits low carbon and burns with high efficiency. Hence, they are widely used in various end-use industries. In 2025, gas burners are expected to hold around 45% of the market share. The need for gas-fueled, high-power industrial burners is anticipated to increase gradually as a result of expanding end-use sectors like oil and gas, chemicals, and others.

End-users

According to end-users, the oil and gas sector is anticipated to hold more than one-high-Power value share in 2025. Great power industrial burners are in high demand due to the growth and expansion of this industry on a global scale.

Other than the oil and gas industry, there has been significant growth in the power production and building sectors, with an increasing focus on environmental sustainability, notably in the European region. In the upcoming years, South Asia, Russia, and South America will emerge as markets for high power industrial burners due to new oil, gas, and petrochemical activities.

Region-wise Insights

North America

As a result of the country in the North American commercial burner market, the U.S. maintains a total estimated nearly seventy-six percent market share of the country’s overall market. In the U.S., the market for industrial burners is growing, largely because of energy efficiency concerns, stricter regulations relating to the environment, an increase in the use of alternative fuels and natural gas, technological improvements, the quest for sustainable options, and growth in the manufacturing and chemical sectors.

The United States is estimated to control over 3/4 of the market in North America in terms of value. The main factors driving the U.S.'s high demand for industrial burners are its highly developed industrial sector and the country's shifting preference for sustainable burner technology.

Due to the growth of end-use sectors such as power generation, metallurgy, oil & gas, industrial, and others, the U.S. has a highly developed market for high power industrial burners. These industries are what are driving the sales of high-power industrial burners.

Additionally, the U.S. government's recent investments in infrastructure and municipal waste management are anticipated to boost sales of industrial burners in the nation.

Europe

The share of the industrial burners’ market by Europe will be approximately 24% in 2024, whereas an increase of 4.7% per annum is estimated from 2025-2034. With the European Green Deal and Fit for 55 packages, the EU has set an ambitious target for carbon neutrality by the year 2050. If implemented, it will stimulate the need for better technologies for cleaner burning. Increasing fuel prices and the requirement for effective energy utilization are also factors favoring the growth of the market.

The market of industrial burner in Germany is projected to increase quite considerably at a CAGR of 5.6% between the years of 2025 and 2032. Germany’s industry 4.0 policy involves the usage of automation, IoT, and AI technologies and intelligent industrial burners are in great demand. These burners facilitate maximum fuel utilization, real-time control, and maintenance forecasting which save money and increase productivity.

Asia Pacific

Asia Pacific is forecast that the industrial burner market in the Asia Pacific region will grow at a compound annual growth rate of 5.7% between 2025 and 2032, with a 37% share in 2025. In Japan, China, India, South Korea and other ASEAN countries, the rapid growth of industry is raising the demand for industrial burners. Such industrial development has a high payoff in the automotive, metal, chemical, manufacturing and power generation industries.

By country, India is likely to hold a composite CAGR of 6.3% for the period ranging from 2024 to 2032 regarding the Industrial Burner Segment. Considering the ever-expanding nature of the industrial sectors that India houses, a substantial need for industrial burners arises which in turn aids expansion. The manufacturing, textiles, chemicals, and cement industries contribute mostly to the high demand.

Competitive Landscape

The high-power industrial burner Market is moderately consolidated between leading players, in which the key players account for nearly 70% of the market share. The intrusion of regional players in the forecast period will make this market more competitive during the forecast period. Manufacturers are focused on the development of advanced technologies by integrating IoT-based connected technologies for remote monitoring and controlling of real-time processes of burners in industrial sectors.

Prominent players in the high-power industrial burner market are launching low NOx emission type industrial burners to support the strict regulations pertaining to a clean environment. Moreover, industrial burner component manufacturers are highly focused to supply burner management systems to boiler applications in the global market.

Recent Industry Developments

- In August 2023, Fives Group launched Hy-Ductflam, their first hydraulic 100% Duct burner. Hy-Ductflam has no emissions and thus allows manufacturers to use it without regard to the deadweight cost they would otherwise conserve. The equipment is so powerful that there is not much alteration needed in the procedure for it to be retrofitted with normal duct burners.

- In June 2023, Emerson targeted its “Floor to Cloud” portfolio along with the ASCO combustion valves and the Movicon automation systems to guarantee their safety, reliability and performance during the Thermprocess 2023 event and instill good faith in its international clients. The combination of all these factors emphasized Emerson’s large range of certified products such as solid firing equipment, safety machines, burner automation, controls, and hardware and software.

Companies Covered in High Power Industrial Burner Market

- Babcock Wanson

- Honeywell International Inc.

- Thyssenkrupp

- Alfa Laval AB

- Baltur S.p.A.

- Andritz AG

- Oilon Group Oy

- ELCO Burners

- SAACKE GmbH

- Tenova S.p.A.

- Weishaupt Group

- ZEECO Inc.

- Other Market Players

Frequently Asked Questions

The High-Power Industrial Burner market is estimated to be valued at US$1.727 billion in 2025.

The key demand driver for the High-Power Industrial Burner market is the accelerating electrification across industrial, transportation, and energy sectors, fueled by the global shift toward energy efficiency and renewable integration.

In 2025, the Asia Pacifc region will dominate the market with an exceeding 35% revenue share in the global High Power Industrial Burner market.

Among the By Fuel Type, Gas hold the highest preference, capturing beyond 52.7% of the market revenue share in 2025, surpassing other By Fuel Type.

The key players in the High-Power Industrial Burner market are Babcock Wanson, Honeywell International Inc., Thyssenkrupp and Alfa Laval AB.